When announcements were made in April and May that Galaxy Resources and Bacanora Lithium were to be acquired by Orocobre and China’s Ganfeng Lithium, respectively, I wasn’t surprised. Lithium (Li) prices were on the move and electric vehicle (EV) sales were soaring. Two months later, Ganfeng announced a proposed acquisition of Millennial Lithium, only to be outbid by Chinese battery maker CATL.

On September 15, Australia-listed ioneer ltd. announced the sale of 50% of its flagship Li-boron project to Sibanye Stillwater for $490 million. Last Friday, Neo Lithium agreed to be acquired by China’s Zijin Mining. The last two transactions are notable because the buyer has no meaningful experience in lithium. Sibanye is a PGM/gold producer and Zijin a gold-copper conglomerate.

That makes five major transactions in six months. Of those five, just two acquirers are lithium companies. This demonstrates my long-held view that multiple types of companies and investment funds could be interested in lithium assets.

Automakers should be interested in direct Li investments. In fact, analysts are perplexed as to why major OEMs have not secured major stakes in Li assets. I’m tracking 38 automakers, 30 have enterprise values >$10 billion, 10 are >$100 billion (Tesla’s enterprise value is nearly $800 billion).

Diversified miners like Teck, BHP and Vale could care, Rio Tinto already has a large Li project in Serbia. ExxonMobil and Chevron have been diversifying into solar. Royal Dutch Shell and Suncor have added wind projects to the mix. I would not be surprised to see oil/gas companies investing in Li projects this decade.

Giant commodity traders like Glencore, Mitsui anf Trafigura are getting more into battery metals. Finally, private equity, hedge and sovereign wealth funds (SWF) should care about hard asset commodity companies, especially as inflation fears mount.

There are trillions of dollars invested in SWFs alone. Unsurprisingly, three of the largest SWFs on the planet, from Norway, Kuwait and Abu Dhabi, have large allocations to oil/gas assets.

As companies and funds turn to battery metals, how many Li companies are there to choose from? I’m tracking ~110 names with market caps of at least C$10 million. Some have advanced projects, but already have strategic partners. Orocobre owns 66.5% of its project in partnership with Toyota Tsusho.

Standard Lithium is closely tied to Germany’s Lanxass, a specialty chemicals company. Czech group ČEZ owns 51% of European Metals‘ project. AVZ Minerals owns 51% of its large African project after selling 24% of it to Suzhou CATH Energy Technologies for $240 million.

How many publicly traded, pre-revenue companies host (20,000+ LCE/year), 100%-owned projects that are (at least) at prefeasibility study (PFS) stage? I come up with seven, one of which is my long-time favorite Cypress Development Corp. (CYP:TSX.V; CYDVF:OTCQB; C1Z1:FSE). There are plenty of privately owned Li projects, but most of them are presumably tied up. So, I believe there are only about 10 Li companies that have sizable, 100%-owed projects, at PFS/bankable feasibility study (BFS) stage.

Cypress has delivered a PFS, and is starting up a pilot plant. It owns 100% of a sedimentary, clay-hosted Li project in Nevada and maintains control over 100% of its prospective Li hydroxide off-take. A BFS is expected in about six months.

Of the 10 names I referred to above, some have off-take agreements in place, and/or are closely aligned with much larger players. DLE hopeful Vulcan Energy Resources has two off-take deals signed. Piedmont Lithium has an off-take with Tesla.

In addition to its 100%-owned Thacker Pass clay-hosted Li project, Lithium Americas has a 49/51 joint venture with Ganfeng, and Ganfeng also owns 12.5% of the company’s shares. Cypress hosts one of a handful of PFS/BFS stage projects that’s 100% owned, 100% open for off-take discussions and does not have a significant strategic shareholder looming over it.

Not only is M&A heating up, Li prices have been rising for over a year. The China spot price has more than quadrupled from August 2020 lows. The chart below is in Chinese yuan, 178,000 yuan = US$27,625/tonne. Since last summer, Li is one of the best performing commodities on the planet.

On October 13th, a press release describing the start of a robust pilot plant was put out. In it, CEO Bill Willoughby comments,

“The completion of the pilot plant represents a significant milestone, marking the culmination of months of work by Cypress, our consultants, and contractors. This work, under the direction of CMS and supported by the management and personnel of del Sol Refining, has resulted in a plant that embodies the research that went into our process flowsheet. The testing will be one of the larger piloting efforts to extract lithium from clay in the world, and the only one based on a chloride approach to leaching.

While the ultimate goal is to demonstrate the production of lithium hydroxide from our clay-stone resource on a larger scale, the results from the various areas within the plant, from leaching & tailings handling, to solution treatment & recycling, chemical usage and water balance, will provide the data necessary to carry the project forward to the feasibility level.”

Cypress is within about six months of both meaningful pilot plant results that can be communicated to potential strategic partners and prospective customers, AND a BFS that will help attract project funding. The de-risking over the past few years has been spectacular. A strong BFS will open the door to dozens of suitors.

With all of this good news, management is trying harder to tell its story. Two months ago, Spiro Cacos was hired as VP Investor Relations. He has signed CEO Willoughby up for at least four investment conferences through December 9. Spiro and Bill have also had over a few dozen conference calls with sell-side analysts and institutional investors.

Further ramping up marketing efforts now is very important, especially as Millennial Lithium and Neo Lithium shareholders get cashed out and are looking for places to park that cash.

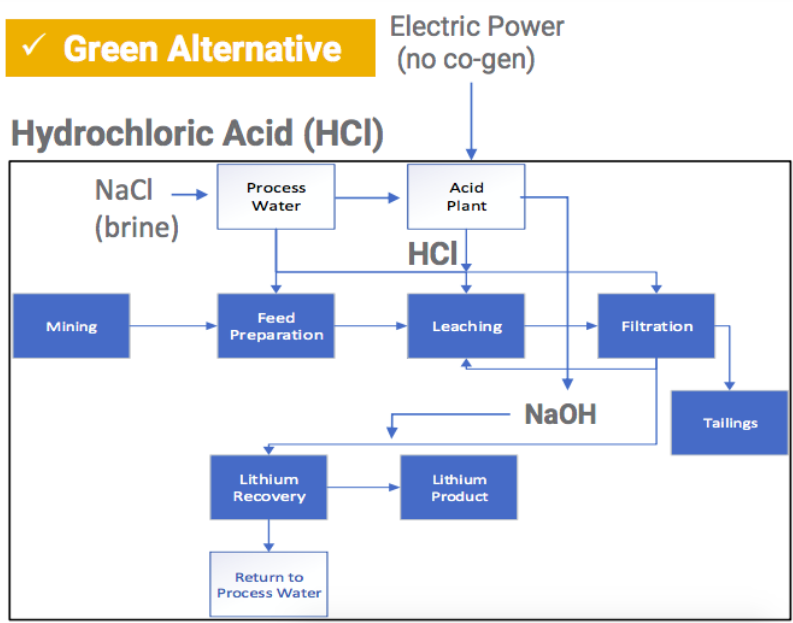

I’ve been writing about Cypress Development Corp. for nearly four years. The more I learn, the more I consider the company’s process flow sheet to be relatively low risk compared to some Direct Lithium Extraction (“DLE”) technologies on the drawing board.

With strong Li prices for years to come and increased M&A, it seems very likely (to me) that Cypress will find a strategic partner and enter commercial production in 2025 or 2026. Once the market realizes that a new Li hydroxide producer in Nevada is on the horizon, the dramatic valuation discount to peers should start to close.

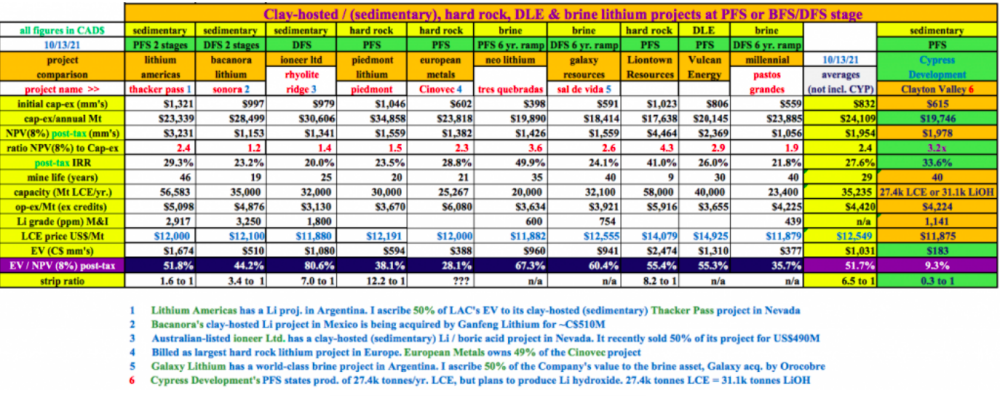

In the chart below, notice that Cypress Development’s clay-hosted project is valued at 9% of its PFS-derived, after-tax NPV(8%). By contrast, eight peers (four of which that are in the process of being acquired) have projects valued at an average of 45% of after-tax NPV(8%). Cypress is trading at an 82% discount to peers.

If peers increase in value by an avg. of 50% over the next 12 months, and Cypress were to triple in value… It would still be trading at a 61% discount. I truly believe there’s room for Cypress to run here.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares in Cypress Development Corp.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.