Ukraine has been invaded by Russia, further disturbing supply/demand chains around the world, where commodity prices are soaring and inflation is increasing to levels not reached in decades. Precious metals, and more specifically gold, are doing well with gold hovering at US$1,915/oz. For Gold Terra Resource Corp. (YGT:TSX.V; YGTFF:OTC; TXO:FRANKFURT), it’s still business as usual, operating far away in Canada. It is currently drilling with four rigs at its Yellowknife City Gold Project, intersecting (visible) gold and watching results coming in on a regular basis now. With the closing of an oversubscribed CA$5.6 million (M) capital raise on Feb. 28, it is fully funded to complete the ongoing, extensive 30,000-meter drill program at the Campbell Shear at depth.

Shortly after taking the reins at Gold Terra, Chief Executive Officer Gerald Panneton didn’t waste much time and announced a bought deal offering shortly afterward on Feb. 9. This offering was intended to raise CA$5M, and was a combination of charitable flow-through (FT) shares, offered at a price of CA$0.30, traditional FT shares offered at a price of CA$0.24, and common shares offered at a price of CA$0.21, with no warrants. The offering was made by way of a short form prospectus in each of the provinces of Canada (other than Quebec) and the Northwest Territories. Common Shares were offered by way of private placement in the United States. The offering was made through a syndicate of underwriters led by Stifel GMP and included BMO Capital Markets and Beacon Securities, who received a 7% cash commission (CA$392,000) over total gross proceeds.

It was good to see that directors and officers of Gold Terra also participated in the offering and were issued an aggregate of 900,000 common shares, including 200,000 traditional FT shares. The result was an oversubscribed offering. Panneton told me he had interest for over 30M shares and he had to cut back himself as well to make some room for others. According to SEDI, he still bought 400,000 shares, Chief Financial Officer Mark Brown acquired 100,000 shares, and two directors each bought 200,000 shares. Also, all existing shareholder institutions supported the deal. The end result was a healthy CA$5.6M, due to the exercise in full of the over-allotment option by the underwriters. In total, 21.6M shares were issued, more specifically 8.9M charitable flow-through common shares were issued at a price of 30 cents, 8M traditional flow-through common shares were issued at a price of 24 cents, and 4.7M common shares were issued at a price of 21 cents.

The gross proceeds from the sale of the Charitable FT shares and the traditional FT shares will be used for expenditures which qualify as Canadian exploration expenses (CEE) and flow-through mining expenditures both within the meaning of the Income Tax Act (Canada). The net proceeds from the sale of the common shares will be used for working capital and general corporate purposes. It is good to see that over 80% of proceeds goes into the ground at Gold Terra. This money goes a long way, as all-in costs for drilling is CA$200 per meter until 800 meters depth, and C$250 per meter for deeper holes, as it requires a stronger drill rig.

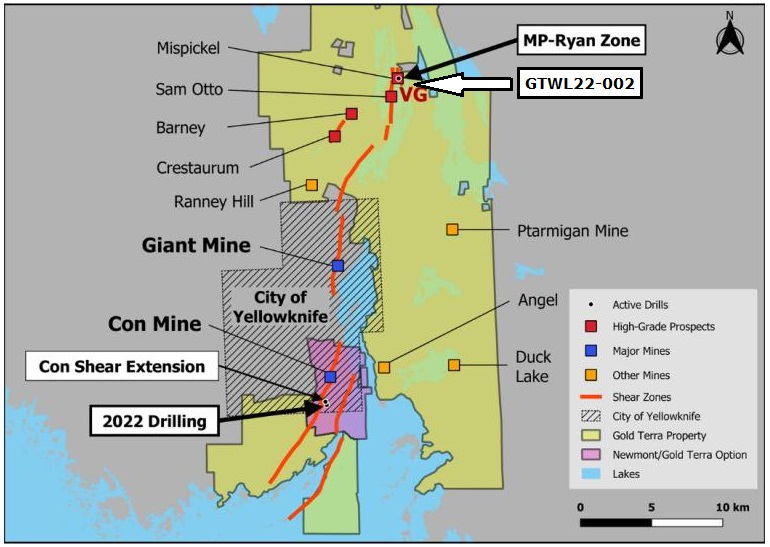

According to Panneton, net proceeds are attributed to about CA$5.1M, and the total cash position is about CA$7M now. This is good enough for completing 30,000 meters of drilling at both the Campbell Shear south of the Con Mine and the Mispickel target more to the north for the winter program.

The drilling at the Campbell Shear has been underway for quite a while now with two rigs, and regarding Mispickel, the company has recently commenced a small 4,000-meter drill program with another two drill rigs as winter is the best window. Panneton believes that earlier drilling at this target wasn’t done efficiently, and hopes to find more high-grade relatively near surface over there, which could add easy ounces to the 1.2Moz Crestaurum/Sam Otto open pit concept he has in mind. The latest results certainly indicate he is on to something of interest, as the first partial assays of hole GTWL22-002 coming back reported 4 meters @ 19g/t Au from only 20 meters depth, including 1 meter @ 73.9g/t Au.

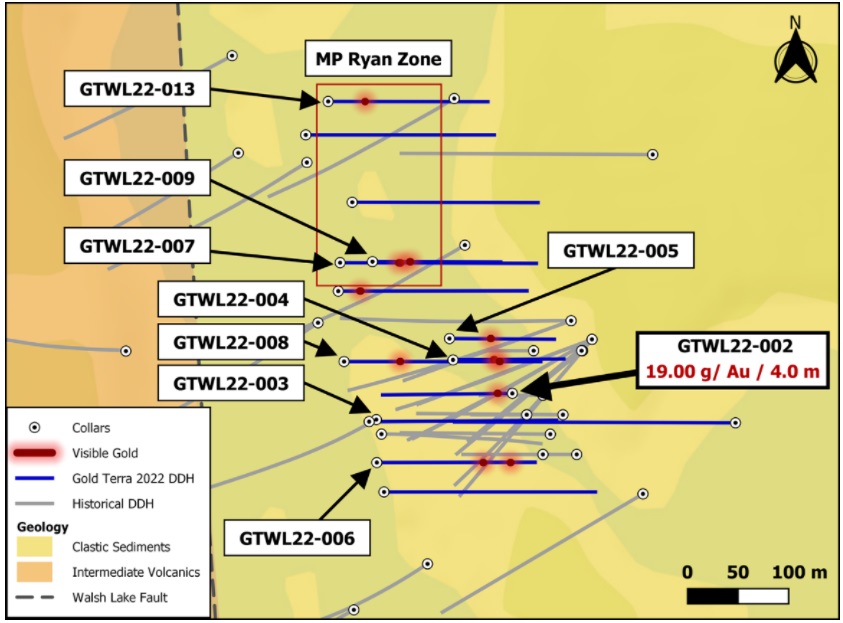

When looking at Mispickel drilling in more detail, Gold Terra is doing a small 4,000-meter winter drill program at the new high-grade MP-Ryan zone 200 meters north of the main Mispickel area. If successful, this program could eventually be expanded to 6,000 meters. Drilling is targeting high-grade trends with the objective of expanding known high-grade mineralization which is open in all directions and identifying new similar zones. To date, 13 holes covering 4611 meters have been drilled with 3,198 samples taken, indicating a sheared vertical gold structure with a strike length of 400 meters. Visible gold (VG) has been reported in 10 out of the 13 holes, and assays are pending for all holes. The collars and trajectories can be seen on the following map of Mispickel:

As can be seen, the orientation of the current drill holes is strictly east-west, as opposed to the more variable historical drilling. Since Panneton indicated that he had a different view on the strategy, I wondered about the thinking behind this. According to Panneton, this was done because winter drilling in Canada allowed them to better drill from the proper azimuth or direction to intersect the mineralized target at the best angle. Also, as winter allowed them to drill from a proper setup, Gold Terra could cover ground more efficiently.

An example of visible gold specs can be seen below:

It isn’t easy to attach certain gold values to visible gold images, but in my view it is very well possible to potentially have over 20-30 g/t Au values here.

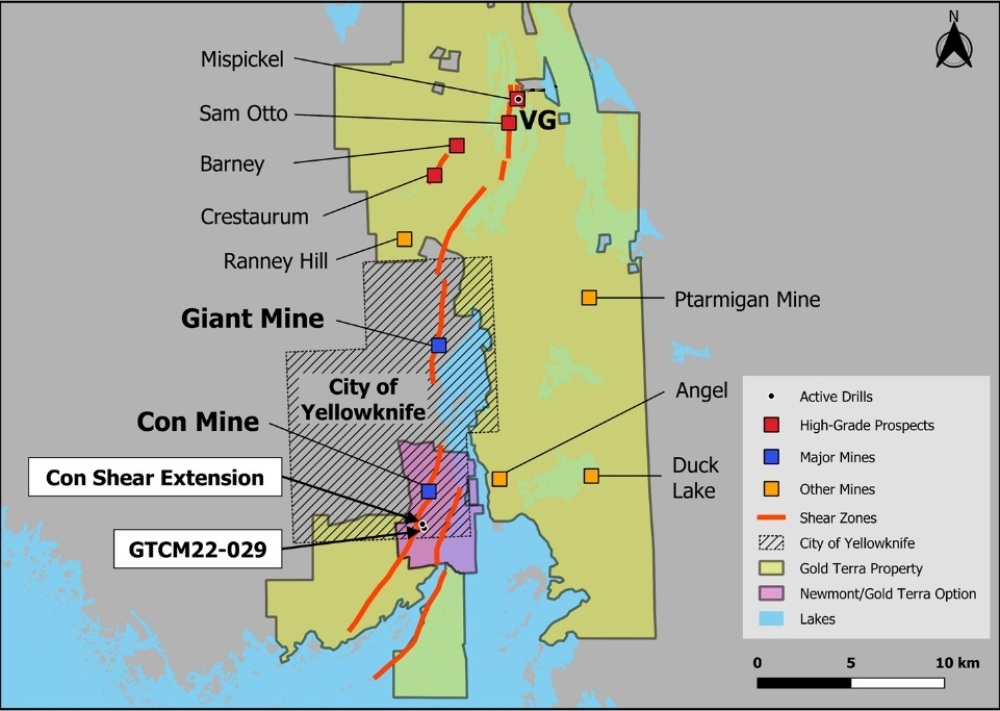

The main drill program is of course targeting the Campbell Shear. The two rigs at the Campbell Shear target are drilling south of the former high-grade Con Mine, with one big drill rig targeting the Campbell Shear at a depth of approximately 1000 meters below surface and at a 200-meter spacing. A second drill rig is allocated to test the Campbell shear, north of Yellorex zone which was not part of the agreement with Newmont (September 2020).

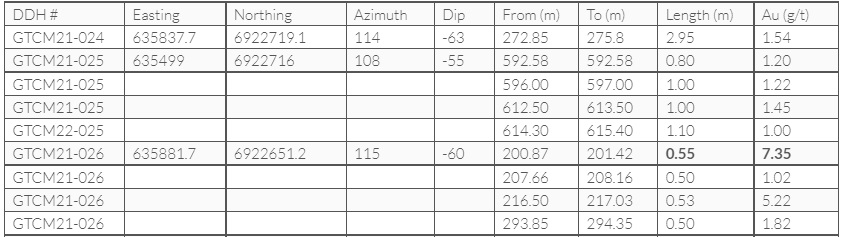

The results of five drill holes with four of them aimed at the Yellorex target (GTCM21-023 to 026) were reported in the last news release (March 15), and one (GTCM22-029) being aimed at the aforementioned deep Campbell Shear target hasn’t completed drilling yet. The drill collar locations can be seen here:

The first four holes — 023, 024, 025 and 026 — were infill drilling, but also testing the outside boundaries of the Yellorex zone (also part of the Campbell Shear). All except 023 hit some gold, although not spectacular high grades as the typical smokey quartz and strong alterations were missing. The table with full results can be observed here:

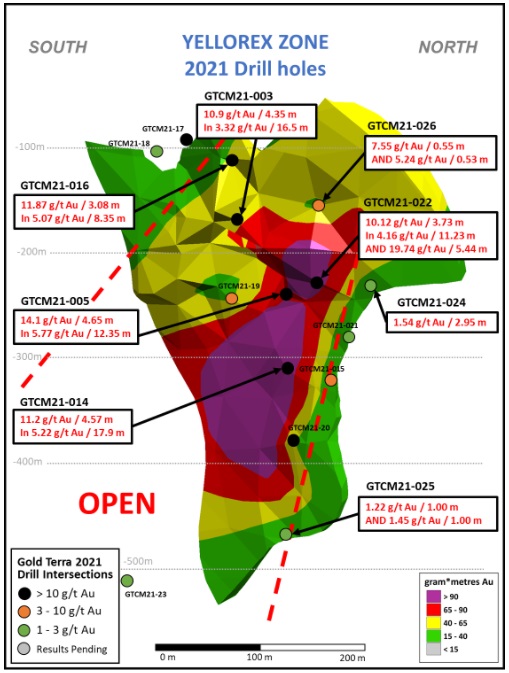

Hole 23, the deepest one so far in 2021 program, was aiming at the zone in the interpreted down plunge. The results were positive in itself as the Campbell Shear was intersected although without economic mineralization, now it is just a matter of adding more holes in the area. I wasn’t really surprised by 024 and 025 as other holes in the vicinity already indicated limited mineralized potential. I viewed 026 as a bit of an infill disappointment though, as nearby holes 022 and 003 were much better:

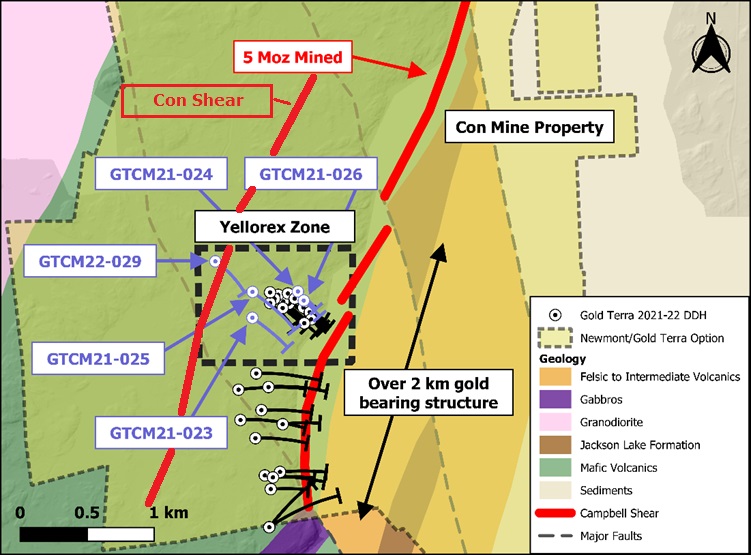

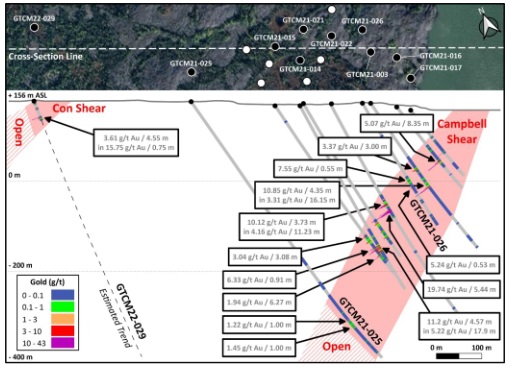

But keep in mind, the big prize on the Campbell Shear is anticipated at depth, and this is where hole 029 is targeted. Panneton thought it would be useful to include the top part of the Con Shear, as near surface ounces are always cheaper to mine than deep underground ounces, a bonus so to say. As only the first 50 meters of the hole were assayed, the result was nice with 4.55 meters @ 3.61g/t Au from 37 meters (including 0.75 meters @ 15.75g/t Au), and the drill is underway now to 1,000 meters depth, aiming at the Campbell Shear at depth:

For now the plan is to follow the mineralization at the Campbell Shear down plunge, and over the next 24 months the strategy is to increase the current extent of drilling mainly south of the original Con Mine below depths of 1,000 meters. As a reminder, see the long section below, representing the Con Mine, Yellorex and exploration targets, with the black stars indicating first drill targets, the red ones following up on this:

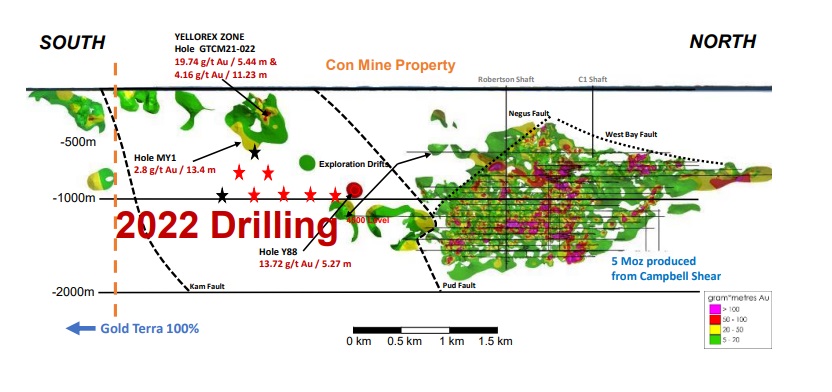

Management is intending to drill up to about 40,000 meters this year, with the objective of delineating at least a 1.0Moz high grade gold resource at the Campbell Shear at the end of 2022, and eventually a minimum of 1.5Moz high-grade gold the year after, south of the Con Mine. One more powerful rig is targeting the Campbell Shear at 1,000 meters depth at a 200-meter spacing. The second standard rig is allocated to test the Campbell Shear north of Yellorex, until a depth of 800 meters. The current cash position of about CA$7M would cover about 30,000 meters of drilling. Subject to its success, the company could be looking at raising more money for more drilling.

Also, keep in mind that there is a historic resource remaining at the Con Mine of 651koz @ 10.2g/t Au located below 1,000 meters depth, and according to Panneton, there could be about 1 Moz Au down there. It will probably take at least 10-20% verification drilling to convert this into a NI43-101 compliant resource, and this probably has to be done from surface as it is too early to start dewatering the Con Mine. According to Panneton, it is too early for dewatering and going underground, until a resource is reached to support underground drilling.

Conclusion

This is exactly what I hoped for when Panneton took over as CEO, raising another CA$5.6M as fast as he could so drilling at the Campbell Shear could be increased in 2022 with a target of 30,000 meters, even adding some Mispickel drilling to it, which already returned lots of visible gold and a first, pretty economic assay result. Yellorex drilling seems to have hit its boundaries, but the company is awaiting results of deep holes, and as Panneton and myself are anticipating that the big prize might be located right there, I’m very curious about the outcome. And remember, this exploration of the Campbell Shear is being backstopped by a solid, likely economic 1.2Moz NI43-101 resource but also a 0.65Moz historic resource at depth, with pretty good data available on it. 2022 could be an important year for Gold Terra.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

This article is also published on www.criticalinvestor.eu. To never miss a thing, please subscribe to my free newsletter, in order to get an email notice of my new articles soon after they are published.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Please note: the views, opinions, estimates, forecasts or predictions regarding Gold Terra Resource Corp.'s resource potential are those of the author alone and do not represent views, opinions, estimates, forecasts or predictions of Gold Terra Resource Corp. or Gold Terra Resource Corp.'s management. Gold Terra Resource Corp.s has not in any way endorsed the views, opinions, estimates, forecasts or predictions provided by the author.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high-quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

The author is not a registered investment advisor, and has a long position in this stock. Fancamp Exploration is a sponsoring company. All facts are to be checked by the reader. For more information go to www.fancamp.ca and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosures

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Gold Terra Resource Corp., a company mentioned in this article.