There's been a tremendous amount of attention on gold juniors over the past year, and rightfully so. Gold at $1,846/oz is up +27% from 2020's March low (down from an all-time high of $2,070/oz. last summer).

Silver is up even more. However, I bet few readers know that copper ("Cu") at $3.72/lb (near an 8-year nominal price high) has soared +87% from its 52-week low. In the midst of a global pandemic, Cu has been one of the best performing commodities.

Copper fundamentals are strong, not just for this year and next, but for a long time to come. Goldman Sachs believes the world is entering a multi-year commodities super-cycle.

A renewed push for global decarbonization (with the U.S. back in the game and climate change increasingly undeniable) is one of several key factors pointing towards a new super-cycle thesis.

Copper fundamentals are strong for decades to come .

The 2020s will be remembered for massive deficit spending/debt issuance, which is bullish for precious metalsbut also for base metals. Tens of trillions of dollars will be spent on giant Cu-intensive infrastructure and green energy projects. Renewable energy projects require 5x the Cu of fossil fuel plants.

The paradigm shift to vehicle electrification will boost Cu demand as well. EVs require 4x the Cu of internal combustion engine cars. Not to mention that Cu soon to be needed for 18-wheelers, delivery vans, construction, mining, military vehicles and equipment, ocean-crossing container ships, etc. Prodigious quantities of Cu will be required to build a vast battery charging infrastructure to make it all work.

Strong Cu demand is all but assured, but global supply is increasingly precarious. Many of the largest Cu mines are also the oldest and deepestsome date back to the 1800s.

Mined Cu grades have been in decline for decades, as has the number of new, blockbuster Cu discoveries. Several well-known open-pit mines are now operating at grades at or below 0.25% Cu. That's US$19/tonne rock.

.but copper supply is increasingly uncertain

Everything I've written points to one critical takeaway. Higher Cu prices are necessary to incentivize mining companies to invest billions of dollars, over 1020 year periods, to develop reservesand then plan, permit, fund and build mines, processing plants and tailings facilities.

Adjusted for inflation, the all-time high Cu price breached $6/lb in the mid-1970s. In 2011 it was >$5/lb. The 2020s will likely see a new record high price. That's great news for up-and-coming Cu juniors with (prospective) mines opening this decadenot so good for old, high-cost, low-grade mines nearing end of life.

Chile is by far the leader in Cu production, accounting for 28% of the world's mined copper in 2020. But, cost inflation and lower grades are taking a toll. Obtaining water to operate the mines, many of which are at elevations above 3,500 meters, is tremendously challenging, costly and time consuming.

Peru is the second largest Cu producing country, it delivered 12% of last year's mined copper. It too has mines at high and very high! elevations (>4,000 meters). Northern Peru is widely considered to be more difficult for companies to do business in due to opposition to mining in some areas.

However, in the central and southern parts of the country, which in many cases have less population density, mine operations are better tolerated and permitting is easier to achieve.

In the most recent Fraser Institute Mining Survey, Peru ranked higher than 7 of 12 Canadian provinces and (also) 7 of 12 U.S. states. Overall it ranked near the top of the second quartile.

Chile and Peru (a combined 40% of 2020 mined Cu) have been great jurisdictions to work in. Looking forward, both countries will likely remain Cu powerhouses, but fresh new mines will lead the way as aging, depleted mines shut down.

A newly listed company that's well positioned with two 100% owned, potentially world-class copper porphyry projects in Peru is Element 29 Resources Inc. (ECU:TSX.V). Both projects are at <2,500 meter elevation, a level that does not require specialized equipment as is often the case for mines at elevations >4,000 meters.

Element 29 Resources; advancing two promising Cu projects in Peru

Unlike for a growing number of properties in Chile, water is not expected to be an issue for Element 29. In fact, one of the two projects is close to a river. Both are outside of northern Peru, in the more mining friendly southern and central parts of the country. And, both are <100 km from the coast.

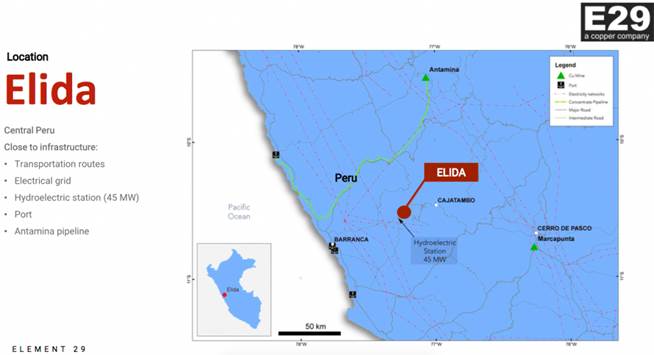

The Elida property hosts a recently discovered (2013), untested copper-moly (Cu-Mo) porphyry cluster located ~170 km northwest of Lima, and ~85 km from the coast. Elida sits in a highly prospective porphyry belt in central Peru.

The property consists of 28 mining concessions totaling 19,210 hectares. It's a cluster of at least four porphyry centers, with only the central target drilled.

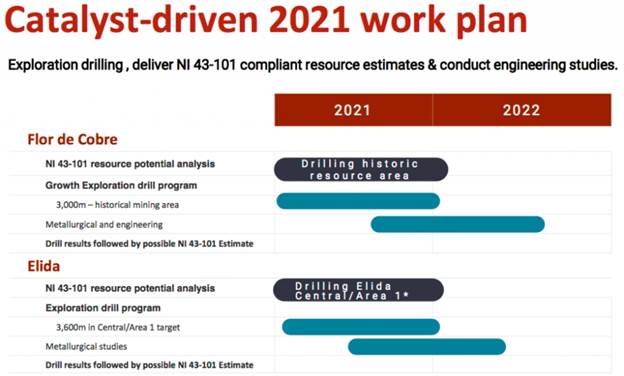

The initial focus at Elida is on a sizable 750 meter by 600 meter central porphyry target. Management is pursuing a conceptual exploration target of 200 to 500M tonnes, grading between 0.35% to 0.45% Cu plus 0.03% to 0.05% Mo plus 3.5 to 4.5 g/t Ag.

This is no pie-in-the-sky three-year goal. Element 29 is funded to deliver a NI 43-101 resource that could be >200M tonnes by Q1 2022. Management already has 18 holes, nearly 10,000 meters of historical drilling. The team needs to tighten up the spacing. A 3,600 meter infill drill program is expected to start in April.

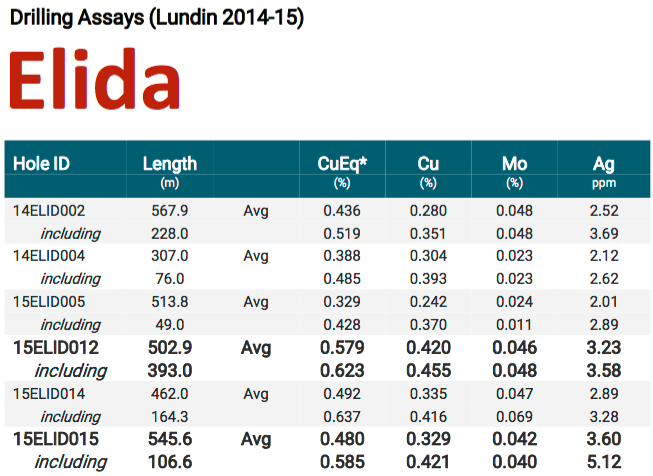

In 201415, Lundin Mining completed a modern 18-hole / 9,880 meter drill program that intersected a robust porphyry system. All holes hit Cu-Mo-Ag mineralization. Most holes ended in mineralization, (some holes in moderately high-grade mineralization) meaning that the system remains open at depth.

Note: Drilling and sampling was carried out by Lundin Mining Peru SAC (2014-2015). ALS-Global Laboratories in Lima, Peru, analyzed the half-core by ME-ICP41, which includes 35 elements using an Aqua Regia digestion ICP-AES analysis and gold fire assay with an AA finish (Au-AA23). The over limits underwent ME-OG46 for ore grade elements using an Aqua Regia digestion. Reported widths are drill core lengths; true widths are unknown at this time. Assay values are uncut. The calculated Copper Equivalent (CuEq. (%)) grade was used to determine the significant intervals (>0.20% CuEq. and >30 m core length, with higher grade intervals using a >0.40% CuEq. and >15m core length). *CuEq. = Cu(%) + Mo(%) x 2.667 +Au (ppm) x 0.6320 +Ag (ppm) x 0.0097 (no metallurgy has been completed at Elida, therefore no metallurgical recovery was applied in the copper equivalent formula). Cu Price= $3.00 USD/lb, Mo Price = $8.00 USD/lb, Au Price=$1,300.00 USD/oz, Ag Price=$20.00 USD/oz. The numbers correspond to Table 4 in the Elida Technical Report (refer to www.sedar.com for the full report).

The best assay at Elida was from hole DDH-15ELID012, which hit a wide intercept of 503 m of 0.42% Cu plus 0.046% Mo plus 3.2 g/t Ag = 0.58% Cu Eq., including 393 m of 0.455% Cu plus 0.048% Mo plus 3.6 g/t Ag = 0.62% Cu Eq.

Drilling confirmed very significant areas of potential mineralization. Management believes there is excellent exploration upside. And, preliminary metallurgical studies are planned with existing core taken from prior drilling done by Lundin. In my view, this is a top-quartile global Cu exploration project.

From Element 29's NI 43-101 technical report on Elida:

The property and surrounding areas are mostly uninhabited. Land in the immediate region is not being used. Engagement with locals has been ongoing for years. A community agreement that was set to expire in 2020 was successfully renewed until 2025. Management anticipates few, if any, difficulties in obtaining surface and water rights.

I'm placing a great deal of faith in this leadership team. The chairman, Richard Osmond; CEO, Brian Booth; and VP of Exploration, Paul Johnston have worked extensively in Peru and have considerable large and small mining company experience. The team includes notable experts in copper as well, like Director Peter Espig.

President and CEO Brian Booth (P.Geo) is very impressive; he has over 20 years with mining giant INCO and has held CEO and director positions at other junior miners and is currently a director at SSR Mining and GFG Resources.

Flor de Cobre, a second potential company-making asset

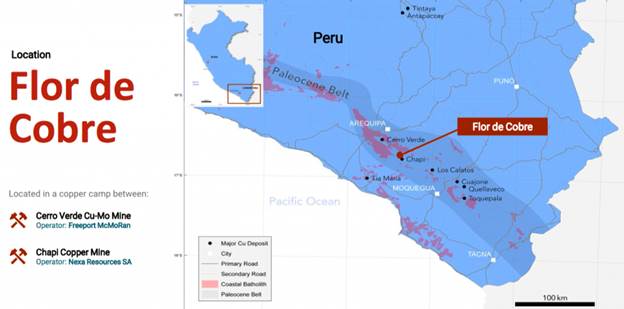

Second, but not last, Flor de Cobre ("Flor") is an 1,800 hectare property (+127 ha under option) in the Southern Peru Copper Belt. It hosts an under-explored, higher-grade, small past-producing copper mine in southwestern Peru.

The project sits 45 km southeast of the country's second largest city (Arequipa). It's 30 km southeast of the fifth largest copper mine in the world, Freeport's Cerro Verde, and just 7 km northwest of the Nexa Resources' Chapi mine. Flor is wide open at depth and along strike to the northeast.

In addition to Cerro Verde and Chapi, multiple operating mines and deposits of >10 Mt of contained Cu are in the belt, including Cuajone and Toquepala (Southern Copper) and Quellaveco (Anglo/Mitsubishi).

The Flor area hosts a porphyry copper-molybdenum (Cu-Mo) system called the "Candelaria Porphyry," with characteristics similar to other porphyry deposits in the belt.

One or more Cu enrichment zones support high-grade potential

The Candelaria zone was outlined by two drill campaigns in the 1990s and includes an enriched Cu zone with pockets of >1% Cu. The dimensions are 850 m x 1,000 m. Rio Amarillo later produced an initial resource estimate based on drilling that covered ~488 ha, and was based on 40 diamond drill holes. {See page 10 of Corporate Presentation}.

In another area, there's evidence to suggest that the Atravezado target could be a second Cu-Mo porphyry system, bigger than Candelaria at roughly 1.2 x 1.0 km. A geophysical resistivity signature at 400 m depth is similar to other porphyries in the belt, making it a compelling target for testing.

In 1994, there were 60 drill holes completed at Flor, totaling 5,960 meters. The best hole, K-008, returned 124 m at 1.37% Cu (from an enriched Cu zone). Preliminary metallurgical test work was completed to investigate recovery by leaching and flotation. The reported Cu recovery was 89.5%.

Phelps Dodge followed that year's program with 36 holes totaling 5,882 meters. Drill hole CD-128 returned the best intercept, with 40 m at 1.0% Cu.

Well funded to advance two top-quartile Cu exploration projects

Flor has higher-grade potential, but if Elida demonstrates 200M+ tonnes at a Cu Eq. grade of 0.40%-0.45%, then Element 29 Resources (TSX-V: ECU) could be sitting on two 100%-owned, top-quartile, (global) Cu exploration projects.

Both projects are funded through most of the year. New resource estimates, then third-party Preliminary Economic Assessments ("PEA") in 2022 could re-rate this exciting new story, especially if the Cu price moves north of $4/lb. Readers take note, the current price of $3.72/lb is just 7% away from that important $4/lb threshold.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Element 29 Resources., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Element 29 Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Element 29 Resources was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events and news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.