Drilling at Clayton Valley Lithium project, Nevada

1. Introduction

Despite negative sentiment in commodities and especially lithium of late, Cypress Development Corp. (CYP:TSX.V; CYDVF:OTCQB; C1Z1:FSE) keeps delivering the goods at its Clayton Valley Lithium project in Nevada at high speed. A Preliminary Economic Assessment (PEA) was announced at September 6, 2018, and the resulting economics were impressive. An after-tax NPV of US1.45 billion at an 8% discount rate and an after-tax IRR of 32.7% (LCE price of US$13,000/t) indicate the large size of Clayton Valley, making it a potential buyout or JV target for one of the major players like nearby Albemarle. This is exactly the kind of growth CEO Bill Willoughby had in mind when he signed up with Cypress Development, as he saw the potential for the large assets of Cypress one day gaining serious attention. Let's have a look where Clayton Valley stands at the moment, after this PEA.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. PEA

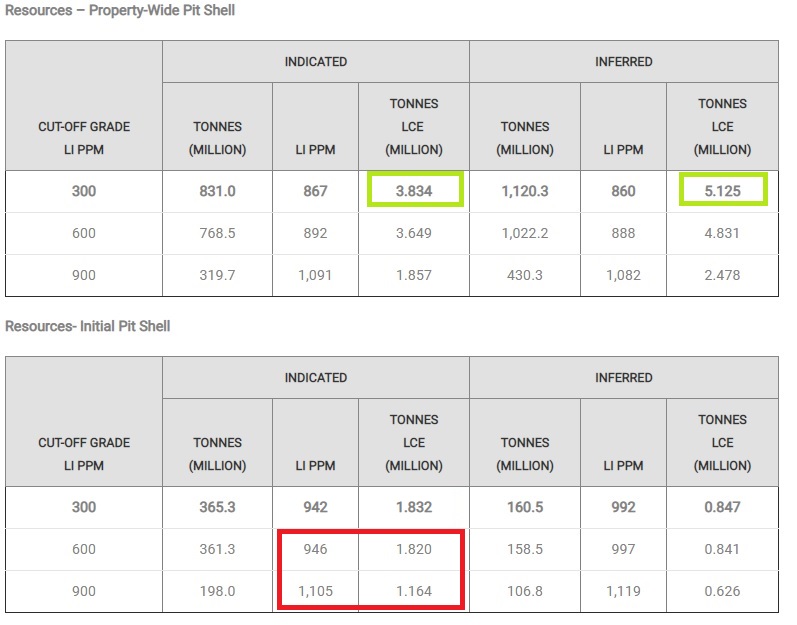

The new PEA wasn't just an impressive study in itself, as it beat my expectations for NPV (my hypothetical NPV7.5 @US$12,000 would come in at US$966 million vs the PEA NPV8 of US$1,260 million; on the other hand the hypothetical IRR at 33.8% was slightly better vs the PEA IRR of 29%), Cypress Development also updated its resource statement. Notwithstanding the first NI-43-101 compliant resource estimate of 6.5Mt LCE that was already world class, the company now has almost 9Mt LCE (see green markers):

Again, as a continuous reminder, examples of world class sized LCE deposits in each category are brine projects like Cauchari/Olaroz (Orocobre 6.4Mt LCE, SQM/Lithium Americas 11.7Mt LCE), clay projects like Sonora or Thacker Pass (Bacanora: 7.2Mt LCE/Lithium Americas: 8.3Mt) or hard rock projects like Whabouchi (Nemaska: 4.06 Mt LCE). Although Cypress doesn't have reserves yet, for size it is the largest clay-hosted deposit in the Americas at the moment.

For the PEA the company has elected to use only the high-grade portion to the east of the deposit (see red marker), with an average grade of plant feed ore of 1012 ppm Li. This is a viable option as the deposit is so big that high grading it results in a life of mine of 40 years at an annual production of 24,000t LCE anyway.

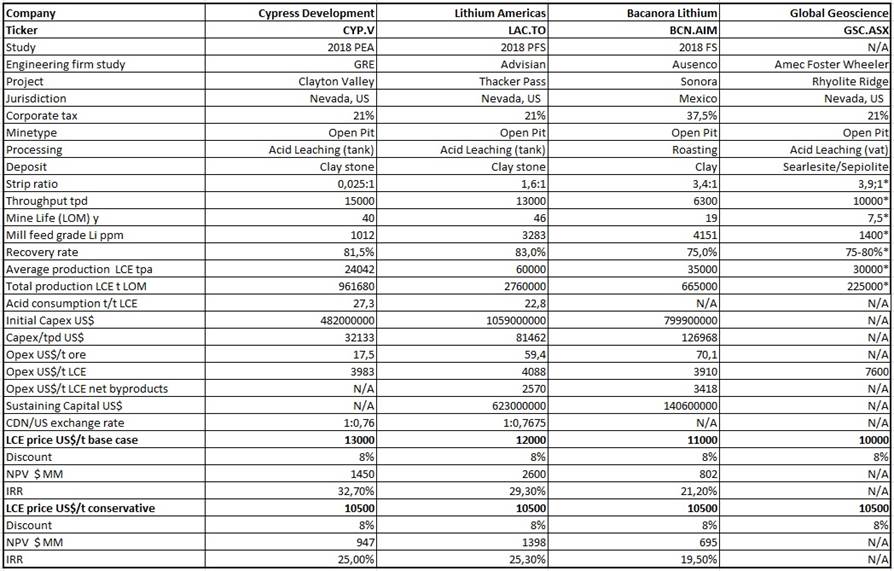

In order to discuss the PEA metrics a bit further, it is always useful to see those metrics lining up with the data of other peer projects. In this case there are three clay-hosted projects (although Rhyolite Ridge of Global Geoscience has low clay content), of which Bacanora's Sonora is hectorite clay, which means it can't be leached by acid at all, and needs very expensive roasting. Thacker Pass of Lithium Americas seems to have non hectorite bearing host rock (smectite and Illite clay) but sample material is called hectorite by metallurgical description, nevertheless it still can use acid leaching, and Rhyolite Ridge of Global Geoscience can use acid leaching as well. This last project is the only one without a completed economic study, but some work has been done already for a small (end target is a 30y LOM project) PFS study, and Australian companies can report these findings easier than Canadian ones, so some metrics are already available for the audience. On a side note: Global Geoscience has hired Amec Foster Wheeler for its upcoming PFS, and I consider Amec the single best engineering firm out there by a country mile, so in my view this study could become a future reference for likewise projects. Here we go:

*estimates by Global Geoscience

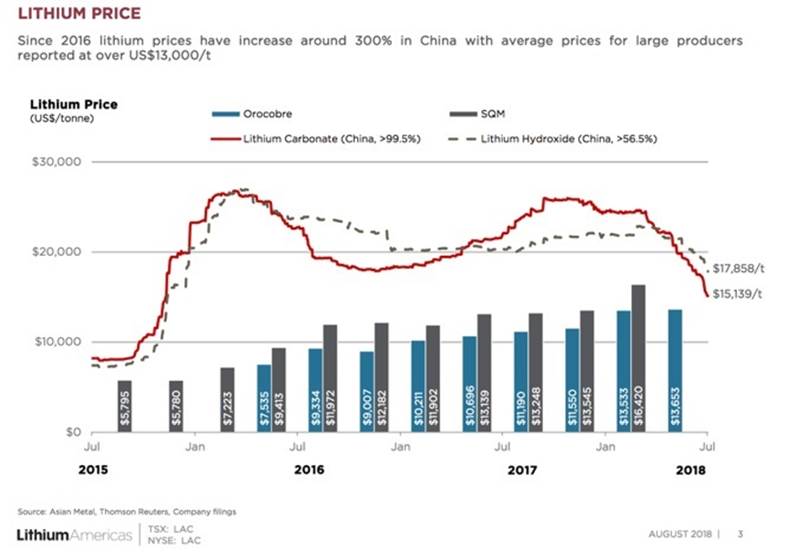

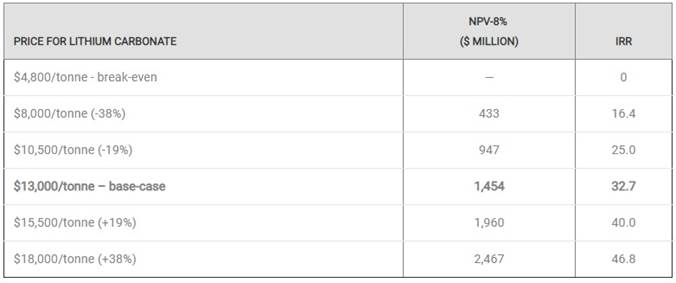

I have normalized the post-tax NPV and IRR for a lithium carbonate equivalent (LCE) price of $10,500/t, which I deem a reasonable and fairly conservative lithium product price. As we can see in the next chart, these prices have been much higher for the last two years or so, but the long-term contract prices are hovering around $13,000/t now, and as far as I am concerned this is the market where serious producers are doing business, and not the much smaller spot market, where prices are much more volatile:

Source: Presentation Lithium Americas

I can see this bottoming easily at $10,00011,000/t so $10,500/t seems like a realistic midpoint to me. The very bearish Morgan Stanley report was timed to perfection in itself, but I don't see, for example, SQM bringing online the projected 500kt LCE anytime soon, resulting in the dreaded oversupply from the end of 2019 onwards, as the company already has big issues expanding modestly as it is. It might be the case that the trade war between the U.S. and China is putting the brakes on the world economy, and in turn this could have an effect on electric vehicle (EV) demand, which means less demand for batteries and thus lithium, but as I don't have a good grasp on the machinations of the lithium spot market, I don't really have a good explanation on why lithium product prices dropped off so sharply over there the last six months or so. Maybe the negative commodity sentiment influenced small traders working with the most risky metals the most. Enough about the lithium price, let's continue with the PEA.

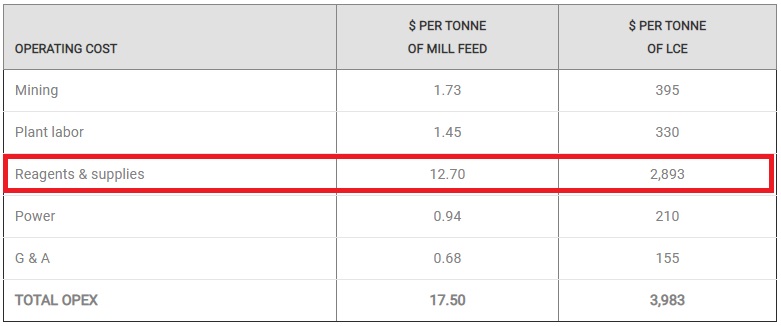

When we look at the peer comparison, it will be clear that Thacker Pass comes closest to Clayton Valley, as both projects use acid tank leaching, and the ore is claystone hosted, although the ore from Thacker Pass seems to have slightly hectorite characteristics as mentioned. To what extent isn't really clear, but what is clear is that opex and the capex/tpd ratio of Thacker Pass are significantly influenced by this, as both are much higher than the numbers for Clayton Valley. One of the reasons is that Thacker Pass needs about triple the amount of acid per tonne ore. Acid consumption is by far the biggest opex item for Cypress, as can be seen here:

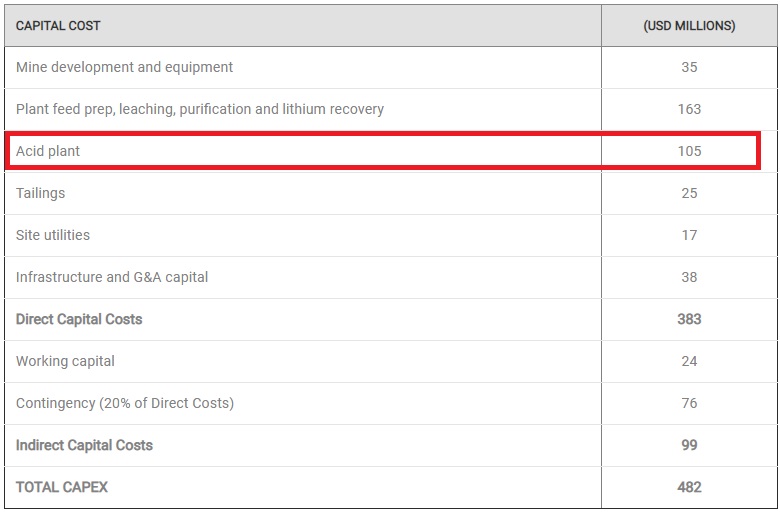

And the acid plant isn't cheap either:

When we look at the PFS of Thacker Pass, we see relatively equally high costs for utilities and reagents, and raw materials for the acid plant accounted for this: reagents are $18.14/t, raw materials for the acid plant $22.18/t, mining costs are $7/t, so this adds up pretty quickly, resulting in much higher opex compared to Clayton Valley. On a side note, a further item in the Thacker Pass PFS that I found to be interesting was the dewatering pump capacity with a peak of 340m3/hour, which is substantial. This might even influence the processing of mined claystone, as wet ore behaves differently.

The absence of hectorite ore at Clayton Valley is another reason that CEO Willoughby was excited to join Cypress. As he mentioned to me: "Early on, I saw leach tests from surface samples on Cypress' property which showed the lithium was soluble in water and dilute acid. This was a good indication the lithium wasn't present in hectorite." I asked him if he didn't think 10% contingency on opex was on the low side, and acid consumption could increase after further testing, and the answer was he even thinks they can go from 125kg acid/t ore to 100kg acid/t ore, which would shave off another estimated $1.52/t of opex, increasing after-tax IRR with an estimated 23% and the after-tax NPV8 with an estimated $4060 million.

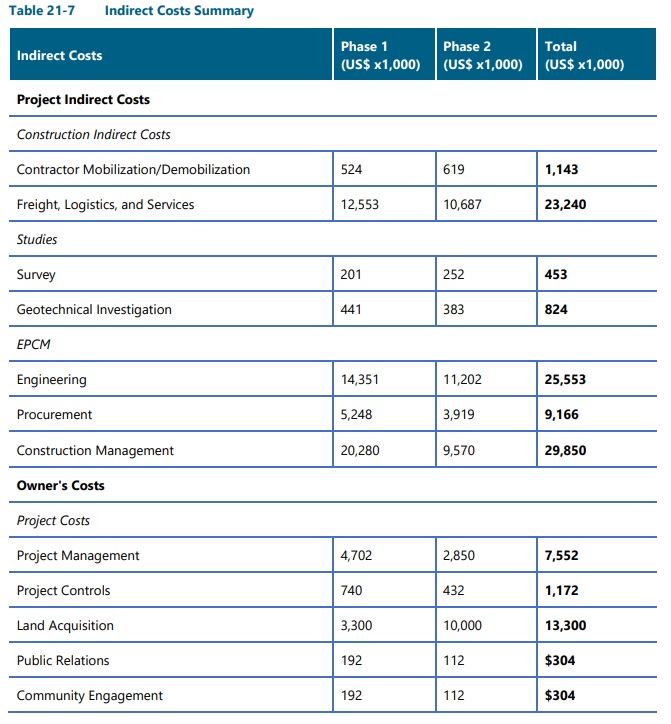

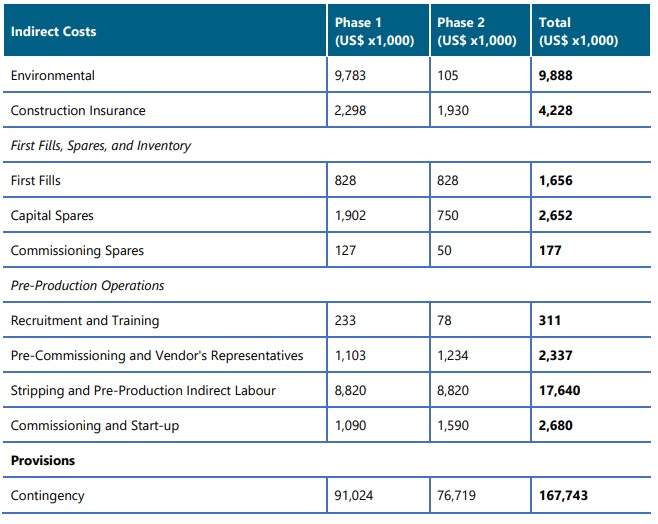

In case you wondered what the item Indirect Capital Costs stands for, as it isn't really the margin for error, have a look at the indirect costs of Thacker Pass:

As Thacker Pass has more substantial stripping costs because of a higher strip ratio, Cypress has almost no stripping/pre-stripping as mineralization frequently begins at surface at Clayton Valley.

As no blasting or drilling is required, mining is very simple. Engineering firm GRE evaluated four options for mine equipment and mill feed transportation, and selected an in-pit feeder-breaker with slurry pumping for the base case.

Feeder breaker; Source

The only major piece of mobile equipment is a front-end loader to feed the in-pit feeder-breaker:

Front end loader; Source

Such earth-moving monsters are capable of scooping up 40-70t in one move, meaning one front-end loader could feed the processing plant at nameplate capacity. Waste mining is minimal, amounting to a total of 6Mt over the 40 year mine life, resulting in the very low strip ratio of 0.025:1.

The plant design of Clayton Valley includes agitated tank leaching, and a multi-stage thermal-mechanical evaporation system for concentrating leach solution. Slurried feed is transported to the mill where lithium extraction is achieved through leaching at elevated temperatures with dilute sulfuric acid. The sulfuric acid concentration is targeted at 5%, with the addition of concentrated acid delivered from the on-site 2,000 tpd acid plant. Steam from this acid plant will be used for heating in the leaching and evaporation stages of processing.

The retention time of pregnant solution in the leach circuit is estimated at 4 to 6 hours with acid consumption estimated at 125 kg per tonne of feed as mentioned. This is an advantage compared to the cheaper vat leach method which Global Geoscience intends to use, which takes much more time (days) and would need a much bigger plant for the same production. Net recovery of lithium throughout processing is estimated at 81.5%. Tailings are aimed to be dry stacked, which will improve permitting procedures.

Process water for the operation will be obtained by recycling barren leach solution after treating in a reverse osmosis plant, and by introducing fresh make-up water, estimated at 345 m3/hour and delivered via pipeline from a well field located off-site. Reducing fresh water needs as much as possible is also an advantage in Nevada, which is known for its water rights that can be owned by private individuals, and complicated permitting around using these water rights.

3. Next steps

The biggest issue for Cypress Development is the viability of the recovery method. Preliminary test results continue to be positive, according to management, but the company has to prove its method at a commercial scale at one point. When discussing this, and the potential need for a pilot plant, with CEO Willoughby, he answered that a pilot plant wasn't needed to complete a PFS, this was only needed for a FS. The company is already looking at acquiring an existing pilot plant for this purpose. At the same time, he indicated that he wasn't convinced Cypress would have to get a PFS first before going towards a FS.

In his view the recently completed PEA was already at the level of a PFS with respect to cost estimates; only some more drilling and metallurgical work would be needed for a PFS. He would rather see that Cypress would spend money on a FS in that case. Such an advanced study would be scheduled for completion by next summer by his estimates. As the treasury contains just C$500k at the moment, the company needs to raise sufficient cash in order to complete permitting and the FS. This means it has enough money to do additional met work as recommended by GRE. Cypress intends to proceed with this recommendation as soon as possible, beginning with the collection of representative sample material.

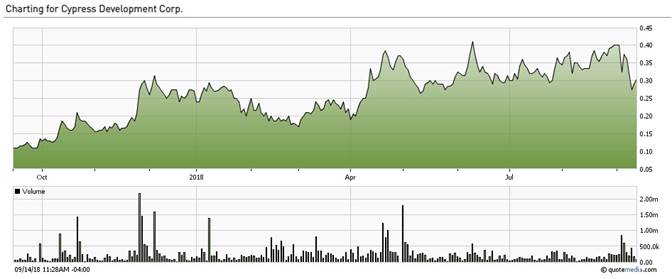

Share price 1 year time frame; source tmxmoney.com

The release of the PEA caused an unexpectedly fierce liquidity event, causing the share price to drop over 25% in a few days. Unexpected, as the PEA economics are robust, and the share price had held up strongly compared to almost all lithium competitors, who already shed 2560% in the last few months, after overall- and lithium sentiment turned negative. It is possible that investors expected or hoped for a lower capex, as it would be a hugely dilutive event to finance capex by itself, at such a tiny market cap of C$19.8 million. But in my view a US$482 million capex is below average for the usual lithium project, as these are big ventures, and at some point Nemaska and Orocobre were tiny too.

A PEA is still early stage as a development stage, so it usually gets discounted quite a bit until it advances further, depending on the various parameters and economics of the project. With Cypress, the recovery method needs proof so I can imagine the markets are still willing to assign an increased discount to this as long as the method hasn't been proven on a commercial scale. When Cypress manages to achieve success in this regard, the re-rating should be pretty significant, as the conservative NPV8 @US$10,500/t Li is about 62 times the current market cap.

4. Conclusion

The resource update for Clayton Valley ranks this project as the largest lithium clay deposit in the Americas, and the accompanying PEA indicated robust economics, holding up well at 20% lower lithium product prices. This comes in handy, as lithium prices are having a hard time these days. After this PEA, Cypress Development will probably start to appear on the radar of most major lithium producers/processors, and management already indicated it received interest from several of those parties to talk business. An important part of convincing others is proving up recovery at a commercial scale, and it is up to CEO Willoughby, who has a PhD in mining engineering and metallurgy, to lead this effort. Management is deciding now whether it wants to proceed with a PFS or a FS, which will determine the financing needs and timeline. I am curious what its next steps will be, as an interested shareholder.

Lithium bearing claystones at Glory project; Clayton Valley, Nevada

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at http://www.criticalinvestor.eu/, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor, and has a long position in this stock. Cypress Development is a sponsoring company. All facts are to be checked by the reader. For more information go to Cypress Development Corp. and read the company's profile and official documents on Sedar, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Read what other experts are saying about:

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: Cypress Development. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and graphics provided by the author.