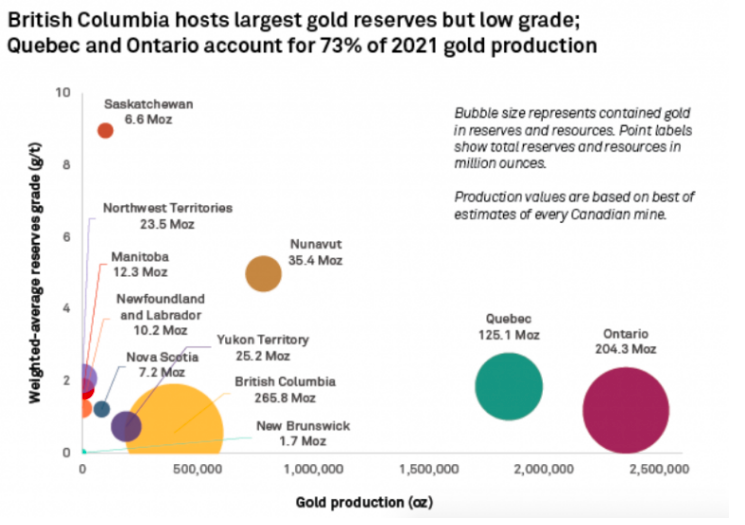

Canada’s gold production grew to 6.7M ounces in 2021, rising to 4th place after China, Australia, and Russia. The provinces of Quebec and Ontario accounted for 73% of that figure. Last year Canada was the most explored country in the world.

The best way to succeed in the high-risk/reward junior mining space is by choosing projects in great locations hosting past-producing mines. The inflation-adj. replacement cost of historical work, years of exploration and development time avoided, and operating in a brownfield setting carries considerable monetary value.

Few gold camps are as prolific as the Red Lake, Timmins, Hemlo, and Kirkland Lake mining districts. Working there, with ample infrastructure, skilled labor, service, and equipment companies is a recipe for success.

Projects that can book a million+ high-quality ounces will be highly sought after takeover targets. Those with line-of-sight to multi-million-ounce resources, especially if high-grade and/or near-surface, will attract an even larger universe of suitors.

That’s why companies like Barrick Gold Corp. (ABX:TSX; GOLD:NYSE), Newmont Corp. (NEM:NYSE), Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE), Kinross Gold Corp. (K:TSX; KGC:NYSE), Evolution Mining Ltd. (EVN:ASX), Yamana Gold Inc. (YRI:TSX; AUY:NYSE; YAU:LSE), Centerra Gold Inc. (CG:TSX; CADGF:OTCPK), Equinox Gold Corp. (EQX:TSX; EQX:NYSE.A), Alamos Gold Inc. (AGI:TSX; AGI:NYSE), and New Gold Inc. (NGD:TSX; NGD:NYSE.MKT) are active across Ontario.

AngloGold Ashanti is a cornerstone investor in Red Lake’s Pure Gold Mining. Finally, First Majestic has a substantial streaming agreement in place with First Mining.

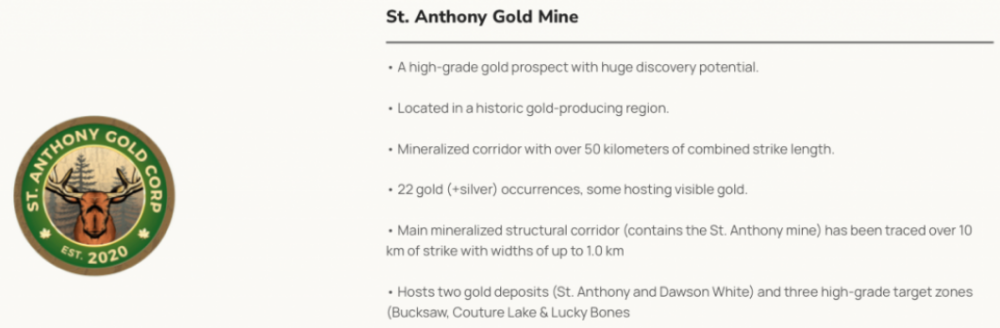

I believe that St. Anthony Gold Corp. (CSE: STAG; OTCQB: MTEHF) has all the attributes of a compelling gold junior. A company that could deliver outsized capital gains as investors discover the story and management executes on key objectives. A company with a Pro-forma Enterprise Value (EV) {market cap + debt – cash} under CA$3M.

Ontario is known for world-famous low-grade deposits, but also pockets of high-grade in places like Red Lake. Imagine enjoying the regional infrastructure, labor pool & mining services brought about by prolific lower-grade mines, but in a high-grade setting.

That’s what St. Anthony Gold is looking at. It’s earning into two very promising projects. The St. Anthony Gold project hosts multiple historical operations spanning 233 contiguous claims (4,224 hectares) with 22 known gold occurrences.

Four historical operations sit on the St. Anthony Gold project. Although slowed by COVID-19 restrictions, last year management was able to complete half of a planned Phase 1 drill program. Press releases have reported, “exceptional visible gold showings in all drill holes.”

The Company also owns a 50% interest (soon to be 70%) in the 11,700 hectare Panama Lake project, contiguous to Barrick’s JV with Kenorland Minerals and south of First Mining’s 4.9M oz., PFS-stage, Springpole project. Past exploration has been done by Goldcorp, Noranda, Benton Resources & St. Anthony.

There’s huge & renewed interest in the area surrounding the Company’s Panama Lake. In December, Kinross offered to acquire Great Bear Resources [GBR] for CA1.8 billion. It was reported that five Majors were pursuing GBR. Those five and more could have an interest in Panama Lake. Barrick has invested in companies surrounding Panama Lake including; Red Lake Gold Corp., Kenorland & Dixie Gold.

Make no mistake, St. Anthony Gold Corp. is high risk, but some of the heavy lifting has already been done. Ontario hosts several prolific gold mining districts, permitting is straightforward, with no serious weather, power, water, elevation, First Nation, or geopolitical issues.

Management has been re-assaying the historical core, leading to the announcement of a revised interval of 3.7 m of 169 g/t gold (625 gram-meters!). given it was not a new discovery, it didn’t attract the attention it deserved. How strong is 625 g-m?

It would have been in the top-25 across Canada in 2021. [source: Miner Deck]. All the historical drill core, and there’s a lot of it, stands to potentially benefit from re-assaying.

In speaking with CEO Peter Wilson and consultant Allen J. Raoul P Geo, it seems that historical exploration was done sub-optimally. Prior drilling focused on identifying the continuity of lower-grade mineralization, but failed to systemically look for high-grade ore shoots.

That’s why there’s an opportunity to pick up ounces, at a fraction of the cost of drilling, by re-assaying historical core.

After three Phases of drilling are completed & logged + ongoing re-assaying of core, the Company hopes to deliver a NI 43-101 compliant mineral resource estimate of up to 1M ounces (net to the Company).

Management has not given guidance on the anticipated resource grade, but there’s reason to believe it will be good due to the historical production of 5.95 g/t gold.

Importantly, depending on how the re-assaying work goes and based on new drill programs on untested zones, that targeted 1M ounce goal could grow.

Management believes there’s a possibility of a multi-million-ounce resource, (not incl. anything found at Panama Lake), more than enough to build a standalone mine.

CA$1M is currently being raised, and several million more will be needed to prudently advance the Company’s key initiatives. Due to a reverse split in November, there are ~52.5M shares outstanding, (pro forma for an upcoming share issuance to the vendor of the St. Anthony project).

Management is exploring ways to raise some of the capital without issuing new shares, but there are no assurances that this can be achieved on attractive terms.

As mentioned, some of the heavy lifting is behind us. We know for certain there’s gold on St. Anthony’s namesake property. That’s more than can be said for many pre-discovery gold juniors, some of which have properties in far less hospitable places than Ontario.

The reason I see true blue-sky upside is twofold. First, the EV is under CA$3M. After considering a Company’s projects, people & jurisdictions, valuation is a critical step in assessing speculative investments.

If St. Anthony can deliver 1M net ounces, the Company’s share price should soar. Moreover, gold prices are strong and likely to remain so. Today’s $1,851/oz. is nearly 50% above the average gold price from 2013 to 2019 of $1,272/oz. (macrotrends.net).

If 1M net ounces can be delineated, that would demonstrate management’s understanding of the project’s geology and structure, possibly giving investors line of sight to a lot more ounces.

The Lucky Bones and Couture Lake targets represent a mineralized structural corridor that extends over a 6+ km strike length with widths of 200-400 m (open for an additional 7 km to the south). The corridor contains numerous shear zones and quartz veins (8-10 m widths). There are historic shafts, trenches & pits along this trend.

Lucky Bones saw five holes drilled in 2013, three hit visible gold. Some think the mother lode could be sitting at the bottom of Couture Lake. Mining operations in 1940-41 were headed in this direction.

Past sampling and trenching at the Bucksaw target returned values of up to 24.1 g/t gold. Prospecting in 2011 identified historic trenches with grades of up to 12.95 g/t gold plus additional pits in shear zones with grab samples up to 19.6 g/t.

Near-term catalysts will generate news flow for months to come. Assay reports from drill program Phases 1, 2 & 3, as well as announcements of ongoing results from re-assaying existing drill core.

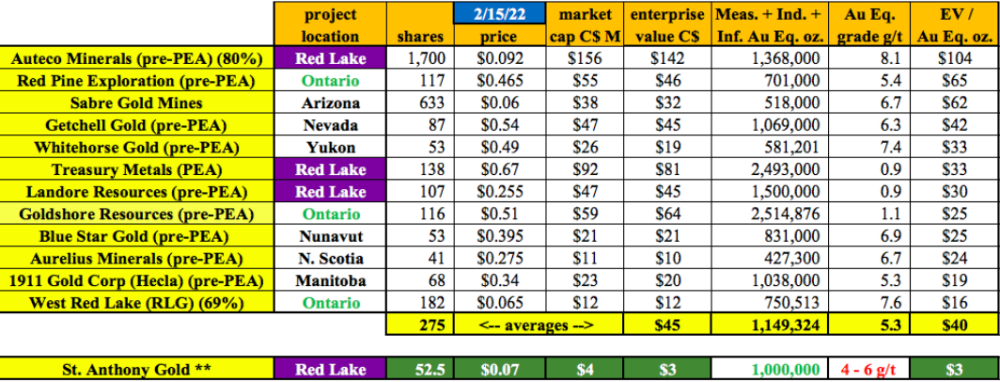

It would be hard to find a better gold junior in Canada, with such bright prospects, trading with a market cap of < $3M. Looking at nearby companies in Red Lake; Auteco Minerals has an 80% interest in 1.71M Inferred ounces grading 8.1 g/t gold. Its market cap is CA$140M.

Landore Resources has a reported 1.5M ounces @ 0.90 g/t gold and a market cap of CA$47M. Treasury Metals has a PEA-stage project with 2.5M ounces at 1.0 g/t gold and a market cap of CA$97M.

Those three companies are valued at between CA$30 & CA$104 per troy ounce in the ground. If St. Anthony Gold Corp can deliver 1M ounces (net to the Company), its market cap should rise much higher, subject to obtaining the necessary funding along the way.

GBR is being taken out by Kinross at ~CA$150/oz. (assuming a 12M ounce resource, there’s no maiden resource yet)… This goes to show how much a large high-grade deposit in Ontario can be worth.

Readers are reminded that commentary about relative value is for illustrative purposes only. St. Anthony Gold Corp. does NOT have a NI 43-101 compliant mineral resource estimate at this time.

Management expects to have a lot of news to report this year. Once investors recognize the cheap valuation, prime jurisdiction, and strong mgmt. team, buying shares at CA$0.07 or CA$0.075 could be a distant memory.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

Disclosures: The content of this article is for information only. Readers understand & agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about St. Anthony Gold, incl. but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of St. Anthony Gold are highly speculative, not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was originally posted, Peter Epstein owned shares of St. Anthony Gold and the Company was an advertiser on [ER].

Readers should consider me biased in my view of the Company. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events and news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.