Maurice Jackson: Welcome to Proven and Probable, where we focus on metals, mining, and more. We are speaking with Sam Broom, an investment executive at Sprott Global Resource Investments. Today, we will discuss nickel and cobalt propositions for his portfolio.

Sam, you've truly carved out a niche for yourself in the nickel and cobalt space. Many speculators don't hear much about these metals and the value propositions that they may present. Let's begin with nickel. At the 10,000-foot level, share with us the supply and demand fundamentals for nickel.

Sam Broom: Nickel is actually quite an interesting market. It was a darling back in the early to mid-, even to late 2000s, up until about 20072008, where the price rose dramatically. A lot of people and a lot of speculators made a lot of money in the nickel market in the 2000s.

What happened was the Chinese came up with a new way of producing largely stainless steel, which was the main use for nickel. Formerly, Chinese companies used refined nickel to produce stainless steel. Nickel is a fairly rare metal. There's not a lot of high-quality deposits out there, but the Chinese figured out a way to turn ferronickel, which was basically an iron-rich nickel dirt, a withered rock. You could now use that as a replacement for refined nickel in creating stainless steel.

That truly was almost like a shale oil moment for the nickel market, and drastically changed the cost structure of the industry. It also coincided with the global financial crisis in 2008, and then nickel promptly fell off a cliff. It was trending at about $54,00055,000 a ton. It was as low as almost $7,000 a ton about a year ago. So that's we're talking an 80% decline over the last 10 years, in terms of the nickel price.

What resulted was all of a sudden you hit this flood of nickel, or iron-rich nickel, nickel pig iron, or ferronickel, that flooded into the market from places like Indonesia and the Philippines. It basically destroyed the price of nickel. If you look at a long-term chart of nickel, the refined nickel stores on the LME, you'll see exactly what happened. Basically, supply went through the roof, and then we saw this huge accumulation of nickel. The nickel market was in a huge surplus for years and years.

To this very day, there are still huge amounts of nickel on the LME, compared to historical norms. That's why a lot of people still steer clear of the market. One key thing to note, though, is for the last few years, the nickel market or the refined nickel market has been in a deficit. If you look at that very same chart, you'll notice that stock piles have been starting to draw down, and that's initially what got my attention. That's a key thing for investors and speculators to keep an eye on.

The draw down has actually been in excess of what I was expecting at this point in the cycle, so clients of mine will know that I've been talking about nickel for the better part of about 6 to 12 months as being a commodity I think could be one of the best performing commodities over the next few years. The tide is turning, and it's actually exceeding my expectations so far.

Maurice Jackson: You made two interesting points here. You have a supply deficit and an 80% reduction in price. That really prompts some unique opportunities. Do you foresee a catalyst that will constrain supply in the future, or add to the demand?

Sam Broom: The main driver that I see moving the nickel price is it's a very crucial ingredient in just about every type of lithium-ion battery there is out there. If you look at all the various chemistries, most of them are very nickel-rich.

What we're seeing or just starting to see is increased buying from those getting set in the electric vehicle space where they don't actually need refined nickel, nickel metal. The EV industry uses nickel sulfate, which is basically a nickel salt, but you can make that. You can process refined nickel into nickel sulfate. We're starting to see a little bit of an impact from that.

Nickel is also what I would term a kind of an affluent commodity. Stainless steel is obviously something that an increasingly wealthy population consumes in greater quantities as they become affluent. Global growth in places like China and in the developing world is driving this nickel drawdown at the moment, but I do foresee that in the near future, probably not in the next 12 months, but maybe 18 to 24 to 36 months down the track, the growth of the electric vehicle industry is going to be what drives refined nickel demand.

The key thing to note here is that all of that additional supply that came onto the market back in the late 2000s with the invention of nickel pig iron is completely unsuitable and unusual in the electrical vehicle space. So basically, that can go towards servicing demand from stainless steel fabrication and production, but it cannot be used at all to create electric vehicles and to go into the cathode of lithium-ion batteries.

In a nutshell, that EV demand is going to directly impact on what we term "class one nickel," which is what the LME stock piles represent.

Maurice Jackson: You hit on some very key points here, and that's a lot of ambiguity that I heard regarding the nickel space. There's excess supply that can be used, and you just addressed it cannot be used. For our readers, please do take note here. But I want to stick with this theme here for the supply deficit. Where is current production coming from and will that remain for the future?

Sam Broom: There are two very different classes of nickel supply here. The pig iron and the ferronickel that's getting fed into the Chinese furnaces, this is the supply that can't be used by electric vehicle fabricators and manufacturers. It's coming from primarily from places like Indonesia and the Philippines.

Basically, what they do is they literally just dig it up, and put it on a ship, and ship it to China, and it's a iron nickel-rich dirt that goes over there. That's where that supply largely comes from. There's a little bit coming out of Australia, but mainly places like New Caledonia, Indonesia and the Philippines.

Class one nickel, or refined nickel, comes from a whole host of other places around the world. A major producer is Russia, with Norilsk Nickel, one of the larger mining companies. Outside of that, another major name you've probably heard of is Voisey's Bay in Canada. Outside of that, there's very little in the way of primary nickel production. It's primary nickel sulfide production, I should say; so, sulfide mines.

We won't get too much into the weeds here, but they are the type of mines that can easily produce refined nickel. They're very rare, and there has been next to no major discoveries, at least in the last five years. The last one I can think of was Sirius Resources, which was run by a legendary Australian prospector, Mark Creasy. It discovered Nova Bollinger back in 2012. That's the last major nickel sulfide discovery that I can think of, so that was over five years ago now.

That gives you an idea about how little nickel exploration there has been and how many new high-quality class one nickel discoveries and new projects are in the pipeline. It's basically non-existent.

Maurice Jackson: Sam, with the exclusion of Canada, how mining friendly are these jurisdictions?

Sam Broom: I guess Russia's pretty topical at the moment with all the sanctions that are going on at the moment. The Norilsk company, the Russian company I mentioned, its share price got smashed 20% yesterday on the news. So, Russia's kind of self-explanatory. I personally think Russia's very cheap right now, but it does come with a high degree of geopolitical risk, given the tensions there.

The ferronickel and the pig iron producers, I would say have a moderate to high degree of geopolitical risk. For those of you who aren't familiar, the Philippines has been doing all sorts of things. There is a lot of talk about cracking down on its mining industry, and banning all sorts of open-pit mining because of the damage that these nickel laterites mines have been causing to the countryside.

I would say there's a relatively high degree of risk and potential disruptions to supply from that side. Outside of that, you're looking at places like Australia, Canada, the U.S., parts of Africa. There's potential around the world, but it's just finding these deposits, because they are so rare and so hard to find that we're just seeing next to nothing come through in terms of new, high-quality sulfide deposits that are capable of cheaply producing class-one nickel.

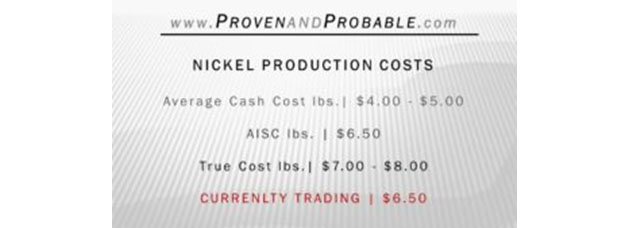

Maurice Jackson: Give us some numbers here. What are the global costs for production versus the all-in sustained costs on nickel?

Sam Broom: It's hard to give an exact number, but last I checked I would say industry-wide cash costs average somewhere around $4-5 a pound. If you take in all-in sustaining costs, you're probably looking at above $6.50 a pound. If you take into consideration the true cost of production, including capital costs, which you should always do, it's probably above $7 or $8 a pound. Nickel's currently trading at $6.50 a pound, or about $13,000 to $14,000 a ton. By and large, the industry is underwater at these prices.

Maurice Jackson: Switching gears, let's delve into cobalt. At the 10,000-foot level, share with us the supply and demand fundamentals for cobalt.

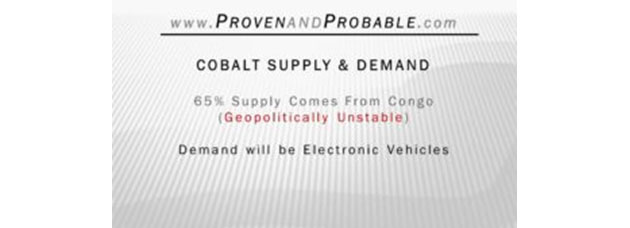

Sam Broom: Cobalt's completely different to nickel, even though they're often found together. By far and away, the main producer in terms of a jurisdiction of cobalt is the Democratic Republic of Congo, which I would probably describe as a country with the highest geopolitical risk of almost any that I know right now. There's a whole lot of strife in terms of what's happening with the government there. The formerly democratically elected president has failed to step down as he is constitutionally mandated to. That was over a year ago now, so there's a lot of shenanigans going on, a whole lot of conflict, the potential for civil war, and that type of thing. I don't know whether that will happen or not, but some not good things are going on over there.

On top of that, it's a very poor country. There are a lot of historical conflicts between different tribes within the country, and issues like that. It's not a very safe place to have one of the key ingredients for electric vehicle lithium-ion batteries. Some 65% of global supply comes from the DRC, so that's what initially got me interested in cobalt well over a year ago. Here's information that I have put out that explains the situation there.

https://www.youtube.com/watch?v=sVt8kfhqGEk

http://www.mining.com/web/why-cobalt-not-lithium-could-be-the-battery-booms-big-commodity-winner/

http://www.mining.com/web/base-metal-breakout-industrial-commodities-threaten-decade-long-downtrend/

Basically, we've got huge amounts of supply coming out of a single country that has extremely elevated geopolitical risk. On the demand side of the equation, the main driver moving forward is going to be the growth of electric vehicles. Now, cobalt, along with nickel and a few other elements, is one of the key ingredients in the cathode component of electric vehicles. It is the ingredient that controls or has a large impact on both the stability and the amount of energy a battery can store. It greatly affects the range of electric vehicles.

I can't see it being replaced any time soon, and I can see a huge increase in demand coming as electric vehicles proliferate. Given we've got an extremely high-risk geopolitical supply backdrop, with an exceptional growth outlook on the demand side, it's a very interesting proposition. Obviously, the cobalt price has already gone up dramatically in the last 12 to 18 months. We're already well into the cobalt price re-rate.

Maurice Jackson: You've already answered part of my question here. The current production is coming from the DRC, and as a speculator, your eyes light up when you have this geopolitical turmoil. Will that change in the future? Do you foresee other production countries coming with production?

Sam Broom: Cobalt's a really interesting one, because it's rare but it's relatively pervasive in very low quantities in rocks around the world. What is really rare is cobalt in economic concentrations. There are many places around the world that have cobalt in economic quantities that it can be mineable. Basically, the main source of cobalt that I see outside of the Congo moving forward is likely to be laterite, the very same type of deposit as the nickel pig iron we talked about earlier; it often has economic quantities of cobalt. The one key jurisdiction I've been focusing on is Australia, because it has the same type of deposits as the Philippines Indonesia and New Caledonia that we've talked about. Yet it's obviously a fair safer jurisdiction.

There are a handful or more of these nickel-cobalt laterite plays in Australia, and that's where I've largely been focusing my attention, because I think that the electric vehicle industry is going to value security of supply over price in the mid- to long term. In other words, they'll be willing to pay up for their nickel and their cobalt, cobalt in particular, if it's been mined in a jurisdiction they're not worried about blowing up into a civil war and losing that supply in six months' time. These companies are spending billions of dollars in capex building these factories. The last thing they need is a supply crunch when it comes to cobalt.

I'm keeping a very close eye on the Australian nickel cobalt play. I will say, though, that these types of plays are more of a speculative investment than an investment-grade proposition. I view them as being almost at the money at current prices. They do require higher prices, nickel in particular, to actually pay off in the long run.

Maurice Jackson: Talk to us about the global costs for production versus the cash costs and the all-in sustaining costs for cobalt.

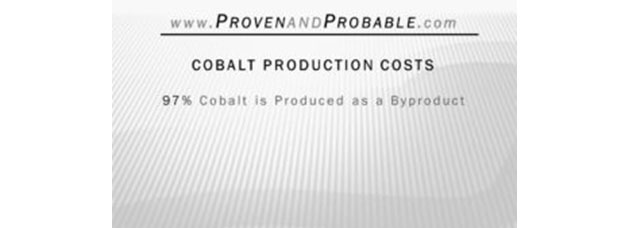

Sam Broom: It's very hard to say because probably 97% of cobalt is produced as a byproduct. There isn't really a cost curve out there for cobalt that you can examine. Usually it goes as either a credit towards nickel or copper production. Looking at it in terms of the cost to produce cobalt, I don't really have any good figures out there.

What I would say is look at cobalt as a way to render nickel and copper projects economic. For example, there's a company I watch that just put out a feasibility study that the nickel all-in sustaining costs per pound are something like $5 to $6. With the cobalt credits, that drops to about $1. That goes to show you how much the cobalt credits it's getting from its project go towards making these projects economic. Basically, this project would be completely uneconomic at current nickel prices, moderately economic at current prices, and extremely economic at say, $20,000 a ton of nickel.

Maurice Jackson: Thank you for a very comprehensive interview regarding cobalt and nickel. Does Sprott Global Resource Investment still provide a free grading of one's natural resource portfolio at no cost and obligation?

Sam Broom: Absolutely. If you want me to take a look at your portfolio, particularly those with an EV metal and material focus, I'd be more than happy to give you a no obligations ranking of your portfolio. Bear in mind that this is wouldn't be investment advice or anything. It'd be a one to ten ranking. But if you would like to take me up on that offer, my email is [email protected]. I'd be more than happy to receive your request and give you a no obligations ranking there.

You can either attach an Excel attachment, or simply just list your portfolio in bullet point form in the email. With the subject line: Proven and Probable

Maurice Jackson: Do we have a contact phone number for you at Sprott?

Sam Broom: You can reach me at 800-477-7853.

Maurice Jackson: For our readers, we want to remind you to register for the Sprott Natural Resource Symposium, which will be conducted July 17-20 in Vancouver, British Columbia. Just click on the registration tab on our website for free tickets. Featured speakers will be Rick Rule, Doug Casey, Jim Rickards, Jim Grant, just to name a few. We will be present and we look forward to meeting you. Sam, let me ask you this as well, will you be in attendance?

Sam Broom: I am certainly planning on being there. I have my first child due in early August, so as long as that doesn't happen ahead of schedule, I will certainly be there.

Maurice Jackson: All right, look forward to seeing you there. Last but not least, please visit our website, ProvenAndProbable.com, where we interview the most respected names in the natural resource space. You may reach us at [email protected].

Sam Broom of Sprott Global Resource Investments, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Statements and opinions expressed are the opinions of Sam Broom and Maurice Jackson and not of Streetwise Reports or its officers. They are wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Sam Broom and Maurice Jackson were not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

Images provided by the author.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. YOU SHOULD NOT MAKE ANY DECISION, FINANCIAL, INVESTMENTS, TRADING OR OTHERWISE, BASED ON ANY OF THE INFORMATION PRESENTED ON THIS FORUM WITHOUT UNDERTAKING INDEPENDENT DUE DILIGENCE AND CONSULTATION WITH A PROFESSIONAL BROKER OR COMPETENT FINANCIAL ADVISOR. You understand that you are using any and all Information available on or through this forum AT YOUR OWN RISK.