COVID-19 has vaulted telehealth/telemedicine into the big leagues. Six months into this global pandemic and experts now contend the industry is years ahead of where it would have been. Yet by any measure, telehealth is still in its infancy. Make no mistake, this will become a multi-trillion-dollar industry.

Regulators and insurance companies were forced to rapidly understand and support telesessions in March/Apriland they did. There's no turning back to the way healthcare used to be administered.

Telehealth: Still Early Days of a Multi-Trillion-Dollar Industry

Going to the doctor is a hassle and an unwelcome expense, but a necessary evil. By car, taxi or public transport, finding parking, paying tolls or bothering friends or family for a ride. A 45-minute appointment can turn into a two-hour annoyance. Not to mention the real risk of contracting or transmitting a serious disease, virus or flu.

With telesessions, patients can avoid missing work or school. They can save time and money. And, not having to drag children to the doctor's office? Priceless. Less spread of disease is great news for everyone. A true societal benefit. . .a positive externality.

There are dozens of entities, large and small, well-established and new entrants, trying to catch the telehealth wave. One that I wrote about in July is CloudMD Software & Services Inc. (DOC:TSX.V; DOCRF:OTCQB; 6PH:FSE).

Is CloudMD a Good Way to Invest in the Telehealth Craze?

CloudMD shares have soared since my initial article, in which I pointed out it was trading very cheap compared to peers, in large part due to an overhang of a private placement becoming free-to-trade.

Following the SaaS (software as a service) business model, CloudMD has the potential to be a stable (low churn), rapidly growing company, with long-lasting, recurring revenue. Management is prudently pursuing a hybrid approach to healthcare delivery in Canada, and increasingly in the U.S.

In addition to telehealth, the team continues to acquire, own, optimize and operate conventional healthcare clinics. I believe this approach encapsulates the most efficient and cost-effective way to gain market share. CloudMD has about $30 million in cash (some of which is earmarked for announced acquisitions) and is overflowing with new deals to consider.

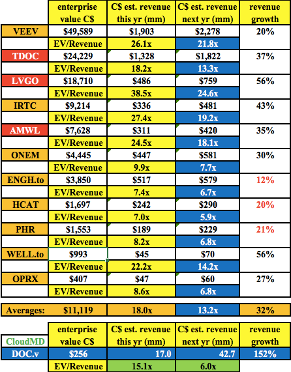

Although the company's valuation is not as cheap as it was two to three months ago, it's trading at less than half the average (enterprise value [EV]; market cap + debt cash/2021 consensus revenue) multiple (6.0x), versus an average (13.2x) multiple of 11 peers in the chart below.

Valuations Continue to Expand; Revenue Growth Critically Important

Readers might notice a new name, American Well Corp. (Amwell; AMWL:NYSE), which listed in the U.S. earlier this month. I estimate it trades at 18.1x 2021 expected revenue. This is an important comparable peer as it just came to market, benchmarking valuations in the space.

Another recent development of note, two large, blue chip names in the sector, Teladoc Health Inc. (TDOC:NYSE) and Livongo Health Inc. (LVGO:NASDAQ), announced their intention to merge. The combined company would trade at 16.6x next year's pro forma (combined) revenue.

This month Loblaw invested $75 million for a reported 2025% stake in private telehealth start-up Maple Corp. According to a recent article in the Global and Mail, Maple's run-rate annual revenue is $25 million. Therefore, Loblaw's investment values Maple at $300$375 million, or about 1215x revenue. Presumably, Maple will execute an IPO (initial public offering) at a higher valuation.

So, that's four bellwether names that have recently been marked-to-market (via an IPO, merger and PE investment). Two other large players, Veeva Systems (VEEV:NYSE) and iRhythm Technologies (IRTC:NASDAQ) are trading at 2021e EV multiples of 21.8x and 19.2x. CloudMD is trading at a 6.0x multiple.

Tsunami of M&A Likely to Continue for the Next 23 Years

The telehealth firm most often compared to CloudMD is WELL Health Technologies Corp. (WELL:TSX.V; WLYYF:OTCMKTS). It trades at a 14.2x multiple and analysts expect it to enjoy revenue growth of 56% in 2021. WELL has an EV that's four times larger than CloudMD's, yet based on respective growth rates, the two companies could generate about the same annual revenue in 2023.

Interestingly, the four companies with the largest EVs trade at an average EV/2021e revenue multiple of 19.7x, while the four smallest trade at 8.3x. That's a huge difference. Clearly, the bigger players have ample room to make highly accretive acquisitions. They also benefit from much cheaper costs of capital to fund mergers and acquisitions (M&A).

Blockbuster revenue growth makes CloudMD a standout, yet it's trading at an EV/2021e revenue multiple that's below that of the slower growth peers. The three lowest growth names have an average growth rate of 17%, versus CloudMD at +152%.

When I get questions about CloudMD, they typically fall into two buckets. First, isn't the company too small to be compared to the likes of TDOC or VEEV? No, in the telehealth ecosystem there are large, medium and small players. M&A will take care of the small and mid-sized names.

To be clear, not all telehealth companies will be acquired. In fact, some will not survive. Only the bestsay, the top quartilewill be keenly sought after. Which companies? Those that have 1) demonstrated strong revenue growth, 2) robust acquisition pipelines, 3) innovate platforms (like mental health) and 4) a lean, sustainable, high-tech business model.

CloudMD is not a target high on the list of majors like TDOC, but dozens of healthcare-related players are aggressively looking for well-run operations. Everyone needs to show rapid growth (organically or via M&A) in order to get acquired themselves!

CloudMD an Aggressive Acquirer Now; a Takeout Target Next Year?

The second concern I hear: CloudMD is not yet EBITDA (earnings before interest, taxes, depreciation, amortization) positive. While certainly true, readers should note that (8/11 = 73%) of the peers in the chart had negative EBITDA on a trailing 12-month basis. This is common in new, high-growth industries. Having said that, I believe CloudMD will be EBITDA-positive sooner than some of the larger companies.

Furthermore, as a lean operator, the company could, over time, generate good EBITDA margins (20%+). Much faster revenue growth and the prospect of attractive margins make CloudMD a prime takeout candidate.

One of the primary metrics that investors and prospective acquirers focus on in new industries is revenue growth. Notice that the consensus growth rate in 2021 for the 11 peers is 32%. CloudMD's revenue growth is forecast to be +152%, albeit from a smaller base. If revenue were to reach the consensus estimate of $42.7 million, that would be >500% above 2019's level.

As mentioned, the consensus revenue estimate in 2021 is $42.7 million (including acquisitions announced through Sept. 29). However, that does not include $15$20 million of additional revenue generating assets to be acquired in coming quarters, which will drive revenue estimates higher.

Although analysts try to capture synergies and cross-selling opportunities that accrue from M&A, it's difficult to model. Therefore, combined with upcoming (funded) M&A, there could be considerably more than $42.7 million in revenue next year.

Without trying to peg a number for potential synergies and cross-selling, suffice it to say that revenue growth >150% in 2021 (from a base of at least $16 million) is already head-and-shoulders above peers.

Conclusion

Readers are reminded of the low correlation telehealth stocks should have to the overall market. If, as I fear might be happening, the COVID-19 situation gets worse (again) in the U.S. and around the worldthat could be terrible for the stock market, but not necessarily bad at all for telehealth.

Investors can play it safe by investing in TDOC, AMWL, VEEV, or reach for higher returns, with commensurately higher risk. I can't predict the future, but if the telehealth majors were to rise by 50% in the next year, I think a company like CloudMD could possibly rise by a lot more.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

Disclosures: The content of the above article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about CloudMD Software and Services, including commentary, opinions, views, assumptions, reported facts, calculations, etc., is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, professional trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of CloudMD are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, CloudMD was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events and news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of CloudMD, a company mentioned in this article.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.