Ayawilca project; drilling location

1. Introduction

It is a busy and exciting time for top zinc junior Tinka Resources Ltd. (TK:TSX.V; TLD:FSE; TKRFF:OTCPK). Drill results are rolling in all year now, Tinka is the talk of the town at many conferences, the team got a much deserved accolade by receiving the Mining Journal "Explorer of the year 2017" award, and the company got listed on the Peruvian stock exchange (Lima Stock Exchange or BVL). I liked this move, as it made the company less dependent on for example Canadian brokers/banks to raise money in the future.

Being one of the major zinc juniors of 2017, the recent resource update of November 8th was highly anticipated by a number of newsletter writers, among them no less then Joe Mazumdar and Brent Cook of Exploration Insights, and of course yours truly. There seemed to be a widespread consensus about a 30-33Mt target, which turned out to be a 42.7Mt resource in the end, but this needs a bit more explanation as the newsletter writers used the higher cut-offs from the first resource estimate, in order to compare apples with apples

As the zinc price staged a decisive upswing for the last year as the long-time deficit theory finally played out, Tinka management felt it was fitting to use a higher zinc price, which in turn meant a lower Net Smelter Return (NSR) value, equal to a lower cut-off ZnEq grade, and this usually generates higher tonnage compared to higher cut-offs, as almost always more mineralization (at lower grade) is eligible to be included. In this article I will explain the actual increase of the resource, the implications of different cut-offs and I will venture into economic analysis of peer projects in order to project estimated valuations and price targets for Tinka Resources.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Please note: the views, opinions, estimates or forecasts regarding Tinka's performance are those of the author alone and do not represent opinions, forecasts or predictions of Tinka or Tinka's management. Tinka has not in any way endorsed the information, conclusions or recommendations provided by the author.

2. Rehashing some basics

Before I delve further into the story, let's quickly rehash/update some basic information on share structure and financials first, and some additional background info on zinc for interested readers. Tinka Resources has 212.23M shares outstanding. The fully diluted share count stands at 249.49M shares, as there are 10.14M options, 0.5M shares reserved, and 26.5M warrants (all comfortably in the money: and most of the 12.6M warrants @C$0.30 expiring Nov 2017 will be exercised in the last two weeks of November according to management)

Large institutional shareholders are Sentient (25%) and IFC (9%), and management is holding about 2%. The company is lead by CEO Graham Carman (PhD Geo). Recently director David Henstridge, one of the founders, retired from his position, and according to Carman this had nothing to do with freeing up a board seat for eventual new strategic investors, this was just for personal reasons. Coverage by analysts is developing at the moment, as Tinka now has three parties tracking proceedings (GMP, Industrial Alliance and Beacon). The current cash position is estimated by management at C$5M, with no debt, and management expects to have about C$7M in the treasury by year end. This should be enough to do more drilling, metallurgic test work (in short "met work") and complete the Preliminary Economic Assessment (PEA) during H1 2018. The current share price is C$0.70, resulting in a current and fully diluted market cap of C$174.6M (which is realistic as all warrants are well in the money).

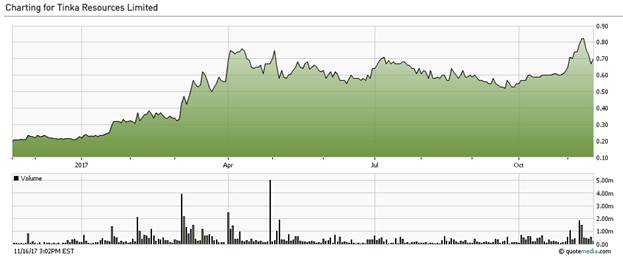

Share price; 1 year time frame

Despite the rising zinc price, the Tinka share was sideranging for a while, as the markets were hoping on a second big discovery following the South Zone, besides the successful delineation of this first new target for this year's drill program. Fortunately, the resource update and the anticipation of investors leading up to it has caused a breakout, printing a C$0.87 all time high on the day of the update. It dropped off again to C$0.78 that day, which probably indicated some profit taking. The share price consolidated in the low seventies this week, which could very well be new support, as the company is fast-tracking towards the Preliminary Economic Assessment (PEA) in Q2 2018) which I expect to be impressive as mining costs in Peru are low. More on this later.

I expect more institutional interest after this resource update, and hopefully positive step out drill results to contribute to a higher trending share price for the foreseeable future, depending on overall stock market sentiment and metal prices of course. Carman has been flying all over the world since the resource update to present the story to interested parties, so I'm curious what comes out of this in due time.

But first let's have a look at the primary metal Tinka is looking for, the base metal zinc.

3. Zinc

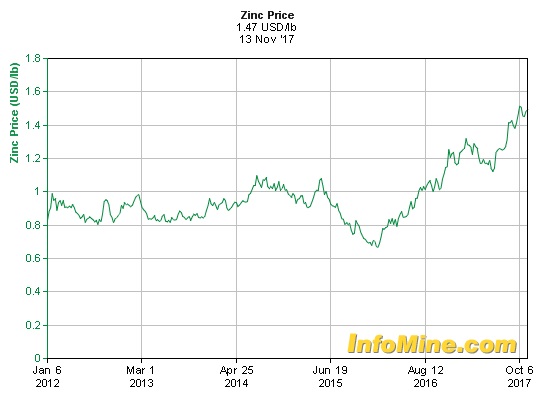

A chronic shortage of supply of zinc is being forecasted. The coincidental closure of major zinc mines (Brunswick, Perseverance, Century, Lisheen, Skorpion) through depletion, taking 500kt per annum off the table, and this, coupled with a very limited number of new zinc mines in the near-term development pipeline set to come online, is expected to lead to a robust zinc price for the next few years. The price of zinc already ran up from US$0.67 to US$1.47/lb, and is forecasted to go up even more:

The zinc market has been in deficit for a long time (since 2012), but only since the end of 2015 did the zinc price start to appreciate, probably due to covert stockpiles which finally seem to be depleted. So, despite the current modest correction, the long-term zinc case looks pretty convincing in my view, and playing into the hands of Tinka Resources.

Here is a chart from Kitco.com, indicating long-term weakness in LME inventories, but only since the end of 2015 coinciding with factors like production going off line:

It seems like the stocks are heading for new lows. Following up on supply constraints, cutbacks like the ones announced by Glencore, as well as decreases expected for Kazakhstan and Peru, have tightened supply further and deepened the concentrate deficit. Interestingly, China had also shut down 26 mines in August 2016 due to safety and environmental concerns, which was a serious gesture.

Analysts believe that the zinc price could appreciate further, to $2.00/lb levels or more, as a new critical deficit could be looming for 2018. Biggest risk factor in all this remains main producer and consumer China (like it is with almost every other metal).

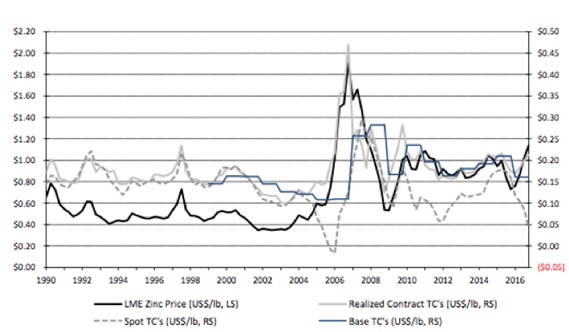

On a side note: an interesting phenomenon in zinc production are the treatment charges (TC). These are the charges paid by zinc miners to the smelters, for refining their zinc concentrates into zinc ingots. These TCs are often quite substantial, often to the amount of $200/t Zn for long-term contracts. Besides LT contracts there are also spot TCs for smaller quantities, and those have gone down a lot lately, going from $100-120/t to $40/t, as smelters are having a hard time getting zinc concentrates to process. As this chart shows, the interesting part of this is that spot TCs go down first as an indicator, before zinc prices start rising:

Zinc prices and TCs; source RBC zinc report Jan 2017

The funny part is that the long-term contract TC prices don't go down first with shortages, but only go up when the zinc price really starts to take off. So apparently there are two different TC pricing mechanisms at work at the same time with smelters.

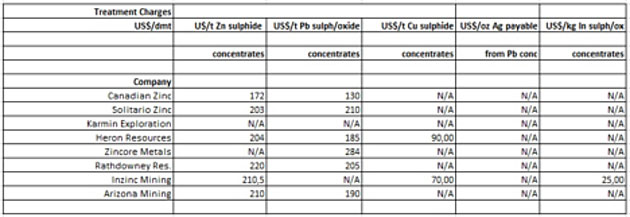

Smelters have a dominant position in the zinc business, as they can set the TC terms. These terms are so one-sided, that zinc concentrates usually need significant by-products, or miners need to have a lead concentrate as well in order to be profitable. This was an important reason for BHP and Rio Tinto to exit the zinc business. Usual by-products are lead, silver, gold, and copper, but sometimes iron ore, molybdenum and even indium are recovered and paid for.

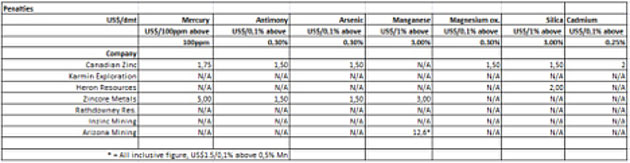

Normally, smelters don't always recover and pay for indium, but Tinka management confirmed that due to the current scarcity of concentrate, smelters are most likely willing to handle their indium, as amount and grade are sufficient. Indium is valuable, as the price hovers around $280/kg In. When analyzing a few economic studies of zinc juniors, I came across several TCs, and I gathered them in this table, to get an impression:

Please note that Canadian Zinc provided the latest figures, as it delivered a FS in October. To me it is doubtful to see these TCs continuing for the life of mine for Canadian Zinc, so a bit more conservatism would have been more convincing. But at the same time their project saw quite a bit of cost escalations, so they had to try everything to keep it viable. Besides TCs, there are also penalties for deleterious elements or impurities, which, if present above certain limits, can have a negative impact for smelters regarding toxicity or obstructing the smelting process. Those limits can vary per smelter, as they buy different batches of concentrates, each with different impurities, resulting in different mixed smelter feeds. If there is too much of certain impurities, the entire concentrate can even become unsalable. As far as this wasn't already clear to investors, now it is.

Earlier this year, a lot has been made of the case of Arizona Mining, which stated in their 2016 NI43-101 report for Taylor that the concentrates contained no deleterious elements, which was wrong unfortunately, as the zinc concentrate did contain 1.3% manganese, and the lead concentrate 0.1%. However, circulating claims about Taylor being rendered uneconomic because of Mn grade being over a 1% smelter threshold didn't appear to hold any ground, as an apparent $13 penalty (according to Arizona management) over a $1100/t revenue wasn't significant.

Again, I created a table based on the penalty terms for Canadian Zinc and Zincore, which appeared to be a very global industry guideline as there was very limited data available in most studies:

The $12.6/t penalty for Arizona is a total as provided by management, and not a price per grade percentage etc, which can be found in the footnote of the table. As can be seen, for Zincore a 1.3% manganese content wouldn't even result in a penalty, as the term I used for this table was coming from the Zincore 2013 PFS study. It has to be noted that this term was quoted for the fume case (roasting), and for the refined zinc con scenario there wasn't even a manganese term mentioned. A distinction was made between Chinese and non-Chinese smelters so this could make a difference. The study was done by AMEC which I held in very high regard, so I don't expect sloppy work there. In general, a 1% Mn percentage is considered a threshold for a good zinc concentrate, although cost-wise a multiple of this wouldn't make much of an impact. However, smelters are able to dictate what they want.

Arizona Mining used much more stringent terms, in a time smelters are scrambling for ore, so if anything, compared to the numbers in the Zincore study at least, Arizona seemed to be conservative here.

It will be clear by now that zinc isn't as straightforward as for example copper, but has a lot of moving parts.

So far for zinc, let's continue with the updated resource estimate of Tinka's flagship project, Ayawilca.

4. The updated resource

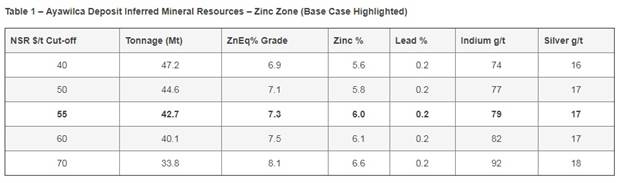

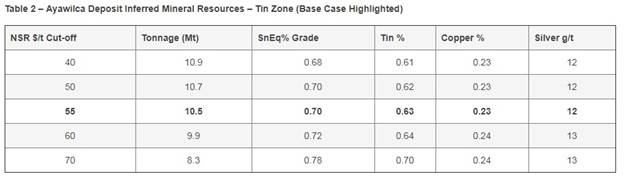

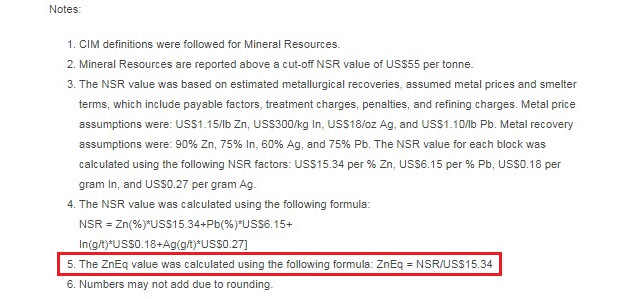

The news release about the new resource estimate came out on November 8th, 2017. There were actually 2 resource estimates completed in the same report, both Inferred: the zinc resource came in at a very decent 42.7Mt @7.3%ZnEq, and the tin resource contained a more than expected (at least with me as an armchair geo) 10.5Mt @0.70% SnEq. Both resources had a lower cut-off of $55/t NSR and $1.15/lb Zn, as the earlier resource estimate used a $60/t NSR and $1.00/lb Zn. A lower NSR cut-off seems appropriate as the zinc price went up quite a bit since the maiden resource came out. The resource tables look like this for tonnage and grade:

For the Zinc Zone:

And for the Tin Zone:

The base case $55 NSR generated the following updated resources:

For tin:

This tonnage actually surprised me a bit as I estimated it very globally in the 6.5-7.5Mt range, but I am sure that a lower cut-off mattered quite a bit here, just as it did for zinc, which I will discuss in more detail now. Here is the resource for zinc:

The 42.7Mt @7.3% ZnEq looks a lot more than the former resource estimate at 18.8Mt @ 8.2% ZnEq, but things are a bit more nuanced as I will explain.

I wasn't too familiar with the NSR cut-off concept as I usually use grade cut-offs, but fortunately the notes with the tables provided more insights:

The grade cut-off I was looking for can be calculated quite easily (see item 5.) by dividing the NSR by $15.34, which means $55 / $15.34 = 3.59%ZnEq. This is substantially lower than the 5% ZnEq used in the 18.8Mt, and has consequences as we will see next. I will show this by extrapolating an estimated set of tonnage and grade numbers to cut-offs comparable to the maiden resource estimate. This primary set of numbers was generated by geologist blogger Angry Geologist, who again was so nice to let me use his Leapfrog data output. This came in very handy as it isn't possible for me to estimate tonnage at different cut-offs anywhere near as accurate as can be done with Leapfrog, which is a professional geo software package to estimate resources. Here we go, first you see the maiden resource, then Angry Geologist's estimate for the newly discovered and delineated resource (predominantly South Zone), and in the end, both are combined:

As the new resource came in at 42.7Mt @7.3% ZnEq at a $55/t NSR or 3.5%, this is very close to the above generated total of 43.7Mt @7.70% ZnEq at the same cut-off. The 30.6Mt @5% ZnEq, more or less identically estimated by a number of parties (there is a good chance I was first with my 31Mt estimate here, and 30.3Mt here, you need to have luck with these things when using back of the envelope estimates), turned out to be right on target. The same cut-off was used for the maiden resource, as nobody knew beforehand what cut-off Tinka was going to use for the resource update, and apples are best to be compared to apples in that case. With the higher zinc price it was a clear opportunity to use a lower cut-off and increase tonnage, and Tinka management made good use of it. In the end it doesn't really matter for buyout suitors, as long as tonnage and grade remain economic at lower prices (around $1.00/lb Zn), as zinc bull markets don't have a tendency to last long periods of time.

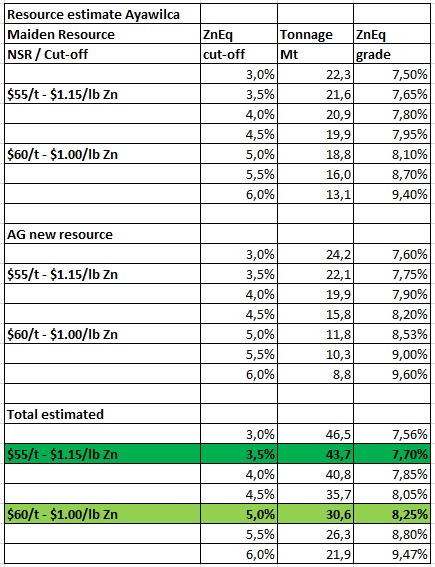

The company made a 3D model of the current resource so you can have a better impression of mineralized envelopes:

When seeing the resource update, the numbers came so close that I wanted to purchase my own version of Leapfrog as it reportedly was easy to learn. Unfortunately, it turned out it would cost me a hefty $30,000 fee for one license, and an annual $5,000 maintenance fee, which is a bit much for a newsletter writer like me. I'm looking into cheaper options as it would be fascinating and give a meaningful head start, to be able to come up with such (hopefully) easy to learn accurate estimates myself, before companies come out with their own official estimates.

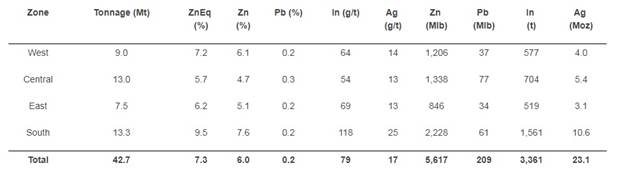

The bottom line of this is that the new resource actually came in very close to expectations, and looks like very solid material to base a PEA on. Especially the thicker, higher grade and near surface part of the South Zone can be used in combination with the West Zone to frontload the project for a rapid payback.

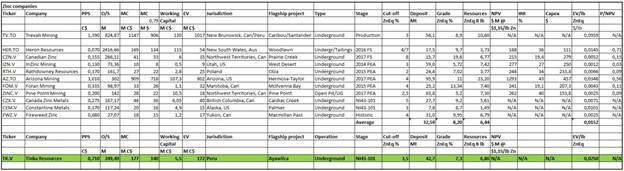

5. Peer comparison

AAs I believe it is useful to keep tracking peers to stay in touch, I lined up Tinka for the second time, against 12 zinc juniors of which a few are new as I found those more of interest and/or more relevant. More specific, Fireweed Zinc has a very low valuation but a quality project, good structure and good people, and I recommend doing dd on it. Furthermore, I added the cut-offs as it could matter a lot for resource size, and the NPV columns in order to say something about P/NPV, an important metric for developers. I didn't normalize the deposits for cut-offs, but tried to normalize NPV and IRR for a zinc price of $1.15/lb for better comparisons, as I view NPV (in combination with IRR) as a more important and telling metric compared to EV/lb as DCF analysis takes everything into account:

The EV/lb metric actually isn't very useful for deposits as economics could vary a lot while EV doesn't indicate this, but it does provide quick insight in anomalies for ratios, and as such is an interesting indication for further dd. Always keep in mind that such a table isn't telling the whole stories of companies, for example Pine Point Mining doesn't have the highest valuation despite their excellent PEA economics as they have to do a lot of well testing in order to see if groundwater could have a meaningful impact on their project economics. I added Trevali to roughly indicate the difference between explorers/developers and producers.

Considering the averages, Tinka isn't cheap as it trades close to for example Arizona Mining, the much bigger zinc developer for EV/lb, but this indicates the premium of the economic potential of Ayawilca, buyout potential for several nearby interested candidates, and exploration potential as well as Tinka isn't done yet as they still have a lot of targets to test. Next up I will try to estimate the economic potential, and let's see how Tinka ranks after this.

6. Economic potential

As the resource estimate has been updated now and analysts are switching to DCF modeling as the PEA is planned to be completed in Q2 2018, I'm going to dive a bit deeper into this subject after briefly touching upon it in my first analysis on Tinka back in May 2017. Therefore I analyzed a number of company figures and economic studies to get a grip, and turned to experts like CEO.CA regular Doug Beattie, who has considerable engineering experience in zinc mining projects, but also designed Cameco's very profitable flagship (despite being halted now for approximately 12 months in total, due to a low uranium price environment) McArthur uranium mine. The guy obviously knows his engineering. Often his provided information and insights are very useful, and I'm happy to integrate relevant parts of it in my analysis. Gems of comments by Doug are for example these two on Ayawilca, which can be found on ceo.ca, and I just quote them here so you can follow his train of thought and sharing of probably useful insights:

"What the project has going for it however is bulk mining potential and it is shallow hence ramp mining such as at Cerro Lindo or Santander may be used. The two lowest cost mines reviewed here. Additionally, the deposit is in the Cerro de Pasco area meaning there is good infrastructure nearby. Volcan for instance has a large mill sitting idle in the area. When I looked at the topography of the project it would probably be better to build a mill on site instead of shipping ore to the Cerro de Pasco area mills. Glencore relocated a mill to Santander to minimize project capital cost and the same philosophy could be applied here.

"The existing inferred resource base, if upgraded to measured and indicated resources could likely support a 3,000 tpd mine utilizing blasthole stoping for the West Zone and East Tennessee zinc mine style bulk room and pillar mining for the Central and East Zones for perhaps 10-12 years. This assumes good ground conditions underground. So a mine producing in the 40,000 T a year of zinc with some minor byproduct credits could be envisioned assuming good mill recoveries. Unit costs could be similar to Santander's at a low $US35-40/T due to the shallow depth and bulk mining methods used."

And:

"The pipeline of projects that Volcan has is slim to non-existent so they could be a willing JV partner here. Likewise, Milpo may see the wisdom of a JV or acquisition along the lines of Shalipayco. If Glencore pulls the plug on Iscaycruz like I think they will, they suddenly have a mill that can be relocated along the lines of what they did for Santander. Finally, if the reserves at Catalina Huanca are being rapidly depleted, Trafigura may also be a willing partner or acquirer."

With the current tonnage (these comments were from before the resource update), a larger operation is warranted. Doug's thoughts about relocating idle mills or JVs with nearby zinc mines look interesting to me strategy-wise, already having outlined the most probably suitors along the way. Before you think of offering him a well-paid analyst/fund manager job after reading this: Doug enjoys his golfing days way too much as an early retiree.

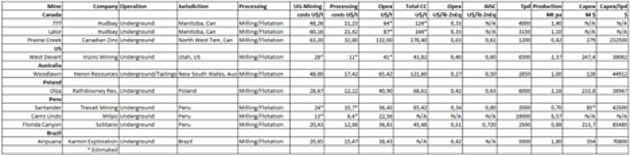

Before I get to actual economic estimates, I want to have a good impression of a number of variables myself. First up are mining costs and capex/tpd ratios:

It can be seen that Peruvian operations do have lower mining costs per tonne compared to other jurisdictions, UG mining and processing are cheaper to the tune of almost 50%. This is likely due to cheap labour and power, and possibly positive FX-inflation effects. Trevali Mining has low opex too, but somehow manages to end up with high AISC. I'm not really into Trevali, but that would be the first focus if I wanted to know more. Their capex is a total mystery as well, since they built it without any economic study.

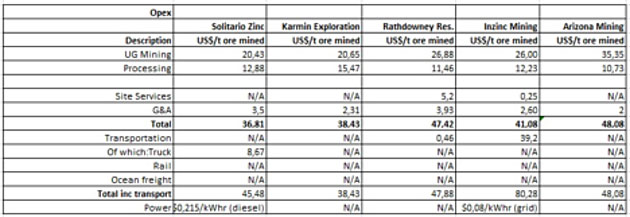

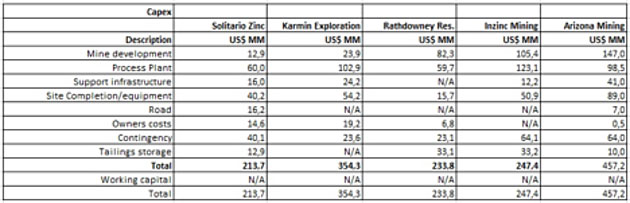

I wanted to get a bit more detail on capex and opex numbers, so I selected 5 companies with relatively recent economic studies:

Opex figures:

On average the LatAm projects have lower opex as expected, but this is just an indication as only 2 projects were taken into consideration. Here are the capex breakdowns:

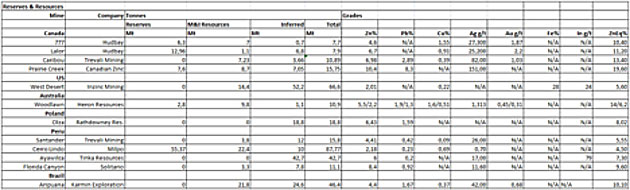

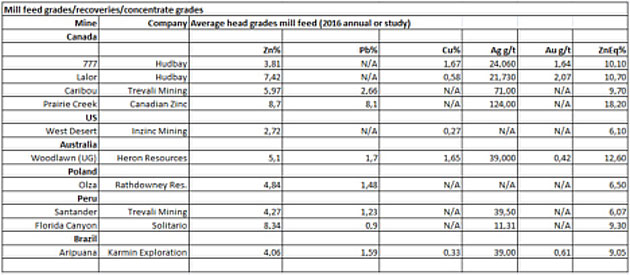

It is hard to compare these projects, as projects differ, companies have different strategies, sunk costs, etc, but at least it gives an impression of costs. I also gathered data regarding resources and reserves, and grades for the set of companies I used for mining costs and capex/tpd ratios:

And the available mill feed grades, as opposed to the R&R grades:

The mill feed grades are 5-20% lower for ZnEq% compared to the R&R grades, something to keep in mind for estimated Ayawilca economics later on. I also looked into recoveries and concentrate grades, to see what's industry standard:

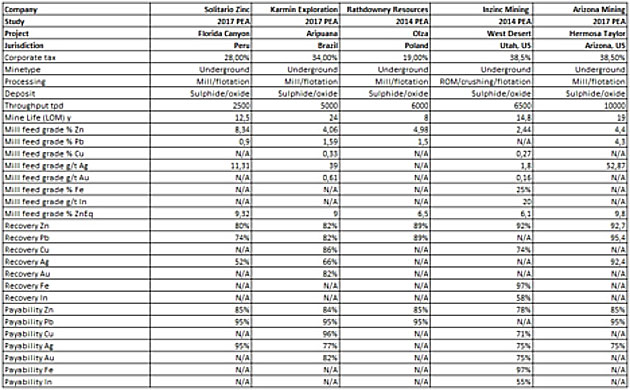

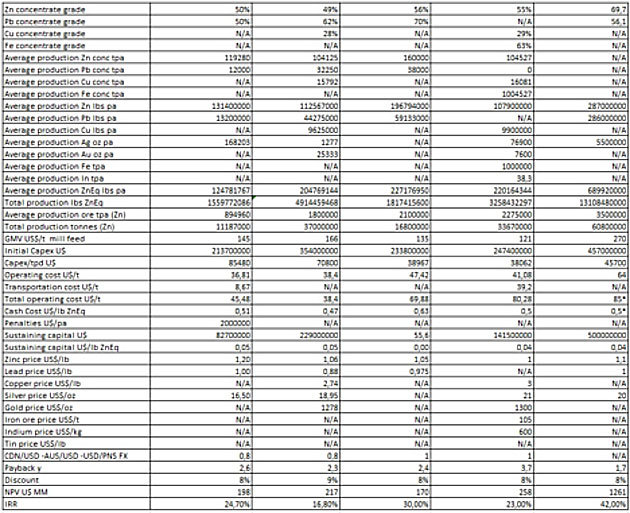

Zinc recoveries and concentrate grades seem relatively stable, but by products go all over the map. To get more detail on relevant project parameters, I compared 5 economic studies, resulting in the following two-part table:

Part I:

and Part II:

Please note that US$ figures are calculated in C$ except the metal quotes. With all this information it should be possible to make very global assumptions for Ayawilca economics.

I use the 42.7Mt ZnEq resource as a base case. As mentioned, it isn't very hard to imagine, if Tinka would be successful on further drilling, that higher tonnage scenarios could come into play, but let's stick with the current resource figure for now.

- production tonnage 75-80% of resources

- mill feed 75-80% of R&R grade

- LOM of 15 years

- capex/tpd:$60k (economies of scale), this is a tricky metric as two LatAm projects have a higher figure ($70.8k/tpd and $85.5k/tpd). But, for example, Santander, the Peruvian mine of Trevali, could have a capex of anywhere between $50M and $130M when looking at the various financings and listening to people more familiar with this than me, so I picked a middle ground and used a $85M capex ($42.5k/tpd). Combined with the on average much lower metrics for North American/European projects (about $40/tpd on average), which is puzzling to me since Peru is supposed to be cheaper no matter what (see opex numbers), an average figure of $60/tpd seemed appropriate.

- recoveries Zn 90%, Pb 75%, Ag 60%, In 60%: I noticed zinc recoveries to hover around 90% on average in the studies, but at first this 90% Zn recovery figure seemed high after Tinka obtained much lower figures in their earlier met work (64.5% after 3rd cleaner recovery). When asked about it, Carman explained that this initial floatation met work was done through open cycle testing, without any recirculation. Later stages of met work will include closed cycle testing with as much recirculation as needed to get to the 90% threshold.

- payability Zn 85%, Pb 95%, Ag 75%, In 55%

- concentrate Zn 52%, Pb 60%

- opex $/t ore: $40

- AISC $/ZnEq lbs: 0.72 > US$0.57

- metal prices Zn $1.15, Pb $1.10, Ag $18, In $300

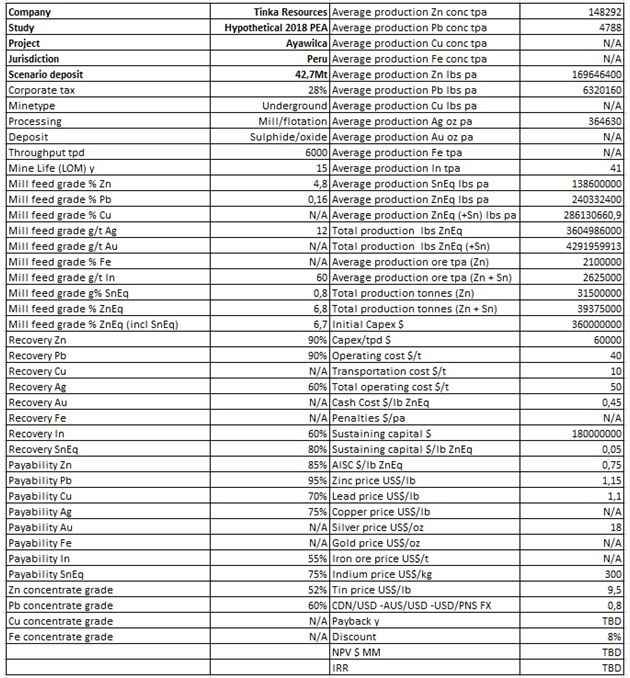

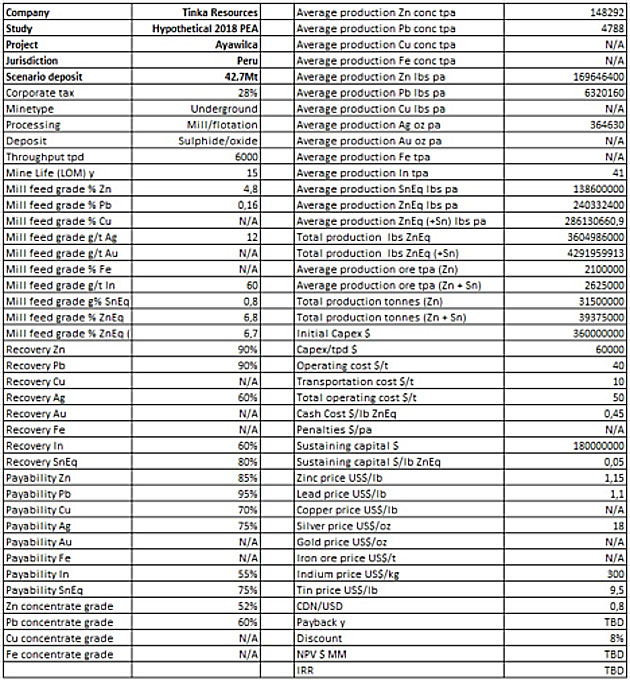

This results in this table:

All this leads to this hypothetical base case scenario of 15y LOM, based on 42.7Mt and a US$1.15 Zn price:

The resulting hypothetical post-tax NPV8 is already larger than the used capex number, which is one of the thresholds used by banks when financing capex. The IRR is looking good too:

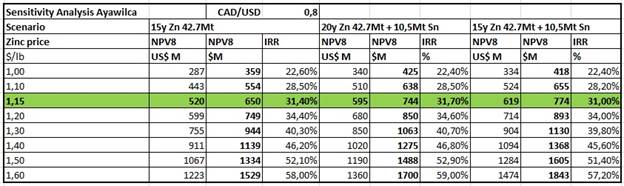

To take this a bit further, I constructed a sensitivity analysis, which indicates a viable project at various zinc price scenarios. Furthermore, two scenarios with additional tin production were added, to indicate upside in that regard. The 20y scenario doesn't require more capex, but the second 15y scenario does, and throughput would go to 7,500tpd in that case, raising capex to $450M coming from $360M:

This sensitivity analysis indicates a very robust project, with solid profit margins even at $1.00/lb Zn. At the current market cap of C$177M, Tinka would be trading at 27% of my estimated NPV8 @$1.15 (so P/NPV is 0.27 for the zinc only 15y scenario), and just 13% of the estimated NPV8 @$1.50, being the current zinc price.

A share price target remains something of a stretch at this early stage, but as Arizona Mining already traded at close to half NPV8 @US$1.10/lb Zn before the PEA came out, there seems to be enough room to appreciate on a larger resource and/or a PEA. As Arizona Mining got more attention, I feel comfortable by estimating a 25% NPV8 target @$1.20/lb Zn when the PEA comes out in Q2, 2018, not taking into account an included expanded resource based on possible ongoing drilling success. Other assumptions would be neutral to better market sentiment and zinc prices holding above $1.40/lb levels. This could globally indicate an estimated C$1.20-1.25 price target after the study results would be announced.

As economics of Ayawilca look destined to be very good, there is no doubt in my mind that the surrounding large producers like Volcan or Minsur will have Tinka firmly on their radars for strategic investments, off-takes or outright buyouts. With zinc fundamentals not appearing to let down anytime soon, I would be surprised if Tinka is still around at the end of 2018.

6. Ongoing work, plans, catalysts

Most of the drill program for 2017 is completed, as about 18,000m of assays is in, and management expects to receive another 2,000 before year end. At the moment Tinka is drilling with 2 rigs. This will remain this way as the wet (rainy) season has started (Sept-March), and will be increasing to 3-4 rigs again in April 2018. One rig is drilling the gap between the South Zone and West Zone, and the other is redrilling hole 091 at Zone 3 at the moment, in order to deepen it further. Management is looking to drill at least one more hole for December, and is planning another few into Zone 3, mostly at the western part of it. They will try to follow up on an older hole, number 031, and go deeper and to the west.

Approximately three to seven holes will be drilled on the Valley target, depending on success. There are still a lot of targets to test according to magnetics, geology and results, and Zone 3 and the connections between this and East/Central will be a major part of exploration drilling for 2018. For now, Carman expects to do another 10,000-15,000m in total for next year. Besides drilling, he also expects to complete met work during Q1 2018. Fortunately this will not take much out of his budget as it would cost an estimated C$200-300k according to him. The PEA is up for Q2 2018, and the actual tonnage will be dependent on the results of drilling. Management is still looking after deeper feeder structures, as they think the potential for this should be there somewhere. This will be tested through drilling a few deep holes at the South Zone, but this has lower priority and is third on the list of exploration targets, after Zone 3 and Valley. As Carman projects a C$7M treasury at the end of December, and drilling costs all in are about C$300/m, he expects to be cashed up at least for H1 2018, and will of course have to raise more during next year, but not anytime soon.

Tinka is besides increasing the overall resource also looking at infill drilling for the Prefeasibility Study (PFS) to get as much to Measured & Indicated (M&I) as possible, but the PEA will likely remain on an Inferred basis. This is also the reason they will most likely not lower the cut-off any further at the PEA, as the resource isn't derisked enough being Inferred. Carman estimates it will take another 15,000m of drilling to get the higher grade parts, say half the tonnage, to M&I, budgeting it around C$5-6M.

Overall things are progressing well for this solid zinc junior, and it looks like they might have a pretty economic project with Ayawilca, which could be of interest for a number of suitors for sure. A next big hit is possible as they still have a lot of targets to drill, and this could really bring it to Tier I status, and this is what management is chasing.

7. Conclusion

Tinka Resources has delivered a solid resource estimate, according to expectations. This tonnage provides a strong foundation on which management can build further upon, with regard to an upcoming PEA (most likely in Q2 2018) and more drilling, which is in progress.

It is the possible exploration upside combined with possible future economics that could distinguish Tinka from most of its competitors, as mining in Peru is much cheaper than in most of the other peer's jurisdictions. When the PEA comes out, this will be the time for Tinka Resources to really set itself apart in my view, as I believe economic potential hasn't really sunk in yet. Exciting times ahead.

Ayawilca project surroundings

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at http://www.criticalinvestor.eu/, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Disclaimer:

The author is not a registered investment advisor, and has a long position in this stock, and in Fireweed Zinc. Tinka Resources is a sponsoring company. The views, opinions, estimates or forecasts regarding Tinka's performance are those of the author alone and do not represent opinions, forecasts or predictions of Tinka or Tinka's management. Tinka has not in any way endorsed the information, conclusions or recommendations provided by the author.

All facts are to be checked by the reader. For more information go to www.tinkaresources.com and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: Trevali. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.