The pause in industrial activity brought about by the Covid-19 crisis has led us to a fork in the road with respect to the direction we as a society take in fulfilling the twin mandates of suppressing global warming and growing the economy in challenging times.

To some extent these goals are incompatible. In a world that continues to run on fossil fuels, how do policymakers wean countries off oil and gas without wrecking their economies? And from an environmental point of view, how can we continue to drive gas-powered vehicles and heat our homes with natural gas and coal, when we know emissions from these fuels add to greenhouse gases that, left unchecked, will eventually render much of the earth uninhabitable?

Unexpectedly, the coronavirus has provided a window into a future with fewer carbon emissions. While nobody hoping for a cleaner environment would wish to pair ecological progress with the worst economic slowdown since the Great Depression, the pandemic does show what happens when industrial activity abruptly stops.

As we now know, clearer skies owing to Covid-19 lockdowns have become the silver lining of the global economy coming to a screeching halt in March.

Combine stay at home orders with travel bans, business closures and the fact that demand for oil has fallen off a cliff with economies locked down, and you get global carbon output dipping for the first time since the 2008 financial crisis.

China, the world's worst polluter, emitted 25% less carbon during a one-month period compared to a year ago, as people were instructed (and in some cases forced) to stay home, factories were shuttered and coal use fell by 40%.

The South China Morning Post reported a significant improvement in China's air and water quality during the first three months of 2020. Limits on industry and travel upped the number of good air quality days by 11.5% compared with the same time last year in 337 cities across China.

Levels of PM2.5, the smallest and most harmful air pollution particles, dropped 18% between January 20 and April 4. The amount of nitrogen dioxide, a greenhouse gas that causes respiratory problems and cancer, was down 42%.

The country's water quality was also much improved, shown by reduced phosphorous and ammonia chemicals.

The sharp drop in fossil fuel pollution during the month of April will result in 11,000 fewer deaths in European countries. A study by the Centre for Research on Energy and Clean Air found measures in Europe to contain the spread of coronavirus resulted in a 40% drop in coal-generated power and one-third lower oil consumption.

Madrid saw a 56% drop in the levels of nitrous oxide, a product of burning fuel, with Paris, Milan, Brussels, Belgium and Frankfurt experiencing similar reductions. In New York State, the U.S. epicenter of Covid-19, measures to contain the virus have cut air pollution in half.

So here we are, at a crossroads. In several countries Covid-19 case curves are leveling off, prompting health authorities to gradually lift social distancing restrictions and allow businesses to resume operations. As the re-opening continues, policymakers need to ask themselves: How do we return the economy to pre-virus levels, by getting people working and spending again? Is it possible to rescue the economy while also making big cuts to greenhouse gas emissions and improving our overall health?

The answer to the second question is "yes." And the way to do it is through a massive "green stimulus" program. We are not talking pie-in-the-sky, no "Green New Deal" schemes costing trillions, espoused by twits and putting governments even deeper in debt, which as we know from a previous article, strangles gross domestic product. No, what we want to see happen is the roll-out of clean and green infrastructure that puts thousands of people to work, restores confidence in heavy industry, while at the same time cleans up the environment and provides renewed hope for a cleaner, safer, sustainable planet for future generations.

It's something we here at AOTH have been talking about for years, and we're not alone.

The International Energy Organization's executive director recently said that turmoil in the oil sector caused by Covid-19 should be seen as an opportunity to embrace green energy. In an interview with Reuters, Faith Birol said lithium-ion batteries and the use of "electrolyzers" to produce hydrogen should be candidates for government subsidies and policy support.

A recent report from Oxford University cited by Oilprice.com concurs the world is at a crucial point in its history, when we either take a step forward in supporting industries that get us to where we need to go in terms of reducing our carbon footprint and cleaning up our environment, or we slide back to a business-as-usual scenario where fossil fuel use continues apace:

Given the scale of spending under consideration, then, there is a once-in-a-generation opportunity to "build back better," the Oxford report argues. "The recovery packages can either kill these two birds with one stonesetting the global economy on a pathway towards net-zero emissionsor lock us into a fossil system from which it will be nearly impossible to escape," they warned.

For the United States and China, infrastructure spending is a key piece of the rebuilding puzzle.

U.S. President Trump realizes he needs a strategy for playing through the pandemic, i.e., a means to pull the U.S. up from its bootstraps when, not if, the economy turns around.

At the end of March Trump took to Twitter to renew his 2016 election campaign pledge for infrastructure renewal, urging Congress to pass a $2 trillion plan for improving the country's roads, bridges, water systems and broadband Internet:

It's likely that Trump stole the idea from the Chinese, who have been touting their own form of blacktop politics as a way of restoring the economy, particularly manufacturing, which has been crushed by the coronavirus.

Beijing is reportedly eyeing a $570 billion infrastructure build-out, not unlike its stimulus package of 2008, to get the economy back on track.

Among the projects that could receive a huge boost in investment, courtesy of a government rescue package, are a $44.2 billion expansion to Shanghai's urban rail transit system, an intercity railway along the Yangtze River ($34.3B), and eight new metro lines worth $21.7 billion, to be constructed in the virus epicenter city of Wuhan.

Employment creation must obviously be a factor in deciding how to restore crippled economies, given the millions of jobs losses from Covid-19.

The Oxford economists note that construction jobs for renewable energy installation or retrofitting buildings can't be offshored, and that they are labor-intensivefor every million dollars spent, 7.49 full-time renewable energy jobs are created but only 2.65 jobs in fossil fuels.

Lithium vs hydrogen

If we accept the idea that we need to "go green," the next question is, which technologies should be supported? Solar and wind are well-developed verticals that will continue to grow, especially as their costs per kilowatt-hour drop relative to natural gas, coal and hydroelectric power, and as renewable energy storage technology keeps improving.

While the biggest obstacle to large-scale energy storage is cost, recent analysis by BloombergNEF found that for applications requiring two hours of energy, lithium-ion batteries are beating natural gas peaker plants on price.

Vehicles are a major source of air pollution. According to the Environmental Defense Fund, the transportation sector is responsible for a quarter of U.S. greenhouse gas emissions. Passenger vehicles produce four times more greenhouse gases than all of domestic aviation.

The electrification of the global transportation system has long been seen as essential to reducing carbon emissions. The two technologies with the capability of delivering vehicles with zero emissions are battery-electric powertrains and hydrogen fuel cells.

An electric vehicle can run on either rechargeable batteries or fuel cells that convert hydrogen into electricity. Both have zero tailpipe emissions, but over the years, cars run on batteries have emerged as the clear winner compared to hydrogen-powered EVs.

There are a few reasons for this. The first is the lack of hydrogen infrastructure. Although fuel cell technology has the advantage of a fast fill-up time, minutes as opposed to the hours-long charge that batteries need, it has proven challenging and expensive to build and support a network of fueling stations that can deliver a highly explosive gas, compressed to 10,000 psi, reliably, quickly and safely.

In California, the only place where hydrogen vehicles can operate as it's the only state with a (still unreliable) hydrogen fueling network, a goal of 100 hydrogen fueling stations by 2020 has fallen short; as of April 8, the state only had 40. Each station costs around $2 million, making them prohibitively expensive.

Compare that to 18,000 EV charging stations servicing half a million plug-in cars currently traveling on California's roads.

Also, hydrogen isn't all that green if the feedstock used to create it is natural gas, which it usually is. Until the electricity is fully renewable, hydrogen vehicles will always have higher CO2 emissions than electric cars.

Finally, the cost per mile favors battery-electric vehicles over hydrogen. Filling a Toyota Mirai or Honda Clarity Fuel Celltwo of only three (the other is the Hyundai Nexo) hydrogen models availablecosts north of $50. Home-charging an electric car on average costs what a gasoline car would if gas sold at $1 a gallon.

The upshot is that BEVs have swamped hydrogen cars. According to The Drive, Despite more than half a century of development, starting in 1966 with GM's Electrovan, hydrogen fuel-cell cars remain low in volume, expensive to produce, and restricted to sales in the few countries or regions that have built hydrogen fueling stations.

Meanwhile, 10 years after the first modern EVs went on sale, electric cars sell in the low millions a year globallytwo orders of magnitude higher than their hydrogen counterparts.

Since 2010 1.3 million battery-electric and plug-in hybrid vehicles have been sold in the US, compared to around 8,000 hydrogen cars.

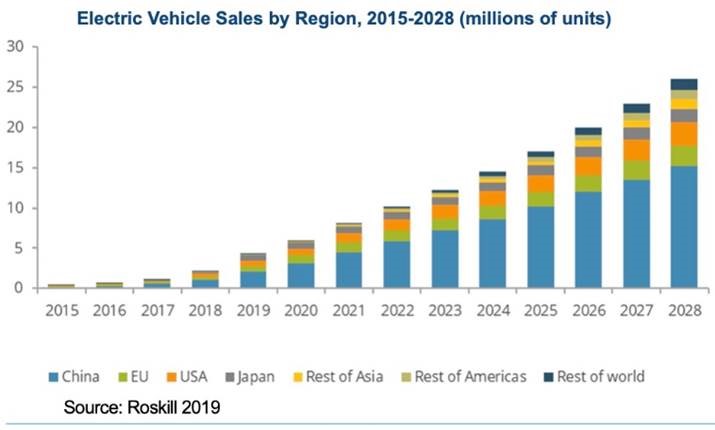

A Reuters analysis shows that automakers are planning on spending a combined $300 billion on electrification in the next decade. Meanwhile more battery factories are being built globally; demand for lithium-ion batteries is forecast to grow at a CAGR of over 13% by 2023.

All of this growth in battery plants and EVs will mean an unprecedented need for the metals that go into them. This includes lithium, cobalt, rare earths, graphite, nickel and copper.

Lithium carbonate and lithium hydroxide are key components of the lithium-ion battery cathode, making it an extremely sought-after battery ingredient.

Lithium, therefore, is expected to see a 29X increase in demand, driven not only by lithium required in EVs batteries, but in consumer electronics like smart phones and power tools, and grid-scale electricity storage.

Yet despite the rosy projections, electric vehicles have a long way to go before they make any kind of a dent in the total vehicle market, which remains dominated by cars, trucks and vans run on gasoline or diesel fuel.

In 2019 sales of plug-in passenger cars achieved a 2.5% market share of new car sales, and while that is up from 2.1% in 2018 and 1.3% in 2017, it means over 97% of global new-car sales were regular vehicles.

The biggest obstacles to higher EV market penetration are resistance to change, range anxiety and price. According to The Drive, 58% of drivers are afraid they will run out of charge while on the road, and another 49% fear the low availability of charging stations.

For many North Americans, sticker shock is a non-starter. While some EV models have come down in price, the lowest-cost Tesla Model 3 in 2019 was $42,900, nearly 19% higher than the national new-car average of $36,115.

Building a better battery

Although electric vehicles have existed as prototypes and with limited commercial production since the 1990s (General Motors' EV1for a great history watch 'Who Killed the Electric Car?'), the momentum in the switch from cars equipped with gas and diesel-powered internal combustion engines (ICE) to vehicles powered with lithium-ion batteries started in 2009 by then-President Obama. Obama announced his administration was putting aside $2.4 billion in order for American manufacturers to produce hybrid electric vehicles and battery components.

Of course Tesla was a few years ahead of Obama, forming in 2003 and producing its first model, the all-electric Model S sedan, in 2008.

Electric vehicles have far fewer moving parts than gasoline-powered cars they don't have mufflers, gas tanks, catalytic converters or ignition systems. There's also never an oil change or tune-up to worry about. But the clean and green doesn't end there. Electric drives are more efficient than the drives on ICE cars. They are able to convert more of the available energy to propel the car therefore using less energy to go the same distance. And applying the brakes converts what was wasted energy in the form of heat, to useful energy in the form of electricity to help recharge the car's batteries.

EV automakers want to know: How can batteries be made cheaply enough to compete with gas-powered vehicles, and with a reasonable range that doesn't have the driver frantically searching for a charging station in the middle of nowhere?

By 2025 the cost of a large battery pack, say 60 kilowatt-hours with a range of +200 miles, is expected to fall to $100 per kWh or less, which is the point when EV prices would reach parity with gasoline vehicles, notes The Drive.

Achieving price parity is critical. Lower prices would not only give people an incentive to buy their first EV, they would facilitate the green infrastructure build-out we and others have been suggesting could be a way out of the virus-induced economic slump.

Recently Tesla announced plans to introduce a new battery in its Model 3 sedan, in China this year or early next.

Reuters reports the new low-cost, long-life battery is expected to bring the cost of electric vehicles in line with gasoline models, and will allow EV batteries to have second and third lives in the electric power grid.

The batteries designed to last a million miles will rely on low-cobalt and cobalt-free chemistries. The California-based company with "gigafactories" in Nevada and China, is reportedly talking to CATL, the largest electric-vehicle battery maker in the world, about employing CATL's lithium iron phosphate batteries, which use no cobalt, the most expensive metal in EV batteries.

Prices for these cobalt-free battery packs have fallen below $80 per kilowatt hour, while CATL's low-cobalt NMC (nickel, manganese, cobalt) battery packs are close to $100/kWh. Comparable low-cobalt batteries being developed by General Motors and Korea's LG Chem are not expected to reach those levels until 2025.

Tesla is also working on recycling and recovering nickel, cobalt and lithium, and re-purposing lithium batteries in grid storage systems such as the one it built in South Australia in 2017 to capture electricity from nearby wind turbines.

Reuters states,

Taken together, the advances in battery technology, the strategy of expanding the ways in which EV batteries can be used and the manufacturing automation on a huge scale all aim at the same target: Reworking the financial math that until now has made buying an electric car more expensive for most consumers than sticking with carbon-emitting internal combustion vehicles.

US mine-->battery-->EV supply chain

We applaud Tesla and its pioneering, though mercurial CEO, Elon Musk, for being first out of the gate with electric-vehicle technology. Being a first mover in the EV space has made Musk rich beyond his wildest dreams and allowed Tesla the capital to innovate and stay ahead of its competitors.

However, we question Musk's strategy of rolling out his new batteries in China, which has become the bogeyman of international commerce, and getting into bed with a Chinese company, CATL.

Need we remind readers, the Chinese government undertook pernicious measures to conceal the coronavirus outbreak in Wuhan. They included destruction of virus samples, suppression of information, and delaying lockdown of a city of 11 million, allowing the virus to spread throughout China and worldwide, through airline travel during the Chinese Spring Festival, the largest annual migration of holiday travelers on earth.

The U.S., Australia and all 27 nations of the EU are demanding an investigation into whether the World Health Organization was complicit with China in concealing Covid-19 from the rest of the world for six weeksenough time to prepare a public health response.

Shenanigans like hoarding key medical gear in a near monopoly, then profiting handsomely from sales to desperate buyers, has led to the Trump administration "turbocharging" an initiative to distance itself from China. According to a recent Reuters article, economic destruction and the U.S. coronavirus death toll are driving a government-wide push to move U.S. production and supply chain dependency away from China...

The U.S. wants to create an alliance of "trusted partners" called the Economic Prosperity Network. Participating countries include Australia, India, Japan, New Zealand and Vietnam. Secretary of State Mike Pompeo said the goal is to "prevent something like this from happening again." (Canada, which refrains from criticizing Beijing due to fear of retaliation, didn't get an invite.)

Pompeo is referring to how the pandemic exposed China's tight grip on global supply chains for generic drugs and medical equipment. Although the country accounts for only 13% of active pharmaceutical ingredient (API) makers supplying the US market, it produces many APIs for widely used medicines along with chemicals used to formulate APIs. Often China ships them to India for processing into tablets.

Such medicines include antibiotics, ibuprofen, acetaminophen and heparin, an anticoagulant taken by patients with heart disease.

We like the idea of a network of trading nations who believe in free trade and open borders without harboring secret ambitions to monopolize certain sectors, as China has done with critical minerals, solar power and medical supplies, to name just three.

China has locked up the rare earths market and is the primary player in a number of critical metals markets including lithium, cobalt, graphite, manganese and vanadium.

The Asian superpower imports 98% of its cobalt from the DRC and produces around half of the world's refined cobalt.

Last year, as part of its trade war strategy, China raised the prospect of restricting exports of rare earths, which are critical to America's defense, energy electronics and auto sectors, similar to a 2010 Chinese ban on rare earth oxide exports to Japan.

We know from previous articles that China has been extremely active in acquiring ownership or part-ownership of foreign lithium mines and inking offtake agreements.

China produces roughly two-thirds of the world's lithium-ion batteries and controls most of the processing facilities.

Lithium is also among 23 critical metals President Trump has deemed critical to national security; in 2017 Trump signed a bill that would encourage the exploration and development of new U.S. sources of these metals.

According to Benchmark Mineral Intelligence, the U.S. only produces 1% of global lithium supply and 7% of refined lithium chemicals, versus China's 51%. The country is about 70% dependent on imported lithium.

To lessen U.S. lithium dependency will require the building of a mine to battery to EV supply chain in North America.

The first step is to develop new North American lithium mines.

Currently the only U.S. lithium producer is chemicals giant Albemarle. Lithium products from Albemarle's Silver Peak lithium brine operation in Nevada are sent to its processing plant in North Carolina. This material is then loaded on ships and sent to Asian battery manufacturers, which sell the batteries to EV companies.

It's curious how several top automakers are planning on, or are already building, electric vehicle plants and facilities without disclosing how they will source their raw materials.

In 2017, Mercedez-Benz announced plans to set up an electric car production facility and battery plant at its existing Tuscaloosa, Alabama, plant. The $1-billion expansion will include a new battery factory near the production site, with the goal of providing batteries for a future electric SUV under the brand EQ. Six sites are planned to produce Mercedes' EQ electric-vehicle family models, along with a network of eight battery plants.

Volkswagen has said it will invest $800 million to construct a new electric vehiclelikely an SUVat its plant in Chattanooga, starting in 2022. For more read Volkswagen to drag Tesla, making EVs in Tennessee.

Korean company SK Innovation has said it will invest US$1.7 billion in the U.S.' first electric vehicle plant, to serve Volkswagen, in neighboring Georgia. The 9.8 gigawatt-hour-plant would be the first EV battery plant in the United States. SK recently announced a second 10-GWh plant requiring an investment of $1 billion.

GM has rolled out its 2020 Cadillac SUV, built in Spring Hill, Tenn., in a move designed to challenge Tesla.

Tesla's vulnerability

Last year a Tesla executive said the company is worried about a long-term shortage of nickel, copper and lithium. The number of EVs are expected to multiply in coming years, but they can only progress as fast as the lithium-ion batteries can get built that go into them. In June of 2019, Musk said that in order to ensure Tesla has enough batteries to expand its product line, Tesla might get into mining lithium for itself.

That, so far, has failed to materialize, although the EV maker has signed an off-take agreement with a planned mine and refinery project in Australia.

Instead Musk seems to be going out of his way to court China, using its mine-battery-EV supply chain rather than supporting North American companies trying to develop domestic sources of EV raw materials.

Currently Tesla produces nickel-cobalt-aluminum (NCA) batteries with Japanese company Panasonic at its Sparks, Nevada, plant, and buys NMC batteries from LG Chem in China. Nothing local about that.

If Musk thinks his company can lead the world in EV sales by getting its raw materials from China, I'm afraid he is setting himself up for a big fail.

Chinese companies dominate the EV space and will do what they need to do to win market share. While Tesla in December surpassed BYD as the world's largest electric car maker, without a safe, reliable supply chain, the company is vulnerable to a sudden supply shock that could stop production in its tracks. Case in point: in January the Chinese government temporarily shut down Tesla's new factory in Shanghai over the coronavirus, delaying production of the Model 3 and denting the company's first-quarter profits.

The trade war between China and the United States is far from over, in fact it appears to have entered a new phase. This week Trump said he was disappointed with China over its failure to contain the coronavirus and that the worldwide pandemic cast a pall over his trade deal with Beijingdespite a "phase 1" agreement signed in January.

Reuters reports the Trump administration is planning to deploy long-range, ground-launched cruise missiles in the Asia Pacific region, including versions of the Tomahawk cruise missile carried on U.S. warships, and the first new long-range anti-ship missiles in decades. The U.S. Air Force has also begun developing the first hypersonic cruise missile, capable of eluding detection by flying at least five times the speed of sound.

The technology the U.S. intends to deploy to counter China's missiles uses lithium batteries and rare earth magnets. China controls the market in both.

Cypress Development Corp. (CYP:TSX.V; CYDVF:OTCQB; C1Z1:FSE)

We have an idea for Elon Musk and Tesla: how about they forget about signing battery deals with China and offtake agreements with Australia, which is a long way from Nevada, and instead look at investing in a lithium mine in the United States?

Three and a half years ago Cypress began prospecting in the Clayton Valley, Nevada, hoping to find a property that could support a lithium carbonate resource to compete with or possibly complement its neighbor, Albemarle's Silver Peak Mine, whose lithium brine grades are declining.

Its Clayton Valley Lithium Project hosts an indicated resource of 3.835 million tonnes LCE (lithium carbonate equivalent) and an inferred resource of 5.126 million tonnes LCE. The project is ranked among the largest in the world.

Last year Cypress Development Corp. completed the first two phases of a prefeasibility study (PFS), confirming that lithium can be acid-leached and extracted at high recovery rates and successfully separating the lithium-rich claystone ores from the sulfuric acid leachate.

It is a major technical problem to separate ultra-fine clay particles (<5 microns) from a leach solution. Cypress has done it, putting the company at the forefront of lithium clay projects globally.

The U.S. now has a major source of lithium carbonate and lithium hydroxide and potentially a not-inconsiderable amount of rare earths including scandium, a highly prized metal used in aircraft components, for example.

The eagerly awaited prefeasibility study is crucial to moving the project forward, not only for proving that the metallurgical process for separating lithium from clays is commercially viable, but demonstrating that Cypress' costs are in line with the 2018 preliminary economic assessment (PEA).

Cypress' vision is to build a mine with the ability to extract whatever oxides they choose, from the processing plant. The project design is based on mining 15,000 tonnes per day to produce 25,000 tonnes per year of LCE.

The end result is that through by-product credits Cypress could shave millions of dollars off of their processing costs, further enriching what we already think is looking to be a very profitable mine.

Cypress is the only lithium junior in North America that has yet to sign an offtake or major financing agreement, despite its project being further advanced than nearby Clayton Valley lithium properties.

Partnering up with Tesla would make sense. Cypress needs a very large buyer for its lithium carbonate and lithium hydroxide end-products, and rare earth oxides needed for permanent magnets that go into EV motors. Tesla has to find a way to bring the cost of batteries down to $100 per kWh, which is the point when EV prices reach parity with gasoline vehicles. Cypress gives them the opportunity to buy their lithium raw materials directly from the mine, cutting out the Asian middlemen. No CATL, no more LG Chem. Surely that would bring down Tesla's costs of production, allowing them to pass on the savings to EV buyers.

Finally, a U.S. company would have the capability of producing electric vehicles that are affordable to the average American, while also becoming the beach-head for a powerful North American electric-vehicle supply chain that could compete with China, and be independent of its critical minerals.

That would be huge.

There's no way Silver Peak can produce enough lithium to supply American needs, especially with all of the EV battery and auto production facilities planned.

When you think about the huge amount of ore available to be minedit's among the largest LCE resources in the worldand the valuable products that will be coming out of the relatively easy processing flow sheet at the end, we believe Cypress may have the most important mine in America in decades.

Cypress has a very important study release coming virtually any daythe Prefeasibility study (PFS) on its Clayton Valley Lithium Project. A positive study result means CYP completes another step on its development path to building a mine.

The project is next to Albemarle's Silver Peak Mine, Albemarle (NYSE:ALB) is the world's largest lithium producer. Tesla is the world's largest EV manufacturer, its gigafactory is just 200km away from CYP's Clayton Valley Project.

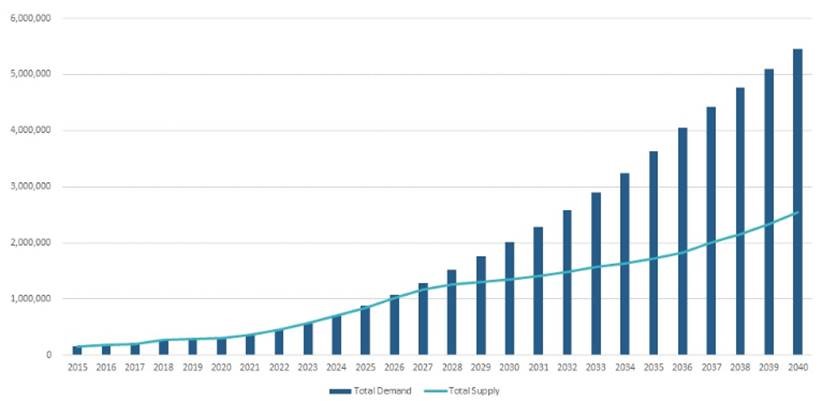

Current annual lithium (LCE) supply is around 360,000 tonnes. Total lithium demand of LCE is expected to reach over 1 million tonnes by 2025 or higher, states S&P Global Platts Analytics.

The United States is about 70% dependent on imported lithium.

How will the United States, how will Volkswagen, Tesla, Albemarle, GM, Mercedes and SK Innovation obtain enough lithium for the storm of demand that is brewing?

Cypress Development Corp

TSX-V:CYP Cdn$0.19 2020.05.16

Shares Outstanding 90,077,001m

Market cap Cdn$17,114,630m

CYP website

Richard (Rick) Mills

subscribe to my free newsletter

aheadoftheherd.com

Ahead of the Herd Twitter

Richard (Rick) Mills, AheadoftheHerd.com, lives on a 160-acre farm in northern British Columbia. Richard's articles have been published on over 400 websites, including: Wall Street Journal, USA Today, National Post, Lewrockwell, Montreal Gazette, Vancouver Sun, CBSnews, Huffington Post, Beforeitsnews, Londonthenews, Wealthwire, Calgary Herald, Forbes, Dallas News, SGT report, Vantagewire, India Times, Ninemsn, Ib times, Businessweek, Hong Kong Herald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com, MSN.com and the Association of Mining Analysts.

[NLINSERT]Disclosures:

1) Rick Mills: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Cypress Development Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: Cypress Development is an advertiser on Ahead of the Herd. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures/disclaimer below.

2) The following companies mentioned in this article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

Legal Notice/Disclaimer: Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH. Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified. AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice. AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

AOTH/Richard Mills is not a registered broker/financial advisor and does not hold any licenses. These are solely personal thoughts and opinions about finance and/or investments no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor. You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments but does suggest consulting your own registered broker/financial advisor with regards to any such transactions.