For the past few years I've been saying that First Cobalt Corp. (FCC:TSX.V; FTSSF:OTCQX; FCC:ASX) offers investors pure-play exposure to the paradigm shift from internal combustion engine cars / trucks / buses, etc. to electric vehicles (EVs), arguably the most prominent investment narrative of the decade.

The EV revolution was kicked up another notch last week as the U.S. announced a US$174B program devoted to EV rebates, charging stations and battery plants. Last month, lithium major Albemarle raised its lithium demand estimate for 2025 by 40%, which obviously bodes well for cobalt demand.

The EV revolution was kicked up another notch last week as the U.S. announced a US$174B program devoted to EV rebates, charging stations and battery plants. Last month, lithium major Albemarle raised its lithium demand estimate for 2025 by 40%, which obviously bodes well for cobalt demand.

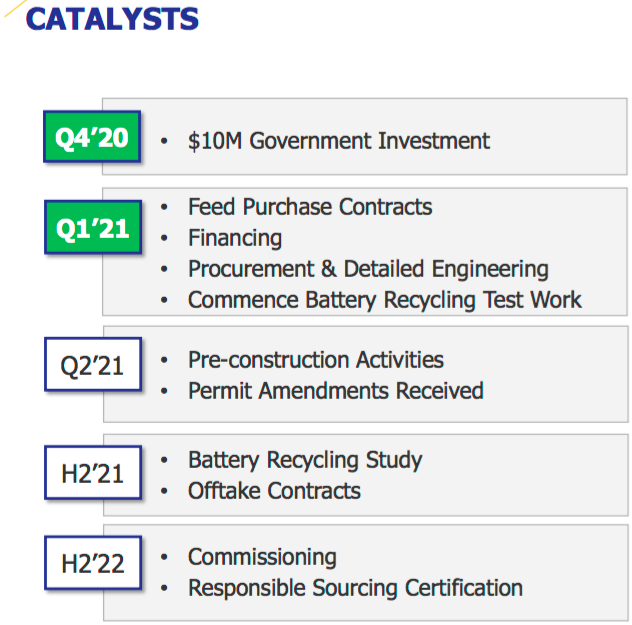

First Cobalt will be ready to meet the challenge. Management continues to deliver on promises made. In the past week there were press releases on debt funding to restart the company's 100%-owned cobalt refinery and on an off-take arrangement for up to 100% of finished cobalt sulfate. In the past year, the following de-risking initiatives and market changes have occurred:

i. feedstock secured, ii. off-take secured, iii. on track to fully-funding US$60M cap-ex hurdle by June 30th, iv. strong progress on significant ESG initiatives, v. nascent surge in global EV sales, vi. increased cobalt prices (double 2020's lows), vii. demonstrated provincial and federal government support. {see latest corporate presentation}

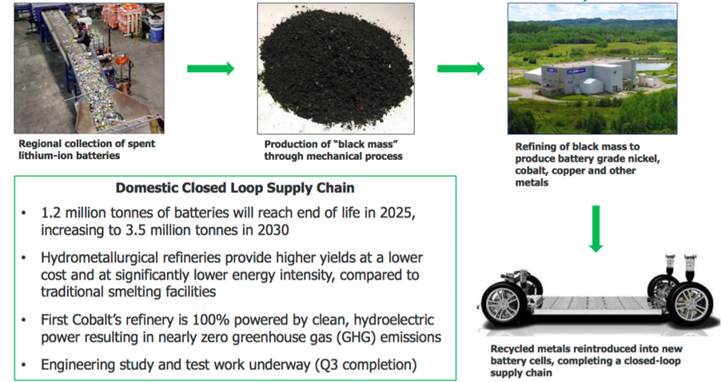

Recycling EV batteries could make this cobalt story extraordinary

I remain bullish on ethically sourced, battery-quality cobalt sulfate processed outside of China. However, First Cobalt now offers that opportunity and more. Recycling "black mass" could be the next big step for the company.

What's black mass? After removing things like plastics, copper and aluminuma sludgy mixture of nickel, cobalt and lithium (and other materials) is left behindthat's black mass.

First Cobalt is graduating from a pure-play Cobalt junior to a battery metals producer (cobalt in 2H 2022, plus recycled metals thereafter).

Processing black mass would greatly enhance and diversify the company into nickel and lithium (and possibly manganese and graphite). Importantly, the same methodology would apply (if technically feasible) to recycling REEs and PGMs.

This could be very impactful on the economic potential of the refinery, and it would bolster the company's already considerable ESG credentials {see slide below}. The Refinery's ESG profile and central north American location make it an incredibly strategic asset that could attract buyout interest.

Many plan to recycle, very few have a hydro-metallurgical refinery!

First Cobalt has the better mousetrap for recycling black mass. Its cobalt refinery will be able to run multiple circuits at the same time. Therefore, in addition to 55 tonnes/day of cobalt hydroxide (feedstock) being refined into battery-grade cobalt sulfate, the refinery could be retrofitted to also process black mass. A preliminary study of this exciting opportunity will begin in July.

Hydro-metallurgical refineries provide higher yields at lower cost. They use significantly less energy compared to conventional smelters, making them more environmentally friendly.

The economics could be attractive as upfront cap-ex would be fairly low, and op-ex would benefit from shared expenses with the cobalt refining segment. Much of the overhead of this expansion would already be in place, most notably a senior management team and refinery plant workers.

Importantly, the refinery building would house the new battery metal circuits, and some existing equipment could be repurposed to support recycling operations.

What might First Cobalt's 55 tonne/day cobalt operation be worth?

Finding companies with sustainable, high-quality, recurring cash flows is the holy grail of investing. Companies with these attributes are handsomely rewarded in the market.

For example, gold/silver royalty and streaming companies are trading [on average] at a ratio of ~25x trailing 12-month EBITDA. Cannabis names are valued at an average of ~25-40x trailing 12-month EBITDA. Drone companies, at ~20-25x. Lithium giants Albemarle and SQM, both around ~25x.

Assuming that First Cobalt can achieve a 10x multiple of its 2023e EBITDA (~C$50M as per two analyst estimates), and discounting that C$500M valuation back two years at 8% equates to C$0.79/shr. (on the current share count, adjusted for pro forma debt of C$70M). Note: {indicative C$0.79/share value does not include potential cash flow from recycling}.

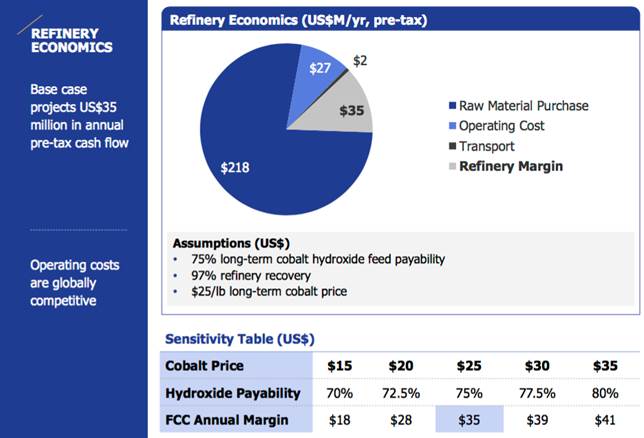

The EBITDA margin for primary cobalt refining is expected to be 10% to 15%, depending on relative prices of cobalt hydroxide feedstock and finished cobalt sulfate. The margin from recycling black mass could be meaningfully higher. Soon to list on NYSE, Li-ion battery recycler Li-Cycle expects to have an EBITDA margin of 60%.

Combined, the margin from refining and recycling would certainly benefit from cost-sharing synergies. A 10% company-wide margin gain on a recycling segment that's one-third the size of the refining business would increase projected annual EBITDA from ~C$50 to ~C$92M.

At a 10x EBITDA multiple, that would be an incremental C$420M in enterprise value, not including a moderate amount of debt and/or equity to fund the expansion. Significant EBITDA from recycling would not arrive by 2023, but perhaps in 2024 or 2025.

However, there's substantial blue-sky upside to the valuation, as each 1x (adds / subtracts) ~C$0.10/share All else equal, at a 12x multiple, the indicative share price increases from C$0.79 to C$1.00. Note: {none of these calculations are price targets, they're thought experiments}.

The recycling opportunity highlights the tremendous underlying value of First Cobalt's refinery. In 2012, Hatch valued it at US$78M. Adjusted for inflation, that's about US$93M today. And, that figure was for a smaller, less capable refinery than the one the company plans to restart in 2H 2022.

Adding the US$60M being invested into upgrading and optimizing the refinery to nameplate capacity of 55 tonnes/day, the replacement value of this scarce asset is more like US$153M = ~C$192M.

Compare that to First Cobalt's Enterprise Value {market cap + debt cash} of ~C$150M. I strongly believe that the C$192M figure should begin to place a floor under First Cobalt's valuation.

The refinery's strategic location is critically important, situated in Ontario, poised to supply domestic markets and sales into the U.S. For example, it's well within rail and trucking distance of major North American auto hubs in Michigan (USA), where 21 global OEMs have a headquarters or technology center.

Conclusion

Few investment themes are as certain (in my opinion) as the transformative move from fossil fuel powered to electrified transportation across the globe.

Not every EV start-up will succeed, there will probably be some epic failures. However, First Cobalt Corp. (TSX-V: FCC) / (OTCQX: FTSSF) is the opposite of a precarious EV start-up. It's a picks and shovels play on this highly compelling thematic. Adding a recycling component would be icing on the cake.

Once in production and generating cash flow, the market will see the full potential of the company's refinery. In addition to tangible hard asset value, the refinery has scarcity value as the only one of its kind in North America. As a result, First Cobalt's business will enjoy barriers to entry that virtually no other EV start-up or battery metals junior will be able to match.

I believe that First Cobalt has enough upside to make it sexy and exciting, but far less downside than hundreds of battery metal / EV start-up companies. This suggests the company could become a prime takeover target. I doubt any takeover would occur at < C$1.00/share.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Cobalt Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Cobalt Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares of First Cobalt Corp., and the Company was an advertiser on [ER].

While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.