The Trump-Mnuchin-Powell "directive," which engaged the Working Group on Financial Markets during the last weekend before Christmas 2018, has worked both beautifully and criminally as the term "moral hazard" has crept back into the mainstream dialogue. Once again, as we have seen countless times since "free markets" were transformed into "managed markets," charts and graphs and volume studies carry zero sway over the "invisible hand" of the politico-banker cartel.

As the S&P 500 hovers some 300 points above the lows seen on Christmas Eve, we have witnessed the full power and fury of the central banking cabal, complete with their government and regulatory confederates, as they offer shadowless doubt that stock prices are indeed a big part of policy mandate. Also, right up there at the top of their to-do list, is "managing" the prices of gold and its junior surrogate, silver, as their centuries-old utilities as canaries-in-fiat-sensitive coal mines has been denigrated by decades of interventionalist price-capping. It is both maddening and infuriating but it is not unexpected; it was actually announced the weekend before Christmas with the Mnuchin statement regarding the Plunge Protection Team (PPT).

As much as the financial media would love to crow about the "biggest rally in a decade," nothingand I mean nothingwould have prevented an all-out crash in stock prices, the severity of which could have easily rivaled October '87 or '29, other than the stark and unabashed bailout by the cretins.

The abject panic that was permeating the trading rooms of every major bank and brokerage around the globe, so very palpable in December, has toned down since the government-mandated and bank-executed rescue took hold in very late December, composed of a series of interventions and TV appearances by current and former Fed officials and stock market perma-bulls. However, as I debate the notion of a V-shaped bottom for stocks leading to new highs in 2019, I am mindful of the results of the results of the Santa Claus rally and the First Five Trading Days rule, which would suggest that 2019 has a 70-80% chance of being an "up" year.

While the stats are simply a look in the rear view mirror of historical stock prices, they certainly are no guarantee of a 2019 lift. But keep in mind that even if inflation came roaring back this year as stagflation takes hold of the mainstream economy, a 5% rise in consumer prices versus a 2% rise in the S&P would satisfy the statistical forecast but be of little or no benefit on a "net" basis.

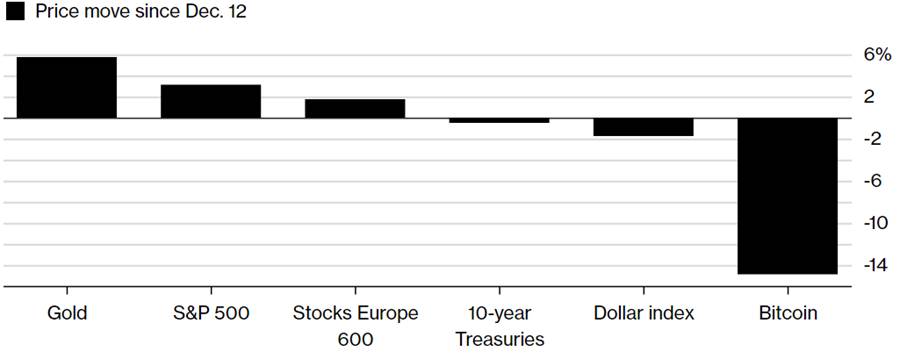

This chart shows the relative performance of the major asset classes (gold, U.S. and European stocks, bonds, currencies, and crypto) since December 12. While a longer-term chart would reveal and much different result, the message is clear: Gold is outperforming everything in the past 45 days.

This is again why I always look around the world to gauge performance. It is also why gold prices are rising and at new all-time highs against a number of non-U.S. currencies. Despite the desperation of the price-capping exercise in gold, both it and silver have been able to hold the bulk of their gains since the summer lows and appear to be simply biding time until the next major downdraft in global equities sends the "fear bid" back into precious metals.

With due deference to Frank Holmes, the gold "Love Trade" is nowhere to be found right now; it has been subordinated by its meaner, older sibling, the "Fear Trade," which rose up in Q4/2018, hissing and growling, with gnashing teeth and bloodshot eyes, in the move from $1,167 to a snick above $1,300. The song-and-dance, hat-and-cane act of Mnuchin and Powell from late last month has becalmed the golden beast for the time being, but if my analysis is correct, markets will soon revert back to behaviors closely resembling the October-December pattern of dip-buying in the precious metals and rip-selling in equities.

Speaking of rip-selling, one of my better passes last year was the purchase of the Goldman Sachs (GS:NYSE) December $200 put options, which I put on right after the headline linking them to that big Asian billion-dollar fraud and lawsuit. I watched the stock crater from $210 to $151.70 in less than two months, taking the puts from $3.40 to over $30 (by expiry) with my portion being cashed in around $25 (well-documented on Twitter). Well, the company that "does God's Work" (ripping off clients) is back approaching $200 after it reported better-than-expected earnings and caught the algobots net short and in trouble.

The fundamental case for avoiding (shorting) GS lies in the macro picture of declining investment banking revenues in 2019 as the global growth story dissipates and is replaced with recession woes. Gone forever is the Blankfein Era and the Teflon Don approach to regulatory malfeasance and benevolent bullet-dodging by the company, which was described as "a giant vampire squid, its blood funnel attached to the face of humanity" so eloquently by Rolling Stone's Matt Taibbi.

As I expect to see happen in the S&P, all markets tend to (as opposed to "must") have "retests" of their respective low points especially after the magnitude of the crash in Q4/2019. The losses from trading in 2019 are still being felt in the earnings reports and the guidance being reported is most definitely trying to gauge the negative asymetrical wealth (poverty?) effect brought about by the many new global bear markets. One thing cannot be denied: Despite the obscenity of the stock market bailout in late December, the S&P did have a closing day that constituted a 20%-plus decline from the highs, and therefore what we are currently witnessing is an exceedingly convincing, classic bear market rally. Goldman Sachs is also having a sharp, endorphin-charging bounce, but with RSI now back in the (overbought) 70s, the beginning of the retest cannot be far away. GS April $180 put options at $3.00 are once again back to a reasonable level, such that a retest of the December lows puts them back at around that magical $30 level. I opened a 25% position on Thursday and failed to trade them when they printed $4.85 immediately thereafter, so I will add an additional 25% early next week and then wait for the stock to roll over, confirming the likelihood that the idea is sound and can work.

As bear market rallies are easily the most elusive narcotic known to mankind, the euphoria being created in January 2019 is a perfect marinade sauce in which to soak the bulls as the bear arises from his well-earned, feast-induced nap begun in late December. When this Papa bear attacks again, he will be twice as violent and five times as destructive, as we get the high-probability retest of the Christmas Eve lows.

Inversely correlated to my stock market thoughts, the current pause in gold and silver should end with both getting an ample injection of amphetamines as the "Fear Bids" return and safe haven buying accelerates in response to any type of retest. However, the timing of that injection will not be an easy exercise, and I emphasize that point because "recency bias" is a cognitive flaw, especially after the emotional beating many experienced last month.

I picked up a graphic off Twitter, and credit goes to Craig Hemke of the TF Metals Report, who tweeted out this morning in a gesture of what I am sure is disgust and outrage.

"The more things change, the more things remain the same," is the quote of the day when I see the open interest balloon like it has. Good for Craig in pinpointing this fraudulent price-capping exercise, which typifies the herding actions of the banking cartel that encourages the ownership of financial assets and discourages any thought of same for hard assets such as precious metals. Truly an outrage of the highest order.

The three big candles shown in the 3-month gold chart are undeniable proof of the interventions of which I have been wary and writing since the 1970s. These are now not only becoming more obvious, they are now actually being telegraphed by way of Twitter and "administration statements." Gone forever are the days when I used to think that maybe I was sensing a little skullduggery in the trading patterns or a smattering of "shenanigans" in the COT figures or bank participation numbers. I now look at the gold and silver markets as "fully rigged," along with stock index futures and the bond markets.

Government officials now view the stock market as a "national security" issue, along with the U.S. dollar. Since the U.S. war machine requires unlimited and infinite funding to police the globe under a U.S. protectionist mandate, there can be nothing allowed anywhere that sheds risk on the status quo. The ultimate Achilles heel of the military is the U.S. dollar's status as the world's reserve currency, and it stands to reason that countries shedding dollars in favor of gold or silver are going to feel the wrath of the price managers.

Forgive my cynicism but the last three sovereign leaders who threatened to take payment for oil in non-U.S. dollar settlement terms were Saddam Hussein, Muammar Gaddafi and Hugo Chavezall deceased in short order and with great dispatch shortly thereafter. Of course, it might be said that Chavez died of "natural causes," but his country (Venezuela) has become a modern-day hellhole after being one of the most prosperous in Latin America a few decades ago. To wit, it comes as little surprise that the bullion bank behemoths executed high-level orders and capped the precious metals rally and U.S. dollar decline last week, coinciding with marvelous symmetry the big pop in stocks.

I was in discussion with Getchell CEO Bill Wagener last week, during which he showed me his NRA membership card and his firearms license, along with photos of his latest sojourn at the firing range in the state of Colorado, where he currently resides. He was offering me some insights on this newsletter and in particular, the opening quote, which is "Gold is the money of kings. Silver is the money of gentlemen. Barter is the money of peasants. And debt is the money of slaves." He asked me if he could add a fifth sentence to the quote: "Lead is the money of the revolution," to which I said "Let's make it, 'Lead is the money of change.'" Ergo, the new jingo for this missive is going to be the one shown at the bottom of the following graphic.

Food for thought?

Going into the upcoming week, I expect to see some profit-taking in the stock market rally, and I will be looking to buy put options on Goldman Sachs and the S&P 500 at some point. However, as you have read here since the Christmas Eve when I showed everyone the RSI for the S&P at 19 and suggested that "the time to be short has passed, "that does not mean that the market has V-bottomed nor does it follow that the advance has to end any time soon. Bear market rallies are dangerous and very difficult to trade because once the mesmerizing effect of the mercurial levitation on clouds of hope and desperation dissipates, you are left with an air pocket bereft of anything but the memories of what exactly took stocks into"crash mode" in Q4/2018. Trade wars, balance sheet normalization, quantitative tightening, and global growth impediments are all still very real threats to valuation, but as we have seen since the 2009 bailout, momentum trumps valuation in this New World Order of algorithmic assignments and interventions.

As you pore over charts and blogs and brokerage reports, just keep one thing pasted above your quote monitor: The "invisible hand" is there to liberate you from your wealth unless you play ball and drink from the party-line punchbowl. Charging stock markets is the champagne narcotic that fills the revelers with confidence and glee; gold and silver are the caffeine that sobers up the room. And the enemy is not without means.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Getchell Gold and Goldman Sachs. My company has a financial relationship with the following companies referred to in this article: Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp., a company mentioned in this article.

Charts and images courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.