Ayawilca project; drilling location

1. Introduction

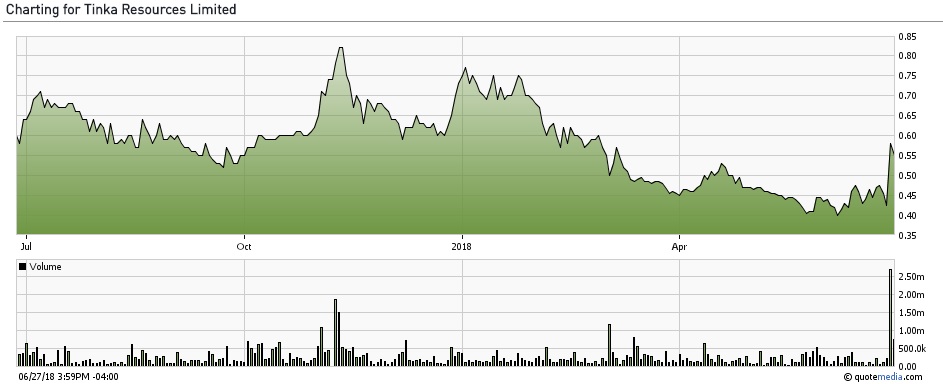

Investors had to wait longer than expected for a big hit, but this week Tinka Resources Ltd. (TK:TSX.V; TLD:FSE; TKRFF:OTCPK) proved that looking for substantially more mineralization first instead of preparing a Preliminary Economic Assessment (PEA) is a viable strategy. The latest hole returned an amazing intercept of 10.4m grading 44.0% zinc (Zn) at West Ayawilca, and what is particularly interesting is that management seems to be verifying their new theory on Ayawilca structural controls of geology with this result. The share price reacted accordingly, with an impressive 36% jump and 2.7M shares traded volume on the day of the announcement:

Share price Tinka Resources; 1-year timeframe; source tmxmoney.com

Obviously lots of investors were impressed, and in my view rightly so, as this news could indicate potential for more and higher-grade tonnage than anticipated. It seems a bottom has formed at CA$0.40-0.45/share, even a bit lower than my forecasted C$0.46-0.48 from the April update, as the selling took longer than expected. Fortunately, this seems behind us now considering the massive volume, also against neutral to slightly negative sector sentiment. The potential implications for the resource and economics can be read in this article.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US dollars, unless stated otherwise.

Please note: the views, opinions, estimates or forecasts regarding Tinkas performance are those of the author alone and do not represent opinions, forecasts or predictions of Tinka or Tinkas management. Tinka has not in any way endorsed the information, conclusions or recommendations provided by the author.

2. Exploration Results

It was a pleasant surprise for Tinka Resources and investors to see an impressive intercept like 10.4m @44.0% Zn being returned by step-out hole A18-129, as part of the current drill program at the Ayawilca project in Peru. Management started focusing more on expanding the high-grade West and South zones as Zone 3 didn't return the results that were hoped for so far, and this seems to be the right move.

Despite all the noise about the latest and pretty large CA$16.2M financing in March-April of this year, I am convinced that Tinka management knows very well what it is doing on the exploration side of things, and it shows so far. It is also always interesting and inspiring to talk to CEO Carman, and hear him elaborating about different geological concepts that might be tested. The Ayawilca deposits don't look very straightforward, but Carman and his team seem more than able to track them down.

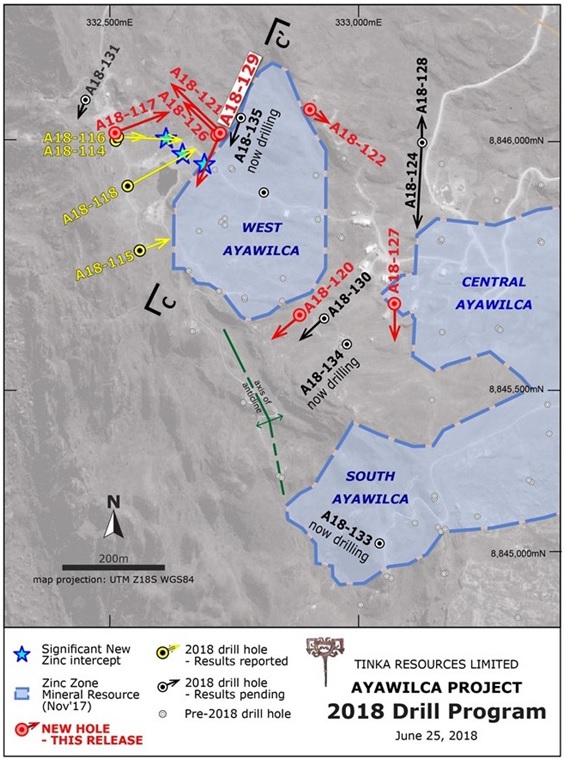

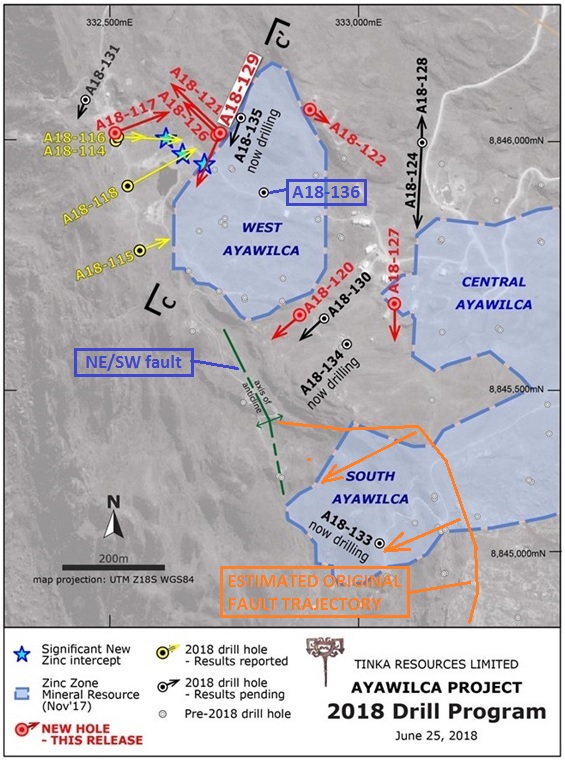

Let's have a look at the latest drill result first, as mentioned in the latest news release. Six holes were reported from the West Ayawilca area (holes A18-117, 120 to 122, 126, 129) and one from the Central area (A18-127).

Key Highlights of the West Ayawilca Area:

Hole A18-129:

- 11.9 meters at 39.6% zinc, 0.8% lead, 45 g/t silver & 761 g/t indium from 339.4 meters depth, including

10.4 meters at 44.0% zinc, 0.4% lead, 43 g/t silver & 869 g/t indium from 340.6 meters depth; - Shallower intercepts in A18-129 include:

- 21.2 meters at 9.0% zinc, 0.1% lead, 13 g/t silver & 53 g/t indium from 260.0 meters depth, including

4.2 meters at 19.2% zinc, 0.1% lead, 17 g/t silver & 186 g/t indium from 277.0 meters depth; and - 6.5 meters at 11.0% zinc, 0.1% lead, 8 g/t silver & 52 g/t indium from 290.5 meters depth.

An average grade of 44.0% Zn in a substantial intercept in sulfides is world class, and is only encountered in Tier I deposits like Arizona Mining Inc.'s (AZ:TSX) Taylor deposit (up to 31.7%Zn) and Ivanhoe Mines Ltd.'s (IVN:TSX) Kipushi deposit (their average grade is even a freaky 34.9% Zn, twice as high as the next highest average grade zinc deposit, according to Wood Mackenzie). As this is a step-out hole, drilled about 50m west of the boundary of the outlined West Ayawilca ore body, it is interesting to see that the existing ore body extends to the west via the shallower intercepts, which are at the same depths, and have very decent width and grade as well.

- Other significant recent drill intercepts include:

Hole A18-117: - 7.8 meters at 8.1% zinc, 5.1% lead & 183 g/t silver from 94.0 meters depth*.

- Hole A18-122:

- 2.4 meters at 14.9% zinc, 0.3% lead, 25 g/t silver & 163 g/t indium from 351.3 meters depth.

- Hole A18-126:

- 1.0 meters at 23.7% zinc, 24 g/t silver & 30 g/t indium from 101.1 meters depth*; and

- 1.7 meters at 18.9% zinc & 28 g/t silver from 111.5 meters depth*; and

- 8.7 meters at 3.9% zinc, 1.4% lead, & 117 g/t silver from 235.7 meters depth.

There is a lot of consistency in the mineralization throughout the property, as almost any mineralization shallower than say 300m is relatively narrow (<10m) in width/thickness, veiny and hosted in sandstone. Hole A18-120 and A18-121 weren't mentioned in the highlights, so I assume these results weren't economic. As can be seen at the map of the latest drill collar locations, (very) economic results like A18-126 and A18-129 can be located very close to uneconomic results like A18-121, so a lot of drilling is needed to precisely define mineralized boundaries:

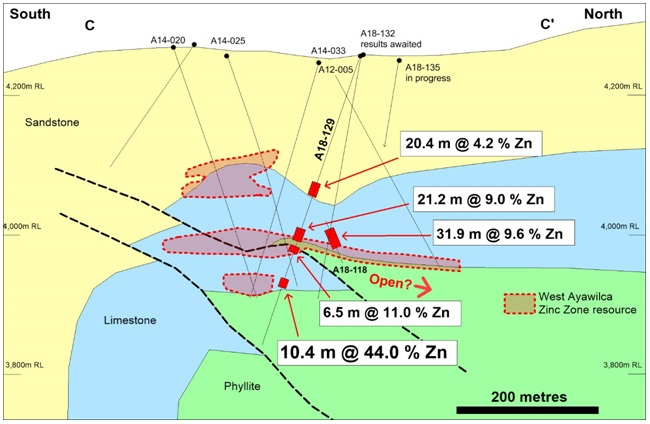

It appears that A18-120 just remained outside the mineralized horizon, but when we start looking at the C-section, it becomes clear what the geologists were looking for: a stacked system of two or more potentially layered limestone host rock. They came to this concept after analyzing the cores more in detail on structural controls, and discovered a few low-angle thrust faults west of West Ayawilca, in the large, semi-vertical North-South trending fault area (which runs west of West and South Ayawilca), potentially capable of laterally (horizontally) displacing the mineralized limestone:

This is why hole A18-129 proved them right. As CEO Carman stated in the news release:

"The exceptional zinc grade in hole A18-129 is very exciting as it confirms Ayawilca mineralization can be very high-grade, while a repetition of the favorable Pucara limestone opens up a new exploration target at depth and also down-plunge of the new intercept. Previously, it was thought that the phyllite metamorphic rock represents a 'floor'to the zinc mineralization. Past drill holes were typically stopped a few meters into the phyllite, and some holes at Ayawilca may have been stopped prematurely.

"The objectives of the drill program are to find additional high-grade zinc resources, as well as to improve the geological understanding of the Ayawilca deposit, which is evolving as more holes are drilled. The three-rig drill program is now focused on testing extensions of the zinc resources at West and South Ayawilca, including deeper repetitions of the limestone-hosted replacement mineralization, as well as possible connections of these areas with Central Ayawilca."

It must have been a good feeling as a geologist to see your theories confirmed with such strong results. On a side note: the holes A14-020 and A14-033 appeared to be ending in a mineralized envelope, apparently located at around the same depth as the new, spectacular intercept, which intrigued me. After looking into the corresponding news releases of 2014 and 2015, it showed that the deepest intercepts of these two holes were situated a good 70m more to the surface compared to A18-129:

"A14-20: 2.2 metres at 21.0% zinc from 164 metres depth; and 34.15 metres at 5.3% zinc from 179.85 metres depth, including 12.0 metres at 10.5% zinc from 179.85 metres depth; and 42 metres at 4.3% zinc from 268 metres depth; A14-33: 77.1 metres at 4.0 % zinc from 268.0 metres depth, including 8.8 metres at 13.5 % zinc from 270.9 metres depth. . ."

So according to my view, and if these two holes ended in phyllite basement rock, the high-grade intercept of A18-129 needs to be drawn in the section at greater depth, and the border between limestone and phyllite needs to be drawn a lot more angled, trending down to the right (eastern direction). This could indicate that a bigger/longer slab of limestone (and hopefully potentially more mineralization) could be located in this wedge between the two low-angled faults that cut up the limestone exactly where it turns downward (anticline). CEO Carman wasn't sure of this but is looking into it with his team.

We discussed the new concept of layered limestone a bit more in-depth, and Carman had some interesting insights to share. For example, he and his geos are contemplating that one or both of the two low-angle faults might actually be the feeder, or lead to the feeder, being the conduits transporting the mineralization. According to him, it is unusual to get this very high-grade zinc, and only zinc in it, in this location, as existing drill results directly around it are more irregular, containing other metals like led and silver. As a rule of thumb, with a precipitation event, copper and tin mineralization crystallizes first, then zinc, then lead and silver, the farther you go to the boundaries of a deposit or mineralized zone. The purity of the zinc tells Carman that it must be closer to a feeder than the more mixed zinc/led/silver intercepts.

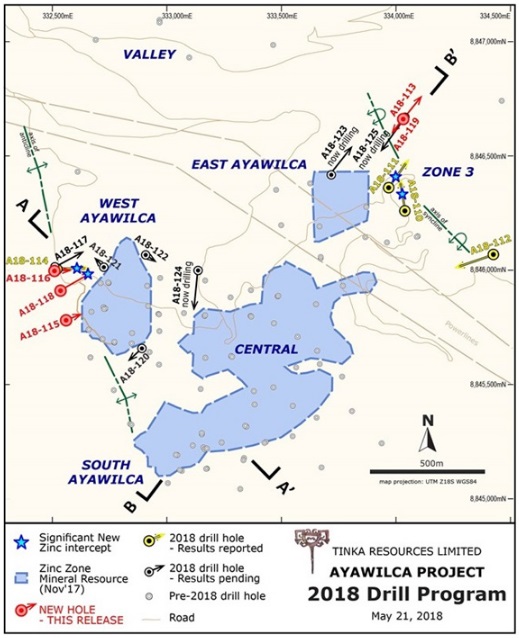

As these two faults trend down, it is anticipated that an eventual feeder system could reside somewhere below Central Ayawilca, and could even be the actual source of all Ayawilca mineralization. This means that the earlier concept of all mineralization coming from the east (Zone 3 and farther away) seems to be less likely, despite the more early-stage copper and tin intercepts over there. For this reason, and not getting very meaningful zinc intercepts at this zone, Tinka management decided not to proceed with more Zone 3 drilling for now, and focus more on West and South. In the news release of May 24, the announced Zone 3 drill results showed little zinc in for example the highly anticipated hole A18-113:

"20.3 metres at 1.26 % tin & 0.30% copper from 658.0 metres depth, including 7.9 metres at 2.39 % tin & 0.64 % copper from 664.1 metres depth."

Holes A18-113 and A18-110 returned substantial amounts of (high-grade) tin though, which could mean an interesting expansion of the existing tin tonnage. However, a hole that was actually pretty impressive in this news release was A18-118, drilled at West Ayawilca, stepping out about 50m: "106.5 metres at 6.8 % zinc (uncut), 0.2 % lead, 17 g/t silver & 48 g/t indium from 237.3 metres."

Assuming continuous mineralization to West and a radius of 25m for this hole, I would like to estimate a hypothetical 1.5-2Mt of additional tonnage, bringing total tonnage to 45.5-46Mt at the moment (in the last April update I estimated 44.1Mt after reported intercepts). These were the highlights of the May 24 news release as a brief intermezzo, and I would like to continue with the new geological concept.

For now, management thinks that these low-angle faults may actually run from West to South, and provide a wide and angled plane(s), acting as possible conduits. To test this concept, they are drilling several holes at the western part of West and South toward the big NW/SE fault, and one hole in between these deposits, named A18-134. Management hopes at least to find more high-grade zinc in a displaced limestone area at the anticline, acting as a second mineralized layer, and possibly even more mineralized layers, and another goal is to try to connect West and South at depth through displaced mineralized limestone.

According to Carman, there is a particular order in time needed to get to the geology as it is now. He thinks the low-angle faults were first, then the big NW/SE fault came, and after this the mineralization event took place. This created a question mark for me regarding the South deposit. Consensus is that South used to be part of Central, and was laterally displaced to the Southwest by an eastwest-running fault after the mineralization event. But the NW/SE fault runs uninterrupted when looking at the maps, with the anticline halting mineralization at the western side of South just as it did at the western side of West.

This isn't possible with the currently assumed order of events, unless the NW/SE fault line actually didn't run uninterrupted in a more or less straight line, but was partly located much more to the east, and got shifted to the west when South started moving laterally as well. As a consequence, management had to pick very consciously a spot to test the connection between West and South, as South was moved, and therefore hole A18-134 was located more to the east to anticipate on all this. See light orange as the estimated original trajectory of the NW/SE fault line:

Something must have happened, but it is not all clear-cut. When looking at the greyish satellite pic, which is the basis of the map, one sees a ridge running more or less at the projected 'old' fault trajectory. This is confusing but the current drilling will probably define the correct structural controls in this area.

More to the west the mineralization drops off quickly when the big northwest/southeast fault is encountered. This type of large fault can act as a subvertical conduit for mineral precipitation, but more often than not they are filled with clay and other material that acts like a barrier. Carman thinks, as mineralization halts abruptly at the NE/SW fault, this is, in fact, a barrier, and he wants to infill drill at a 50m grid spacing and test the consistency of this barrier as well.

For now, the most important objective is to prove up the eventual repetitiveness of the high-grade intercept in the third dimension, parallel at the C section. When the geologists succeed in this, this could create a mineralized zone at West of 300m long, 50m wide laterally and 10m thick that could be about 0.5Mt. The next question, of course, would be if it would be high grade across the entire envelope, if such a high-grade zone could be established at South, and between South and West, and finally if a feeder system could be discovered. Tonnage doesn't need to be big as the ore would be incredibly profitable, and very much suitable to front-load a mining operation for rapid payback and very high IRR.

3. Economics

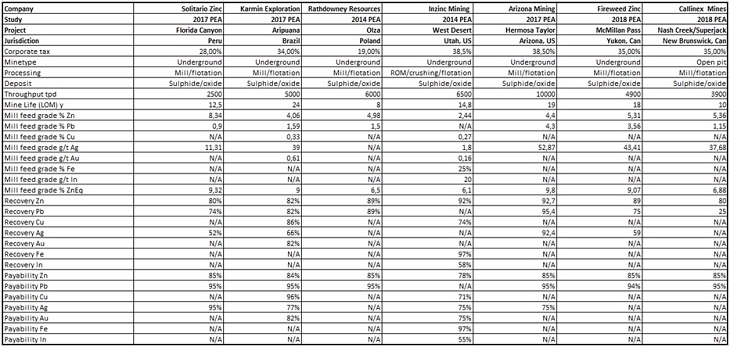

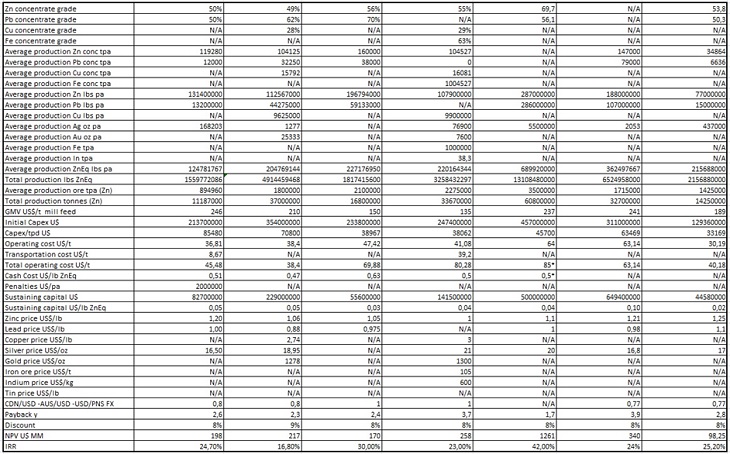

To get an idea of gross metal value: 30% zinc means US$759/t @ $1.15/lb Zn, which is the equivalent of 18.8 g/t gold. One million tonnes of this material mined in the first year or two years could mean a good US$400M pre-tax cash flow after opex, recovery, payability, general and administrative costs (G&A), penalties, treatment charges, etc., which in itself would account for almost the entire capex in my models. Of course, continuous 30% Zn mineralization would be optimistic, so I remained very conservative when modeling (adding around US$100M in total after-tax NPV at base case with more additional tonnage). As a reminder, the basic data for my estimated hypothetical Ayawilca PEA were based on a peer comparison of economic studies. For this article, I added two more studies, the PEA of Fireweed Zinc (FWZ:TSX.V) and the PEA of Callinex Mines Inc. (CNX:TSX.V; CLLXF:OTCQX). The last one is an open pit project, but I added it anyway to get some insight in open pit numbers too. Here is part I:

And part II:

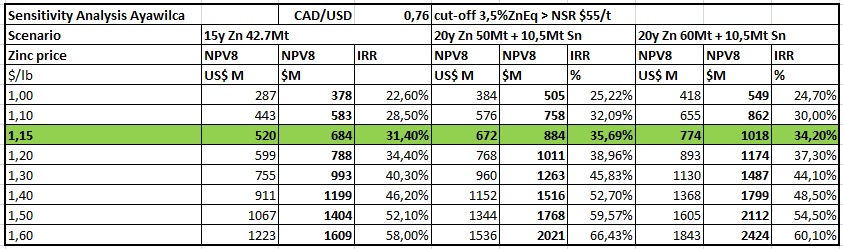

I consider the 50-60 Mt target of Tinka management realistic after this recent development, so I modeled various discounted cash flows on this (6,000 tpd operation) with this new sensitivity table as a result:

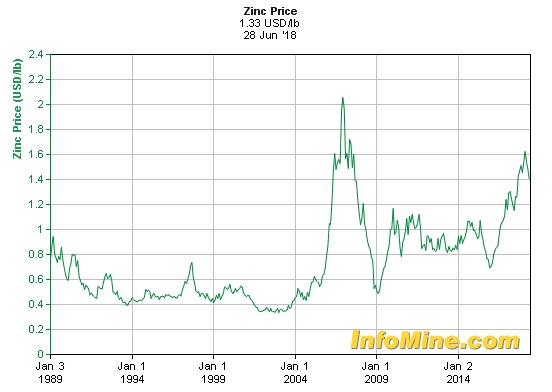

I consider a post-tax internal rate of return (IRR) of 25% at a conservative zinc price the minimum for a medium-size zinc project to be attractive for takeover candidates. No wonder that Arizona's Taylor project got acquired recently, with an IRR of 42% @US$1.10/lb Zn, which is stand-out world class, and traded well above 50% of PEA NPV8 before and after the PEA came out. Economics and jurisdiction of Ayawilca are not as good, but should be able to provide sufficient upside for investors, as it would trade at 17% of hypothetical PEA NPV8 at the moment, if my calculations are correct, of course. I view this project as the best available project behind Arizona's Taylor project. Nonetheless, I still used the US$1.15/lb zinc price for base case, as I consider this a solid target price for the future. Zinc has a tendency to spike for only a few years, and gravitate back to more modest levels:

Looking at this chart, a new normal of US$1.00/lb wouldn't even be too conservative in my view, but considering the lack of good, new advanced projects shovel ready, a US$1.15/lb long term zinc price doesn't seem unrealistic.

4. Catalysts, Plans

According to CEO Carman, Tinka is planning to keep drilling until mid-August with three rigs, which would mean another 8 to 10 holes. This might change when they hit something really spectacular, but this is the current schedule they have in mind. After closing off the data for the upcoming resource update, the metallurgical test work results will be completed and published early Q4, and at the end of Q4 the Preliminary Economic Assessment (PEA) is planned. For now, management doesn't really have a tonnage target in mind, but they are aiming at roughly 50-60Mt.

The idea is to keep drilling during the PEA work, with one rig at Central Ayawilca, probably doing one deep, vertical hole to look for potential layered mineralization over there as well, and/or a possible feeder of it all. Management is also looking at deepening some existing holes at Central after the PEA is completed.

Some final information: Tinka is fully financed for the next 12 months at least, with CA$15M of cash in the treasury. The issued and outstanding share count stands at 260.8M at the moment, and the fully diluted number is about 307M shares. At a current market cap of CA$143M, there is still plenty of upside to be expected, as opex in Peru is very low in general, providing lots of margin of error on my estimates.

5. Conclusion

Hole A18-129 was a very interesting hole. It might not be the biggest overall mineralized intercept for grade times meters, but it seems to be the best indicator for a potential feeder system so far. Besides this, if the new mineralization concept could be verified along the west side of South and West Ayawilca, and hopefully in between, including the extremely high grade, this could imply a significant improvement for already impressive hypothetical PEA economics. Tinka Resources seems very much on its way to a 50Mt target, and this estimated tonnage could prove to be very profitable as well. In that case, upcoming PEA-generated NPV and IRR figures could firmly establish Tinka as the next takeover target after Arizona Mining. This could be shaping up as a pretty interesting second half of this year.

Ayawilca project surroundings

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Disclaimer:

The author is not a registered investment advisor, and has a long position in this stock. Tinka Resources is a sponsoring company. The views, opinions, estimates or forecasts regarding Tinka's performance are those of the author alone and do not represent opinions, forecasts or predictions of Tinka or Tinka's management. Tinka has not in any way endorsed the information, conclusions or recommendations provided by the author.

All facts are to be checked by the reader. For more information go to www.tinkaresources.com and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and graphics provided by the author.