Note: Subsequent to the publishing of this article, management announced a modest CA$2 million (CA$2M) equity capital raise.

First Cobalt Corp. (FCC:TSX.V; FTSSF:OTCQX; FCC:ASX) announced a strategic review of its considerable silver prospects in Canada. Management and investors have been so laser-focused on restarting their 100%-owned cobalt refinery (with Glencore International Plc's [GLEN:LSE] help) that the +133% gain (!!; from $12 to $28/troy ounce) in silver since the COVID-19-induced mid-March low has caught many by surprise.

Management very candidly stated that it's considering spinouts, divestitures, farm-outs and joint ventures (JVs) of most or all of its silver assets. There are a number of possibilities as to how this might unfold. It seems like a very prudent strategy, sell the hot commodity (silver) and hold the metal that might have greater upside from today's levels.

Depressed cobalt prices are widely expected to double by 2022. Will silver double to $56/ounce? I don't know. More about silver in a moment, but first an update on cobalt fundamentals.

Precious metals have soared; could cobalt be the next metal to shine?

According to Fitch Solutions, cobalt production in the Democratic Republic of Congo (DRC), the world's largest producer, is expected to decline by 25% this year, mostly from the ongoing idling of Glencore's Mutanda copper-cobalt mine in November 2019 (planned shutdown for two years). Mutanda accounted for a quarter of the DRC's output last year.

Unlike most copper-cobalt mines, which are heavily skewed toward copper, Mutanda is evenly split between the two metals. This makes the prevailing cobalt price much more important. I doubt the mine would incur the large amount of time and expense required to reopen at a cobalt price below $20/lb.

Cobalt prices are two weeks into a modest recovery, up from ~$14 to ~$15/lb. While nothing to write home aboutcertainly nothing like silvercould this be the start of something bigger? Again, I don't know.

However, I continue to observe global announcements of giant countrywide infrastructure programs, many centered on the electrification of transportation, which is cobalt-intensive.

Silver is up +133% from its mid-March low of $12/lb.

Returning to silver, management assures me that the company will not be dumping assets. It's a seller's market; interested parties are approaching First Cobalt unsolicited. Having said that, if some cash does come through the door later this year, that would lessen the need for new equity capital.

Even by monetizing a portion of the silver assets, management can potentially mark-to-market the remaining assets, thereby participating in silver's bull market run.

Trent Mell, First Cobalt president and CEO, commented, "Silver has more than doubled (+133%) from its March lows due to avid investor interest in precious metals. We have several high-grade silver targets that are not receiving value in our asset portfolio given our focus on cobalt. The Cobalt Camp includes some of the highest-grade historic silver mines in Canada and First Cobalt has demonstrated that potential for new silver discoveries exists beyond historically mined areas.

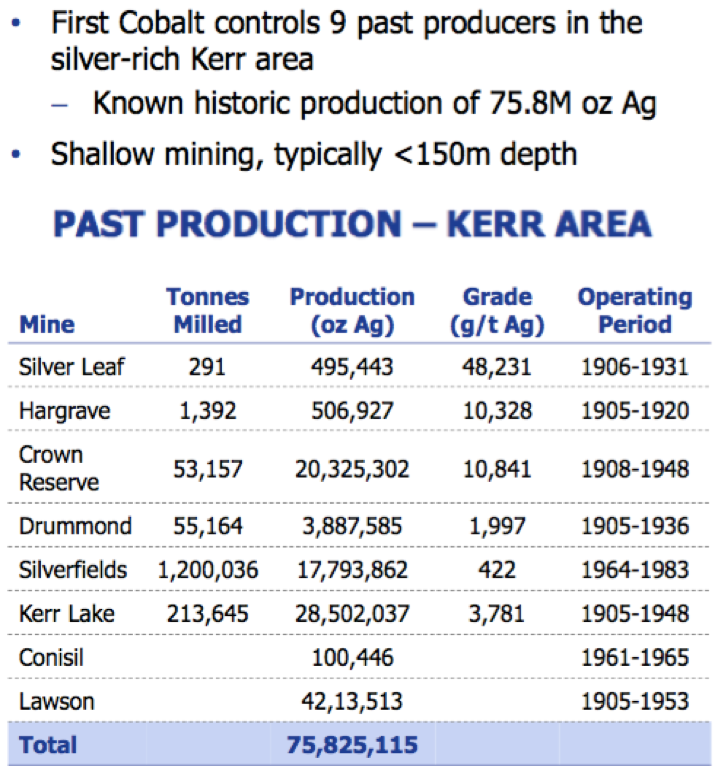

"Due to unsolicited expressions of interest, we have started a review of non-core silver assets. The Kerr Lake area is a prime example given that First Cobalt has combined eight adjacent historic mines that produced 50M ounces more than 60 years ago. We may seek to divest of silver-rich assets or JV them if terms are attractive."

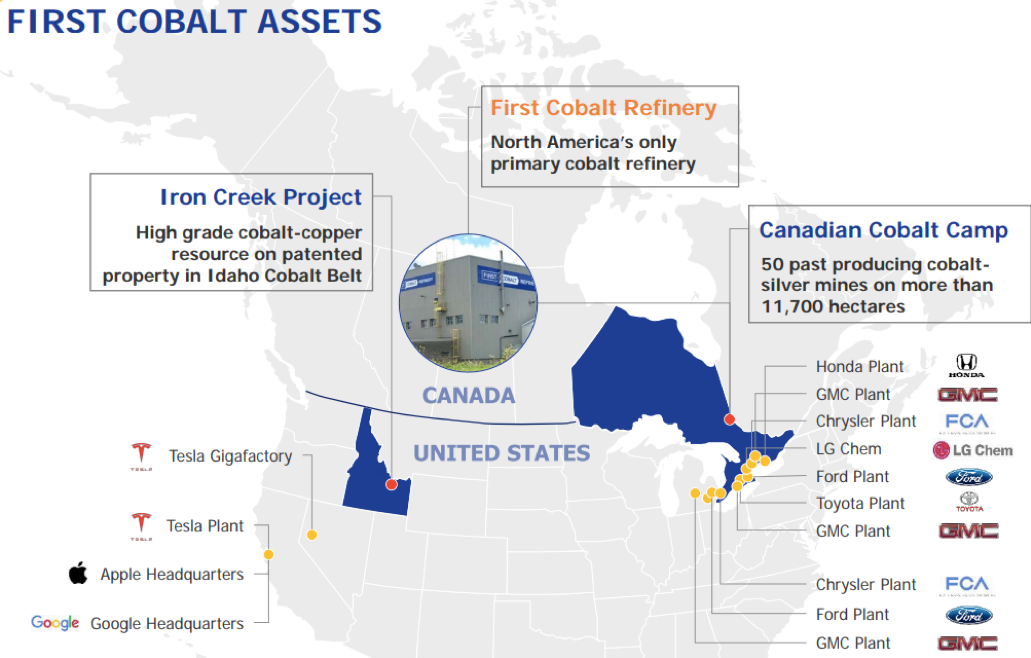

First Cobalt: largest property portfolio (11,700+ hectares) in silver-cobalt camp

Management states that the company holds the largest land package in the historic silver-cobalt mining camp, hosting >50 past-producing mines. Total output was >600 million ounces (Moz) of silver and 50M pounds of cobalt from 1903 to 1989.

First Cobalt has amassed a 11,700-hectare-plus patented land and mineral claims footprint. The next largest landowner in the district, (~7,800 hectares), is Canada Cobalt Silver Works (CCW:TSX.V), a company with a market cap of CA$56M.

Not only does First Cobalt have a dominant land position, it has the only district-scale 3D geological model. The model was developed from historic maps and data, new geophysical surveys, historical and new diamond drilling. The mineralized zones that have been found are mostly below 150-meter depth.

Nearby, Teck Resources Ltd. (TCK:TSX; TCK:NYSE) mined to a depth of 300 meters, and produced >17Moz of silver, ending in 1989. And, in the southern portion of the silver-cobalt camp, new zones of mineralization were intersected outside of the historic Frontier and Keeley mine areas, that produced >19Moz of silver. Exceptionally high-grade vein-style mineralization, mined at up to 185 oz/t silver (5,200 g/t).

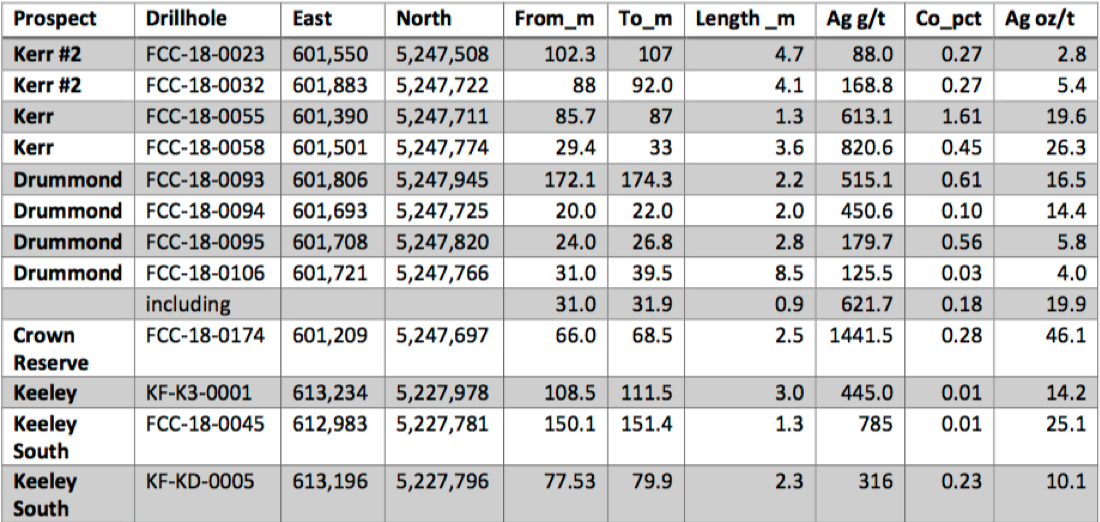

The company completed a $10 million exploration program including historic data compilation, bedrock mapping, prospecting, geophysical surveys and >30,000 meters of drilling across 14 separate sites. Some of the best silver intercepts were found in the Kerr Lake area, which encompasses eight historic silver mines that produced >50Moz of silver and 900,000 pounds of cobalt.

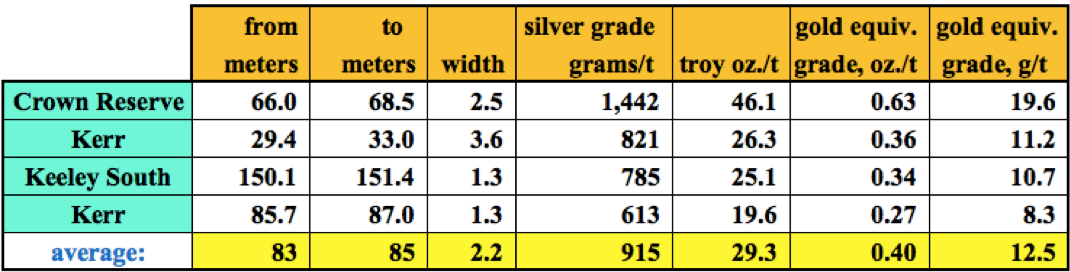

First Cobalt's drill results, >30,000 meters, show serious high-grade Ag!

Management is not cherry-picking one or two strong intervals, there's a lot of high-grade silver across First Cobalt's extensive property package. The following intervals were mentioned in today's press release (Ag = silver; Co = cobalt).

The highest-grade of 1,441 g/t silver equates to 46 troy oz/t, with an in-situ value of $1,295/t. That's 19.6 g/t gold equivalent (gold eq), and it's all near-surface!

The average grade of the four best intervals shown below is 915 g/t silver = 12.5 g/t gold eq, at an average depth of 84 meters. Note: These high grades are not indicative of what the overall grade of these zones might be.

In looking at pre-PEA (preliminary economic assessment) silver juniors, they trade at an average of about US$1.50 per ounce in the ground. If an experienced, well-funded company were to take over First Cobalt's silver interests, could it delineate tens of millions of ounces? I think so.

In the right hands, 20Moz could be worth ~CA$40M; 30Moz worth ~CA$60Meven more if the silver rally continues. To be clear, this wouldn't happen overnight; it would take a few years of active drilling, possibly by multiple operators.

As good as I believe the cobalt refinery/Glencore story is, adding high-grade silver optionality to the mix is quite compelling. Although I believe the cobalt price will eventually rebound (it possibly has started a move back to $1820/lb.), silver is very strong right now. The spot price is up more than +50% in the past month alone.

Starting the process of monetizing silver assets (only upon attractive terms) is a great idea. Not only has the price soared, but increased attention from larger junior players and, importantly, new investors, can only lead to good things.

Finally, although not explicitly mentioned, there's a growing number of small to mid-sized royalty and streaming companies that could be interested in working with First Cobalt on developing its ample silver resources.

These days, royalty/streaming companies are enjoying sky-high valuations in the market. The average multiples of trailing 12-month enterprise value/revenue (EV/Rev) and EV/EBITDA (earnings before interest, taxes, depreciation and amortization) of the largest players is 26x and 40x.

100%-owned cobalt refinery worth twice the company's market cap!

When metals/minerals prices soar (recently it's been gold, silver, palladium, perhaps soon uranium, cobalt, copper), refineries go up in value as well. It takes years to plan, permit, fund and construct a new mill and permit/construct a new tailings facility.

Due to scarcity, as the only permitted cobalt mill in North America, First Cobalt's facility in Ontario is increasing in value by the month. I believe that First Cobalt's 100%-owned refinery is worth at least twice the company's market cap of CA$54M (Hatch estimated its replacement value US$78M in 2012).

If the value of First Cobalt's silver assets can be unlocked, each CA$10M is worth about 20% in the company's current valuation. So, C$20M of (realized + unrealized) value would be worth 40% of the current market cap. That's a really nice pickup for zero cost.

Investors looking for new ways to play precious metals can now have a look here. Readers are no doubt aware that dozens and dozens of silver/gold juniors have soared by 500% or more from 52-week lows (74 of 391 gold companies I'm watching on Yahoo Finance are up 500%+). First Cobalt has plenty of room to run.

Readers should consider taking a few minutes to revisit the First Cobalt story. Cobalt will have its day in the sun again. Silver is a tremendous gift, and the company's 100%-owned cobalt refinery is already very valuable. It's an increasingly attractive hard asset that should be throwing off meaningful free cash flow within 18 months.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about First Cobalt Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of First Cobalt Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares of First Cobalt Corp., and the Company was an advertiser on [ER].

While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.