As the remaining days of the summer of 2021 tick away, I have always looked at Labor Day weekend as the unofficial last day of summer because after the holiday Monday, it has been “Back to School” and that was a stark reality for twenty of the first twenty-five years of my life and then for an equal period as a father of three.

Growing up in a small town, northeast of Toronto, the highlight of the summer for many kids in the region was the traditional bus trip into the city where you got dropped off at the Dufferin Gates and stood in line while hundreds and hundreds of school aged children could not wait to get inside for their annual sojourn to the mighty and venerable Canadian National Exhibition.

We all have our memories of the old “Ex” and whether it was the ancient wooden roller coaster known as “The Flyer” or the equalling terrifying “Wild Mouse,” the one event I never missed was the air show, with everything from CF-105 jets to WWII Lancaster bombers thundering across the shores of Lake Ontario, waking up not only sleeping babies but also slumbering seniors napping in the late-afternoon sun.

It was also the event that drained the last of my summer job money, because after books and clothes were paid for, there was only a few shekels left and that had to be spent on “The Midway” where carnival barkers resembling central bankers tried to guess your weight or have you toss quarters into milk bottles whose apertures were an eighth of an inch too small.

The “Ex” was that final exhaustive gasp of “summer fun” that ended with countless memories, empty wallets, and the misery that we thought (incorrectly) would arrive with the new school year. But as my geriatric memory prevails, within a few weeks it was now hockey season for some and football season for others and life went on, fairly simple but very sweet.

Looking back at the summer of 2021, it played out pretty much as I had expected, with the final lows for the miners coming in the last two weeks of August, and — while I hate it when I read some Twitter megalomaniac use the term “as predicted” — my subscribers have been forced to listen to my fishwife-like nagging and carping and whining and lecturing since May to the point where even I was starting to become irritated every time I proofread one of my missives. (You know you are risking “overkill” when you look in the mirror and are forced to utter the infamous “Shut the **** up!” line.)

I was a few days early in diving into the junior miners (by way of the GDXJ November call options), but after today’s Jackson Hole non-event, I am utterly convinced that former Fed Chairman Paul Volcker is turning over in his grave as this Fed Governor Vaudeville Act that has them all doing a different routine with one guy juggling plates while another is walking the tightrope, ever mindful of the clown tap-dancing in blackface impersonating the Canadian Prime Minister whose undergarments are trying to conceal a poorly-placed banana.

The world of finance that I have loved for the bulk of forty-five years has now officially destabilized me to the point where I am doing my Brian Wilson (Genius Beach Boy founder) impression of self-inflicted gluttony accompanied by excessive medicinal stimulants and despicable self-pity. If this financial freakshow was confined only to the U.S., I could circumnavigate around it, but because globalization orchestrated and mastered by Goldman Sacks wound up with virtually every central banker on the planet being a Goldman Sachs alumnus, the only place to hide these days, at least from my perspective, is in Russia where the national debt-to-gold ratio is the smallest in the world.

The only practical problem I have with that is that Vlad the Impaler loves money, and if you threaten to displace him as “Richest Russian Anywhere,” you will wind up wearing concrete galoshes at the bottom of the Volga River.

All of that aside, I was at once both relieved and disgusted with the results of today’s Jackson Hole “event” as gold prices behaved appropriate to “The Word of Ballanger,” and while I was a tad early this time, the only flaw in my strategy was being overly convinced that I was right, a terribly destructive attribute for any trader of any market.

As I look out to the end of the year, the statistical probability of outsized gains in global GDP remains remote at best, because the horrific COVID-19 mismanagement numbers of a year ago are now history, so the central bank “Custodians of Personal Financial Well-Being” can now deflect to the “slowing economy” as fodder for continued stimulus, which is (as I constantly harangue) the only fuel with which to propel the global banking cartel, the “politico-banco elite” that run our increasingly-fragile world.

At this point, I want to shift to a topic that has been the central theme to the 2020 and 2021 Forecast Issues and is now suddenly becoming far less abstract in deciphering future gold price movements. It all revolves around the concept of ownership and intent.

If you are a shareholder in a company, you want to know that management and the large shareholders have a fierce commitment to increasing the share price. In fact, in the “old days” before corporate buybacks became mainstream thievery, managers would do everything to ensure that the operating performance would attract new investors who would drive the stock price higher. The idea that a CEO held 40% of the issued capital of any company would be total justification to own as many shares as possible because the man in charge had significant “skin in the game.”

Well, if I apply that seam of logic to where we are in the world of gold, who, pray tell, has the most skin in the gold game? Is it the fund managers that flip our beloved gold shares around like confetti at an Italian wedding? Is it the politicians that would tell us that “monetary policy is not important”? I think that the owners of gold most highly motivated to re-price gold are the ones that own it along with chokingly-large amounts of sovereign indebtedness.

In other words, since banks back politicians and since politicians are indebted to banks, then we must look to whom the gold is pledged. Is it the average citizen? Or is it the average banker?

This is precisely where the incentivized rubber meets the agnostic road. The only country in the world that is not actively advertising their purchases of gold is the country that shows up as the largest holder — and that country is the U.S.

Let me tell you something from my days in the trading pits: There is no such thing as a “hold” rating when you are in the “slash and burn” world of trading. The Chinese are announcing that they are buyers and the Russians are trumpeting that they are buyers, while America tries actively to convince the world that the only “buy” is the U.S. dollar, and I think that “they doth protest too much”.

The 8,133 metric tonnes of gold that they are purported to hold serve little utility as an anchor to the US$30 trillion in sovereign debt when priced at US$2,000/ounce, but if one assumed a price of US$15,000 per ounce, it at least provides approximately 10% collateral to the ever-growing mountain of debt created by the U.S. Fed/Treasury Ponzi alliance.

I wrote about this in the 2020 forecast issue, but it has always been my premier reason for accumulating precious metals; I need to own whatever collateral is owned by the central banks. Central banks do not disclose their ownership of Bitcoin or copper or farmland in Iowa as collateral against their burgeoning balance sheets; they own gold, and not only do they own a lot of it, but they also continue to buy it with little or no regard for price.

With Friday’s convincing move to the upside, gold now needs to make distance from that nagging 100-dma around US$1,810 and get comfortably above that big downtrend line from a year ago at US$2,089.

There was a false start back in July just before that massive takedown into the jobs report that created a successful test of the double bottoms seen last March. In fact, it was the ferocity of the snapback that took only a couple of trading sessions to complete that sent me barreling into the Junior Gold Miner ETF, and while I was underwater for a few sessions, it is now looking like the usual bullish seasonality of September through December has arrived.

Silver continues to perform like the Toronto Maple Leafs during first-round playoff series, and while on paper one might want to own it (for all of the reasons that the Wall Street Silver gang provides), it is acting badly and remains a drag on the PMs as a group.

The gold-to-silver-ratio (GSR) has been trending higher since February having increased from the low 60s to over 75. As I have maintained since the breakout in precious metals last summer, no bull market in gold can remain intact without silver at least keeping pace and preferably outperforming.

The same goes for the shares, and when you realize that the HUI index was over 600 back in 2011 with gold at $1,908 and is trading at 41% of that peak with gold only $85 lower, it really does underscore just how despised the gold miners truly are.

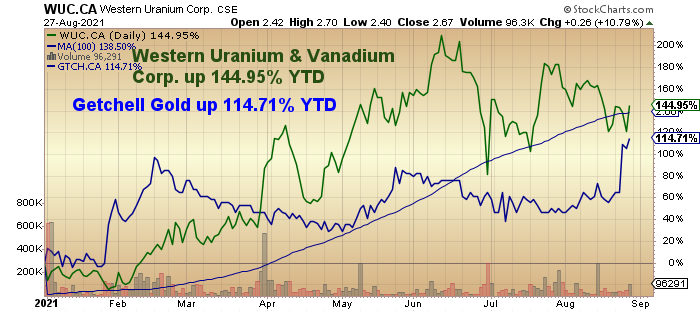

That said, the strategy of being overweight select junior developers has been fortunate with top pick and biggest portfolio position being Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB), now ahead over 114% YTD second only in performance to Western Uranium & Vanadium Corp. (WUC:CSE; WSTRF:OTCQX), sporting a 144.95% return YTD.

These types of returns are outliers of sorts when one considers that the Junior Gold Miner ETF (GDXJ:US) is down over 20% YTD with the Silver Miner ETF (SILJ:US) down 17.5%. My contention has always been to focus on companies with a proven and expanding resource that gets revalued as commodity prices and investor appetites increase, and that is exactly what is happening with these two names. Mind you, I also own a few other exploration issues where some are up and others are down, but by and large, it has been a good place to hide waiting for the end of the PM correction.

If history plays out, the next five months should see sharp rebounds in the precious metals, but the outlook for a continuation of the electrification theme that favors copper and uranium still represents a compelling story for these changing times.

The summer of 2021 can only be described as “challenged” for everyone fading the S&P 500, the NASDAQ, and the Dow Jones Industrials with the S&P making its 52nd all-time high for the year last week. It has also been rough on the silver bugs, particularly the ones that dove in headfirst during the “#SilverSqueeze” nonsense of last February. Now, before the hate mail hits my inbox, I own a few silver names and continue to believe that it will have a substantial rebound in 2022, but I am certainly fortunate to have remained underweight, given the horrid performance of the space.

For gold investors, last week ended really well and provides encouragement for a group that certainly needed it, but make no mistake, there is a great deal of technical rebuilding to get behind us before the “All clear!” siren is heard. I am constantly watching the percentage gains for gold, silver, copper, oil, and the miners, hoping to see everything outperforming gold to the upside. I will also be watching the “FedSpeak” for signs that policy is turning hostile. If they elect to tighten credit to cool off the CPI, nothing can escape the scramble for liquidity that will ensue.

It surely seems that the central bankers and the government fiscal policy geniuses are doing everything in their power to balloon out GDP by way of the money supply — in other words by reflating the system with more debt — but it only works if this new currency creation enables transactional increases that can jumpstart velocity. Otherwise, it is the Stagflation 70s all over again and not a pretty picture for all concerned.

Originally published Aug. 27, 2021.

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at [email protected] for subscription information.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]

Disclosures:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold. My company has a financial relationship with the following companies referred to in this article: Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Getchell Gold. Please click here for more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold, a company mentioned in this article.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.