There is an ongoing bull market that hasn't been internationally recognized yet and that's investing in the North American marijuana sector. One really needs to understand that there is one going on south of the border and another one north of the border. They are two completely separate bull markets and at very different stages as well. One we love and one we wouldn't touch with a ten-foot pole.

The U.S. marijuana sector is not only mature, it's in quite a bad shape from an investor's standpoint. The U.S. cannabis sector is years ahead of the Canadian and has at this stage gone so far as to attract scam artists. On the OTC alone there are now almost 400 companies that call themselves cannabis stocks. These are mostly penny stocks with no revenue or any prospects thereof. Investors that don't suffer from a gambling habit should stay away.

In comparison, Canadian listed marijuana producers are easy to keep track on as they are just a little more than a handful. We believe that the marijuana sector in Canada is setting itself up to become the next big thing everybody wants to get in on. Sure, it hasn't gone unnoticed that the sector has done very well this year and is currently working itself through a well-needed consolidation, but we think the bigger moves are yet to come as we are still in the early days.

We have started to look more closely into the sector and there are some quality companies out there. But what is very striking is the amount of crappy companies overwhelming this sector. For those of you interested to invest in marijuana, we urge you to be very picky and only go for the really high quality names.

Marijuana for recreational use in Canada is getting more and more acceptance and support. It looks like the changes in the laws will be put in motion to make it legal for anyone over 18 years of age to use. As most of you already understand, it doesn't necessarily take for laws to have passed, it's enough if people expect it to happen to get a huge amount of interest and investment dollars to get the bull market going at full speed.

Background

In 1923 marijuana was prohibited in Canada and during the next 80 years, public opinion supported the unlegal approach to marijuana. Today we have a totally different situation both in Canada and around the world. More Canadians now prefer softer marijuana laws and according to a poll made by Globe and Mail, 68% of the Canadians now consider legalization of recreational marijuana to be a reasonable approach.

Justin Trudeau The Road To Legalization

A year ago Justin Trudeau was elected Prime Minister in Canada after a record election of the Liberty Party. One of Trudeau's first proclamations in office was the announcement that a federal-provincial-territorial process was being created to discuss a suitable process for the legalization of marijuana possession for recreational purposes.

This decision is driven by the wish to reduce access for young Canadians, remove cash flow from reaching the criminal sphere and to bring down the amount of taxpayer money used to enforce marijuana laws.

Trudeau first publicly expressed an interest in the legalization of marijuana back in the summer of 2013 when he said:

"I'm actually not in favor of decriminalizing cannabis. I'm in favor of legalizing it. Tax it, regulate. It's one of the only ways to keep it out of the hands of our kids because the current war on drugs, the current model is not working. We have to use evidence and science to make sure we're moving forward on that." (source)

Marijuana in Canada

The Canadian marijuana sector today is worth approximately C$100M and it is growing rapidly. Patient growth is over 10% month-over-month (!), which means that in one year's time Canada will have 360,000 registered patients. For you to better comprehend the significance, Health Canada has estimated that the market for medical marijuana, by 2024, could reach over 450,000 patients and be worth over $1.3 Billion. By the look of things, Health Canada is wrong by at least 6 years. The point we are making here is that the growth is much stronger than ever anticipated.

When legalization for recreational use becomes a reality, all numbers above becomes insignificant from an investor's perspective. The marijuana sector in Canada will rapidly increase in size and many forecasts available today point to the range of a C$7-10B market. To put this number in context, Canadians spent C$8.7B on beer in 2014. We know we are still in early days when we have identified a sector that will grow from $100m to a multi-billion industry almost overnight.

With some of Canada´s most acknowledged businesses and entrepreneurs openly indicating their interest in the medical marijuana sector we guess the stigma that has surrounded cannabis for many years is starting to erode.

Investors need to be picky and should look to invest in those companies that will become large and robust. In the next 3-6 months, we want to invest in newly created enterprises with a solid business plan, great management and access to capital. We are looking to invest in just a few companies and get positioned for what we believe will be one of the best performing sectors in 2017-2018.

We believe that the companies of higher quality that are formed today will become majors in this sector. These are the companies that will over time offer best returns at the lowest risk.

The sector will cleanse itself over time as the strong companies will likely consolidate the sector as a whole while the weaker low quality companies will die and disappear. That's why we are keen on identifying the higher quality new start-ups now and ride them as they grow towards becoming majors in the most interesting bull markets we have seen in a long time.

We have identified such a company that in fact is just about to go public, Emblem Corp. (EMC:TSX.V) There's little doubt in our mind that Emblem will become one of the leading marijuana producers in Canada and we could easily see them reaching north of $1B Mcap within 24 months. We expect them to start trading somewhere around a C$250-300M Mcap.

Let's walk you through the main points on what we believe will be one of the strongest entries by a Canadian marijuana company during 2016. On November 16th, Emblem announced the closing of one of the largest IPO's (Initial Public Offering) ever done by a Canadian marijuana company. Emblem looks to commence trading on Monday December 12th on the Canadian Venture exchange, ticker symbol 'EMC'.

Emblem Corp.'s Share Structure And Cash

The IPO was priced at $1.15/sh + 1/2 a warrant, which with Emblem's earlier financings gives Emblem a fully diluted share structure of ~111m shares (we might be off a little bit but we are close enough). That 111m shares includes warrants and stock options and when all of those are exercised it will bring in another ~C$36m in cash adding to the ~C$30m post-IPO cash position.

Access To Money

Simply a non-issue. In general, marijuana is becoming such a strong sector and this is recognized by the brokers and financial institutions. More importantly, which we will try to describe, is the quality of Emblem itself. When we started looking at the sector a few months ago, we found a couple of decent companies, but none of them convinced us as much as Emblem has.

We mentioned that the size of the IPO is C$23.7m but readers should be aware of the enormously big interest in Emblem. The book was nearly two and a half times oversubscribed and that is as good of a "quality approval" as anything. Emblem could have easily raised $55-60M if they had wanted to.

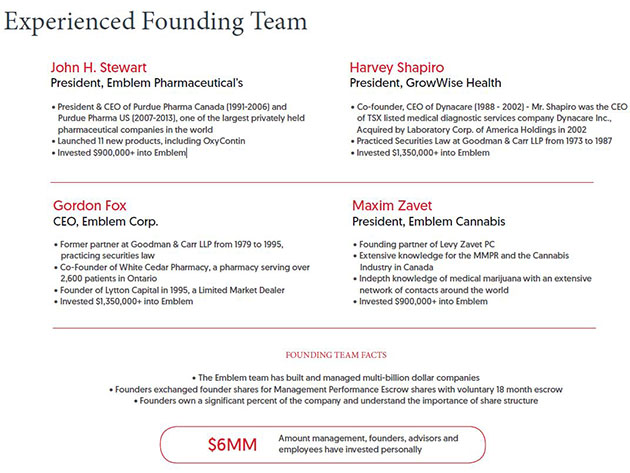

People

Valuating a company is so much more than just comparing numbers to its peer group. Over the years we have learned the hard and expensive way that who is running the business is definitely one of the most important things to look at before investing.

Producing, selling and distributing marijuana is not so much different from selling aspirin or any other pharmaceutical drug. We can't really see a better mix of people running Emblem than this:

To see founders, management and employees invest their own hard earned money into Emblem is refreshing and it has made our investment decision so much easier. Six million dollars isn't small money and it sends a clear message that they believe in what they are creating, one of the best marijuana companies in Canada. To see the people handling our money also having "skin in the game" is important to us and it should be important to you too.

Emblem Gets It Three Legs To Stand On

In our mind, there are two approaches to the marijuana business, either you are an LP focusing only on production and wholesale or you take the same route Emblem has where they control everything from start to finish. Emblem has created three legs in its business:

1) Production

Phase 1 is already producing and Phase 2 will take Emblem to a total production capacity of 2,100 kg (Q2 -17). Phase 3 is already financed and will take total production to a rate of 11,600 kg (Q4 -17). Phase 4 could start producing in Q2 -18 and would bring Emblem's total capacity to 21,100 kg. The timing for planned production expansions vs. when recreational marijuana consumption becomes legal might become nothing less than perfect for Emblem.

2) Pharmaceutical

This division is led by John H. Stewart, former President & CEO of Purdue Pharma Canada (1991-2006) and Purdue Pharma U.S. (2007-2013), one of the largest privately held pharmaceutical companies in the world. Marijuana is so much more than just smoking; the market segment for oils, gel caps, sprays, trans-dermal patches and pills is a huge potential revenue maker. Many of these products will actually be produced from parts of the plants that would otherwise have no other use, kind of like monetizing the by-products to use mining terminology.

3) Education

What's important for every LP out there is to get patients to buy their product. Once a patient is registered they pretty much stay loyal to that LP. One way is to open up medical marijuana clinics, which require large investments. Emblem's approach is a much cheaper and cost effective way to acquire customers. Emblem establishes education centers within already existing medical clinics (1) as well as within stand-alone medical cannabis clinics (2).

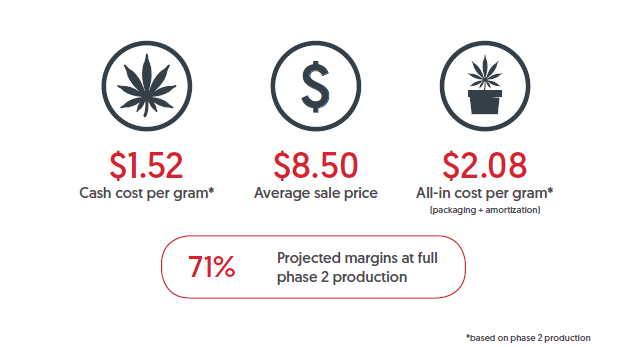

Profit Margins

Production Flowers

Emblem is not your average producer/seller, instead Emblem will deliver medical-grade marijuana from their state of the art production facility, which we are convinced over time will reward the company with a premium for their product. But already today Emblem will enjoy huge margins on their production and sales (see chart below).

Starting up a new business is capital intensive but Emblem is fully financed through the phase 3 expansion. Most listed marijuana companies in Emblem's peer group have yet to reach profitability. Emblem's goal and prediction is that they will deliver a net income in Q3 next year, just ~9 months from now.

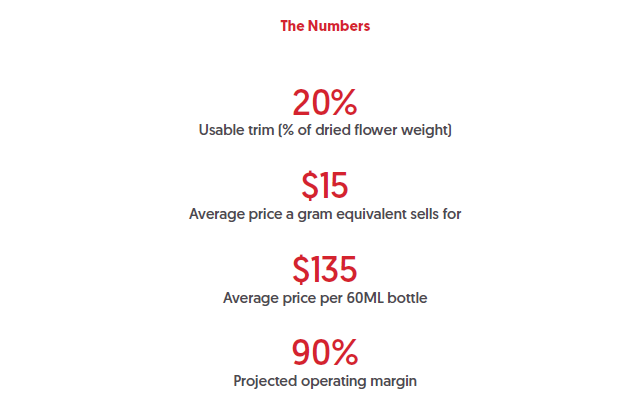

Production Oils

Producers are now able to monetize the entire cannabis plant, not just the dried flower. To produce these oil products require specialized pharmaceutical industry expertise, which is exactly what Emblem has.

The flower margins are looking good, oil operating earnings are a dream as they are projected to reach 90%. Or put in another way, it would be like selling a gram equivalent for $15 that cost $1.50 to produce. Estimated oil revenues from the first 12 months are expected to be $2.9m.

Timing From An Investment Perspective

Supply and demand. Probable legalization in 2017. These two circumstances argue that we are long ways from bubble territory. At the same time we have seen Canadian marijuana stocks double in price in the last three months (after 12 months of consolidation). These facts only reinforce the need for investors to be diligent in their research before making an investment decision.

We feel we have been just that, diligent, and we have come to the conclusion that we are in early days of what will be one of the fastest growing sectors, all categories, in the coming years.

Valuation And Comparison To Peers

At $1.15, Emblem would have a fully diluted Mcap of 128 Mcad, but on a fully diluted basis this would also mean holding ~$66m in cash. It doesn't take a brain surgeon to understand that this valuation is not where Emblem will start trading at.

Let's look at some of the peer group companies and their fd Mcap as per Dec 7th (1):

* Mettrum 342 Mcad

* Organigram 366 Mcad

* Aphria 582Mcad

* Aurora 728 Mcad

* Canopy Growth 1,240 Mcad (2)

(1) Cash positions not taken into consideration

(2) Canopy reached a 2,070m Mcap when ATH C$17.86/sh was reached on Nov 16th

It's obviously not fair to just look at Mcaps, all companies have different production and growth profile, cash position and so much more. But it gives you a feeling of where Emblem could start trading at. We suggest you download each company's presentation just to get a feel for the numbers and compare those to Emblem's ditto.

Canopy Growth is the first Canadian marijuana company to reach a Billion dollar valuation (currently $1,240M Mcap). If plans become a reality, Canopy will reach a production capacity of 24,300 kg in 2018 while Emblem's plans will take them to 21,100 kg in the same timeframe. By that calculation one could argue that Emblem will reach a Billion dollar Mcap in the not too distant future. It's still not a fair comparison to make as Canopy have come further along. But it gives us a feeling and an idea of where Emblem very well could end up.

Conclusion

At this stage and with a long term view, one can probably throw a dart and buy any marijuana stock out there and still do extremely well in the coming years. Some caution is justified though because in the short term, the Canadian Marijuana Index look toppy. Emblem does provide us with an advantage as it's not yet publicly traded and has a lot of catching up to do. Canadian investors are yearning for more names to invest in and we feel Emblem will be the top pick in the sector for others as well.

Remember, buying a marijuana producer is not like buying an early stage mining exploration play where one drill hole decides if your investment will be a success or not. Marijuana producers will not only be in an environment where they enjoy great margins on their product, they also have a production growth factor almost unheard of to consider.

The marijuana companies will be in an environment where they enjoy great margins on their product. However, one must be extremely picky and only invest in the truly high quality companies, the rest should be ignored. Look for 1) a great business plan 2) the right people to execute that plan and 3) make sure that the company has access to future funding as costly financings equals heavy dilution to shareholders.

Editor's note: an earlier version identified Dec. 9 as the first date of sale of Emblem's shares on the TSX.V; the date has been postponed until Dec. 12.

Gecko Research is composed of a small group of private investors whose aim is to broadly share knowledge and investment ideas. Its research is independent and is based on its view of the company or sector based on publicly available information.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosures:

1) Statements and opinions expressed are the opinions of Gecko Research and not of Streetwise Reports or its officers. The authors are wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the content preparation. The authors were not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the authors to publish or syndicate this article.

2) Gecko Research ("the Author") is not a registered financial advisor and investors should seek professional advice before making any investment decision. Our research is independent and is based on our view of the company or sector based on publicly available information. Factual errors might still occur, and it is every reader's obligation to do their own research and not to solely rely on information given by the Author. The article/newsletter is our view about the stock and do not constitute advice to buy or sell shares in the companies we discuss or any other company. The Author's mission is to provide transparent viewpoints on companies we believe provide good investment opportunities. Gecko Research is almost always invested in the companies we write about and thus one can assume that there is some bias within our investment ideas. Although we see ourselves as long term investors, we might buy and/or sell the stocks we write about at any time. In no event shall the Author be liable to any person for any decision made or action taken in reliance upon the information provided herein. In other words, make your own decisions and proceed at your own risk. Investing in junior companies is associated with very high risk as well as extreme volatility. For those of you who cannot deal with that kind of environment, we think you should perhaps look elsewhere for investment ideas. As Gecko Research might occasionally be reimbursed for costs while visiting project sites or arranging investor presentations, Gecko Research does not get reimbursed for the articles we write.

3) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview/article until after it publishes.