I don't know about you, but if you want my unfiltered opinion of the Year of Our Lord 2020, I would rank it in at least the bottom 2% in many respects, but only in terms of a sixty-seven year sample sizeand it has nothing at all to do with markets or money.

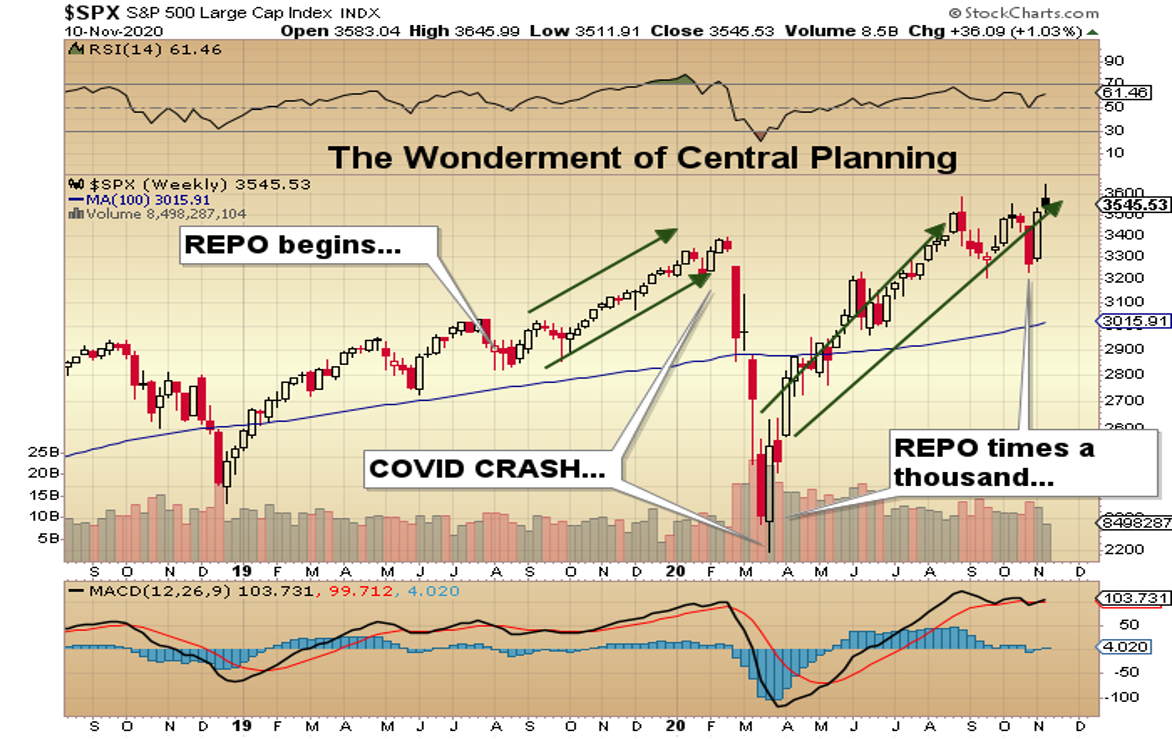

At this time last year, I was writing incessantly about Fed Chairman (ex-stock salesman) Jerome Powell's late summer "pivot," where he decided out of the blue to end "balance sheet normalization" (boasted of by Bernanke and Yellen at every turn) in favor of "liquidity injections" otherwise known as "REPO." It would seem that more than a few of the larger hedge funds had found themselves somewhat under water thanks to accelerated weakness in the corporate bond market, with particular emphasis on the high-yield or more appropriately named "junk" bond market. Now, nobody knows exactly what Powell saw on the horizon, but he did a one-eighty and went from liquidity draining to liquidity sloshing in one dramatic policy-altering keystroke.

I thought at the time that, as always, it had to be related to the credit markets, because literally everything revolves around the actions of the U.S. Federal Reserve, be it currencies or commodities or common stocks. It continued well into the New Year, despite the indignant protestations of Powell and Kudlow and Trump, who all deemed these actions as "normal" while insinuating in Monty Python-esque fashion that we all should "move on" because there was "nothing to see here." After all, what do a few hundred billion dead presidents matter in the context of a multitrillion-dollar Ponzi scheme?

As we enter the proverbial "home stretch" of 2020, it is obvious that the central planners in Washington and Wall Street have indeed "moved on," from pre-election jitters of a Biden victory and attendant market crash to a completely different narrative of V-Shaped, vaccine-triggered recoveries in the global economies. With the S&P now at record highs and the Dow within spitting distance of 30,000, the thundering herd is being driven back into stocks with a vengeance not seen since Henry Blodgett was pumping Petfood.com to a swarm of salivating newbies back in 1999.

In fact, the mania once again infecting the basement-dwelling masses of day-trading universe is a near-clone to that fateful period when Nortel was ascendant, and AOL was worth more than Time-Warner. In a manner of perversity not seen since the Marquis de Sade was testing out his latest model whip, stock investors are in heaven while the unemployed "deplorables" (who can't even spell "capitalism" let alone practice it) are eating out of dog food cans and throwing grenades at the TV screen, at the beaming, gloating faces of CNBC anchors.

We gold bugs, swarming the landscape with unabashed "I-told-you-so's" back in the summer, are now in full wound-licking mode as the hubris so abundant in July has now given way to the sadly familiar feeling assigned to the holders of empty bags and children with lumps of coal in Noel stockings, feelings we endured so painfully from mid-2011 to mid-2020.

The problem for the precious metal legions going into the home stretch is that last summer, a vast pool of seasoned generalists, unskilled in the idiosyncrasies of precious metals investing, came charging into the gold and silver markets, daring to boldly go where few men had gone before. The skeptics (including Warren Buffett), driven by herd mentality into Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) and Newmont Corp. (NEM:NYSE) and GDX and GDXJ, finally chomped down on that Smith & Wesson projectile and loaded their forward hatches with all shapes and sizes of gold and silver miners, driving the HUI to the highest level since July of 2012.

Sadly, as we approach the terminus of the 2020 performance year, a large number of these elephantine money managers are dangerously close to falling into the fourth quartile in performance, which means that they are also dangerously close to seeing a disastrous exodus of their precious AUM ("Assets Under Management"), should they be bold enough to ride out these positions into 2021.

Also under pressure are seasoned precious metals investors, many of whom are enjoying banner years, having been long the space at much lower entry levels going into last January. In fact, profits taken in the mid-year central bank print-athon have left many of us with huge tax bills when next April rolls around, unless we find at least a few losers to pitch overboard to reduce the tax bite.

My point is this: Whether it is the newbies underwater or the oldies with big potential tax bills, there are potential sellers everywhere. If the precious metals sector cannot scramble its way to a bid and quickly, this fourth quarter home stretch outperformance by the S&P may force a wave of liquidations in the bigger, more visible precious metals (PM) names and in the physical metal exchange-traded fund (ETF) proxies as well. This could start a chain reaction of selling that could easily morph into a rout.

The reason that I have chosen to hide in the anonymity of the micro-cap developers is that they have yet to find their way into any of these larger generalist portfolios, and therefore are somewhat sheltered from the same performance anxiety "limpicity" that might be about to infect the senior, intermediate, and junior producers.

I am constantly bombarded with e-mails and tweets from a myriad of gold and silver experts trumpeting the wonders of the "fundamentals" for gold and silver having "never been better." I read what they write and I listen to what they say ("preach") in podcast after podcast and webinar after webinar, and finally end up screaming at the walls, begging them to save their sermonizing about conditions that have been glaringly obvious for over two decades but which only recently have been reflected by price.

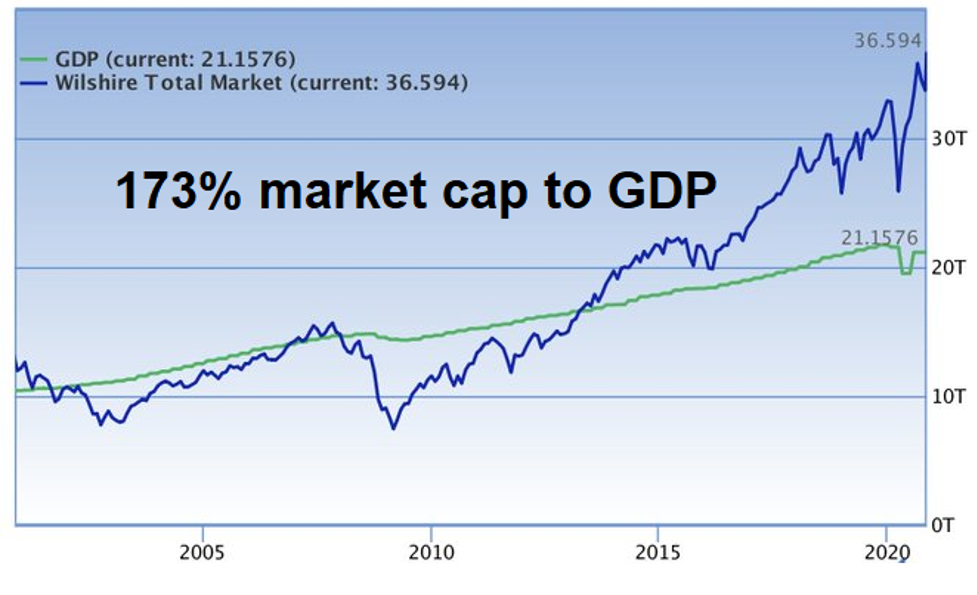

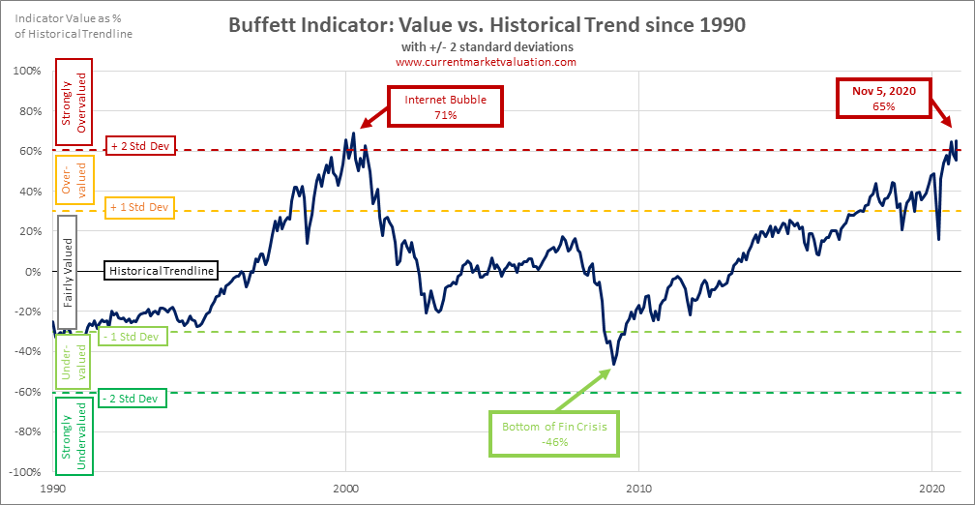

With over half of the world in a depression and the other half in recession, stocks the world over are priced as if the global economic lockdown never occurred. We are at 173% market cap-to-gross domestic product (GDP) levels, the second highest in history and where the Buffett Indicator is forecasting a negative return for stocks for years out.

You can talk about "gold market fundamentals" until you are blue in the face, but if investors are willing to buy common stocks at levels of overvaluation approaching the top in 1999 because the "Fed has their backs," then the opposite must be true for gold and silver, because the Fed most certainly has a knife in our backs.

You will not in your lifetime find a more fervent advocate of sound money than this author, but I have too many scars on this fragile psyche to plunge with blind abandon and selfless loyalty to the premise that gold and silver are deities to be worshipped, stored and never traded. Gold and silver do not by themselves pay one's electric bill or make one's mortgage payment, and taken as a trading vehicle over a term decidedly less than a lifetime, failure to heed warnings can cost a great deal more than loss of profits.

When I was a young lad, I used to love watching the thoroughbreds at Woodbine, in northwest Toronto, as they came thundering around the Clubhouse turn heading into the home stretch. I was there in 1964 when Northern Dancer won the Queen's Plate by seven-and-a-half lengths (without breaking a sweat), and I can tell you that there is a reason it is called "The Sport of Kings." The excitement is palpable.

So, as I look out at the barometric pressure for gold and silver, I detect a distinct possibility (as opposed to probability) of storm clouds forming. What I wish to see is gold trading back over USD$1,900/ounce quickly, and silver through USD$26/ounce as that happens. Conversely, what I do not wish to see is a sharp breakdown of the USD$1,850 level for gold, because that would invite a sharp drop to the 200 daily moving average (dma) of USD$1,785. While still representative of highly profitable levels for the producers, the psycho-trauma of a break like that would undoubtedly take the miners downand it would surely snowball as the latecomers sprint to jettison their losers in fits of anger and disgust.

The home stretch for the calendar year 2020 should favor the micro-cap juniors (operative word being "should"), such as the names covered in the subscriber section of the GGM Advisory. That said, it does not necessarily follow that prices will zoom into the New Year as there are many crosscurrents affecting "flow" (sector reallocations/tax/macro/politics).

As tumultuous as 2020 has been, when I look out 1224 months into the future, I do not see any indication whatsoever of a disinflationary "Goldilocks"-type scenario unfolding. The "not-too-hot, not-too-cold" economic setting is but a relic in the desert of past bull markets, because the central bankers have already pledged to allow inflation to run "hot." The arrogance of these clowns, actually believing that they can control the ebb and flow of wholesale and consumer prices, as if inflation rates could be pegged as they do administered rates, verges on the absurd.

There is a saying going back many decades that states "inflation is like toothpaste; once out of the tube, it is impossible to get it back in." Jay Powell and Co. would be well advised to learn a little hubris when toying with people's living costs, because there are historical precedents that speak volumes.

"Furthermore, significant resentment was felt by the poorer members of the Third Estate (industrial and rural labourers), largely due to vast increases in the cost of living. From 1741 to 1785, there was a 62% increase in real cost of living." This quote is an excerpt from the Wikipedia explanation of the major cause of the French Revolution of 17891799, which saw the removal of the monarchy and most of the upper crust nobility by the "Third Estate" comprised of peasants and the bourgeoisie.

I have long held that recent civil unrest in the U.S. has a great deal more to do with living standards then it does racial equality or civil justice. The elite class, led by the power brokers of Washington and Wall Street, are the 2020 version of the monarchy and nobility of 17th-century France; the Black Lives Matter (BLM) and Antifa movements are like the 1789 meetings of the "Estates-General" (clergy, peasants and bourgeoisie) in Paris. We all know how that ended.

But in the end, what caused the civil unrest was a sharp rise in domestic inflation brought about the massive debts incurred by the monarchy in its involvement in foreign wars, which included the U.S. War of Independence.

Mark Twain is reputed to have coined the phrase that "history may not repeat itself, but it often rhymes." I would submit that central bankers the world over would be well counseled if they were to remember that phrase and if not understood, quickly enroll in a few night courses in "political poetry."

To describe the post-election U.S. market behavior as "bizarre" is an understatement. In forty-three years of covering markets, I have never seen the risk-reward setups as skewed as they are now. The precious metals have the most bullish long-term setups that I have ever seen, with real interest rates deeply in negative territory and an uber-dovish Fed, while common stocks are completely the reverse. It is maddening to watch some of these growth stocks remain elevated against the backdrop of deteriorating income statements and eroding balance sheets, while the gold producers are sinking against the backdrop of accelerating free cash flow and increasing dividends.

The Wharton School financial training I had back in the 1980s, in today's markets, would qualify me as a barista or a Chippendale dancer, but certainly not as a "strategist." Makes me want to hum my cappuccino-maker at the quote monitor (without disturbing my bowtie or collar cuffs).

Originally published Nov. 14, 2020.

Follow Michael Ballanger on Twitter @MiningJunkie.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.