Johnson Camp Mine

After having closed the second tranche of a non-brokered private placement, Excelsior Mining Corp. (MIN:TSX; EXMGF:OTCQB) raised an impressive total of US$30M. Strong features of this round were the absence of warrants, and the fact it was oversubscribed, as Excelsior initially was looking for US20.2M, and ended up with US$30M. Another strong achievement for me was the ability to do this raise before the very important UIC permit was granted, this is a strong vote of confidence for the permitting process, despite the small delay, more on this later. On the other hand, something not impressing me that much was the share price of C$1.00. When looking at the chart, it was obvious that certain parties liked to get in on the cheap, as soon as word got out that management was raising cash:

Share price MIN.TO, 1 year time period; source tmxmoney.com

The share price was walked down professionally from C$1.25 to C$1.00, against all positive copper and mining stock sentiment at the time, and at December 11, 2017 the financing was announced. As majority shareholder Greenstone took up about half the amount, they probably wouldn't have mind to say the least, but there was also a Nordic fund, arranged through UK/Norwegian advisors, which has a reputation of being very aggressive at these sort of things, so management was in no position to raise at higher levels unfortunately.

As a relatively small junior, this is what you can encounter when dealing with multibillion-dollar funds. On a side note, management attracted PI Financial and Clarksons Platou, which is Norway based, for coverage, because of the financing.

In total this meant an increase in share count of 38.635M shares, bringing the total at 206.2M shares outstanding. Greenstone now owns 48.89% of all outstanding shares of Excelsior Mining, and it is my feeling that it is vying for absolute majority in the near-term future as well. Which is not a bad thing as the firm has only one thing in mind, and that is an exit upon successful ramp-up towards commercial production. Excelsior management is eying first production before year-end, as quoted from the news release:

"The Offering was oversubscribed with strong support from major North American, UK and European based institutional investors alongside Greenstone, the Company's major shareholder," said President & CEO Stephen Twyerould. "With this financing, pre-construction activities at Gunnison will continue on pace as we prepare to seamlessly transition to well-field construction as planned, upon the receipt of the final permit and project finance, expected in the New Year. Backed by stakeholders that share our commitment for technical excellence and environmental stewardship, we remain on-track for copper production in 2018."

The cash position of Excelsior was estimated at US$4M before this round, so my take is that after subtracting all fees, a bit of working capital, etc., the company could have about US$33M at the moment. According to the company, the proceeds of the US$30M round will be used for the development, construction and maintenance of the Gunnison project, including the acquisition of long lead items, and for working capital requirements.

As management mentioned earlier that they were looking to raise US25M in working capital to use during the first years of staged construction, and capex is US46.9M, my guess is they have arranged part of capex and a good portion of their working capital for now. I can imagine seeing Greenstone going to 51-53% in another financing, raising about US$4-8M, which should be enough to come up with the balance of capex in a debt package. This will probably take place after the UIC permit is granted. This permit was anticipated in January or February the latest, but the Environmental Protection Agency (EPA) decided on January 23, 2018, that the public comment period would be extended in order to facilitate a public meeting. This meeting is scheduled for February 27, 2018. This extended comment period and public meeting came as a surprise as Excelsior management never indicated this as a possibility. Notwithstanding this, they see it as a good opportunity to inform all stakeholders:

Stephen Twyerould, the President and CEO, said, "We look forward to working with the EPA and all stakeholders to ensure our Gunnison Copper Project meets all regulatory requirements. The Public Meeting is a typical part of the permitting process and represents an opportunity for the communities around us to learn more about the Project prior to receipt of the final EPA Permit. Backed by industry-leading economics, and our commitment to environmental stewardship, the Gunnison Copper Project remains on-track to become the next new copper producer in the United States."

I was surprised as management indicated that there were no extensively motivated comments provided to EPA in the commenting period<. I do believe Excelsior has a very strong case for the UIC permit. Key here is that the Gunnison project is eligible for the requested Aquifer Exemption according to the EPA, and its reasoning is motivated by these two criteria as mentioned in the public notice EPA summary. As a summarized reminder from my last update:

1. 40 CFR § 146.4(a): It does not currently serve as a source of drinking water.

The document explains:

"These reviews demonstrate that the aquifers identified for exemption do not currently serve as a source of drinking water because there are no identified current drinking water supply wells, public or private that currently would draw water from the aquifer proposed for exemption, the formation/portions of formations are vertically and laterally contained (separated) from other USDWs, and no aquifers that serve as sources of drinking water are hydraulically connected to the aquifer."

And:

"The EPA evaluated the modeling approach and the site-specific geologic and hydrogeologic information and planned operational data that served as inputs, in connection with other information in the Class III UIC permit application (including geologic maps, logs, hydrologic information, etc.). Based on this, the EPA determined that the model accurately represents the extent of fluid movement and demonstrates that the aquifer to be exempted is not in contact with any formations that serve as a drinking water supply within one-half mile of the aquifer exemption boundary."

Excelsior Mining searched within a one-mile radius of the boundary for sources of drinking water, but fortunately for the company, there are no public water supply wells nearby.

2. 40 CFR § 146.4(b)(1): It cannot now and will not in the future serve as a source of drinking water because it is mineral, hydrocarbon, or geothermal energy producing, or can be demonstrated by a permit applicant as part of a permit application for a Class II or III operation to contain minerals or hydrocarbons that considering their quantity and location are expected to be commercially producible.

The Gunnison FS showed an after-tax IRR of 40% at a copper price of US$2.75/lb Cu, so this can be called commercially producible for sure, as this kind of IRR is world class for any mining project, let alone for a base metal project.

So, in order to summarize, there are no public water supply wells in the project area and buffer zone, and the copper in situ is expected to be economic, and these are the two most important subjects for EPA for deeming the Gunnison project eligible for the requested Aquifer Exemption. Nothing has changed here, and therefore the chances of Excelsior succeeding on receiving the UIC permit remain very high in my view.

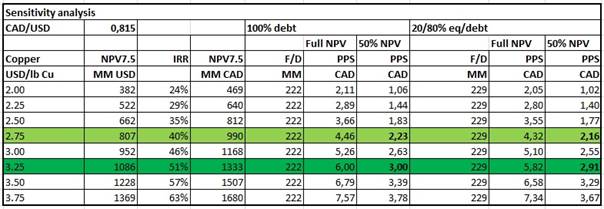

After the recent financing, the number of outstanding shares increased notably, so it was necessary to re-run the numbers on the sensitivity analysis. I included a scenario involving all debt for the remaining part of the US$47M capex, and a scenario based on 35%/65% equity debt which is industry standard. As at least about US$8M of the US$47M has been raised now in equity, the remaining equity/debt results into a 20%/80% scenario. The U.S. Dollar lost some value since my last update as well, so the CAD NPV went down a bit too. A thing I haven't considered yet is the changed corporate tax rate from 35% to 21%; this will be discussed in the next update.

Light green is the base case scenario copper price, dark green is spot copper. Full NPV can be used when commencing commercial production, but in this case production ramp-up is staged. The first stage is planned at 20% of maximum nameplate capacity, but since maximum capacity can be reached in four years according to management, it isn't realistic to use just 20% of NPV for valuation purposes when commercial production commences. 50% of NPV seems like a more reasonable discount at that stage, as further ramp-up is already baked in. Even if a 20% capacity and 20% of NPV would be used, there is still upside from current prices, so I continue to believe that Excelsior represents a pretty strong case.

As a large copper deficit is expected in a few years from now, it seems the ramping up of Gunnison could take place at exactly the right moment, as higher copper prices seem inevitable by then. A number of things have to go well before this of course, starting with the UIC permit, capex financing, construction and ramping up to commercial production. As this is the first greenfield copper ISR project of its kind, the recovery method has to be proven first on a commercial scale, which will happen at the first stage of 25M lbs Cu per annum, which I actually consider the pilot stage of Gunnison.

As various ISR projects on uranium and copper brownfield have been successful in the U.S., I like the odds, but commercial production will provide final proof here. Until then, Excelsior has a number of milestones coming up relatively soon, of which the possible granting of the UIC permit is by far the most important one. With the kind of financial backers that management has lined up, I don't worry about capex financing packages, and I have the impression that these financiers are simply waiting for the UIC permit. Interesting times ahead for Excelsior Mining.

Gunnison project location

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu, and follow me on Seekingalpha.com, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Excelsior Mining is a sponsoring company. All facts are to be checked by the reader. For more information go to http://www.excelsiormining.com/ and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and graphics provided by the author.