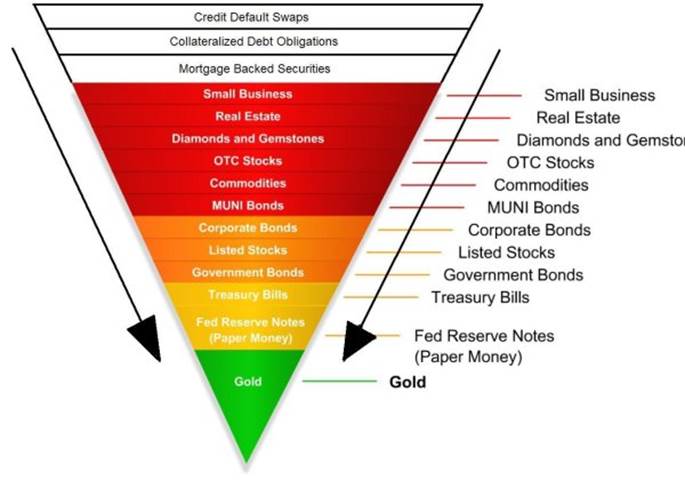

Unarguably, the finest piece of work that I have ever seen on the state of the global financial worldeveris the one recently created and presented by Grant Williams of RealVisionTV entitled "Cry Wolf." I was watching it last evening for the fifth time with my better half (who was watching it for the first time) and despite the fact that as bright and insightful as she is, I could and would not expect her to grasp concepts such as "Exter's Inverse Pyramid" or the definition of a "trophic cascade" but when I glanced over to gauge her reaction to what might have been fairly glutinous material, to my delight she was glued to the screen as the history of her favorite form of metal unfolded in Grant's purely brilliant display of 5,000 years of human folly, greed, and insanity.

The coup de grâce was the ending of the piece where Grant draws a phenomenal analogy between the role of the Grey Wolf in controlling the uncontested overpopulation by the deer and elk of Yellowstone National Park and the role of gold in controlling the uncontested overpopulation by the "money-changers" in global economics. The term "apex predator" is wonderfully applied to gold and the Grey Wolf in that there is no natural predator to keep wolves in check just there are no counterparties to the role and control of gold.

When you look at Exter's Inverse Pyramid, you are looking at a ranking of all assets from the top to the bottom of the risk slope so it is of interest that in the upper half of risk we find none other than real estate, where the city of Vancouver recently reported a 40% drop in residential home sales for December on the heels of a 42.5% drop in November. Prices are down 810% in Vancouver and Toronto as the marginal (foreign) has finally been legislated away as depositories for expatriated Chinese capital. Even New York City has seen a 14% decline in sales with an accompanying 4% drop in prices so the world of asset inflation in the saddle of unbridled money-printing and credit creation has come to a resounding and screeching haltor has it? After Friday's Federal Reserve Lovefest with Janet Yellen and Jerome Powell all sending out dovish signals, perhaps the December rout has altered policy.

Back to the title of this missive, "Cry Wolf" offers the proposition that a return to the gold standard would create a "trophic cascade" of sorts in the financial world. That is to say, an ecological event in which there exists an "apex predator" at the top of the food chain whose re-introduction (as in the case of the Grey Wolf to Yellowstone) to an ecological system triggers a massive metamorphosis of that system. Just as Grant's video depicts changes occurring after the return of the wolves, which include even the rivers, the re-introduction of the gold standard would initiate a change in the financial system whereby purveyors of credit and paper promises would be penalized, and savers and disciples of sound money and fiscal sanity rewarded.

As a true adherent to the rights of all citizens to have their hard-earned savings protected from the ravages of currency debasement, I would welcome any initiative that would wrest the printing presses away from the bankers and the politicians. To wit, this is exactly the message in Grant William's brilliant presentation and it behooves us all to watch over and over and over again until it sinks deep within our cranial vaults and forever alters our ingrained and flawed attitudes about investing, labor and money.

Stock prices closed out the week with a solid gain, which come as no surprise to those who are privy to my Twitter feeds. The time to be short expired once the RSI for the S&P dipped under 25 and the time to go long (for a "trade") was on Christmas Eve when it plunged in a panic liquidation under 20. Notwithstanding that I elected to pass on the long side despite the obvious massive oversold condition that arrived late during the worst December in a decade (at one point the worst December since 1931), I went into Christmas with all (non-precious metals) shorts covered and all puts sold. Only the Santa Claus rally period, defined as the last five days of December and the first two of January, was able to save the month quarter and year for many stock bulls as it eked out a 1.3% gain for the period. Statistically, it infers that there is a distinct possibility that the Christmas Eve lows at 2,351 for the S&P were THE lows but we still need to see what happens after the Monday/Tuesday closes which, if positive, would further enhance the likelihood of a prolonged recovery rally. Without the benefit of a crystal ball, my gut tells me that we are going into a sideways-trending period for stocks as opposed to the "New Highs" halcyon of the past ten years or "New Lows" below the December 24 nadir.

From the trader's perspective, if the Q4/2018 bloodbath did just one thing of importance and one thing alone, it was to alleviate the terror one has been experiencing when even contemplating short selling since the face-ripping fandango of the past few years. "Don't fight the tape and don't fight the Fed!" screamed the late legendary market maven Marty Zweig and no truer words were ever spoken when you look back to 2009 and especially 2018. The last year was a year in which the Fed was openly hostile to stocks by way of quantitative tightening leading to balance sheet reduction and high short-term lending rates, and it finally registered in early October with the rest being history. In retrospect, it is hilarious how the CNBC cheerleaders totally ignored the words of Master Zweig and instead used the phrase "strong economy" no fewer than 652,947 times in the final quarter of the year as a rationale for buying stocks. Forgotten totally was "the horrid economy" of March 2009 when the Fed embarked on its credit-fueled bailout and intervention campaign when that too was an excuse for "buying the dips," proving once again that CNBC is best watched with the "MUTE" button on and only for live data feeds while away from one's workspace. (I overlay a transparent dart board on my TV for maximum adolescent amusement.)

As a trader, I was terrified in early November when I looked at the Goldman Sachs (GS:US) chart in the days after the Indonesian scandal broke because I did NOT see opportunity; I only saw another potential loss from trying to short a big name U.S. bank. What gave me courage was the knowledge that since the Fed was no longer in "protector mode" and social media starting to viralize the GS story, it appeared as though "conditions" had changed, and when conditions change, I change. I bought the GS December $200 put at $3.40 and sold them at $25, which was actually about $15 too early as GS hit $160 by expiry. Nonetheless, I was a nervous wreck throughout.

The point is that with the severe Q4/2018 breakdown in the long-term charts of the global stock markets including the S&P 500, I am no longer engulfed in abject terror at the thought of shorting one of the FANGS or the index ETFs because despite a blow-out unemployment number last Friday and stock-soothing words from Mr. Powell, this current rally is simply a bear market rally and again as stated last week, this Papa bear is simply sleeping off the engorgement binge upon which he embarked last October resulting in him passing out from excessive gluttony on the Eve of the Noel at S&P 2,351. This bear is simply "napping"; he is NOT back into "hibernation."

That said, I am now of the opinion that the elitists are going to attempt to restore market confidence due to their (rightly founded) fear that recent global market turmoil will see the embodiment of the negative asymmetrical wealth effect of declining assets prices. Stocks, housing and commodities are now trending downward and while stocks alone are enough to sour consumer spending patterns, housing has an infinitely greater impact, as we saw in 2006 when the sub-prime bubble triggered the beginning of that catastrophic foreclosure/liquidation cycle. As the Q4 earnings reports start to arrive, we may see accelerated interventions and abbreviated declines as they try to "soft-land" the stock markets. The first five days of January can give you an inkling as to the month of January just as the Santa Claus rally might be giving us a similar bullish hint.

The time to be short has passed us by and while it might be too early to go long the S&P, I await an RSI north of 70 (currently 46.77) for the S&P 500 before I look to establish any shorts and I would avoid any new longs until I see a successful retest of the December lows OR an RSI back under 25. As for the VIX, it has already crashed from 36 to 21 and if there is ANY ONE indicator that smells of intervention, it is the VIX.

Last point on stocks, what spooked me out of all shorts in the days before Christmas was none other than Stevie Mnuchin (U.S. Treasury Secretary) who came out and actually ANNOUNCED that he had called a meeting of the Working Group on Capital Markets and while it "appeared" to have blown up on Christmas Eve, I have ZERO doubt that the Plunge Protection Team were mobilized in force from Boxing Day onward. The action in the gold and silver markets and the massive move in S&P futures immediately following Friday's NFP report were the "tell" along with my curiosity as to why there is no government-generated COT report while the U.S. government is "closed," but there was a magical arrival of the NFP report from yet another government agency that was somehow supposed to be "closed." I do NOT want to be short with shenanigans like this showing up on our doorstep once again. Ergo, I am not.

As to the precious metals and in keeping with my current mistrust of the set-ups from last week, I looked to the RSI on silver as a signal to exit my call option positions, which treated me nicely over the time frame. I did not sell any physical silver nor did I cash the ticket on CDE; all I did was take a little risk off the table last Thursday prior to the NFP Report. While we got a downtick in gold and silver immediately thereafter, they recovered quickly telling me that there is a pretty strong undercurrent of demand for gold and silver here and that pullbacks may be short-lived. I called for a strong Q4 back in August when I wrote "Back up the Truck" and while past luck is no guarantee of future bragging rights, I nevertheless am proud to take the bow just as I did in late 2015 when I called the end of the precious metals bear markets at gold $1,045.

We are undoubtedly entering a period in our lives when "preservation of capital" (AND PROPERTY) is going to replace "return on investment" as the primary objective for a new generation of investors too young to recall a bear market that was ever allowed to go to full maturity without a Fed bailout. Only after they come to the sudden realization that crying into their social media camera phone will not turn back the clock on a margin call will they accept the fact that stocks can and do indeed go down over long periods of time and historically never, EVER get rescued by anyone other than the free market capitalist buying at the lows at the end of the bear market.

Of course, this is where the new generation will flock into the metals because they now recognize that the digital safe haven that they THOUGHT would replace gold and silver as their private, innovative, untouchable store of valuecryptocurrenciesgot absolutely annihilated in 2018. They are slowly realizing that as possession is nine-tenths of the law, allowing a massive supercomputer to control your net worth and savings is nothing short of madness. Yet, despite all of this, social media is still rife with all manner of crypto promotions with bagholding converts all citing various "support levels" from which the next big move to Bitcoin $100,000 will occur. Just as latecomers to the massive 20012011 precious metals moonrocket were mimicking "$5,000 gold!" for months and months and months after they paid $1,800 then $1,700 then $1,500 after the 2011 peak and were soundly thrashed, so, too, will the crypto-junkies be thrashed and forced kicking and screaming into precious metals ownership. Right behind them will be the weed-o-philes and behind them the FANG-buying stockroaches complete with their "DOW 30,000!" baseball caps and CNBC tee-shirts.

Gold prices have had a blistering move since my entry point in late August, albeit we had a few scares along the way before lift-off finally came through. Nevertheless, a $110 move in gold is not to be sneezed at with the GLD April $13 calls recommended in November at $1.00 and then followed up a week later with a strong, table-pounding, screaming "BUY MORE!" when GLD briefly sank back under $114.00. The April calls closed out the week at $1.90 and I have not, as yet, sold them but will be watching eagerly Sunday evening as the Globex opens at 6:00 p.m. EST to see if the PPT shenanigans from Friday carry over into the new week.

To be honest, both my partner and my loyal dog, Fido, both bolted on Friday, off to destinations unknown either the wife to the sister's house and Fido to the cavern below the tool shed (or was it the dog to the sister's and the better half to the oh never mind) but the karma in my den which has been in total harmonious Nirvana for the month of December has been shattered like an icicle falling from the eaves. I might be a tad paranoid but I am of the belief that the same forces that conspired to screw us in 2013 and which stepped up every time the S&P had more than a 5% dip since 2009 are back "in the room" and whether or not that is why I find myself alone is not important. What IS important is that we hang onto the greater portion of gains in gold, silver and our beloved miners bestowed upon us in Q4/2018. Gold gained 7.53%, silver has gained 15.54%, and the HUI (gold miners) has gained 13.83% in Q4, so I'll be damned if I am going to give back any of those gains. I will know early in the week and if I see something between now and the opening, I will send out an email flash or a tweet.

Dr. Copper: Is the good doctor telling us to head for the exits?

As we head into the first real trading week after the low-volume holidays, it will be critical to observe the behaviors of all of the metals, including Dr. Copper, to try to discern the direction of the portfolio. Copper and silver once were strongly correlated and now have diverged, freeing the algobots from pounding silver every time the base metals have a hiccup. The chart shown here is a strongly bearish one, albeit somewhat oversold based upon the MACD/Histograms yet not so for the RSI. The trend is definitely down and until proven otherwise, copper's performance appears to be confirming that which we all suspect to be truethat before too long, the Fed, the PBOC, the ECB and the BOJ will all be in simultaneous and cleverly coordinated EASING and when that happens, the USD is going to get smoked.

The 10-year U.S. Treasury yield has crashed from just under 3.25% in October to 2.67% today which, in the bond world, is a cataclysmic, several-sigma event. As I have written of before, the bond market is infinitely wiser than the stock market in forecasting events and while the Fed can intervene in gold pricing and at the short end of the curve, it has a very tough time with the 10-year. Ergo, my portfolio will be tilted in favor of a watershed-type of event that sees a cessation in rate hikes and a stay in central bank balance sheet reductions. The eardrum-splitting sirens you will then hear are the emergency alert warnings from all FOREX desks across the globe calling all to EXIT the U.S. dollar for the final time, as its reign as the globe's reserve currency comes to a resounding end. With that, gold and silver prices will soar and our gold miners and explorers will flourish.

However, before that happens, remember this: in the animal kingdom, there is nothing more dangerous than a wounded beast. Just as the vast majority of the ecosystem fears man above all as the planet's premier "apex predator" (no natural enemies left), the only creatures that do NOT fear man are insects, sharks, wolves, Komodo dragons and one otherthe "wounded" creature of all shapes and sizes. Even a cornered, injured raccoon can be a fearsome and lethal threat if trapped and desperate.

In this manner, I see the world's central bankers in exactly the same venuetrapped and wounded and in desperate need of a solution to a "problem," which they themselves along with their politician cooperatives actually created. That is why I am going to hold on to my physical precious metals as core positions and not available for trading but as call options; they will be the first to go with the miners a close second in the event that we get a gold/silver-hostile series of events next week. If we do, it means that the "invisible hand" has not stopped with the Friday intervention and that they will continue just as they did in 2013 and crush bearish sentiment for stocks and bullish sentiment for gold and in any way they choose.

I close it off with a chart of how throughout history stocks responded to drops of at least 20% in the period immediately thereafter. The one difference is that until 2009, there was no such thing as central bank or government intervention in markets while here in 2019, it is rampant. Keep that in the forefront of your trading and investing psyches and be very, very careful as you do. More to come later in the week. (@MiningJunkie)

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.