A few days ago, I postulated that despite the seasonal weakness most were anticipating in May and despite the sharp increase in Commercial shorting that was still below 2016 levels, the precious metals would buck conventional wisdom and advance further into even greater degrees of overbought status.

On Tuesday morning, after watching 22,000 contracts in June Gold completely wipe out every bid down to $1,280.60, causing a sympathetic crash in silver down to $18.06, I was not only ready to break out the infamous Louisville Slugger, but also my wonderful dog Fido went screaming out of the house in obvious expectation of the arrival of an MJB tirade and temper tantrum. Actually, Fido was well guided in assuming a Ballangerian response to the blatant intervention of the bullion banks, which was almost a "given" after the pre-Good-Friday COT report that showed the Commercials now at the highest aggregate short position in gold for 2017 and one of the highest ever in aggregate silver shorts EVER.

The Cartel cretins waited until all of the technical funds were "in" after chasing the gold "breakout" above $1,260 and a similar silver "breakout" above $18.50 until they sensed the slightest hint of weakness at which point they descended upon the Crimex trading pits like sharks in a frenzy. However, despite the pounding, gold battled back into the green and was back above $1,290, while the silver market was still reeling down 1% on the day. That was Tuesday. . .

And again today. . .

(Last two charts courtesy of Zerohedge)

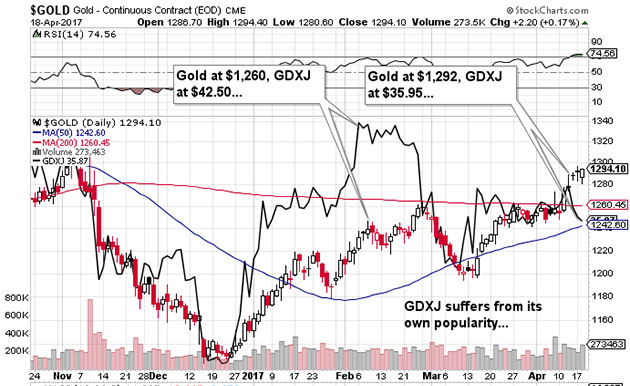

The big news lately is how awfully the junior miners are acting now that Van Eck (creators of the GDXJ [VanEck Vectors Junior Gold Miners ETF]) has been forced to stop buying junior gold stocks. You wonder why the juniors are now in a completely bifurcated market and all you need do is look at the names in the GDXJ that are considered the "anointed ones," while everyone else aspires to be lest they wind up as "orphans" (housed and fed but without sponsorship) or the "zombies" (no food, no shelter, reviled by all). The bankers created the ETFs to capture market share but more importantly, they created ETFs to capture FEES and to corner the bid-ask spreads that allow them to take a haircut on every ETF transaction that occurs.

Applying this line of thinking to the junior gold miners and explorers, back in the days before bankers took greed to a new level, the junior mining space had access to ample funds by way of the junior resource brokerage firms such as Canaccord (before the "wealth management" transformation), Yorkton, Haywood, Fraser Mackenzie, Union Securities and Mackie. Private investors would forge relationships with the resource broker and if he/she wanted to invest in the junior exploration sector, his/her only access would be through the open market or indirectly through a mutual fund or through private placements.

The conduit to the market was not guarded by a gatekeeper called IIROC until the banks decided to exert pressure and then once achieved, the big five Canadian banks squeezed the little firms out of business by creating the money-draining resource ETFs run by ex-bankers whose billion dollar funds would inevitably find their way into the bank-led underwritings, formerly the specialty of the smaller boutique brokers.

Watching the lag in junior miners despite a move over $1,290 in gold is painful but now you know why. The Van Eck GDXJ ETF is a $5 billion fund in a $35 billion junior mining market and there just aren't enough names to go around. This is why I try to have a basket of my own juniors rather than the ones owned by the ETFs because once you are in the GDXJ fund, you are slave to the macro trends and victim to the inevitable moment where you may get ejected from the fund and 18% plus of your issued capital is thrown on the market for sale. In fact, inclusion of your company into the GDXJ has been transformed into a "Sell Signal" because it is the second-greatest liquidity event in a company's life, the first being a takeover by a major.

In all of my writings over the years, I have always held that gold mining stock prices are lead indicators for gold (and silver) prices. In the latest advance in gold to over $1,290, the GDX (the Van Eck Senior Gold ETF) has performed in line with expectations with the exception of the last few trading sessions while its little brother, the GDXJ, has been a pitiful underperformer. So if we are using mining shares to guide our forecasts for gold and silver, do we buy into GDX's strength or do we sell into the GDXJ weakness. I tend to trust the former because the weakness in the GDXJ is due to a technical and regulatory glitch while the GDX suffers no such malaise.

Nevertheless, this confusing signal being given off by the juniors is creating technical uncertainty and it is giving the bullion bank criminals the courage to resume their carpet-bombing of the June Gold and May Silver contracts, thus throwing the karma off kilter. I am currently long the USLV (Velocity Shares 3x Long Silver ETN) and barely onside from the position acquired two weeks ago, while I am on the sidelines for the GDXJ and GDX.

I must apologize if I must vacillate and refrain from some bombastic prognostication as to the next big trade in gold and silver, but the truth remains that both of those markets are very confusing at this point. Accordingly, to have a large leveraged position in gold or silver or the associated mining share ETFs is folly; the next $20 move in gold could take the miners up or down 10% in a heartbeat and I don't feel like taking that kind of drawdown when the indicators are so skewed.

I put a stop loss on the UVXY (above) on Monday morning at $19.90 thinking that the $21.46 close on Friday would provide a large enough gap so as to prevent a whipsaw but, alas, it was not. We were eliminated for the holding by 11:00 Monday morning and it now resides at around $18.40, once again proving that stop-loss strategies for volatile trading vehicles does involve the risk of whipsaws but most of the time, it is far better to protect a small profit than to lament the loss of a larger one. Hence, I am "out" and looking for a re-entry point.

As for the overall investing climate, I have to hark back to Michael Lewis' third most-famous book "BoomerangTravels in the New Third World" (ranking behind "Liar's Poker" and "The Big Short") and the sections in which he describes Greece and Germany. Now, culturally, there are no two more different nations than Greece and Germany. Living and growing up in Canada, I went to school with a great many children of immigrants so I know the various behavioral nuances of Europeans. For example, the British kids were not really "British" in behavior because while they were all pretty tough in the playground, there was NOTHING more frightening that when the big Scot Angus McGuigan got angered by an errant elbow.

Similarly, if you wanted to get something done quickly (like pinching a set of colored pencils from Becky Johnston's desk) I only needed to whisper into Tommy O'Leary's Irish ear and it was done in a fraction of a second. Now, if you wanted to have the schoolyard bully thumped out after class, a casual suggestion to Bruno Teti (with promise of a "plate o' fries" at Burt's Diner) always got the job done. But when it came to the Greek and German lads, they were total polar opposites.

My buddy Ulrich (pronounced "Ool-rick^^^" with the "CK" at the end of his name sounding like one clearing one's throat) could tell you how many ounces of dishwasher soap was needed to remove blood from a white T-shirt but Teddy Gerasimos couldn't tell you what dishwasher soap was used fornot that he was unclean, his mother did all the laundry EVERY DAY. Ulrich had his desk organized in a manner that resembled a floor plan at a jewellery store; Teddy's looked like the bargain bin at Target. Ulrich liked to play tennis and gymnastics (where he didn't have to "TOUCH" anyone) while Teddy loved hockey and rugby and wrestlinganywhere there was total chaos and lots and lots of physical punishment.

The point of this rather ethnocentric critique of the European Union and its inhabitants is that we have now watched the English (not British, mind you) decide to leave the EU and very soon we will have the French elections where, no matter what the outcome, the dual dilemmas of debt and immigration are bearing down on the integrity of this absurd "union" like a handshake between Ulrich and Teddy, which would never happen for the simple reason that Ulrich would never TOUCH Teddy let alone shake his hand let alone agree with him on ANYTHING.

The root cause of the immigration problem in Europe happens to have been the unilateral American decision in 1992 to invade Iraq in order to defend "freedom"erHalliburtonerMobil Oiland create a generation of jihadists-to-be after these little Islamic girls and boys watched Uncle Amir get blown up by a bunker bomb. They all went "refugee" and wound up in Holland or Norway or Germany and especially France and are now awakening from within the walls of their ghetto-like cocoons as fully grown young adults eager and willing to assign blame for the 40% unemployment rate and near-poverty conditions.

These same conditions are prevalent in every single country in Europe and to defend against it requires that basic freedoms (like the right to drive a cement truck) must be policed in order to prevent the mass murders. In my politically incorrect opinion, these Eurozone politicians should have remembered Granny's old health adage "Prevention is the best medicine."

Carrying on with this geriatric and ethnophobic line of thought, these young Millennials that are soon to inherit the mantle as the largest voting bloc in the democratic world are 90% liberals and >50% socialists and before long, they will be legislating we Baby Boomers into exile from the Halls of Elitist Power. Since the Millennials gravitate to an urban world of mass transit and Uber and prefer to share rental accommodations rather than equity, the adherence to pro-Wall Street policies and "global growth" agendas will be thrown to the wind in favor of "safe spaces" and "wealth redistribution."

To wit, those are NOT optimum surroundings for bull markets in stocks and they are nightmare surroundings for sovereign debt and the ensuing defaults. In sum, after a government-supported nine-year bull market in financial assets, it is time for a pause (at best) or a crash (at worst). You might not wish to short stocks now (or ever) but to be sidelined with ample cash and buying power and a liberal holding of gold, silver and the associated gold and silver mining stocks is most certainly not a bad place to be.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts courtesy of Michael Ballanger except as noted.