Skyharbour Resources Ltd. (SYH:TSX.V; SYHBF:OTCQB) is in a strong position to benefit from a rebound happening right now (finally!) in uranium prices. The management team, board and technical advisors are world class, especially for a company with a market cap of CA$9.8 million (CA$9.8M)/US$7.0M [see April presentation, pp. 46].

For years pundits have been saying that a recovery in the uranium price was 312 months away. They have been wrong. For the first time in two years there's been a noteworthy bounce in the spot price.

Spot uranium price up 22% in past five weeks

The uranium market has relatively sticky demand, as producers are required to deliver material into long-term contracts. By contrast, supply is highly concentrated in a handful of mines and jurisdictions. In the past five weeks, the spot price is up 22%, to $29.10/lb from $23.85/lb [investing.com]. That's a four-year high.

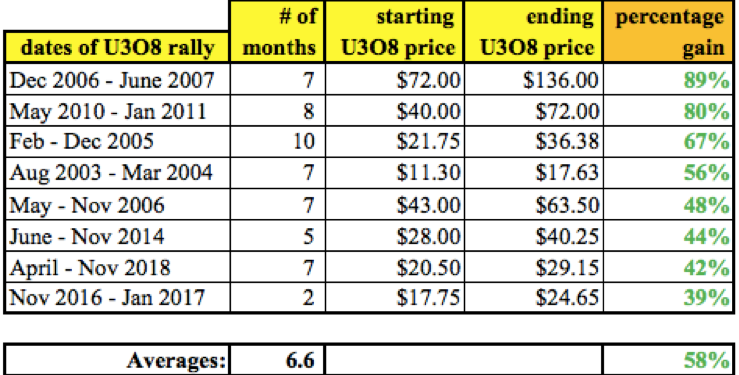

As can be seen in the chart below, the eight largest upward moves in spot prices range from 39% to 89%, with an average of 58%. These spikes took place over an average of 6.6 months. Two important things to consider: first, this data reflects historical spot prices, not long-term contract prices; and second, the current 22% bounce is only in month two of its ascent.

If history is a guide, there could be further upside well into the summer or even fall. Having said that, there's no certainty that the price will continue rising.

If we are at the beginning of a significant move higher, the price could move north of $35/lb. An "average" breakout move of 58% would bring the spot price to ~$38/lb. Even more important is what might happen to the long-term contract price.

Skyharbour could outperform giants like Cameco Corp. (CCO:TSX; CCJ:NYSE) and NexGen Energy Ltd. (NXE:TSX; NXE:NYSE.MKT)

Over the past 51 months, the average premium paid above spot for long-term contracts has been ~36% [Cameco Corp. website]. That implies a contract price of $52/lb (36% above the $38/lb figure). Is this too aggressive? Not necessarily; a majority of uranium producers have no interest in locking in long-term deals under $45/lb

The current premium is 12%. Could we see a $45$50/lb contract awarded this year? A move to $45/lb would likely generate a lot of excitement. We haven't seen that level since June 2015.

Although there's been a modest rebound in uranium stocks, I strongly believe that an increase in the contract price from the current $32.5/lb to $45/lb (or more) would spark another, possibly larger, move for the sector. It's worth noting that historically the spot price traded above $70/lb from December 2006 to March 2008, and hit a monthly high of $136/lb in June 2007.

I find it interesting that industry leaders Cameco, Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT), NexGen Energy Ltd., Fission Uranium Corp. (FCU:TSX; FCUUF:OTCQX; 2FU:FSE) and Uranium Energy Corp. (UEC:NYSE.MKT) are up more from their lows (+86%) than Skyharbour. Higher-risk, smaller market cap juniors are poised to have outsized gains if the uranium price continues to climb.

Good things are happening for Skyharbour

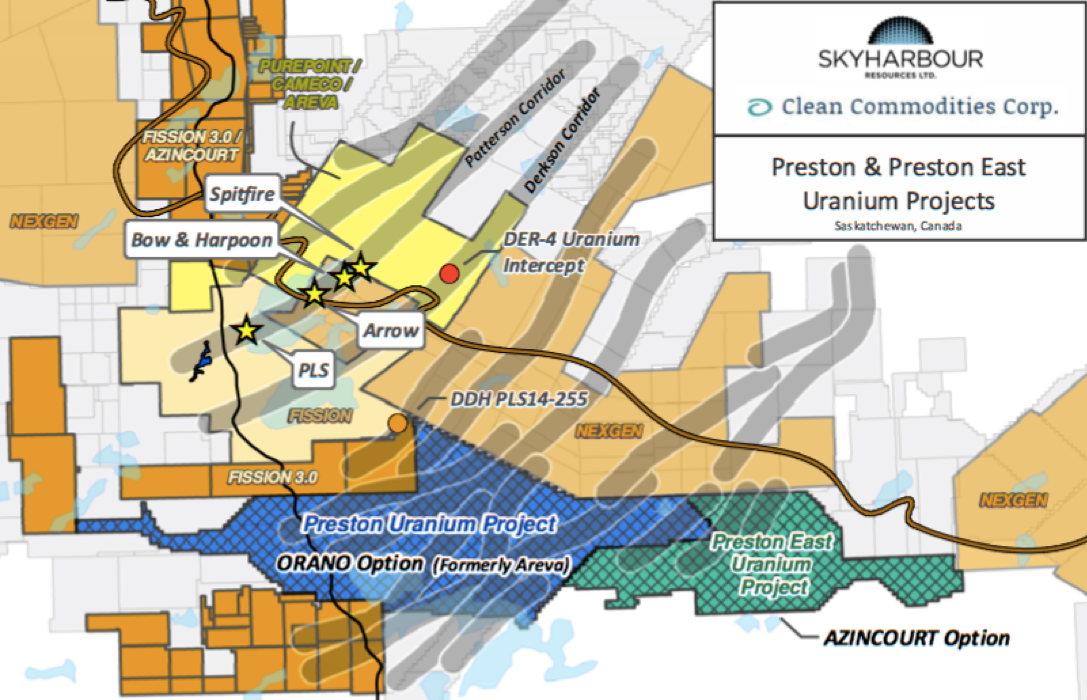

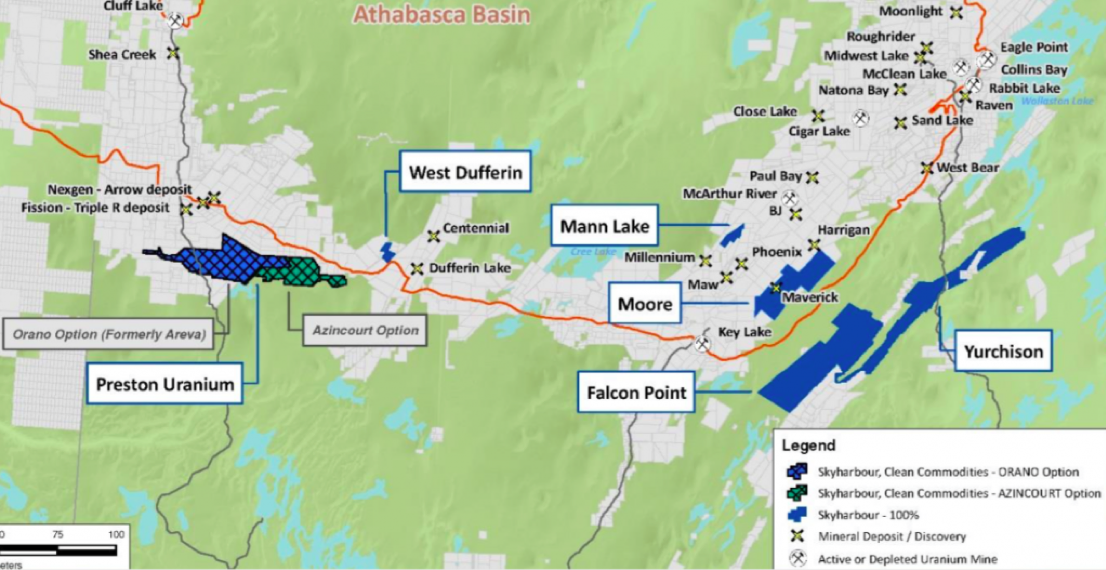

CEO Jordan Trimble and his team have prudently assembled a basket of six properties in the eastern half of the world-famous Athabasca uranium basin. The portfolio covers >250,000 hectares and contains wholly owned assets as well as farmed-out properties. Three projects are being actively explored, but management is only funding exploration at its 100%-owned Moore uranium project.

On March 9, option partner Orano Canada Inc. commenced its exploration programs at the Preston uranium project, located near NexGen's high-grade Arrow deposit and Fission Uranium's Triple Rproject. Orano can earn up to 70% of a 49,635-hectare central portion of the Preston uranium project for CA$8M over six years. Skyharbour owns 50% of the Preston project. Orano is currently about half way through the CA$8 million earn in.

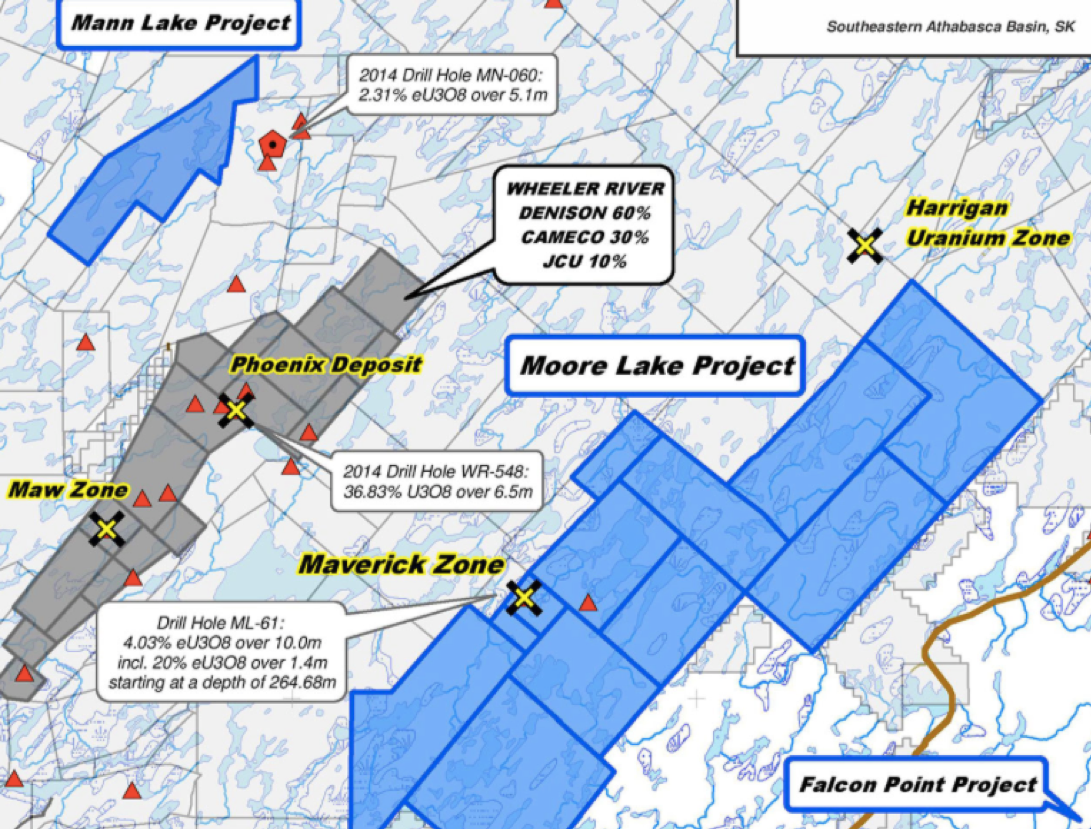

On Feb. 13, Skyharbour announced the start of, and is now wrapping up, a 2020 winter diamond drill program at its flagship, 100%-owned, 35,705-hectare Moore uranium project. This project is ~15 kilometers east of Denison Mines' Wheeler River. Management announced plans for 2,500 meters of drilling in six to nine holes to follow up on last year's exploration successes.

An option to acquire the Moore project was obtained from Denison in June 2016. Twelve contiguous claims total a sizable 35,705 hectares (~88,230 acres) located just east of the midpoint between the Key Lake mine and mill complex and Cameco's McArthur River mine. The project has seen extensive historical exploration, including roughly $50 million of inflation-adjusted exploration expenditures. More than 140,000 meters have been drilled in >380 holes.

100%-owned Moore project has seen a lot of drilling

Unconformity-style uranium mineralization was discovered on the Moore property at the Maverick Zone in April 2001. Historical drill results include 4.0% eU3O8 over 10 meters (10m), including 20% eU3O8 over 1.4m. In 2017, Skyharbour announced select assays of 6.0% U3O8 over 5.9m, including 20.8% U3O8 over 1.5m at a vertical depth of ~265m.

Another highlight can be found at Maverick East, with an intercept of 1.8% U3O8 over 11.5m, including 4.2% U3O8 over 4.5m and 9.1% U3O8 over 1.4m. Refinement of the company's geological and structural model has greatly improved drill targeting in the basement rocks of Maverick East, along strike and down dip of current mineralization.

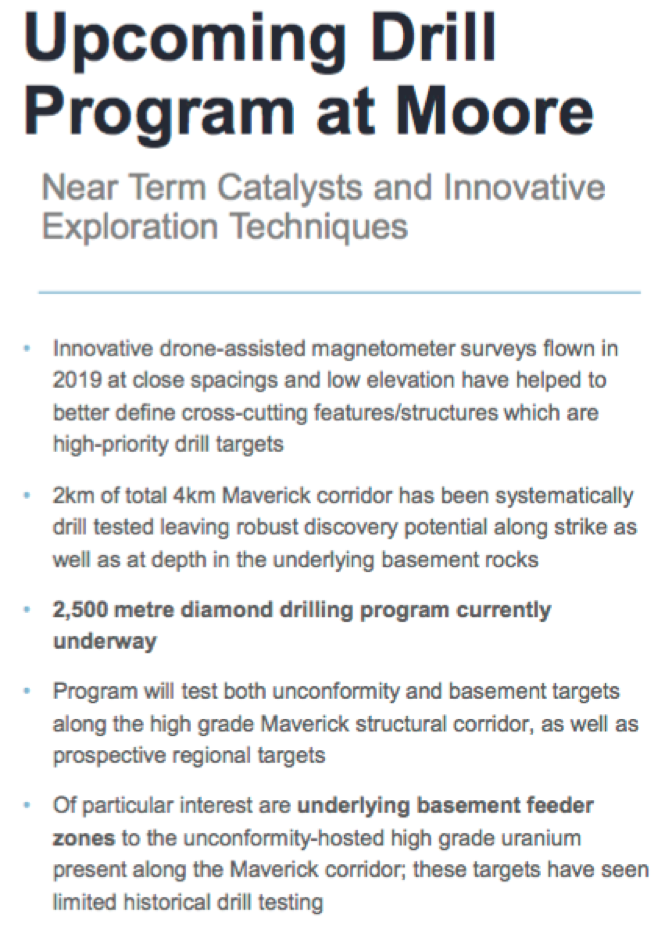

This fully funded and permitted drill program is testing both unconformity and basement-hosted targets along the company's high-grade Maverick structural corridor. Of particular interest is the active search for underlying basement feeder zones to the unconformity-hosted, high-grade uranium that's already been identified.

Importantly, these targets have seen only minimal historical drilling. Management hopes to expand the high-grade mineralization discovered at the Maverick East Zone and to test the Goose and Viper target areas along strike, with a focus, again, on basement-hosted mineralization. It's worth noting that most of the recent high-grade discoveries in the basin, like those made by NexGen and Fission, have been made in the basement rocks.

Most of the historical drilling at Moore has not tested basement targets and it has only been recently, with modern geophysical techniques and new geological modeling, that Skyharbour has properly refined its top basement-hosted targets, which are being tested in this drill program.

At Maverick East, drilling by Skyharbour intersected significant high-grade uranium mineralization extending from the unconformity into the basement rocks. Last year's hole ML19-06 intersected 0.62% U3O8 over 12.0m, including a high-grade basement-hosted intercept of 2.31% U3O8over 2.5m.

Drilling to the northeast of Maverick and Maverick East will be done this year on the underexplored remaining two kilometers of the Maverick corridor. The promising Goose and Viper target areas, step-outs of ~500m and 1,500m along strike, will be drill tested.

Drill results and final assays are expected in the next month or two, so this is a key near-term catalyst for investors to look out for.

Why uranium? Why now?

Perhaps no single attribute of uranium as fuel is as compelling as this; a 20-gram pellet of uranium, just half the size of a AA battery, packs the same punch as 400 kilograms of coal, an amount that would fill a container measuring ~9.3 cubic feet! This is a big reason why nuclear power plants are popping up all over China and India. The need for uranium to fuel nuclear power plants that will replace coal-fired plants is growing by the day.

Over the past few decades the global outlook for the maintenance/growth of coal-fired power plants has fallen, with no end in sight. Although China and India will build coal plants for the foreseeable future, growth rates are slowing. In most parts of the world, it's increasingly difficult to fund new coal plants. This is bullish for the long-term prospects of nuclear power.

Cameco's bullish earnings commentary and the U.S. government's 10-year proposal (starting in 2021) to spend US$150 million per year acquiring U.S.-produced uranium, barely moved the needle of investor sentiment. Depending on negotiated contract pricing, perhaps three or four million pounds (per year) will exit the market into U.S. storage. That's fairly important for U.S. producers. However, by far the bigger news is Cameco's bullish commentary.

Cameco's CEO said, ". . .we have more prospective for long-term business in the contract pipeline than we have seen since 2011. . . .the underlying fact is that uranium demand is going up while supply is going down. Current weak prices are putting future supply at risk; this is not sustainable."

Cameco offers bullish commentary

Importantly, Cameco's CEO reported that his team has been rejecting proposals by utilities on contracts in the "$40s/lb." There appears to be a widening gap between bids and offers. This suggests prices could move fairly rapidly as buyers finally move off the sidelines.

The spot market is relatively tight now; it typically sees between 3060 million pounds transacted annually. However, last month Cameco announced a one-month shutdown of its Cigar Lake operations. This is yet another bullish signal for uranium prices, as Cigar Lake accounts for ~13% of primary mine supply. Prior to the pandemic, Cameco had plans to buy 2022 million pounds of uranium in the spot market this year.

An extended shutdown would force Cameco to buy even more in the spot market. Other recent announcements include Namibia cutting ~10% of global supply, and the world's largest producer, Kazatomprom, cutting up to 10.4 million pounds in 2020.

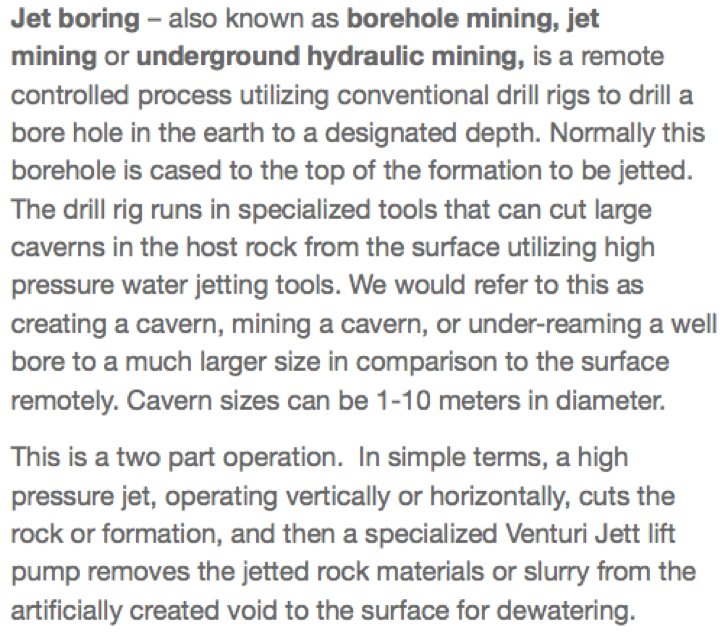

Might borehole mining be a game changer?

An industry development I'm watching is borehole mining (BHM) testing in the Athabasca Basin. Like in-situ recovery (ISR), BHM is amenable under select conditions, most notably in permeable rock at depths below ~300 meters. In BHM, a narrow hole is drilled. At bottom, high-pressure water jets break apart the ore. The resulting uranium slurry is then pumped to surface.

If any of Skyharbour's six properties prove amenable to BHM, it could truly be a game changer. Denison and Orano have been working on this for years. As these companies continue to optimize BHM, this technology could soon be ready for primetime.

An interesting peer uranium explorer in the eastern part of the basin is IsoEnergy (ISO:TSX.V). Its market cap of approximately CA$40 million is four times the size of Skyharbour's, a valuation discrepancy that's due to blockbuster drill results on the company's flagship 8,371-hectare property. Like Skyharbour, IsoEnergy is pre-maiden resource.

Could Skyharbour's valuation approach that of IsoEnergy? If the Moore project were to hit higher grade mineralization across wider areas, then the potential for the larger (35,705-hectare) property would be immense. No one knows what the drill bit will deliver, but it's worth reiterating that in addition to Moore, Skyharbour has multiple exploration programs underway with partners Orano and Azincourt Uranium Inc. (AAZ:TSX.V).

Six properties, three actively explored = increased discovery potential

Skyharbour stands to benefit from discoveries on its 50%-owned Preston project, being drilled by Orano, and the East Preston project, being drilled by Azincourt. [Note: Both Orano and Azincourt can earn up to 70% interests in Preston and East Preston]. Orano is currently doing geophysical work and a field program to generate drill targets. Azincourt is conducting a $1.2M drill program consisting of 2,0002,500 meters in 1015 holes.

By farming out assets, Skyharbour has three bites at the uranium apple. These prospects in the world-famous Athabasca Basin could become considerably more valuable if/when uranium prices move higher. Exploration success, plus a continued uptick in prices, could drive juniors higher, especially the share prices of companies that operate in safe, ultra-high-grade jurisdictions.

During the last major uranium bull market, there were hundreds of juniors to choose from. Today there are, at most, a few dozen worth consideration, and far fewer in the Athabasca Basin, with a world-class team, minimal cash burn, low valuation and multiple projects being actively explored. Companies like Skyharbour Resources (TSX-V: SYH / OTCQB: SYHBF) have ample room for upside.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

Read what other experts are saying about:

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Skyharbour Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Skyharbour Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned no shares in Skyharbour Resources, and Skyharbour was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: Skyharbour Resources. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Skyharbour Resources, a company mentioned in this article.

Graphics provided by the author.