Copper prices bounced back through July, following a rise in U.S. demand and diminishing influence of Chinese strategic reserve releases on the overall market. A global copper supply deficit is expected to widen through next year and could be exacerbated by the passage of a U.S. infrastructure bill, as well as the threat of mining industry strikes and a new political regime in Chile, the world's top copper-producing nation.

Related ETF/ETN & Stocks: iPath Series B Bloomberg Copper Subindex Total Return ETN (JJC), Global X Funds – Global X Copper Miners ETF (COPX), Freeport-McMoRan Inc. (FCX)

Over the last few weeks, copper futures have rebounded strongly from the $4.20/lb level to as much as $4.59/lb. As of yesterday's close, the red metal had eased to $4.43/lb, well below its 2021 high of $4.76/lb, but still more than 52% higher than this time last year.

Copper's strong July was capped off by investment bank Goldman Sachs reiterating its bullish call for a copper price of $11,000 a tonne (just below $5/lb) by the end of the year and $11,500 by this time next year. As Mining.com notes, Goldman expects tight supply and a bottleneck for primary metal production in China, reinforcing its projection for a significant 430,000-tonne refined deficit in the second half of the year.

To receive all of MRP's insights in your inbox Monday–Friday, follow this link for a free 30-day trial. This content was delivered to McAlinden Research Partners clients on August 3.

Goldman also projects a 200,000-tonne deficit next year, and also halved its projected surplus for 2023 to 129,000 tonnes "after which open-ended deficits start," driven by rising electric vehicle adoption and increasingly insufficient Chinese strategic reserves.

Deficit Expands, Chinese Reserve Releases Cause Muted Reaction

According to the International Copper Study Group, the global market for refined copper showed a 75,000-tonne deficit in April, expanding significantly from a 13,000-tonne deficit in March. Though the copper market remains in a thinning surplus of about 69,000 tonnes through the first 4 months of 2021, that's largely due to demand still being in a recovery phase from the COVID-19 pandemic.

As Argus Media reported in May, Chilean copper agency Cochilco expects the refined copper market to register a deficit of 145,000 tonnes by the end of the year. The firm also sees strength in the copper market persisting even longer than previously expected, significantly raising their projection for 2022's average price to $3.95/lb, up from previous estimations of $3.00/lb.

The Chinese government spooked investors earlier this summer when it announced it would be releasing industrial metals from its national reserves to curb commodity prices, but as that strategy has unfolded fears have faded significantly.

China injected a total of 50,000 tonnes of copper into the market via two auctions last month, the second of which actually ended up boosting prices since it was much less than expected. While much was made about the Chinese government's tough talk, Goldman Sachs notes that 50,000 tonnes of copper is equivalent to approximately 36 hours of Chinese copper consumption.

Demand Growth Shifts to US, Gearing up for Infrastructure Drive

Though Chinese import volumes have slid 10% from the first half of last year's record import tally of 4.67 million tonnes, US demand has just started picking up.

That comes as Chicago Mercantile Exchange stocks have sunk to 45,885 tons, down by 31,700 since the start of January. Meanwhile, Reuters reports that funds have slashed their bear bets from 44,978 contracts in June to just 22,210 contracts, according to the latest Commitments of Traders Report. That has lifted the collective net long to 46,137 contracts.

"The realities of the current logistical bottlenecks have meant that U.S. copper imports have so far not been enough to meet demand, and it does not look like it will get materially better until after September," according to Citi analysts who estimate that apparent U.S. copper consumption jumped by 22% year-on-year in the January-May period.

That rise in demand is especially pronounced in expanding U.S. premiums for copper. Per Bloomberg, New York traders were paying as much as $250 a metric tonne more for Comex copper than metal traded on the London Metal Exchange at the end of July, the widest spread since 2011.

That may only be the beginning of a new wave of demand set to sweep the U.S. when a $1 trillion infrastructure bill finally gets passed. Though it has taken some time to hammer out, and may take another week to finally finish up amendments before the U.S. Senate leaves for summer recess, it appears increasingly likely that the bill will eventually pass both houses of Congress, driving $73 billion of funding toward modernizing the copper-rich electric grid, including $7.5 billion to develop electric vehicle charging stations across the country—a move likely to hasten the adoption of electric vehicles.

As MRP has noted, electric vehicles take around 83 kilograms of copper on average, while charging points need 10 kilograms of copper per unit. A team of Jeffries analysts, led by Christopher LaFemina, expects copper demand for electric vehicles will rise to 1.7 megatons in 2030 from 170 kilotons in 2020.

Strike Could Shut World's Largest Copper Mine

One final catalyst that could play a significant role in a copper comeback is the threat of a prolonged strike at Chile's La Escondida, the world's largest copper mine, solely responsible for almost 5% of the world's supply of the metal. Union workers have already rejected owner BHP Group's final wage offer in voting last week by overwhelming majority of 99.5%.

The Wall Street Journal notes that miners by law must continue to work during a period of obligatory mediation by the government for a period of up to 10 days, so a strike isn't a done deal, according to some analysts. If no deal is struck, however, a walkout of miners could last some time. When Escondida workers walked off the job in 2017, they didn't return for 44 days.

As Bloomberg notes, two other smaller mines—Codelco's Andina and JX Nippon Mining & Metals' Caserones—are in the same situation. Chile, the world's top copper-producing nation has already seen output fall by 2% through the first four months of the year.

As MRP has previously noted, this rising labor movement coincides with the rise of Chile's Communist party and other left-wing independents, who overcame Chile's ruling coalition in nationwide elections last May to choose 155 delegates who will write a new constitution for the nation. October's general elections in the country could mark a further political shift to the left for Chile. Copper-rich Peru has experienced similar political intrigue as Pedro Castillo of the socialist Free Peru party was elected president earlier this year.

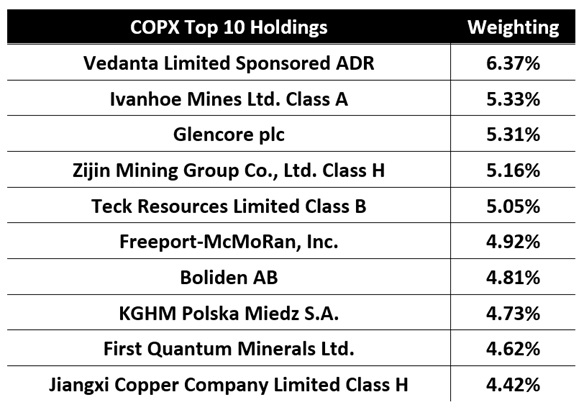

For Freeport-McMoRan Inc. Chief Executive Officer Richard Adkerson, the outcome of South America's political machinations is still up in the air. But he did note that the shift appears to be supportive of higher prices with plans for expansion becoming more uncertain in both Chile and Peru, accounting for a combined share of 40% of global copper production.

The unimpeded expansion has become much more critical in recent years. Wall Street Journal cites CRU Group, a commodities consulting firm, which estimates production from existing copper mines will peak in 2023, with a shortfall emerging in the middle of the decade and deepening unless new projects advance.

For Investors

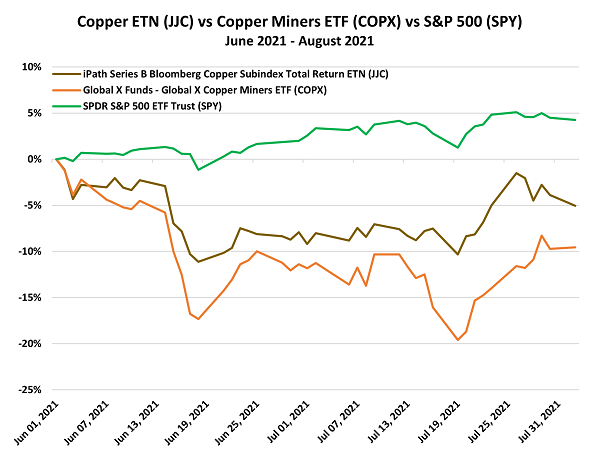

MRP will continue to monitor developments in copper and other metals markets. Less than two months ago, MRP suspended our long themes on copper and copper miners.

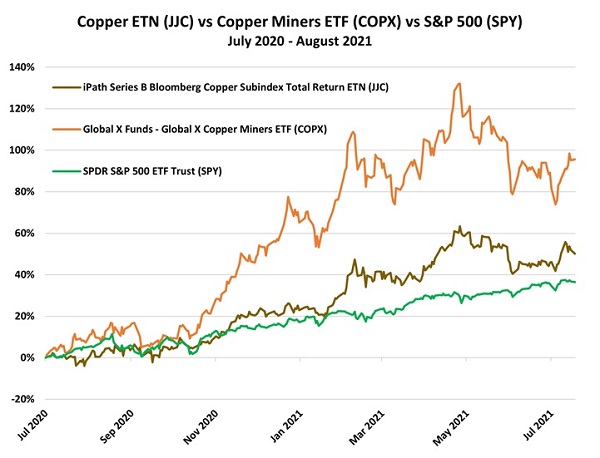

Over the lifetime of those themes (each being active from July 16, 2020 – June 20, 2021), the iPath Series B Bloomberg Copper Subindex Total Return ETN (JJC) and the Global X Copper Miners ETF (COPX), have returned +41% and +77%, respectively, over the life of the theme. Each of those has outperformed the S&P 500's return of +31% over the same period.

Originally published August 2, 2021.

McAlinden Research Partners (MRP) provides independent investment strategy research to investors worldwide. The firm's mission is to identify alpha-generating investment themes early in their unfolding and bring them to its clients' attention. MRP's research process reflects founder Joe McAlinden's 50 years of experience on Wall Street. The methodologies he developed as chief investment officer of Morgan Stanley Investment Management, where he oversaw more than $400 billion in assets, provide the foundation for the strategy research MRP now brings to hedge funds, pension funds, sovereign wealth funds and other asset managers around the globe.

[NLINSERT]

Disclosure:

1) McAlinden Research Partners disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

McAlinden Research Partners:

This report has been prepared solely for informational purposes and is not an offer to buy/sell/endorse or a solicitation of an offer to buy/sell/endorse Interests or any other security or instrument or to participate in any trading or investment strategy. No representation or warranty (express or implied) is made or can be given with respect to the sequence, accuracy, completeness, or timeliness of the information in this Report. Unless otherwise noted, all information is sourced from public data.

McAlinden Research Partners is a division of Catalpa Capital Advisors, LLC (CCA), a Registered Investment Advisor. References to specific securities, asset classes and financial markets discussed herein are for illustrative purposes only and should not be interpreted as recommendations to purchase or sell such securities. CCA, MRP, employees and direct affiliates of the firm may or may not own any of the securities mentioned in the report at the time of publication.

Charts and graphs provided by McAlinden Research Partners.