It has been a busy, and volatile, last two weeks for RumbleOn Inc. (RMBL:NASDAQ). Shares in RMBL suffered from a PIPE financing done to facilitate the acquisition of Wholesale Inc., and announced in the midst of the market selloff. The stock went from just under $9 to below $5 as the market reacted to the financing, the acquisition and reduced guidance from the company.

Since then, shares have been bouncing back as investors digest all the news and start to understand the value of the acquisition along with the logic behind the company's self-imposed guidance miss. To help investors get a better understanding of the combined businesses and management's plans for the future, we caught up with RumbleON's CFO, Mr. Steven Berrard.

Tailwinds Research (TW): First off, just to clarify guidance from your recent shareholder update call. You closed the acquisitions of Wholesale Inc. and Wholesale Express LLC in Q4 but your guidance for 2018 doesn't include this, right?

Steven Berrard (SB): That is correct. We closed the acquisition and became the owners of Wholesale Inc. on October 30th. We believe it is prudent to provide guidance for the full year 2018 excluding the Wholesale Inc. and Wholesale Express LLC acquisitions.

Our goal is to be transparent with Wall Street and we believe guiding to full year 2018 exclusive of Wholesale Inc. and Wholesale Express provides investors and analysts a baseline to measure our progress towards our primary objectives and our organic growth rate.

For the same reasons, we will report our 2018 annual and fourth quarter results both on a standalone and proforma basis. The latter will include operating and financial results for Wholesale Inc. for the months of November and December.

~ Tailwinds Sidenote: 2019 guidance from RMBL is for revenues of $900M $1.1B and EBITDA of $15-18M. With an enterprise value of around $120M, RMBL trades for 8X EV to EBITDA (using the low end of guidance). ~

TW: What synergies do you expect from this acquisition? Are any realized synergies incorporated into guidance, or additional upside?

SB: RumbleOn believes that the combined company will benefit from incredible synergies:

- Access to Pre-Owned Car and Truck Markets With annual unit sales of more than 20,000 units and average inventory of more than 2,000 units, Wholesale provides RumbleOn an immediate and accretive method to access the 44 million annual unit sales pre-owned car and truck business. RumbleOn will be the only nationwide online provider that allows for the buying, selling, trading, financing and listing of any vehicle across all segments.

- Accelerates Natural Expansion Opportunity Eliminates the significant start-up costs, time and resource investments typically associated with new market entries.

- Capital-Light Model Unlike other pre-owned vehicle retailers, RumbleOn does not need to ramp hiring and deploy additional resources around the country in order to enter new markets.

- Extends the Online Acquisition and Distribution Model Leveraging RumbleOn's 100% online model, will produce purely incremental purchases and sales of highly desirable and profitable inventory for Wholesale Inc. to consumers and dealers.

- Supply Chain Solution Focus pre-owned vehicle acquisition on controlling the inventory at the source will prove to be a winning proposition in the supply of vehicles for consumers and dealers that will span all pre-owned vehicle segments. RumbleOn was built around inventory acquisitions and optimize our business through a completely agnostic distribution model.

- Agnostic Distribution Multiple sales channels allows RumbleOn to maximize revenue by selling to the channel where the opportunity based on customer demand, market conditions or inventory availability is the greatest at any given time. Adding RumbleOn's powersport vehicles as a new source of inventory will provide incremental volume and improved gross margins to the current Wholesale distribution platform.

- Branding and Marketing RumbleOn will market under the Wholesale Inc. brand, independently as a separate channel and in parallel, taking advantage of two brands and capitalizing on the associated marketing leverage.

- Powerful Technology Platform The powerful technology suite includes integrated vehicle appraisal, inventory management, customer relationship and lead management, equity mining and other key services necessary to drive the online marketplace.

- Trusted Logistics Wholesale Express, LLC has become a well-known brand for the movement of thousands of cars and trucks for dealers across the country. RumbleOn's logistics across powersports will be moved onto the Wholesale Express platform, which will drive sustainable, long-term cost benefits.

These expected synergies are incorporated into our 2019 guidance, but we believe there is plenty of upside to be had and look forward to providing updates in the future.

~ Tailwinds Sidenote: This is not management's first time at the rodeo. CEO Marshall Chesrown built a large chain of auto dealerships which he sold to AutoNation and CFO Berrard is a co-founder of AutoNation where he led their aggressive expansion strategy. ~

TW: Your core motorcycle business is growing rapidly, but you did reduce your guidance for that segment of your business. What caused the miss in guidance on the motorcycle side?

SB: There were several factors that impacted our results. Some of which were intentional, and others an artifact of the macro environment:

- We made the decision to terminate any cash offer that did not produce a $1,000 of margin in August. This resulted in 12% gross margin per unit in the third quarteran 80-basis point improvement over the second quarter.

- The flow-through of the change I described is higher-quality inventory, but less inventory and thus less sales volume than we had previously assumed in our forecasts. Our cash offer tool is an incredible vehicle acquisition tool for the company and we will continue to tune our cash offer algorithm with an eye on optimizing margins.

- Reducing the cash offer made to consumers by 10% in response to the seasonality of resale pricing being experienced during the quarter.

- 2018 is our first full year in operations and we are still learning the seasonality of the business. For example, we learned that a major holiday, such as Fourth of July, falling in the middle of the week impacts our customers' behavior for the full week, rather than one specific weekend, as we previously forecasted.

The effect of these factors resulted in a reduction in vehicles acquired and sold. While volume was down from our previous expectations, we believe that the negative impact to unit sales in the quarter was offset by other benefits we realized such as, enhancing the RumbleOn brand, driving continued gross margin expansion and protecting the quality of the customer experience.

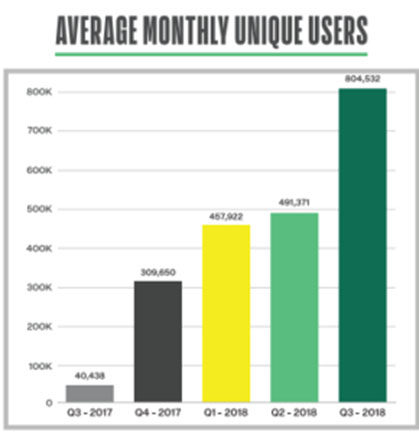

~ Tailwinds Sidenote: While below expectations, growth in the third quarter is still phenomenal and a big uptick from the second quarter. See below graph. ~

TW: Competitors trade at significantly higher multiples. How do you explain this? Can you compare your models with them?

SB: I am not going to speak to our stock price or valuation, but our competitive position in the market is a really important point to consider. We don't view any of today's players as a true competitorand the market has significant barriers to entry. We have the benefits of both a large brick and mortar auto reseller, and a capital-light online model, without being a true competitor with either. What I mean is that:

- Our strategy is to acquire our inventory primarily from consumers, the lowest cost vehicle acquisition channel, enabling us to optimize our margins. We believe that controlling the inventory at the source will prove to be a winning proposition in the supply of vehicles for consumers and dealers, as it has proven to be in the powersports markets.

- While we built RumbleOn around inventory acquisitions, we optimize our business through a completely agnostic distribution model. Multiple sales channels allow us to maximize revenue by selling wherever the opportunity exists, based on customer demand, market conditions or inventory availability, at any given time. Our agnostic distribution strategy means that we offer the same vehicle to dealers and consumers simultaneously, which results in our ability to maintain our incredibly low inventory turn, which was 31 days in Q3.

- We are building a supply chain solution that will span all pre-owned vehicle segments. Wholesale accelerates our plan to enter the huge automobile marketplace and allows us to do it with meaningful size and scale, and without the significant start-up costs typically associated with new market entries.

- We are building a supply chain solution that will span all pre-owned vehicle segments. RumbleOn will be the dominant marketplace in online acquisition of vehicles direct from consumers and dealers while continuing its agnostic distribution approach of rapid turns of vehicle supply.

~ Tailwinds Sidenote: Carvana (CVNA) has an Enterprise Value $6B which is 1.6X estimated 2019 sales, while expecting negative EBITDA for next year. RMBL's Enterprise Value is at 1/6th estimated 2019 revenues with positive EBITDA. ~

TW: There's concern that the economy peaked in Q2. What happens when the economy slows?

SB: We believe that an economic slowdown may provide an opportunity for RMBL to significantly increase market share. The fact that we have minimal brick and mortar facilities or the staff to manage such facilities allows us to remain competitive with our brick and mortar competitors. Instead of our margins and profits being used to maintain facilities and people we can continue to invest in marketing and opportunistic product procurement while offering customers highly competitive pricing

TW: How do you interact with iconic brands like Harley and Indian?

SB: We believe both manufactures clearly see the impact we are making on the market and the host of opportunities we will create over time. Because they manufacturer new products which we don't buy, sell or market we do not present any risk to their core offering, instead however, over time our data will be very valuable to them and assist them in bringing new riders to the market by bringing used equipment out of garages and re-marketed to new riders who will need service and may want to buy branded equipment and clothing.

TW: The great thing about data is improvement in business models and metrics. Are you seeing any improvement over time as you mature? Is there an opportunity to improve Wholesale through better use of technology?

SB: Data is the key driver of our business as we grow. Everything we do from acquisition through distribution is data driven. Since we capture the same high level of data on every cash offer whether we acquire the asset or not, the value of understanding year, make, model, miles, condition, location, customer info and so forth is valuable data for many.

As we noted in our shareholder letter, we will integrate our powerful technology with Wholesale, enabling us to acquire cars and trucks direct from consumers and creating liquidity, while maintaining our capital-light and agnostic distribution model that underpins RumbleOn today. We are excited to bring RumbleOn's technology and processes to Wholesale. Increasing the inventory sourced from consumers will provide incremental volume and improved gross margins to the current Wholesale distribution platform.

Further, RumbleOn will market the current Wholesale inventory on RumbleOn.com to provide the same friction-free transaction RumbleOn currently offers to motorcycle and powersports consumers and dealersas well as our upcoming consumer-only platform, rumbleonclassifieds.com.

I'll also note that we will be moving RumbleOn's logistics to Wholesale Express, which will drive sustainable, long-term cost benefits. Wholesale Express, LLC is well-known for the movement of thousands of cars and trucks for dealers across the country and we will benefit from their established brand and reputation.

TW: Where do you envision the company in three to five years?

SB: RumbleOn will be known as the only one stop marketplace platform that you can buy, sell, trade, finance ANY vehicle of any kind from your home computer or mobile devise. The only place where you can trade a motorcycle on a car, a boat on an RV and so on across the entire spectrum of vehicles. We will have an unparalleled image of trust with consumers and dealers since we are the provider of instant liquidity in an easy friction free process. RumbleOn will give you cash for your asset or help you sell it via our Classified option, which we believe will be a business model to effectively match and most importantly we do it all truly 100% online.

Daniel Carlson is the founder and managing member of Tailwinds Research Group and its parent company DFC Advisory Services, which is a licensed registered investment advisor (CRD # 297209). Tailwinds is a microcap focused research company that provides research on and consults to over 20 emerging growth companies in the technology and life sciences arenas. DFC Advisory Services is an RIA that manages money dedicated to investing in the companies covered by Tailwinds. For more information on these two companies and their track record, please see www.tailwindsresearch.com. Prior to founding these two entities, Dan spent many years working with small public companies, having been CFO of two public companies and helping finance many others. A 1989 graduate from Tufts University with a degree in Economics, Dans formative years in business were spent as an equity trader, first on the Pacific Coast Stock Exchange then on the buyside at several multi-billion dollar firms.

This article was submitted by Tailwinds Research. For more information on Tailwinds Research or on RumbleOn, please visit www.tailwindsresearch.com.

[NLINSERT]Disclosure:

1) Daniel Carlson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: RumbleOn. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: None. For a full list of disclaimers and disclosures, please cllick here. I determined which companies would be included in this article based on my research and understanding of the sector.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.