1. Introduction

The zinc market is on the verge of a potentially huge supply deficit as several large mines have been shut down with more zinc producers to follow suit, as I have already explained in a recent article on sponsoring company Tinka Resources.

The uptrend in the new zinc cycle has already started when the zinc price moved from less than $0.70/lb to a recent high of $1.32/lb, consolidating around $1.12/lb at the moment, so it is interesting to focus on interesting projects which could be brought into production in the current zinc cycle, which is expected to last two to three years.

A company that is generating more and more attention these days is Vendetta Mining Corp. (VTT:TSX.V), which is advancing its Pegmont Lead-Zinc project in Australia as quickly as possible. The company is progressing well in 2016 and 2017 so far, and is now ready for the next step: increasing the tonnage at Pegmont. Vendetta is now fully cashed up after the recent closing of a CA$4.2M capital raise, and the next 12 months will contain several catalysts, of which an upcoming updated resource estimate will be the very first one, as it is expected in a matter of days, and has the potential to significantly increase upside for this stock, despite the already impressive gains since last summer, as I will discuss in this article.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. The company

Vendetta Mining is an advanced stage exploration company headquartered in Vancouver, Canada, and is focusing on its only project: the Pegmont Lead-Zinc deposit in Queensland, Australia. Pegmont certainly isn't a new discovery as the project has been around for several decades, and didn't draw much interest, but Vendetta studied the available data thoroughly, and successfully applied a new theoretical geological model last year, which turned out to be a real game changer. This new model proved to be true, and made the project much more interesting as it suddenly had a good chance to eventually become a mine.

As the Pegmont project is located in Australia, the geopolitical risks associated with an investment in Vendetta Mining are modest. According to the most recent Fraser Survey of Mining companies, Queensland is ranked a decent #36 out of 104 jurisdictions regarding the Policy Perception Index, which is indicating the degree of mining friendly policies. On top of that, Queensland ranks #4 on the Best Practices Mineral Potential Index, which looks at regions solely based on their mineral potential.

Vendetta Mining has a strong management team, spearheaded by Michael Williams, the man behind selling Underworld Resources to Kinross Gold for CA$138M. Peter Voulgaris has the technical side covered after having spent decades developing and building mines in the Mount Isa District, although his most important tenure was being the Technical Services Manager at the large Oyu Tolgoi copper-gold project in Mongolia. A third co-founder of the company is Doug Ramshaw, a former mining analyst who now has 20 years of experience in the industry in corporate roles.

Good people usually attract more good people, and in 2016 Doug Flegg and David Baker joined the board of directors. Director appointments usually aren't a big deal, but Doug and David aren't your every day additions.

Doug Flegg has in excess of 30 years of experience in the mining finance side after having spent the last decade as no less than the Managing Director of Global Mining Sales at BMO Capital Markets, a subdivision of the Bank of Montreal. His network and experience (with in excess of $25 billion worth of deals under his belt) is very likely a significant and useful asset when Vendetta for example could be approached for a M&A deal.

David Baker also has two decades of experience of which 15 years were spent with the Ivanhoe group of companies, where he managed the prefeasibility study on the huge Oyu Tolgoi project in Mongolia, followed by leading the Oyu Tolgoi financing due diligence program for a $4 billion debt finance facility.

With these two new additions, Vendetta Mining has considerably strengthened its board of directors, almost to the point that I started wondering at the time why guys of this caliber would even bother. The share price action since then shed some light on the quality of this story and investment return potential, which was probably what attracted them.

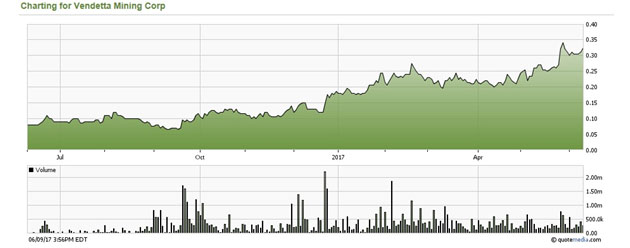

Vendetta's share price has been strong since touching an all-time low of CA$0.045 last year, as its share price increased by a very impressive 622% based on the most recent closing price of CA$0.325. The average daily volume is a healthy 308,000 shares:

Share price; 1 year period

Share price; 1 year period

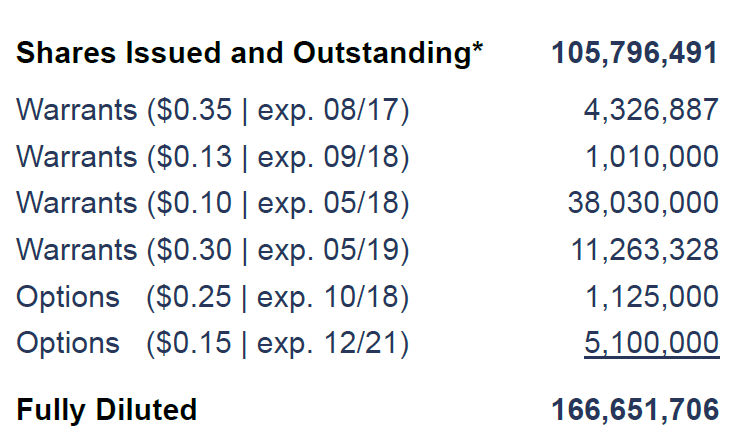

After the most recent financing, Vendetta currently has a cash position of approximately CA$4.3 million, which will be sufficient to complete the 2017 exploration program, publishing an updated resource very soon and likely another updated resource in Q4 2017, and possibly a preliminary economic assessment (PEA) by the end of this year or early next year. The share count has now increased to 105.8 million shares outstanding for a market capitalization of CA$34.38 million, whereas an additional 60.8 million options and warrants (of which most are well in the money) result in a fully diluted share count of 166.7 million shares and a fully diluted market cap of CA$54.18 million:

This actually is a relatively high F/D share count for a junior still developing a resource, but approximately 10 million warrants are still out of the money whereas an additional 38 million warrants priced at 10 cents expiring in May next year will be very useful to fund the final payment to the property vendor. The first important expiration date is the one for the 4.3 million warrants priced at CA$0.35, expiring at the end of August. It is not unrealistic to assume that a convincing resource update and following positive drill news could push Vendetta's share price well above this CA$0.35 threshold, which would likely add an additional CA$1.5 million to its treasury.

Vendetta's management team owns approximately 8% of outstanding shares, and very likely also controls a substantial amount of warrants and options. Together with Solitario Exploration and Royalty and Resource Capital Fund, almost 35% of the company's shares are in strong hands with a long-term investment horizon. The free float is quite low, and this explains why Vendetta's share price remains relatively strong.

3. The Project

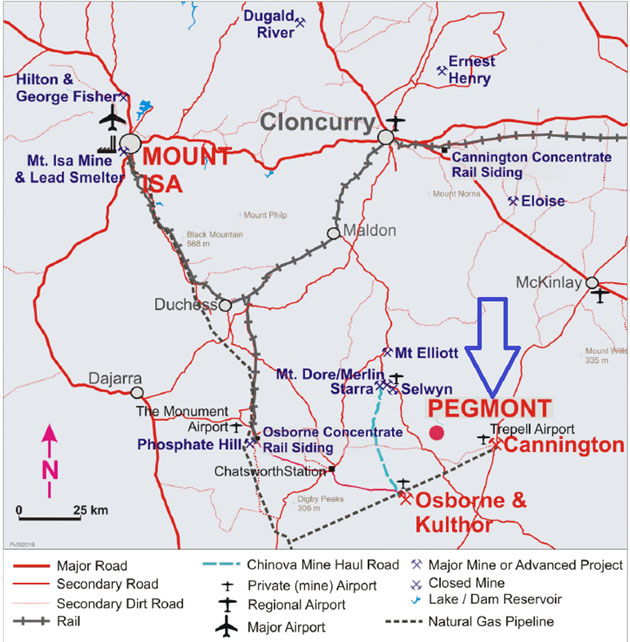

The Pegmont Lead-Zinc project is located in Australia's Queensland province, approximately 175 kilometers south-east of the Mount Isa Mine, one of the biggest mining operations in Australia (copper/zinc) combined with a lead smelter, and is right in the middle of a very prospective area as there are several producing and past-producing mines within 25-40 kilometers. The Cannington Mine owned and operated by South32 (BHP spin-off), is probably the best known mine and is located within trucking distance from Pegmont.

Geographic map Pegmont location

Geographic map Pegmont location

As the Mount Isa region is widely known as a world-class mining region that hosts in excess of 20% of the world's zinc and lead reserves, there is no lack of infrastructure (including roads, railhead and natural gas for power generation), the technical and operational know-how is already there, and permitting isn't expected to create any problems.

Pegmont project; map location

Pegmont project; map location

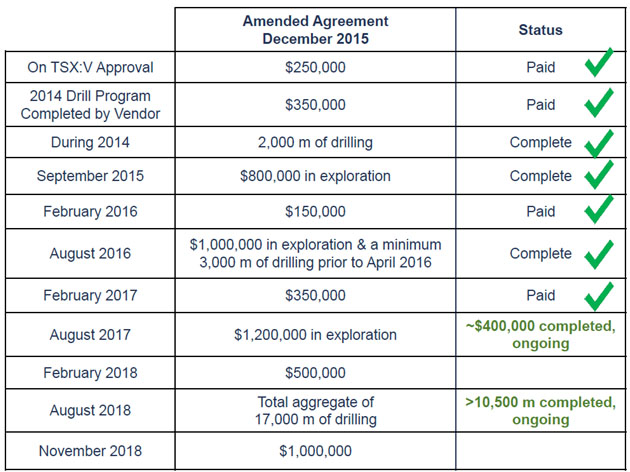

Unfortunately (and fortunately for Vendetta of course) none of the large companies (Placer Dome, Newmont, BHP), which previously owned the project, could make Pegmont work (due to a misinterpretation of the geological structure, which I will discuss later on) and for the past 20 years the project was owned by Pegmont Mines, a privately owned company that entered into a earn-out agreement with Vendetta Mining in 2014.

The recently completed CA$4.2 million financing was important for Vendetta, not only to demonstrate it had the funds required to complete their programs, but that it could also easily meet the earn-in requirements for the 100% option.

The warrants, mostly in the money and expiring six months before the option does, would have been sufficient to take care of the final property payments and an advance royalty payment should this be necessary, but not being dependent on this is an obvious advantage.

Vendetta is also shaping up to be an interesting acquisition target for one of the nearby operators in my view, so it isn't unrealistic to see someone making an offer even before the final property payment is due.

Payment schedule Pegmont

Payment schedule Pegmont

With the deep in-the-money warrants taking care of the property payment, the proceeds of the recent placement will be used to drill out the resource to the company's targeted tonnage of around 12-15 million tons (Mt). Vendetta has almost met its exploration commitments of A$3 million and the planned 12,000 meters of drilling this year will meet the 17,000-meter drilling commitment required under the option earn-in.

The market now really seems to start to understand the Pegmont project and as Vendetta had to upsize and oversubscribe what originally was announced as a CA$3 million financing, it now also already has the funds to start working on its environmental baseline study, and is able to quickly fine tune the metallurgical test work, in order to further derisk the project and enhance future economics as much as possible.

One of the requirements for a Canadian mining company to obtain a listing is filing an NI-43-101-compliant technical report, which Vendetta also did in 2014. This is the only NI 43-101 report available to date but will be updated soon when a new resource estimate will be released within the next week.

Most new projects only have a technical report just describing exploration claims and geological make-up without any indication of resource as often hardly any drilling has taken place, but one of Vendetta's strong points was Egmont's well documented exploration history, which allowed it to complete a maiden resource estimate based on historical drilling:

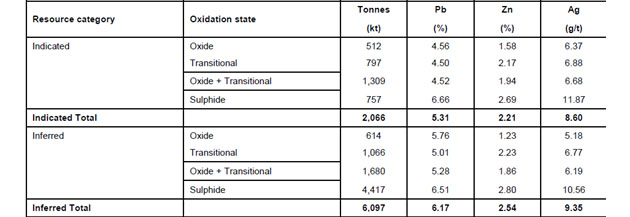

Pegmont: 2014 NI43-101 resource estimate

Pegmont: 2014 NI43-101 resource estimate

This resource estimate contains a total of 8.15 Mt mineralized rock, but due to (expensive) recovery issues it is best to keep the oxide and even transitional zones out of the equation for now, and solely focus on the sulphide zones at Pegmont. This would result in a total sulphide resource of almost 5.2 Mt at an average grade of in excess of 6.5% lead (Pb) and almost 2.75% zinc (Zn). The much higher lead content was probably the main reason why the market has never really seen Pegmont as a true zinc play until last year, when the earlier mentioned new technical model was validated and more higher-grade zinc zones were encountered.

This new geological model was the idea of director Peter Voulgaris.

Voulgaris worked at the nearby Osborne mine several years ago and was keeping an eye on the work that was being conducted by the previous operators at Pegmont. Over the years, he got the idea to disapprove a long-time held geological theory.

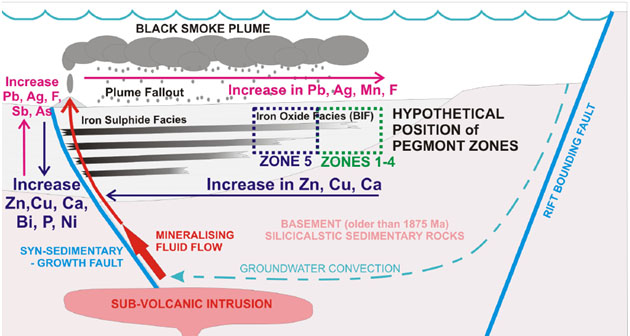

This theory assumed Pegmont being a single lens, lead-dominant system with a limited silver credit. Back in the 1970s and 1980s, this might have been a valid assumption, but Voulgaris considered the project to have all the characteristics of a classic Broken-Hill style deposit. The concept of this deposit was based on multiple stacked and folded mineralized horizons, with increasing zinc grades at depth and thicker mineralized zones at the folds itself, as was the colossal Broken Hill deposit itself, in the end laying the foundations of giant BHP (BHP means Broken Hill Proprietary). This would have interesting consequences for the future of the project.

As the mineralization would come closer towards the feeding source, it shouldn't only result in an increase of the overall grade of the Pegmont mineralization, but also the zinc to lead ratio would increase from the more lead-rich upper part of the deposit. The Broken Hill-model discards the single lead-dominant lens theory and supports an updated view of multiple stacked zones at depth. This was an incredibly important analogy/idea as it basically would allow Vendetta Mining to look for additional tonnage, which was necessary to have a viable mine plan.

Pegmont; geological concept

Pegmont; geological concept

The first drill program, while small at 3,000-3,500m, was perhaps the most important drilling that has been conducted in the last couple of years of exploration, as the new theory was indeed validated by it. This already had tremendous market implications and several producers probably have Pegmont firmly on their radar since then. Another important piece of the puzzle was the metallurgical test work, of which the results were announced earlier this year in March.

When Vendetta became involved with the Pegmont project, there were a couple of areas that were critical to the success of advancing the project. The first subject was as described the new theoretical model that allowed the company to start building economic grades and tonnage, but perhaps just as important was the metallurgical test work, which would indicate the economic viability of Pegmont.

From a historical perspective, the only metallurgical work conducted prior to Vendetta's involvement was a bulk concentrate test which is meaningless, as there are separate lead and zinc smelters for a reason.

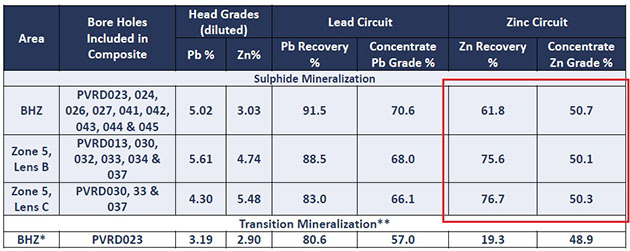

Confirming the potential to produce two separate concentrates was absolutely essential for any investment thesis. Using drill core from the 2016 drill program, Vendetta commenced and reported the first results of differential concentrate test work, which was a very important additional step to derisk the project. The results of this test were very good as Vendetta Mining was able to produce a zinc concentrate with an average zinc grade of 50.2% from the underground sulphide zones with an average recovery rate of 76%. The open-pit target resulted in a recovery of 62% of the zinc for a concentrate grade of 50.7%. In both cases the recovery rate for the lead was substantially higher.

Met testing; recoveries

This was a great and very important result for first met test work, as it delivered the much-needed verification. The recovery rate for both zinc and lead are relatively high whereas the concentrate grade meets the requirements of the smelters. I expect the company to optimize recoveries even further from now on. Understandably, management was pretty stoked about it during PDAC when the news came out, but as met work isn't as well understood and sexy as good drill results, all the attention for zinc plays went to colleague/competitor Tinka Resources, which produced a stellar first drill result on its project at the same time. Fortunately, things have improved markedly though on the investor awareness side for Vendetta, due to management telling the story at many occasions, and solid coverage by the likes of much respected Eric Coffin, and continuing good news, also on the exploration side of things.

Let's have a look at the current exploration plans, and possible implications of them.

4. The exploration plans for 2017

As several important parts of the puzzle have now been confirmed, the recently unveiled 2017 drill program will only have one real target: increasing tonnage.

With an existing resource containing just over 5 Mt in the sulphide zones, Vendetta Mining obviously doesn't have enough ore to warrant a mining operation. Even after the upcoming resource update, which most likely involves a significant increase, Pegmont probably still lacks the size to unlock the necessary economies of scale.

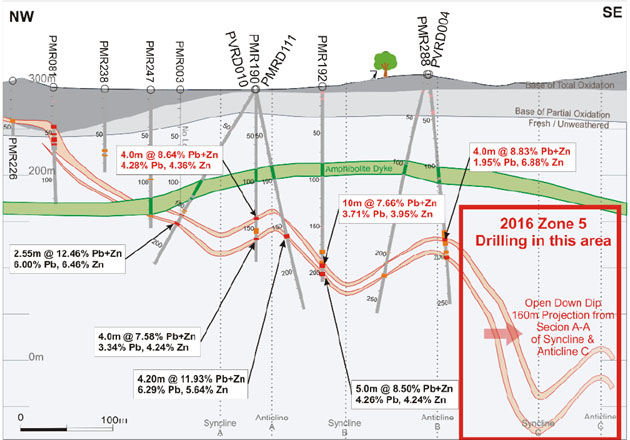

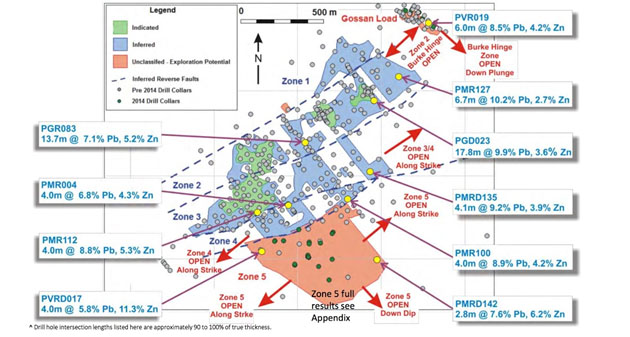

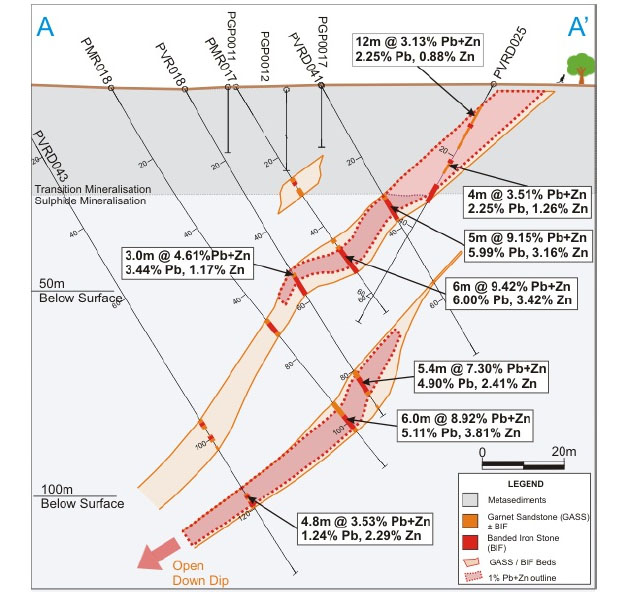

The company has now designed a 12,000-meter drill program that will solely focus on resource development in three separate areas. First of all, Vendetta will test the Z-fold underground target (the area between the flat dipping Zone 2 and Zone 3) where the company should be able to quickly add tonnes and pounds if the drill program is successful as this zone is expected to be high grade.

Pegmont; long section

Pegmont; long section

A second focus will be on Zone 5 where Vendetta thinks it will be able to add more Inferred tonnes to the overall resource estimate. This Zone 5 could play a very important role in the future development of Pegmont as the previous drill program has confirmed the zinc grades are increasing along strike towards the southwest. This zone has not been included in the previous resource estimate, but will be included in the upcoming update, and the potential to add tonnage here is very real.

A third and final part of the program will be zooming in on the gaps in the Inferred resource estimate in the open pit zone of Zone 1 and Zone 2, as confirming the continuity of this mineralization should allow Vendetta Mining to upgrade some tonnes from the Inferred category to the Measured and Indicated (M&I) category.

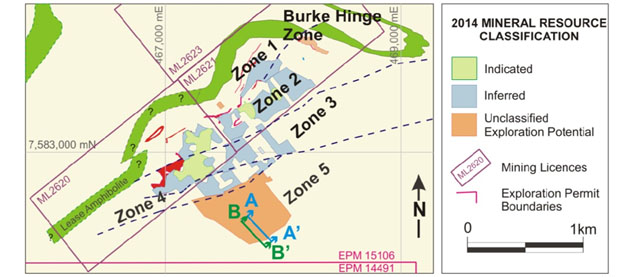

The Pegmont deposit is a lead-zinc deposit hosted within banded iron formation. The mineralized zones are surrounded by quartzite, which seems to be very stable. This is important, as underground mines in the area often seem to have issues with rock stability. The Broken Hill type classification of multiple stacked mineralized zones combined with post mineral folding and sometimes faults is very relevant for Pegmont, and implies thicker mineralized zones in folds. The 2014 deposit model was based on faults, defining the different zones, but although these faults seem to be obsolete now as the entire deposit seems to have the characteristics of a folded blanket, management likes to keep the existing way of zoning intact as the folds still have an impact on mining sequences beyond Zone 1 and Burke Hinge, both deemed eligible for open pit mining. Taken from the 2014 NI 43-101 report, the fault lines are shown by the dotted blue lines on this map:

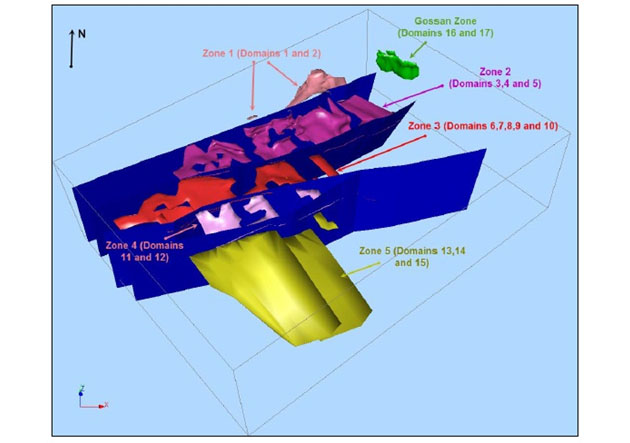

The report also provided a 3D model of the resource, the blue "curtains" being the fault structures. Already visible is the blanket concept, although each zone is heavily perforated except zone 5, which hadn't enough drill holes to visualize adequately:

Management is planning to incorporate 13,500m of drilling in the upcoming resource update, which will in short integrate the folding structures, a delineation of Zone 5 and Burke Hinge, and further infill of the other zones. As can be seen here (and in the news releases since the summer of 2016), the zinc grades are increasing at depth (Zone 1 near surface, Zone 5 deepest):

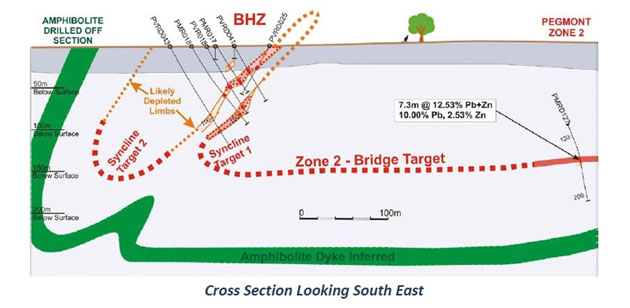

The Burke Hinge target on the other hand isn't substantial, but it is open pittable and as such very interesting for a starter pit scenario, likely saving lots of future capex:

Burke Hinge Zone; map/projection

Burke Hinge Zone; map/projection

The sulphide mineralization starts at just -24m depth, and between this and surface the mineralization is almost all transition. The company has done met testing on transition mineralisation based on just one hole for recovery of zinc, the results weren't very encouraging so far. Lead recovery attributed to 80.6%, which wasn't far below the sulphide recoveries (83-91.5%), but the zinc recoveries came in at just 19.3%, which trailed sulphides significantly (61.8-76.7%). Zinc was in fact already concentrated very close to the mandatory 50% threshold (48.9%) so this seems within reach, but a recovery of 19.3% obviously would need a lot of optimization work before becoming economic, as the zinc grade was just 2.9% for this one hole (and in line with other near surface drill holes btw).

Burke Hinge Zone; section

Tonnage will not be impressive (I estimate a few hundred thousand tonnes at most), but it definitely could move the needle for a potential second starter pit. Vendetta will continue its metallurgical test work, to continue to work on and advance on the preliminary results, but is also looking to connect the Burke Hinge Zone (BHZ) to Zone 2:

Interestingly, Vendetta considers part of Zone 2 as an open pit target as well, although the strip ratio would be considerable, I would estimate it ranging from 7:1 to 10:1. The flat dipping, deeper part of Zone 2 and Zone 3 will be eligible for underground mining, to be more specific by Room & Pillar methods. The steeper dipping parts will probably need Open Stope mining. But with a gross metal value (GMV) of about $200-250/t (is comparable with 6 g/t gold) there is margin for a high strip ratio, as a strip ratio of 4:1 to 5:1 is roughly considered an economic threshold at 1.2-1.5 g/t gold open-pit operations (non heap leach, which could have much lower grade).

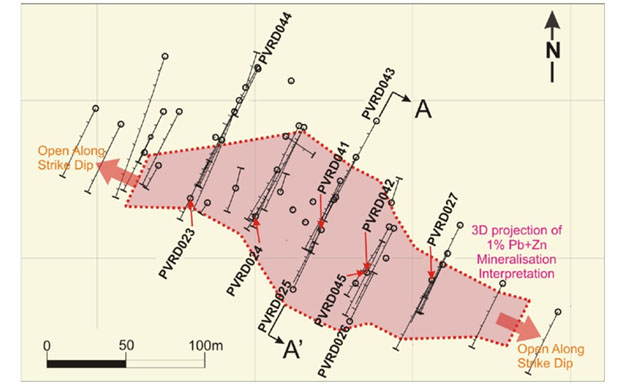

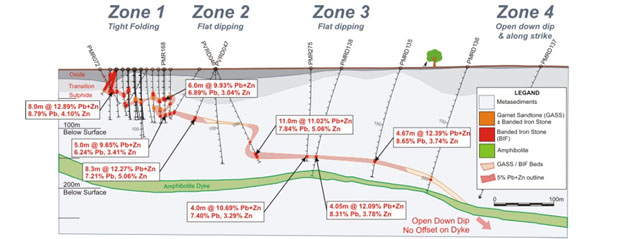

The Z-fold between Zone 2 and 3 was probably interpreted as a fault in 2014, but the company has completed enough drilling to conclude it is a continuously mineralized fold, and one with higher grades at the turning points (noses) as well, which is confirming the theoretic model. As the strike length is about 2km, this Z-fold of about 60m high and thicker mineralization, could easily add 1Mt alone if continuous. As Vendetta's corporate presentation indicates on p. 12, there could be more of those Z-folds:

"Flat dipping through Zones 2, 3 and 4, each zone separated by a drag "Z" fold"

meaning much more tonnage could possibly be added in the upcoming resource update. But I will stick to just one Z-fold for now to be conservative. This fold is shown on this section, between Zone 2 and 3:

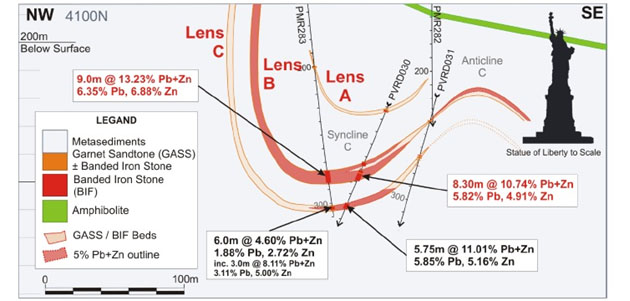

Zone 5 actually has three mineralized lenses but only lens B and C seem to have economic mineralization:

With a strike length of about 500m, the mineralized envelope could be an estimated 0.7-0.8 Mt in the thicker nose part (B+C), and another estimated 0.7 Mt in the steeply dipping part of B. If infill drilling of Zone 1-4 manages to find at least another 1 Mt, my rough estimate for total new sulphide tonnage comes in at about 3.7-3.8 Mt. If this would be added to the existing sulphide resources of 5.2 Mt, the new total sulphide resource would come in at 8.9-9.0 Mt. If this would be added to a slightly increased transitional resource of about 2 Mt, the total economic resource would come in at about 12 Mt. In my view, the company would be well underway in that case to become a standalone viable project, which would need for example a 10-year life of mine, and an annual production profile of 1 Mt sulphides, which could be achieved by a 3000-tpd operation. Besides this, for example the continuously falling grades at the nearby Cannington mine could spark interest of owner South 32 as well, with the zinc deficit story well underway, and interesting economics usually generate more interested parties, of which is no shortage in the region.

To be really attractive in both scenarios, Vendetta needs to upgrade this hypothetical resource one more time to about 12 Mt sulphides as there is always quite a bit of dilution, in order to be able to convert 10 Mt of those resources into mineable reserves. And there is enough exploration potential left, as can be seen in the map with the zones and drill collar locations, so I don't have much doubt about this being achievable. My take is the company will do a PEA after it has reached its standalone tonnage target, whether it will be 12 Mt or maybe even in the range of 15 Mt sulphides as the company has implied. As a consequence, it is likely this tonnage will not be reached during the upcoming resource update (in a few days most likely), but it will take a second resource update later this year or maybe Q1 2018, before a PEA can be completed. We will see.

I'm not going to delve into DCF calculations as it is too early resource-wise and I don't really have a good clue about capex and starter pit economics, but with an excellent rock value (GMV) of over $200/t, something pretty economic should come out of it. Ballpark back of the envelope numbers suggest at the very least a super conservative NPV8 of $100 million or CA$135 million based on 10 Mt and $1/lb Zn prices, which would be four times the current market cap.

5. Conclusion

Vendetta Mining has made major progress in the past 12 months, and whereas Pegmont was just a very small, sleeping lead/zinc project two years ago, the project is now becoming one of the hottest stories around. I expect the upcoming resource estimate to add a substantial number of tonnes to the existing resource estimate and as the metallurgical test work proved the ability to produce saleable lead and zinc concentrates, Vendetta's main task is now to get the total size of the resource up to critical mass.

I believe the upcoming update will show at least 9 Mt sulphides, and if Vendetta Mining is able to define a 12-15 Mt resource estimate this year, it could use (at least) 10 Mt sulphides in the mine plan of a PEA which I'm anticipating early next year, which could definitely be able to generate stellar economics in my view. And projects with sufficient size and strong economics usually attract interest of (nearby) producers, and there is no doubt in my mind that those parties will perform their own calculations when the first resource update comes out, and might even decide to make a move before a PEA comes out.

At the current, still modest market capitalization of CA$34.4 million, the risk/reward ratio seems very favorable for those who would like to increase their exposure to zinc and lead in a safe region.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at http://www.criticalinvestor.eu/, in order to get an email notice of my new articles soon after they are published.

The Critical Investor Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. All facts are to be checked by the reader. For more information go to www.vendettaminingcorp.com and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

2) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and graphics provided by The Critical Investor