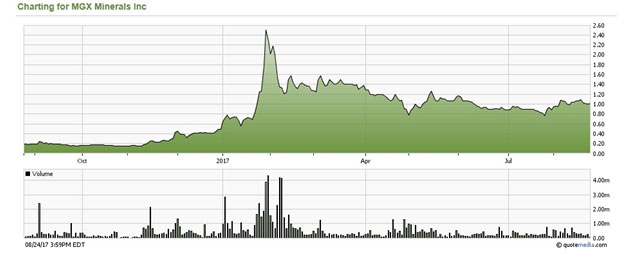

According to the significant number of news releases and different projects and activities going on at the moment, MGX Minerals Inc. (XMG:CSE; MGXMF:OTCBB) must be one of the busiest junior mining companies I know. A few of those activities definitely have the potential to be company makers on a vast scale, in my view. However, as most activities are still relatively early stage, not verified and sometimes seem to compete for strategy focus, it could be difficult at times to follow what's exactly going on for investors, let alone adequately value the company. As a consequence, the share price has been side-ranging for quite a while now, as can be seen here:

Share price; 1 year time frame

As the long awaited and delayed Ryder Scott report on the Paradox Basin recently came out, it looked like a good time to me to have CEO Jared Lazerson of MGX Minerals elaborate on the MGX story and recent developments. The right platform for this seemed a Q&A, where Lazerson could answer questions of yours truly, but also of investors, in this case being users of the company channel on CEO.CA. I do believe the end result will help clarify a lot of subjects for the interested investor.

TCI: Welcome, Jared. I'm looking forward to get to the core of the MGX story with you, as the story needs a lot of clarification for investors, in my view. So much is going on that it is easy to lose oversight. I have quite a list of questions, as you have seen, so we should be able to cover most angles here.

JL: Happy to do this interview with you. I'm super busy as you know so planning this wasn't easy, unfortunately. But I want investors to really understand what we are trying to achieve so here we are. It is a lot as you say, no doubt about that, and it might be time to be more selective but right now we feel we have everything pretty much under control.

TCI: Let's start with the subject I hardly know anything about, as I am mining focused, and this is the O&G/waste water component of the petrolithium story, with an increasing focus on oil and gas it seems per the Paradox advancements lately. Take me a bit through the waste water issue for O&G producers: they separate it from oil at the well head and store it or have it treated? Costs for this? Is this also a byproduct at shale oil? Could this technique prolong the life of wells for oil producers? I can imagine at a certain point the oil production of a well isn't economic anymore for those producers, could you say at what point this is, for example, the percentage oil/waste water? And what is the potential on a U.S. scale at the moment here? Any indication of ongoing waste water potential at current U.S. production rates?

JL: It happens both, depending on a lot of different parameters per individual project. A very large amount of waste water is produced in general, to the amount of 6 up to even 18 barrels of waste water per barrel of oil. Producers used to get rid of a lot through disposing wells, but this method is no longer considered environmentally sound. This also caused earthquakes in Oklahoma. The costs vary a lot between different states and projects for treating/transporting waste water. In Texas, for example, the costs are about $1.5/barrel, in Pennsylvania it's about $1213/barrel. Some 25% of all waste water can't be treated anyway and has to be stored somewhere. The total amount of waste water is huge, as tens of millions of barrels of waste water are produced every day. I estimate 510% of this could be eligible for our methods, roughly having operating costs of about $11.5/barrel of waste water.

TCI: Why is MGX acquiring O&G leases/rights; does it need this for access to the brines? Or is actual O&G production a target?

JL: O&G leases and drilling are done to create reserves; this will serve as an asset base. Marc Bruner sees chances with Paradox to create an integrated energy company here, combining O&G with the MGX technology, a true petrolithium concept. He wants to partner with a producer to develop the O&G assets. This is a long-term project as we are not starting a drilling program this year on this, as it needs more work. I like the concept of having assets and related services combined, so you aren't as dependent on commodity cycles.

TCI: What are the details of the agreement for the lease of Paradox; what are the expenses of petroleum production operation that MGX has to pay until it has completed drilling of at least one well and made required payments? This is for a 75% interest in what exactly? What will happen afterwards? Why did the vendor sell the Paradox assets?

JL: MGX gets 75% of the O&G/mineral interests, when paying $2 million in three years, and drilling two horizontal wells or three vertical wells in five years. The carrying costs are $0.25 million per annum. After this the interest is no longer carried, and MGX has to pay 75% of drilling costs. The property became available when a major oil company dropped the property as a result of internal restructuring and low oil prices.

TCI: If MGX is to go into O&G, what about NPV10 and 2P metrics? Reports?

JL: We are not at that stage yet for Paradox; you can compare the current resources a bit to Inferred in mining. The total unrisked contained resource is over 6 billion barrels of oil equivalent (BOE) and total recoverable resource is around 500 million barrels, which is in the latest Ryder Scott resource report. Usually you have one or two pay zones, but Paradox has 20+, which makes this a special asset. It will take some successful drilling to bring this to reserves; first we are beginning with a 3D seismic survey and drill permits. Drilling will start about a year from now.

TCI: Do you have plans for the treated clean water coming out of the waste water treatment process?

JL: Oil companies can reuse this water for cost savings on water. Industrial water is about one third of the total water market in the U.S., and O&G is a big part of this, so it is a significant market. It could be part of water handling contracts we are involved with, we could also sell it ourselves. This is a flexible concept, as every oil producer has different strategies for its water handling. I feel MGX should focus on processing instead of going into the water trading business; we are already branching out a lot as it is. Fact is there are so many good options in this field opening up, and our goal should be to select the most profitable and closest to our core strengths.

TCI: The contracts are with unidentified clients and no amounts; why is this? Usually these are made public by the smaller party in order to gain more credibility with investors.

JL: This usually is the case in mining, but in O&G they don't want to disclose any names or amounts. Only the major deals are announced with all information disclosed; we are small business to them. We also don't have hard revenue contracts at the moment, just testing and demonstration contracts. Now that the pilot plant is running, we are processing water every day. The test data will be available shortly and we will start issuing proposals and move to contracts. On the offtake side, demand for lithium remains very strong, and we have a number of very good options and partnerships ready to move ahead with producing lithium chloride concentrate.

TCI: What is the importance of the Ryder Scott report?

JL: It shows a resource with a lot of potential, lots of pay zones, which is rare, at the very least 25 million derisked barrels of oil. We are working with a big engineering company partner to assist with drilling. The resources will be upgraded to 2P reserves along the way; the goal is to produce oil and brine right awayas soon as we hit. This is essentially a hybrid petrolithium play, for oil and lithium at the same time. It will take time to develop this asset; we will do a 3D seismic in Q2 2018, and start drilling our first oil well in Q3, 2018.

TCI: With regards to the Paradox Basin, does MGX intend to extract the oil and natural gas resources as well as the brine/lithium? Or will it partner with a gas/oil company to extract those resources?

JL: We are planning to extract oil, gas and lithium, and possibly other minerals from brine. MGX will be the operator, and will probably JV as drilling will amount to about $20 million.

TCI: Does MGX actually own the rights to the oil and gas, or only to the brine water and contents?

JL: MGX owns the rights to oil, gas, brine and mineral contents.

TCI: Could you give us a status update on timelines for commercial contracts?

JL: We are now into demonstration contracts with interested parties. Bulk samples are going on now, being processed by the 120-bpd pilot plant. Lab assays are expected in two weeks from now, scientific reports in six weeks. These reports will be used in contracts with our partners and interested parties. So we are at the turning point now and will be issuing proposals and contracts within the month. Keep in mind that MGX was generally approached by these parties, as MGX has first-mover technology, so there is definitely a lot of serious interest from the largest oil and lithium companies in the world.

TCI: What are the water treatment opportunities?

JL: Water and energy are the the biggest businesses in the world, so when we are talking about water use and disposal in the energy business the opportunities are massive but it's so large it needs to be segmented. Again, we are really targeting the biggest and most profitable opportunities so the first contracts will be in oil sands and high disposal cost areas in the U.S. Uneven environmental regulation has really pushed disposal prices up in some areas, as well as demand for reuse and repurpose as a result of limited availability of fresh water. Obviously global opportunities for producing fresh water from oilfield brine are significant.

TCI: Has MGX an idea of any hard indicators on all its projects, like actual cost/CF indications, production units, capex for them and how to raise the cash for it, timelines on units production itself (and exactly which metric units, just for waste water or also for lithium, as it seems to vary with every news release on this topic)?

JL: I don't have official numbers yet, but a solid ballpark number (coming from engineers working on the method and pilot plants) for the costs to treat waste water per barrel would be about $1 on average. A lot of these costs depend on the amount of oil in the waste water, and the amount of minerals. When there is a lot of minerals present, this will need more reagents to extract them, which is more expensive. I estimate the capex for our commercial unit of 7,000 bpd starting at about $3 million, of which the most part is used for oil and heavy metal separation. If oil wouldn't be present, capex could be as low as $0.5 million to give an indication of other applications, such as extraction of lithium from traditional lake brines. The amount of reagents can differ considerably with each project.

Today a 120-bpd pilot plant is producing lithium concentrate at the moment, a 750-bpd plant will be assembled in October 2017, and a 7,000-bpd commercial plant will be completed by December 2017. After this MGX hopes that mass production can begin, with the right partners. The company works with long-term financial partners, like lithium producers or O&G service companies, to borrow the money needed for capex, or have advance payments against off-takes made. Besides this, a significant Canadian government grant been applied for through our engineering partner. This grant is to pay for equipment for an oil sands water handling contract, where this would pay for about 2/3 of the necessary equipment of a 7,000-bpd plant and MGX would pay the balance. That project is a nice consortium of government, an oil sands producer, our engineering partner and a big systems partner to handle control systems, remote monitoring and AI.

TCI: Are there plans to follow up with the government's offer of additional funding for the water treatment process? Purlucid received $3 million, and the documentation said they could get another $7 million.

JL: Yes, see the question before, a decision can be expected soon.

TCI: How is MGX planning to proof those hard indicators to investors?

JL: We are going to build and demonstrate the commercial scale plants, and when revenues and cash flow start coming in, we can verify our in-house engineering numbers with reality. MGX is scheduling to have the first commercial unit of 7,000 bpd ramped up and commercially operational at the end of Q1, 2018. At the moment, we have a 70% recovery for lithium coming from 70mg/L brine/waste water, and we can concentrate this up to 1600mg/L, basically at $11.5/barrel costs. Magnesium has a recovery rate of 99%.

TCI: Who will be operating these plants? One of your pillars is O&G, so please could you explain MGX's involvement in Oil and Gas related to these plants?

JL: We will have our own operators. We will be training personnel from local producers; it is a relatively simple system. This could also be personnel from an O&G service company; there are a handful of global service companies that make a good fit as an alternative to MGX or the producer. It will be a project by project case, as each producer will have different plans, each project will have different characteristics for products and profitability. We think the hybrid way (O&G and lithium) will be the way to go.

TCI: How important could the waste water concept be for revenues? Cost to revenue could be stellar for this.

JL: Our primary business is lithium at the moment; waste water treatment comes in second. As discussed, the gross margins can vary a lot, but I believe there is a large market waiting for us that currently pays on average $37/b of waste water. With our opex of about $11.5/b, we can make a lot of producers happy on an average price of, for example, $2.53/b. I can't go too deep into this for competitive reasons, and this differs per project as you understand. It's a very uneven market; even producers right next door to each other might have totally different water handling costs due to very basic factors, for example, trucking versus onsite disposal.

TCI: Last reporting on the lithium extraction was the formation of a gel, still containing 28% of water, which must be surely uneconomic to process further. What is the current status on this process?

JL: Gelling occurs as the minerals near crystallization right at that maximum edge before physical particulate forms. The original system evaporated much of the water initially so gelling started to occur, which is usually easily remedied by just not evaporating quite as much water. We now have a new system in place. The gelling happened only at the former evaporation system, and we have just patented a nano filtration system, so it's not an issue. We do like the evaporator system when a project needs a lot of distilled water or very clean water for surface or aqua release, as the original system does produce a very high quality byproduct; the nanofiltration system is superior due to low operating and in particular CAPEX cost. The nano filtration system is based on a membrane protection system, which is basically a coating over the filters. This coating is recoated after 12 hours, so the expensive filters themselves don't need replacement.

TCI: How is it possible to build a 1,000 liter per day (lpd) AND a 100,000 lpd pilot unit at the same time, before even testing the 1,000lpd unit? The big issue with upscaling from bench to commercial is the technical equipment, according to an expert I know, and is not easy in general.

JL: The 1,000-liter system has been upgraded to 24,000 and is being run everyday with different types of water from all our projects. The 120,000 liters (750 bpd) is mostly done and will be deployed, so we will have some additional data before going to 7,000 bpd, but the engineers we have working on this are very experienced with water treatment systems, and this type of system happens to be easily scalable; the technical equipment isn't an issue in this case. Proof is in the pudding of course, we will know much more in Q1 2018 when the first big unit comes online.

TCI: Also per this expert: he thinks the concept should be just nanofiltration, not nanoflotation as also mentioned elsewhere in news releases. He also thinks the issue is the recycling of the used nanomaterials, and the blocking of filters. He says lithium is very tricky as it is a very small atom, which creates difficulties. Any comments on this?

JL: It is both actually. We need nanoflotation for pollutants such as oil and the heavy metals; it is part of the plant. Besides this, the pre-treatment unit for oil and nanoflotation are the most expensive components of the entire plant. The trick with having a saleable lithium product is impurities so we take everything else out first and then concentrate the lithium. This is actually where many technologies have failed by trying to isolate the lithium, which is difficult; we just remove everything else and are left with lithium. It seems counter intuitive on the cost side but it's not all that expensive to begin with because it's low energy and the product is reasonable quality.

TCI: As I laid out in my analysis on the company, the actual production of lithium will probably be only a small part of revenues, as byproducts sodium chloride and calcium chloride seem to be the big economic drivers behind the process. But I don't believe the markets are waiting for huge quantities of those two byproducts, and it would also increase capex and opex. What about this?

JL: A lot has changed since your analysis and assumptions. We are targeting an average lithium grade of about 100140mg/L, and with the current, much-improved method and concentration rates this will be the dominant source for revenues. Calcium chloride and sodium chloride are both big markets, but the key is the proximity of buyers. A rough estimate for those byproducts to be economic would be a transportation radius of about 300500 miles (480800km), so eligible projects likely need to fall into this radius and have a sufficient lithium grade. Both byproducts would have to be removed as an essential part of the process as both are contaminants of the lithium, so no additional capex or opex should be required.

TCI: I see one article claiming your process can produce lithium carbonate in a day, but elsewhere some kind of concentrate is produced in a day and then shipped to third parties refining the concentrate into LC. What is the actual status?

JL: In a day we can produce a low-grade lithium chloride concentrate of 2030%. This is shipped to an upgrader to convert it into lithium carbonate, which we then sell to customers. The total process will take about two to three weeks, which is still 12-17 months faster compared to conventional lithium brine operations that need to raise capex for the processing plant as well; we just pay the upgraders a fee.

TCI: Giant companies and specialists like POSCO or Tenova Bateman are developing comparable fast recovery methods for many years (Tenova also for oil brines, I believe), but without proof on a commercial scale so far. What is the difference between those giants with large budgets and the best chemists, and MGX and Purlucid, seemingly cracking the code on low budgets in a very short time frame on the other side?

JL: I know it could sound unrealistic at some point, but I also think there is a fairly simple explanation for all this. Our lithium extraction technology has been developed as part of a waste water technology, which was a totally different way of looking at things and easier to advance since this patented technology had been developed with high volume, low opex and capex in mind. Tenova Bateman and POSCO are looking at brine recovery from a mining perspective, and therefore had a much more difficult approach. As a consequence, MGX removes everything from brine, whereas, for example, Tenova targets just the lithium. It has a selective method, which is apparently much more difficult to develop successfully, as it has been working on this for many years now. On top of this, MGX and Purlucid have very short lines and a small organization, which enables them to kill unsuccessful methods or approaches much faster.

TCI: Could some adjustments make the MGX/Purlucid method eligible for a much faster version of conventional brine recovery, now done by evaporation ponds? Aka the holy grail Tenova Bateman and POSCO are looking for?

JL: Yes, MGX and Purlucid are looking into this right now, and I believe this could be the next pillar of our story. The plan is to develop an economic recovery method for this, partner with lithium producers, and also to acquire assets. Those assets will likely have to be North American, and should be clean brine without oil, which would lower the capex and opex drastically.

TCI: I see concentration efforts of 67 ppm Li to 1600 ppm Li, making it rival LatAm grades, but no mentioning of costs is provided. What about objectifying of these metrics?

JL: Our engineers indicated the already mentioned ballpark number of $11.5/b of waste water/brine, and very clean brine without oil or heavy metals or significant other impurities could cost less than $0.50/b to treat. The concentration stage is part of the recovery process, and wouldn't add to opex. The recovery method works best at lithium grades of over 100 mg/L we found, so not all projects are eligible. Right now we are at breakeven point for lithium revenues vs, opex, and water handling and byproducts add value. We like to focus more on lithium production so we continue to optimize this at the moment.

TCI: I also see the resulting concentrate is a 1600 ppm Li lithium chloride concentrate. The lithium chloride market is much more difficult compared to lithium carbonate, and needs another step of processing.

JL: The lithium chloride concentrate can easily be upgraded for a modest fee to lithium carbonate, which we can sell to numerous interested parties as shortages are ongoing and not likely to be solved anytime soon by new supply.

TCI: Why is Purlucid still so small with a hardly developed website, company staff, revenues, etc., if it has developed a successful method, garnering clients like Shell? I don't see commercial scale follow up contracts with those giants yet, instead Purlucid gets acquired by a small player like MGX?

"MGX partnered with and invested in Canada's Purlucid Treatment Solutions to create and commercialize an oil well lithium brine separation process. Per its investment agreement with Purlucid, MGX has rights to acquire 100% ownership for $15 million in total investment. Purlucid is already established as an industry leader in oil well wastewater treatment, with a client list including the likes of Imperial Oil (IMO:CA)(IMO), SunCor Energy (SU)(SU:CA) and Royal Dutch Shell (RDS-A)."

JL: Purlucid always has been a government funded research initiative, consisting of a team of scientists, and not a commercial company. They weren't into marketing in any shape or form, or aggressively playing the markets. Its treatment method was top notch, but it was in no hurry to follow up on those demonstration contracts with big names. Not much happened the last 1.5 year or so, after the demonstration contracts were done. This is exactly where MGX comes in.

TCI: It looks there are two phases in the Purlucid concept:

"The strategy involves using the expertise and technology of Purlucid to begin the separation process by removing particulates and other dissolved materials, such as emulsified oil, colloids and heavy metals. The core technology was a finalist for The Katerva Award, which recognizes disruptive sustainable innovations from around the world. Phase 2 involves a proprietary process to remove the valuable materials, namely the lithium, from the relatively pure feed material."

Has this core technology being tested on a commercial scale yet?

JL: Yes, the demonstration tests of this technology by Purlucid were at a commercial scale and the core technology has been deployed at three refineries in China to date.

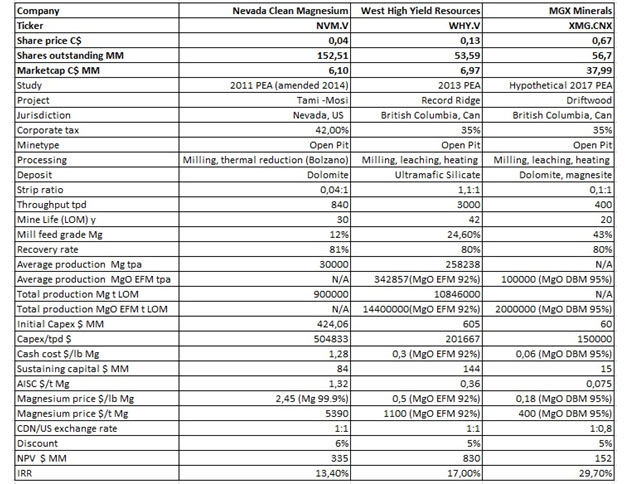

TCI: As you know, I like the Driftwood Creek project a lot, as my estimates in my first article could indicate a significant NPV for the upcoming preliminary economic assessment (PEA), providing a tangible underpinning for most of its current market cap. To illustrate this, I'm showing the table again that was published in my first article on MGX (share price, etc., is outdated as a consequence), lining out my estimates against the direct magnesium-based peers:

What is the status of this upcoming Driftwood PEA, and the scheduled timeline on this? How is the commissioning of the test mill at Driftwood going? Last we heard it was taking longer than expected. Is it up and running now? If not, what is the timeline on this?

JL: The PEA is pretty much done, the test mill is up and running and delivering results for the engineers, the process design has been reengineered, although not with big changes from the original plan. This took three additional months, which I didn't like a lot as it is a cornerstone asset, but it looks like we are finally coming to a close now. My expectation is a release within two months from now. The problem with the test mill was the moving from the Yukon to its location, all of a sudden, we were confronted with considerable contract price increases for transportation.

TCI: Other companies have tried to mine magnesium in British Columbia and struggled with an effective/economical process. What progress have they made with the pilot plant towards an effective process, how much longer can they keep this plant that they don't own but have invested so much time and money into, and when can we expect actual numbers and/or an actual plan for Driftwood? Follow-up to that...is Driftwood even something the company plans to pursue, or with the hype around petrolithium are they only looking to firm up the value and sell it?

JL: I don't know anything about struggling magnesium mines; we have a fairly big one operating for many years not too far away from us, I don't know about any problems or issues with their process. The test mill agreement officially ends about now, but we know the owners very well, we are on a very friendly basis, and we have arranged to lease the mill for another six months for some shares, nothing significant. Total investment in this test mill isn't significant either, not sure where the "so much" comment comes from. The PEA comes out in two months as discussed earlier. Driftwood is a cornerstone asset, and will not be sold. As the PEA looks like it will be thorough, and the process is relatively simple; we are looking into doing a PFS or FS to give the asset more value. Besides this, we are looking into partnering with big producers, for possibly staged capex funding, which is possible here.

Driftwood Creek: test mill

TCI: Could you tell me about the status of uplisting to the Venture, possibly to the NASDAQ and the timeline on this?

JL: We definitely worked on the uplisting to the Venture since Q1 2017, but we realized it would limit our dealmaking capacities. We know of a lot of companies that are frustrated with limitations on deals largely due to capital requirements. So the exchange often requires companies to have the development capital available as part of a listing requirement or major asset plan. The reality is you cut the deal then finance it, not the other way around. We also do a lot of property deals and on the Venture every small detail would be vetted with a lot of scrutiny, in particular on valuation, so you basically have the exchange telling us what the deal is worth when the reality is that months of negotiations have often occurred with a high level of expertise and to have all that time and money thrown away because the exchange has a different opinion is just not an acceptable risk to conducting this type of business ultimately having deals squashed and we have seen that happen. We have many deals going on at the moment, so to have an exchange interfere with this at this building stage of the company is not an option for us. However, we do recognize the increase in credibility, coverage and trading, leading to much more interest of institutionals in Canada, so it has become quite a dilemma. This also makes me hesitant for giving a timeline for this.

Uplisting to the NASDAQ would have priority for us as this market is much larger, and we already have a lot of U.S. coverage at the moment. Right now, we are busy with step one, which is uplisting from pink sheets to OTCQB; the filing has been done, and this will be finalized in two weeks. I will come up with a plan for further uplistings in Q4 2017.

TCI: Why doesn't MGX have a presentation online? Is there again a timeline on this?

JL: Our lawyers asked us to remove it while we went through the prospectus process with regulators. That was finalized yesterday and we will have a new presentation online shortly.

TCI: Something else. Why continuing with so many news releases with subjects that can easily be concentrated, let's say three to one? It hurts credibility in my view.

JL: Most if this is regulatory; if it's a material event then it has to be disclosed straight away. Other news such as updates are done as a courtesy to our shareholder and for equal dissemination of information. Most of our shareholders want more news not less so it's a balance reflecting a diverse shareholder base we haveinstitutions on one side and retail investors on the otherso it is a good point but there are a lot of different perspectives but most of it is regulatory.

TCI: Could you provide us with some background information about the latest financings?

JL: Sure. The first one was by Mackie, a short form of $5 million. It was for retail, and it was initiated by our existing banking relationship. It took longer than expected because of some internal changes at Mackie but it panned out beautifully in the end. The second one was initiated by Marquest, a flow through fund that is institutional, and also had an existing relationship with us as it participated in other rounds. Marquest called us, and pitched MGX to Sprott, which took about 50% of the oversubscribed $3.3 million round. So we are cashed up well into 2018 now.

TCI: Has MGX looked into partnering with geothermal power plants in California (Salton Sea) for water treatment and lithium extraction? A company called Simbol Materials was into this four or five years ago but failed, reportedly for financial reasons.

JL: We are not active on this; we want to stay away from California in general, because of environmental/permitting risks. Lots of companies have looked into Salton Sea, and nothing came out of it yet, so there must be a good reason. At some time I will look at the lithium grades and see if we could do something with it, but not anytime soon.

TCI: What are your thoughts on all the halts for corrections to company releases? What steps are you taking to avoid this going forward?

JL: It didn't look good, although I didn't understand all of it. To avoid all this misunderstanding, we are now filing with the regulators first, in order to reduce our exposure and eliminate anything that might be viewed as promotional. The main strategy is staying in touch with the regulators from a to z. They have their job and we have ours, but it's not exclusive and it doesn't have to be conflictual or dramatic as it was in the past. Canadian junior mining companies are some of the most tightly regulated in the world due to NI 43-101; there is nothing comparable and most people are unaware of how this plays out in the market.

TCI: Can investors expect to see any results made public from the pilot lithium plant that they said would be processing bulk samples throughout July, or do investors have to wait for results from the larger plant in October-November timeframe? Will either one of those plants allow the company to take credit for an economically viable process that would lead to some resource estimates? Do they ever plan on publishing resource estimates that might help with financing faster growth, or are they sticking to one plant at a time with revenue from each plant financing the next?

JL: I know this has been a hot topic for you and others, and rightly so, but the reality is that we can't disclose too much of our costs, as this would ruin our competitive advantage with clients. This is services, not mining with fixed worldwide metal prices, for example. When the business contracts are signed, revenues will come, and economics can be derived from here. We will provide resource estimates when we have proven up economics. We are no longer planning to finance plants on internal cash flow as it would take way too long; our preferred model is working with (JV-) partners on this.

TCI: The patents on the lithium recovery method are still pending. Is there a timeline on this?

JL: There are two patents pending: the one on the evaporation crystallizer method is expected to be approved in November this year, and the other one on the filtration method will take about a year. We do have a U.S. provisional patent though that protects us. There are no plans to commercialize the evaporation crystallizer method soon as it is only useful for producing distilled water.

TCI: What are your thoughts about licensing your technology to other lithium companies?

JL: We are certainly looking into it, as I explained earlier we are actually reviewing clean brine projects to acquire ourselves as I see a lot of potential here to produce lithium very cheaply on very low capex. Again, this is also something that could materialize through JVs.

TCI: What are the results of sending the resulting gel out to be purified? What was the concentration of lithium in the gel, and how economical was it to get the last bit of water out of it?

JL: The gelling method was the former and discarded method, this is no longer relevant.

TCI: MGX does not report financials, but could they tell us how much income they are getting from their stake in Purlucid, given that it already had contracts with oil producers (CNRL)?

JL: Purlucid is not generating any significant revenues today; it only works with demonstration contracts, as it has with CNRL. A business contract is in the works, and part of it is based on a substantial government grant, which if successful will support about 1/3 of the oil sands treatment project that is the subject of this contract.

TCI: On politics: given that his company's technology has a potentially huge positive environmental impact, does Jared see a benefit in the recent increased role the Green party has in the British Columbia government?

JL: MGX doesn't really associate with politics. We are also involved in possible oil production and mineral extraction, so we aren't exclusively a green company that could directly benefit from this development.

TCI: What do you think of the other companies coming online with plans to extract lithium from well water?

JL: There are a few juniors trying to follow our storyline at the moment, but we haven't seen any serious competition so far as recovery methods go. I know of an Australian company with a promising technology, but it has a method that involves a $700 million capex processing plant, much more expensive compared to traditional plants.

TCI: Do you see any application for the Purlucid tech in the field of desalinization? Given that one of the main issues of desalization is the power consumed by the process, would it be possible to leverage the tech to create fresh water from ocean water? Is this on its future roadmap?

JL: MGX is looking into desalinization as part of heavier polluted water/brine; we will likely not be more cost effective than the competition with regard to ocean water. Therefore treating ocean water is not part of our plans, but we get asked this question a lot and are looking at this closer.

TCI: When will the quarterly report be released and what are the capex plans for the next few pilot plants?

JL: We are working on having the Q4 report unaudited out at the end of September, and the July 31 year-end report out in November.

TCI: There are some concerns about the Purlucid deal, as investors are voicing a lack of transparency on the staged ownership, and the Purlucid owners possibly cashing in on the back of MGX investors?

JL: If I were to take sides, I would say it the other way, that MGX is cashing in on Purlucid's core technology but the reality is that MGX has brought Purlucid into no real extraction and Purlucid has brought MGX into nanofiltration. MGX is about as transparent a company as I know, so I am not sure where this idea comes from. Purlucid is a combination of IP and human assets, so making sure those human assets don't disappear is important. We have a 35% interest and will move this towards a 65% ownership over the next year for about $3 million additional after investing about $1.2 million in Purlucid and directly in technology development. At that point we will have a majority and will be able to control things, but we already own the mineral extraction patent license and UP, so its really the working relationship that's most. We are not taking Purlucid owners out or running Purlucid; these guys left big corporations with a purpose and MGX supports that type of independent thinking as they want to stay involved. They also understand the filtration technology better than anyone. If everything works out as planned and they succeed, I don't mind them scoring big, as in that case we will all score big, but it's best to think of this as a replacement for a third party engineering company that also has a lot of technology and IP in the water handling space. In that light it's a smart deal.

TCI: How about the compensation of Bruner? Does he get 17% of the company in free shares, or can he buy those shares for fixed prices? How does this exactly work?

JL: It's not that high; by the time all is said and done it will be about 10%. We have an agreement with him where he gets paid in shares for his work. If he doesn't work he doesn't get paid. He was pretty busy in the beginning at other projects outside MGX, in Australia, etc., so he only got 0.5 million shares up to now. At the moment, he is much more focused on MGX, despite his other ongoing involvements. He has a two-year agreement where he could get a maximum of 9 million newly issued shares. He has to bring in big deals, help with other deals, financings, and he will get paid based on, for example, the acquisition value of those deals and his input. I'm happy at the moment with how things are progressing under Marc; his influence and network is starting to pay off and he is involved in talks with important parties that could prove to be game-changers for the company. It is always important to recognize traditional energy industry players and integrate with those groups; it makes moving ahead quickly a lot easier. We like the hybrid model of new energy/traditional energy and Marc knows the traditional energy business very well, particularly the unconventional side, which is where we fit in.

TCI: How about the "COCChance of Commerciality" and why is a figure of 9.7 % in the Cane Creek clastic considered "good" at unconventional plays? The report is not really about the risk or chance of commerciality but rather a resource/reserve quantification estimate?

JL: 9.7% is fairly good to be honest, as it is the chance of discovery times the chance of production. This is just how you describe these early-stage resources in O&G. It is a way of quantifying, try to derisk it and to put a valuation on it. Which isn't easy by any means though, but Ryder Scott is a very respected firm and conservative.

TCI: Investors are wondering if you are able to provide more detail in news releases that are easier to understand for non-technical people?

JL: We are not more technical in our news releases than other O&G or mining companies, but if there are any questions just call or email the company and I am happy to elaborate further. When it comes to valuation though on this large project, it's best to get third party opinion from a petroleum engineer; this is not a complicated interpretation and my guess is any review would be a positive towards an investment decision or asset evaluation of MGX.

TCI: Could you explain why this O&G resource is a good resource, and how it will help build the company? It's a different operation.

JL: The Ryder Scott report indicates this could be a very large resource; it is still early stage but could prove to be the ultimate petrolithium asset for us, if we succeed in drilling so we can produce oil, gas and lithium right away.

TCI: If Paradox is a special asset with 6 billion barrels, etc., how come this hasn't been picked up before by a producer a long time ago? Could profitability and infrastructure be an issue?

JL: No, there are no issues with Paradox. We bought from the lease holder because a major producer didn't want to pursue further exploration on this asset at that time due to low oil and corporate restructuring. This where Marc Bruner is most effective in oil and gas dealmaking. The project is now unitized as well, which really increases value. We had to act quickly as it is a good asset, it came up, Bruner jumped on it and did the deal, so it was only on the market for six weeks or so. This was one of the instances where Bruner was instrumental for MGX.

TCI: How do you see AMP (American Potash Corp) playing a major role with the strategic partnership with MGX Minerals?

JL: We have many projects and joint ventures. American Potash represents a lithium brine opportunity in Utah that opens up the North Paradox Basin. It's essentially drill ready for Li and K so we are working with AMP on a drill plan. There has been a lot of work done on this project so that's a big advantage. We still prefer the Lisbon Valley area of Paradox, as the Lisbon Valley oilfield is a 50 million barrel producer but North Paradox has the potash mine. So it is our number two choice but we really view Utah and Paradox as being the top petrolithium prospect in North America, which really means combined minerals and oil.

TCI: How about the plans for leasing out your equipment/tech to other companies? Specifically, the need to have certified/qualified staff on site to run/maintain the machine. How many people will be needed to operate one? How long will it take to train the staff so that they are able to handle any issues that could arise on a day to day basis?

JL: The systems require one full-time operator and with remote monitoring this may be reduced, but for now one full-time operator. In terms of sales and licensing agreements, we are really focused on per barrel charge for water processing and a credit or royalty against minerals extracted. Obviously on our own projects we keep pretty much everything: oil, gas and minerals. We have a number of connections in the oil and gas services business that may provide a large-scale operational and deployment framework for North America.

TCI: We are coming to an end of this pretty long interview, I think we covered all important subjects here. Could you tell me more about upcoming catalysts?

JL: Sure. It's all about deployment, lithium and water handling contracts. For example, on the water handling side, one of the most important catalysts will be Purlucid signing the first water handling contract as discussed earlier, combined with the reception of the government grant. Furthermore, we are working on agreements with large parties to buy our lithium, and with other major parties about working together on partnerships for drilling wells, waste water services, production of minerals. We are also looking into applying the technology with clean brine assets. The completion of the 750-bpd lithium pilot plant is close and deployment is planned for October 2017. The first 7,000-bpd is scheduled to be ready December 2017. We have a full project pipeline, so sales, joint ventures and development of our direct assets will be where the big action comes from over the next few months. I believe the company will look very different come December and how things play out as we start deploying systems will be exciting as well. I think it is inevitable that we become a takeover target due to our massive lithium land position and advanced technology.

TCI: Thank you for your time, Jared. This certainly provided a lot of additional insight. I am looking forward to further developments, which could turn the promising, very dynamic and multi-faceted petrolithium story of MGX into tangible, focused, easy to value assets and provide clear metrics for investors on other assets. The next six months will be important to the company in this regard in my view, and if it all works out fine it will be an important step towards materializing the eventual vast potential of MGX Minerals.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website www.criticalinvestor.eu, and follow me on Seekingalpha.com, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor, does not own MGX securities, and MGX Minerals is a sponsoring company. All facts are to be checked by the reader. For more information go to https://www.mgxminerals.com/ and read the companys profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Want to read more Energy Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles with industry analysts and commentators, visit our Streetwise Articles page.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Images provided by The Critical Investor