After compiling, interpreting and modelling all available data and surveys, and defining targets, Genesis Metals Corp. (GIS:TSX.V; GGISF:OTC) needed cash to advance their flagship Chevrier Gold project to the next stage: commencing of drilling. Management worked hard to gain interest, and it seemed they succeeded in their aim to get the company funded to drill well into 2018. On top of this, they welcomed two of the most respected and well-known names in the business, Eric Sprott and Osisko Mining as significant shareholders, which is impressive. The company completed 2 rounds of financing to achieve this.

On June 5, 2017, Genesis Metals closed its C$3.25-million non-brokered private placement previously announced on May 24, 2017. Eric Sprott, Delbrook and other large, strategic institutional investors also participated in this first big round.

The company issued a total of 7.3 million (7.3M) units at the price of C$0.14 per unit for gross proceeds of C$1M and 13.95M flow-through (FT) units at the price of C$0.16 per FT unit for gross proceeds of C$2.2M. Each unit consists of one share of the company and one-half of one warrant, each whole warrant exercisable to purchase one share at $0.20 per share until June 5, 2019. The FT units have warrants with an exercise price of $0.23 per share until June 5, 2019. A 2-year warrant is a healthy period, and the small discount and the 40-45% warrant exercise premium isn't a dead giveaway too. Sometimes you see up to 5-year expiry periods with hardly any premium, which create an almost (and often sizeable) risk free overhang for non-participating investors, which I don't really appreciate.

Finders fees accounted for 7% in cash and 7% in 2 year warrants, which is normal; standard finders fees are about 6-7% and can go as high as 10% in a bear market. The cash fee being paid was C$121,732.80 (C$117,672.80 to Medalist Capital, C$2,100.00 to Raymond James and C$1,960 to Echelon Wealth Partners) and the warrants issued were 146,160 finder warrants at C$0.14 and 632,940 finder warrants at C$0.16. (751,100 warrants to Medalist Capital, 14,000 warrants to Raymond James and 14,000 warrants to Echelon Wealth Partners). The warrant expiry prices were significantly lower compared to the placement warrants, but the amount is relatively small so I don't bother too much here.

Sprott buying into Genesis for the first time and Delbrook topping up was a good thing to see, as big names bring additional credibility to a story. Eric Sprott acquired 4.85M shares and 2.4M warrants, representing approximately 7.2% of the issued and outstanding (O/S) shares on a non-diluted basis and 10.4% on a partially diluted basis. Delbrook acquired 3.48M shares and 1.74M warrants, which together with Delbrook's existing holdings of 3.85M shares, resulting in a total of 7.33M shares and 1.74M warrants, representing approximately 10.83% O/S on a non-diluted basis and 13.07% on a partially diluted basis. This is all based on 67.65M shares O/S post-financing. Of course, a 21M shares plus 11M warrant dilution is very significant, as the company had a very tight 46.6M shares O/S and about 15M warrants and options, which would make this a 45% dilution O/S, and 34% F/D, but the company had to raise the cash anyway, the share structure is still relatively tight, and the company is set to start trenching and drilling shortly.

Chevrier Gold project; trenching

Chevrier Gold project; trenching

One can always debate whether a junior should raise in different rounds or not, trying to get success with the first-round cash, get the share price up and raise a second round at less dilution, but in this case I don't see a lot of difference as for example a C$0.30 would save only about 5M shares O/S, and raising it all at once brings a lot of comfort for management, not having to go to the markets in the midst of a drill program. On top of that, Osisko Mining wanted in too, and you can't send those guys, being the big power player in the Quebec region, away very easily as a small junior in my view.

On June 15, 2017, Genesis Metals closed its second and smaller non-brokered private placement previously announced on June 6, 2017, and this placement had the same share prices and warrant exercise prices as the C$3.2M placement. The company issued a total of 1.75M units at the price of C$0.14 per unit for gross proceeds of C$206,500 and 3.9M flow-through units at the price of C$0.16 per FT unit for gross proceeds of C$624,000.

Most of this placement was taken by Osisko Mining as a first investment, which acquired 4.7M shares and 2.3M warrants representing 6.4% of O/S shares of the company and 9.6% on a partially-diluted basis. The above percentages are calculated based on 73M O/S shares after closing. Again, Medalist Capital played a vital role in bringing Osisko to the table, receiving the same finders fee (about 7% cash and warrants) as was paid during the other round. This Osisko stake is in line with other strategic investments of Osisko in juniors in the broad area around Windfall, like Beaufield and Enforcer.

I estimate the cash position of Genesis Metals at C$4-4.2M at the moment, which is enough to complete several drill programs and other exploration activities well into 2018. So far, the company has been busy analyzing and interpreting existing data, completing an IP survey, modelling the Main, South and East Zones and defining trenching- and drill targets.

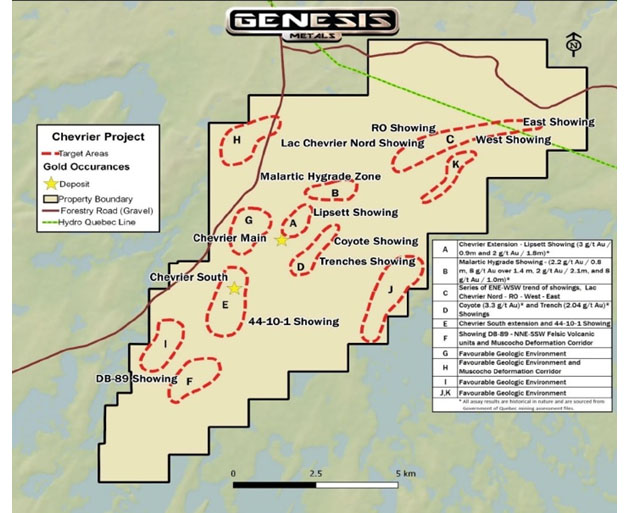

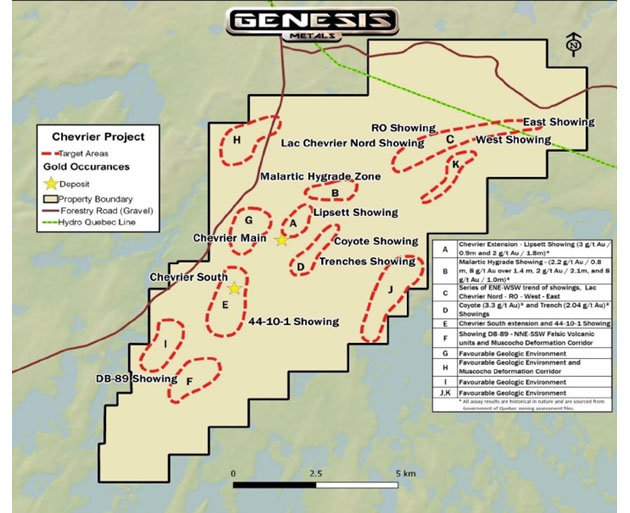

The interpretation of compiled data has identified 11 (I, J and K were added recently) priority targets that require evaluation by drilling in 2017:

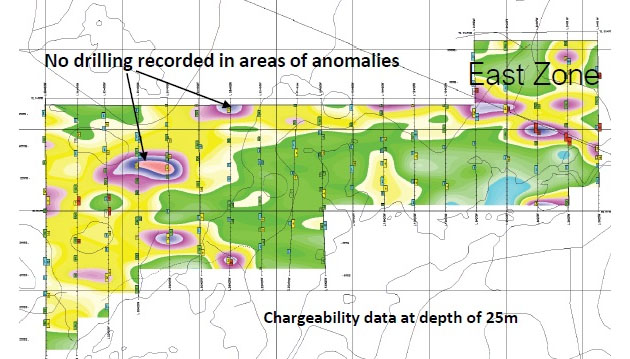

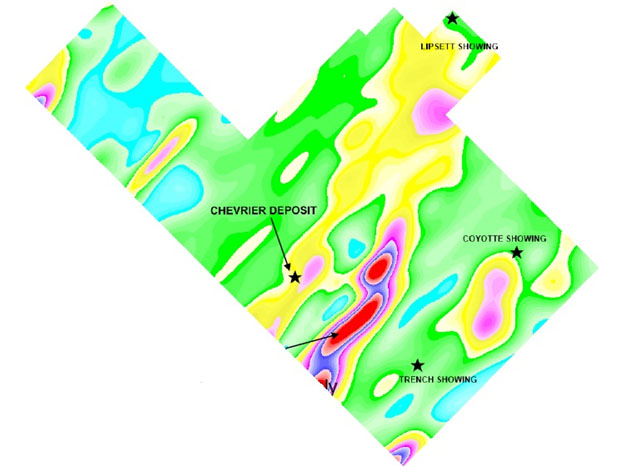

Additionally, results from the recent IP survey have identified at least two new chargeability anomalies that appear to have not been evaluated by drilling:

And:

These anomalies probably will result into targets with following letters of the alphabet, and are the first targets to be drilled by Genesis, starting in the beginning of July, followed by the East Zone, and after this the drill rig will be mobilized to the Main Zone. Trenching around the Main Zone will start at the end of June, by the way. The company has planned a 5,000m drill program based on one rig for this summer, of which 2,000m will be focused on the IP targets and the East Zone, and 3,000m to the Main Zone for infill drilling.

As discussed in my earlier article on Genesis, the company only needs to redrill a fraction (about 10% it seems) of the historical holes to prove up the historical resource estimate, and my view is they can achieve 0.7-1.0 Moz by this small drill program, which is a bargain of course. If this figure can be reached and the ounces could be indeed economic as estimated, then this would put in a solid floor for Genesis. This summer program will be followed by a 5,000m fall-winter program. The all-in drill costs are estimated by management at C$170/m, so this entire program would only cost C$1.7M, with plenty of meters to spare if new discoveries would need further exploration.

I suggested to add one more rig, but it appeared that available rigs and especially personnel are very rare now in Quebec, since again Osisko Mining is using a lot of available drillers with their current 400,000m program, and active developers like soon to be acquired Integra also have a large drill program going on. In addition to this there are numerous explorers like Balmoral, Aurvista, Beaufield, etc. at work, and of course producers doing grade control drilling.

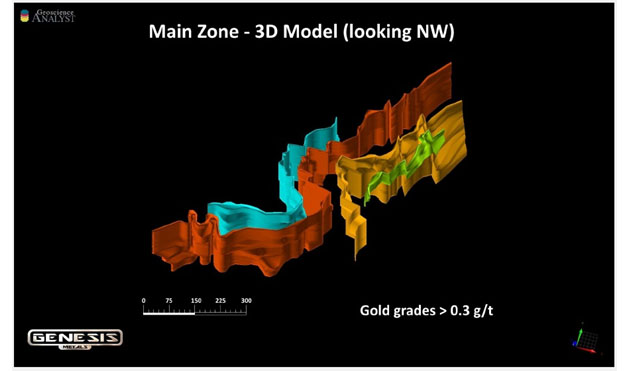

The 3D geological modeling is nearing completion for each of the three mineralized zones as mentioned, and the company is also working on rendered sections, which will increase the understanding of deposits. The results from the modeling will enable a better understanding of gold distribution and parameters that control this mineralization, and define the infill drill program for each zone:

Another issue discovered by the company was the fact that not all located drill core was assayed, so the company is reassaying 1 out of 5 existing drill cores at the moment. To give you an idea for costs of this particular method of analysis, this will cost C$22/m, so this is relatively cheap since it is only a few holes of a few hundred meters each. I also asked the costs for an IP survey for the entire claim package since this seems to be flooded with targets, but this would be too costly, as the last IP survey already cost about $150k and covered only several targets. Management estimated a total survey at about C$1M, which was out of reach, plus the company already had defined more than enough targets to keep themselves busy for a year.

Genesis Metals is also performing the same work on compiling and interpreting of data on its other property, October Gold, to be finished in August. Since prices of claims and land packages were going up like crazy and there is increasing interest, the company told me looking for a JV partner was definitely something from the past now. It will be obvious that there is no money to complete all sorts of exploration and drilling on October Gold, but management isn't planning on shelving it completely either.

A bit of a surprise was the leaving of Chairman Rob McLeod, who has been with the company and its predecessor since inception. As exploration is in his blood I'm sure he wanted to be involved at the beginning of drilling at Chevrier, but it appeared that Rob had too many directorships according to Glass Lewis rules, and his focus was increasingly needed at his family company, IDM Mining, of which he is CEO. Fortunately, and despite those rules of best practices, etc., Rob is able to stay involved at Genesis as a strategic advisor though, and CEO Brian Groves will assume the role of chairman in addition to his current position. Less of a surprise was the appointment of Vice President Jeff Sundar to president, as he was the founder and president & CEO of Genesis until the restructuring last year.

A long story short: Genesis Metals is fully cashed up and ready to drill, and I'm very curious what will come out of this. I expect the first few exploration drill holes to take two to three weeks to complete, plus another three to four weeks of assaying, although it will most likely also be crowded at the assay labs at the moment. Nevertheless, I expect a busy second half of the year for Genesis, with hopefully a lot of positive drill results, possibly taking care of a long-awaited re-rating.

October Gold project; prospecting

October Gold project; prospecting

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at http://www.criticalinvestor.eu/, in order to get an email notice of my new articles soon after they are published.

Critical Investor Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Genesis Metals is a sponsoring company. All facts are to be checked by the reader. For more information go to Genesis Metals Corp. and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long term commodity pricing/market sentiments, and often looking for long term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Streetwise Reports Disclosure:

1) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

2) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and photos provided by author