A Brief Word on Forecasts

Each year between December 25 and January 1, every blogger, analyst, newsletter guru, or market historian like me issues their "forecast" for the upcoming year, and what I find a worthy exercise is to go back and read what we all wrote in the same manner that, as a youth, I used to track the meteorological forecasts of the famous CBC weatherman, Percy Saltzman.

The one thing that has struck me over the years is that forecasting markets is rarely much different than the trackman's picks at Woodbine Race Track or the Vegas line on football games or Percy's chalkboard alchemy deciphering rain clouds. Even when forecasts of economic or financial events are correct, particularly in the years following the 2008 Great Financial Bailout, the outcomes have been skewed at best and bizarre at worst. To watch as trillions of dollars, pounds, euros and yen were magically created out of thin air while the two monetary metals were prevented from levitating through government edict is a clear and present danger to the art of prognostication.

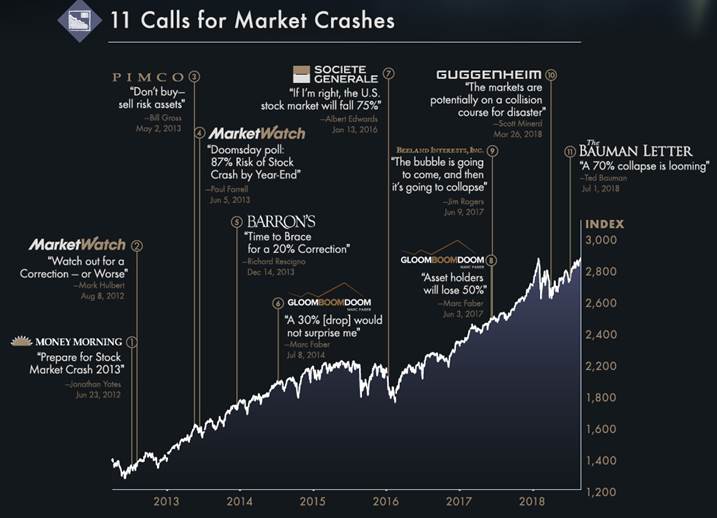

So take this missive with a large grain of salt and try to find amusement or value in it, but as the graphic below clearly indicates, forecasting markets is an inexact and difficult science.

Eleven bogus market crash calls over six years

Stock Market Outlook: As we close out the final few trading sessions of 2018, I want you all to observe what I was looking at this time last year when I wrote my 2018 Forecast entitled "2018: The Year of Living Dangerously," in which I gave these closing remarks:

"With the Internet now a massive source of investment knowledge, opinion and deception, you will soon be reading voluminous tomes of 'Get rich quick!' e-mails designed to liberate you from your hard-earned savings and critical investment capital. The quote I inserted above is really all one needs to know about asset prices in the years ahead. The Fed will have a new chairman in 2018 and the critical question is 'Will the punchbowl be drained in 2018?' For the past nine years, there has been an injection tube feeding the financial punchbowl with all manner of fiscal and monetary stimuli, which has kept all bank collateral (real estate, stocks, bonds) afloat despite massive debt and swamping entitlements obligations. The Fed has stated that this tube is now shut off as the tightening cycle has begun.

"However, if inflation rears its ugly head and it causes civil discontent, the tube will not only be removed, the plug at the bottom of the bowl will be removed and the contents allowed to drain. Food prices, rents and healthcare will be the barometer by which policy pitchforks and torches are trotted out, so keep your seatbelts securely fashioned in the New Year and stay alert. Draining punchbowls do not permit rising stock markets and rampant speculation.

"2018 will be an interesting year."

Well, 2018 was indeed an extremely interesting year. as that heavily telegraphed but even more heavily ignored punch bowl-draining by Jerome Powell has finally ended the longest bull market in history, with the S&P closing out Christmas Eve down over 20% from its Oct. 3 zenith of 2,929.86. In case you didn't get the memo, we are now officially in a bear market, and because this bear has been hibernating with not so much as one decent correction since February's 11.68% warning shot, he was an enraged, starving Papa Bear. What people are ignoring is that in the past eleven weeks he has enjoyed one massive gluttonous feast on the carcasses of shell-shocked "BTFD"-ers. While this bear was bulging-eyed ravenous on Oct. 3 from years of neglect, for the past eight weeks (save last week's PPT stick save) he devoured everything in his path and is ready for a brief respite from his engorgement, perhaps a nap for a fortnight or so as he prepares for his next Millennial Meal.

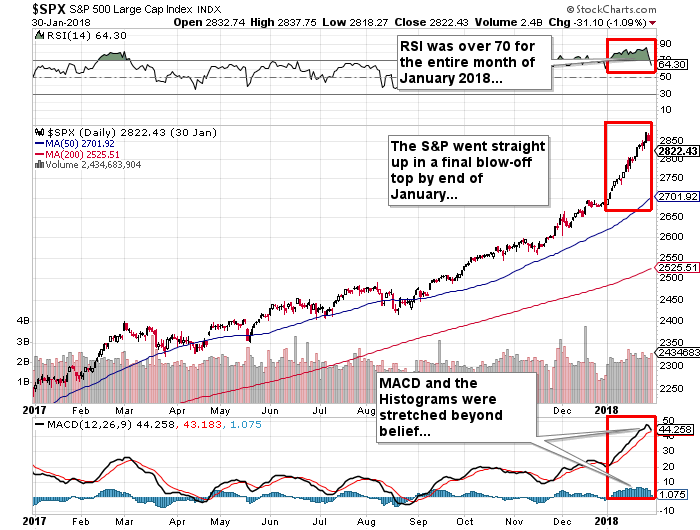

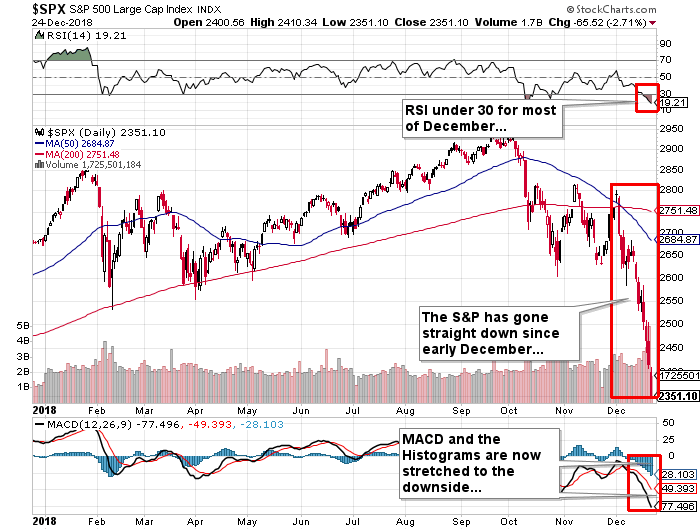

The reason for my sudden newfound bullishness lies in these two charts. The first takes us to the end of January of 2018, when RSI has spent literally the entire month in a plus-70 overbought condition before getting tagged in early February. Sentiment was at an absolute extreme and while I was certain of an impending downside reversal, I played it through volatility, and on Jan. 16 began to scale into the UVXY below $10 with a target of $30. Less than ten trading days later, I exited, a tad early, but averaged the mid-$20s. Fast forward to December, and as the second chart clearly shows, conditions are today a virtual carbon-copy opposite of those of eleven months ago. So, if conditions were screaming sell last January, they are most certainly screaming buy, perhaps less loudly today than on Christmas Eve, but still a solid buying opportunity on a retest of the lows around 2,351 on the S&P.

Now, before you take what room you have left on your credit lines and load up with your favorite FANG, understand that this year may see a tax-related downside phenomenon occur, where longer term investors still sitting on terrific gains from the 2009 meltdown are awaiting the end of the fiscal 2018 trading period to book their long-term capital gains, which involves a lower tax rate in the U.S. The ideal entry should be after Dec. 27 for those brave enough to take the plunge.

As an aside, please do not think for a moment that a 150-point (or so) pop in the S&P 500 would qualify as a "bottom" because the singular most violent of all upside moves occur within the context of bear market rallies. Greed-fueled "hopium" is infectious and it forces investors to panic into positions fearing that they are going to miss the bottom. It isn't until the last bull capitulates and swears to never buy another stock ever that real investable bottoms arrive, and I assure you they do not happen two days or two weeks after a new bear market has just been pronounced. That being said, I should urge caution because in the New Era of Interventions, anything is possible, as we saw on Boxing Day.

Commodities Outlook

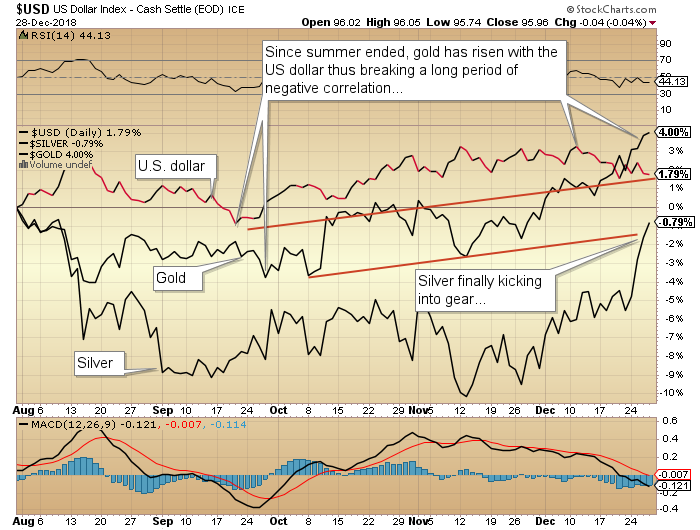

Gold: You all recall the late August "Back up the Truck" call on gold (and silver), after I correctly interpreted the Aug. 16 reversal as the low at $1,167, and then added silver a few days later in the $14.50 range. It was a fitful start to what I think is a longer-term move to $1,400 gold and $28.00 silver. But after grinding back and forth with annoying frequency, silver has finally punched out through the $15.00 ceiling and quickly taken the Gold-to-Silver-Ratio (GTSR) from 87 on Monday to 84.22 this morning.

As I have written about for the past thirty years, you simply cannot trust any gold rally where the gold miners (GDX, GDXJ) and silver (SLV) underperform. They should lead the advance and by default, the GTSR should be declining. Until lately, we had not seen silver do anything close to outperforming, but what we have seen is the gold miners (HUI) put on a blistering performance versus both gold and silver, up 11.57% since the end of August.

However, on Boxing Day the silver market closed up 1.86% versus gold's late-day reversal decline of 0.16% and that is the type of outperformance badly needed to fuel the advance.

This next chart shows how well the gold miners have done when measured against the spot price. The gold miners have been outperforming bullion since mid-September but must continue this outperformance to avoid non-confirmations (to gold's advance), which always bring out the bears.

Tactics: I have elected to own physical gold plus the GLD April $120 calls at $4.30 for added leverage. I am going with two exploration juniors, Getchell Gold Corp. (GTCH:CSE) and Stakeholder Gold Corp. (SRC:TSX.V), plus one discovery junior, Great Bear Resources Ltd. (GBR:TSX.V; GTBDF:OTC), as my proxies for gold ownership. I particularly like GTCH for reasons mentioned in previous missives and which can be revisited here (report) and I am adding to SRC because of the upcoming drill program in Nevada by Seabridge Gold Inc. (SEA:TSX; SA:NYSE.MKT) on the Snowstorm property situated adjacent to SRC's Goldstorm property. This could be a serious tailwind for SRC as we move out of winter.

Silver

2019 is going to be the year silver outperforms gold, copper and the mining stocks. It has been under enormous pressure from secondary supply sources, the bulk of which is byproduct deliveries from the big base metal miners. After the 2016 peak above $20, silver went into total "lockdown" with the bullion bank behemoths, acting under the guise of "hedging," opening massive open interest in CME futures and smothering all forms of momentum, sentiment and upward movement. Only until the Justice Department indicted JP Morgan for manipulating the silver market a few months ago did it at least "appear" as though the shackles had been finally broken. Needless to say, silver is cheap relative to gold and cheap relative to the S&P and cheap relative to credit so one must surmise that it has to be ownedperiod.

Tactics: While physical silver is my favorite way to play this metal, I have owned the SLV (iShares Silver Trust [ARCA]) April $13 calls from mid-November, when I advised purchases over a three-day period and averaged $1.00 per contract as an average price. As we close out the year, they are currently $1.65 and I have a target price of $10 by expiry on April 18. Also added to the list is Coeur Mining Inc. (CDE:NYSE), originally recommended in December in the $4.25 range; this stock was above $8.00 in July and was north of $16 during the first upleg of this bull market in 2016. I will carry a Q1/2019 target of $8.00 and use a $3.95 stop-loss. Silver is my odds-on favorite of all the metals for 2019.

Uranium

The uranium outlook is based largely on the elimination of excess supply created in the immediate aftermath of the Fukushima incident seven years ago. Seeing as uranium has been in a long and agonizing bear market since then, I decided in 2016 to look into the industry because the one thing that leaps off the page for uranium stocks is that when the price turns up, they absolutely rocket.

In 2016, I was introduced to the founder of U.S.-listed Energy Fuels Inc. (UUUU:US), George Glasier, who was then and is now the founder and CEO of Western Uranium & Vanadium Corp. (WUC:CSE; WSTRF:OTCQX), a Colorado-based uranium/vanadium developer whose primary asset is the Sunday Mine Complex (SMC), located in Nucla, a uranium-friendly area of the state. By assisting them in raising money, I was forced to do a great deal of research on the uranium industry, and because there exists a large vanadium resource at the SMC, it also shifted my focus to the shifting landscape for this little-known "battery" metal, whose primary use lies as a hardening agent in steel production.

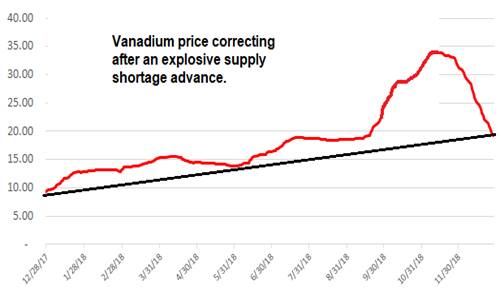

With new Chinese regulations calling for increased minimum hardness for steel used in the construction industry, China went from a net vanadium exporter to a net importer in the stroke of a legislative pen. With end users thrown into a frenzy, the vanadium price peaked just under $35/lb in November before correcting to under $20 in December. Nevertheless, with a 75 million pound uranium resource and a 35 million pound vanadium resource, the in situ metal value of the SMC resource is approximately $2.9 billion. When compared to WUC's $27.2 million market cap, the valuation case for investment is compelling. To own any company at less than 1% of its resource value is usually a wise move and I decided to do exactly that.

Because the Sunday Mine Complex is going to be immediately accretive to any acquirer due to the impact of the upcoming Section 232 investigation petitioned by a couple of domestic producers, acquirers of WUC could pay up to U.S.$100 million for WUC and secure a U.S.-based supply source for a metal increasingly strategic to American security interests. The existing infrastructure at the SMC is all in place, and as the company has announced intentions to reopen the complex in the New Year, the vanadium ore could be available for sale and shipping in early 2019.

I am not expecting WUC will be around to enjoy the upcoming lift in uranium prices because it will be acquired by another entity in desperate need for vanadium or feed for an existing mill currently operating well below capacity. With a 52-week high at $3.32, the current $1.50 level appears to be a reasonably attractive entry point.

Tactics: Buy WUC/WSTRF in the CA$1.50/US$1.20 range with a stop at CA$0.95/US$0.70. Target: US$3.40

The last trading week of the year has been incredibly volatile, with Dec. 26 and 27 recapturing about 150 S&P points. I was going to write that I expected stocks to be higher over the next thirty days but that was at 2,351.10 on the S&P 500 on Christmas Eve, before the Plunge Protection Team (PPT) came riding in on Boxing Day on a huge white stallion.

All around the social media world, there were polls asking whether Trump would fire the Treasury Secretary or the Fed Chairman first. Big N.Y. money then went to work and pounded out the largest one-day advance in history, with the Dow flash-spiking over 1,000 points with the algobots all short and going totally berserk in the final hour. See from the charts shown at the start of this missive that a bounce from ridiculously oversold conditions was overdue, with the RSI for the S&P under 20. CNBC was forced to change its scripted narrative, and after broadcasting Mnuchin's "PPT call" all weekend, they changed their story to credit "Pension Fund Rebalancing" as the reason for the turnaround. The PPT-fueled updraft saw the RSI nearly double, but still left the S&P down 9.12% for the month and that was after the late-week rebound. It would seem that intervention interference in "free market capitalism" is alive and well.

Tactics: Avoid buying anything until we get the retest of S&P 2,351. If I see 2,550 next week, I will be looking to buy puts. If instead we see a retest of the Christmas Eve lows, I will issue an alert via email or Twitter. (@MiningJunkie )

Base Metals

The base metals (ex-batteries) will be slave to the trade war rhetoric and until clarified, I am avoiding them with a special aversion to copper.

Tactics: The ProShares Ultrashort "basic materials" ETF is the inverse or bearish vehicle for shorting the base metals. While I am not including it in the model portfolio, the SMN April $35 calls at $3.40 are a speculative trading suggestion for the risk-oriented punter.

No matter what happens next, remember that all bear market bottoms will demand a secondary retest, so since I was a fraction too late in making the "go Long for a trade" call on Christmas Eve, I am convinced that we are in the very, very early stages of what history may prove to be the Grandfather of all Bear Markets. That is not to say that stocks can't trade sideways for a while. But based on the RSI reversal last week (19 to 41 in three days), the time to be net short has past, at least for the next few weeks.

Tonight I am typing in the wee hours of the 'morn and quite content to tell you all that after forty-one years as a financial person and forty-four years as a stock market investor, I have never been more certain that the world and its entitlement-driven masses are going to be soon screaming for a global currency benchmark. It won't be the tinfoil hats you see at all the newsletter pumpathons warning you of impending social chaos; I was first exposed to that in 1976 with Harry Schultz. It is going to be a demand by the masses for a return to fiscal sanity by all nations in order to restore the sanctity of the work ethic.

To have non-elected government officials traveling executive class drinking complimentary champagne and arguing with the flight attendants over their "right to a meal of my choice" is worthy of the same fate endured by Marie Antoinette and her elitist intelligentsia. I made money in markets over the years based upon my ability to understand causation and predict reactive outcomes. In the "Knives and Bearskins" era of the 1970s, I would pore over the Standard and Poor's index cards, and once I had a balance sheet or income statement that looked extraordinary, I would either buy or short the company's stock and be fully prepared to take my lumps if my assessment of future performance was faulty. Since 2009 (and many would argue long before that), the markets have behaved in a most unusual manner. Stocks no longer respond to news but rather to the tape action; fundamental causation is now dead.

We "old folks" have been left largely behind by a new wave of tech-savvy Millennials that watched their grandparents go virtually bankrupt by plunging their savings into gold and silver in response to the credit-creation, money-printing orgy of the post-2008 meltdown. These youngsters saw through the charade of intervention and government-sponsored fraud post-2008, and instead created their own "safe haven" in the form of cryptocurrencies. While it is true that I called the top in Bitcoin in 2017, I was nowhere near as smart as these kids who embraced its introduction at penny-pricing levels somewhere around 2009 by a Japanese computer whiz called Satoshi Nakamoto. If you had mined 1,000 Bitcoin units as a response to the bankster-driven bailouts of 2009, your cost base would have only been "labor," and if you were lucky enough to have sold it in 2017 at the December top, your "labor" would have yielded $19,891,000. These kids took the Dot.Com Model of the late '90s and they perfected it to the point where CNBC was flashing the BTC price minute-by-minute late last year right beside the Dow, S&P, and NASDAQ!

So, with the cryptojunkies now neutralized and the potheads in full retreat, it is my expectation that 2019 will see a return to true, full and plain discovery of price. The terms "price discovery," "transparency" and "integrity" are three of the most important assumptions upon which investment decisions are made. If there is any hope of avoiding a devastating outcome for portfolios in 2019, it will lie in the restoration of those three attributes for not just the stock market but for all markets where public participation is present. Interventions must be eliminated from all markets where the malodorous misallocation of capital has gone unpunished and where market mayhem is encouraged to run amok. If you believe as I do that the moral hazards created by the Great Financial Bailouts of 2009 (and beyond) have yet to be expunged, then the only place to be is in the monetary metals, where physical possession avoids confiscation and corruption.

Cutting directly to the quick, here is what I own going into 2019 with the idea being the establishment of the model portfolio. In 2019, I am offering an informational service that will allow subscribers (US$799 per year) to access changes to the portfolio as well as short-term trading ideas (such as the VIX, S&P, and junior exploration trades) via my GGM Advisory e-mail alerts. Please forgive the brazen solicitation of your hard-earned after-tax dollars but please remember that the taxman considers investment publications as legitimate business expenses. Also, when you look at the January 2018 VIX trade where I rode 5,000 UVXY from around $10.00 to $25 in eleven trading days, a 100-share position would have alone paid for the service more than twice over.

I wish everyone out there a very Happy New Year and deserved prosperity, health and peace of mind in 2019.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Read what other experts are saying about:

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Getchell Gold Corp., Stakeholder Gold, Great Bear Resources, Western Uranium Corp. and Coeur Mining. My company has a financial relationship with the following companies referred to in this article: Getchell Gold Corp. and Western Uranium. My firm no longer does consulting work for Stakeholder Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Seabridge Gold, Great Bear Resources and Energy Fuels. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Western Uranium and Vanadium. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp., Western Uranium and Stakeholder Gold, companies mentioned in this article.

Charts courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.