The financial risks associated with Greece are now mostly forgotten. Its place was taken over by worry over the migrant crisis and ISISboth issues came suddenly from nowhere and grasped hearts and minds, and then slowly receded in memory. Somewhere within these events, Russia's problems with Ukraine came up, and then the drop in the oil price. Neither provokes much anxiety any more. People have also grown tired of regurgitating about America's "never-ending wars" and "religious fanaticism" and what came first.

Happenings in Venezuela and particularly in Brazil have shown the difficulties of the emerging markets and their huge intellectual, financial and trade dependence on the Westdespite claims to the contrary. Then there is the huge fear of China slowing down. India has consistently failed to meet expectations, but the West's enchantment refuses to go away, mostly underpinned by desperate ideological support for democracy. When it comes to walking the talk, investors instinctively abstain from India. The most recently worry has been about BREXIT.

"Callinex Minerals Inc. has recently discovered two new mineralized zones at its flagship Pine Bay project in Manitoba."

The market has its moods and fascination with headlines. Investors often anticipate what Federal Reserve Chair Janet Yellen might say next for investment decisions. Quite to the frustration of the value investor, big-money has become extremely speculative, investing in currencies, bonds and ETFs. The need to keep up with the indices has forced money managers to follow the herd. If any of this leads to wealth creation, it is a mere unintended consequence. Bottom-up valuationof politics, society and economicshas taken a back seat.

Every crisisreal or imagined, economic or socialseems to have one panacea: Buy the U.S. dollar.

Of course, this does not mean that the universal lawsvalue-investing and that wealth cannot be created by printing currenciesno longer assert themselves. They do in a quiet and, to the taste of many, boring fashion.

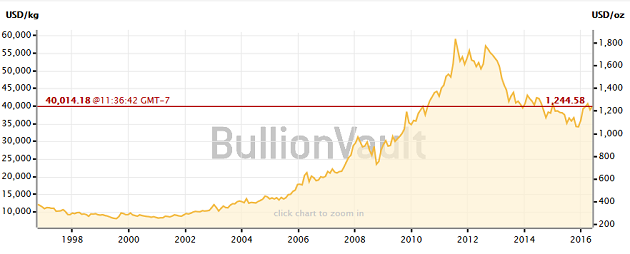

While gold has frustrated many investors, it has been among the best performing financial instruments of this century, the last 16 years. It has gone up about 300%, beating virtually every other major financial instrument.

Indeed, the last five years have been a time for consolidation for gold, underpinned mostly by the fact that big money in troubled times moved to the most deep and liquid asset class, the U.S. dollar.

Despite its own problems of migration from the south, a stagnant economy and a very uncertain political future, the U.S. looks stable in comparison to events outside. But stable the U.S. isn't, certainly not economically.

In the U.S. and Europe, the fundamental nature of the economies is of financial repression. Their economies have stagnated and are increasingly negative yielding. Contrary to the expectations of many, emerging markets have failed to take a leadership position. They have failed to become creative and nurturers of the future growth of the planet. A large part of emerging marketsperhaps with the exclusion of Chinahave grown through merely consumption supported by debt, rather than by building more factories. These emerging markets are starting to stagnate and mostly revert back to their historical norm, negative yields. On top, their huge debts and consumption patterns have created massive systemic risks.

While many reasons are attributed to why people buy gold, the major reason is negative yields. Gold is a zero-yielding asset, hence better than negative-yielding assets. Gold has done very well in the last 16 years, and there is nothing on the horizon that shows a reversion in the negative-yielding economic environment. With periods of consolidation, gold's rise of this year should continue. When investors have accepted that the U.S. stock market has indeed stagnatedwhich has gone nowhere for the last one yearand when the property markets in cities like Vancouver have burst, all eyes will move to gold, setting in place what might become mania.

Now to investing. It has been the nature of the mining industry that investors tend to build in their valuation metal prices that are higheroften much higherthan spot prices. This corrupts valuation and diverts money into projects that are not yet (and perhaps never will be) economical. This enables promoters with polished presentations to positions of lifestyle. If nothing else, building higher metal prices in equity valuations results in giving away upside from metal price appreciation.

While gold has done quite well so far this year, mining companies have gone up far more than what could be justified by the increase in gold price. I offer two names that have either generated more value than their share price increase reflects or have gone unappreciated by the market.

Reservoir Minerals Inc. (RMC:TSX.V) is being acquired by Nevsun Resources Ltd. (NSU:TSX; NSU:NYSE.MKT). Despite being one of the most successful mining companies in the recent memory, Nevsun has suffered because of its jurisdiction, Eritrea. Owning Reservoir offers an arbitrage upside of a couple of extra percent and a small possibility that another bid might come for Reservoir. The merger of these two companies gives them the fuel to finance the Serbian project that Reservoir brings to the table. This will put Nevsun's cash pile to use. Nevsun's unused cash was being discounted in the market valuation, and Reservoir's lack of cash was seen as its shortcoming. With the merger, discounts from both sides should disappear. I prefer to buy Reservoir for extra icing on the cake, an arbitrage upside and a possibility of a better acquisition bid.

Callinex Mines Inc. (CNX:TSX.V; CLLXF:OTCQX) has done very well over the last two years. It has managed to raise money from significant investors including Resource Capital Funds, to fund ongoing exploration at its flagship Pine Bay project in Manitoba, where the company has recently discovered two new mineralized zones. If enough economic quantity of rock can be found, it can be very easily trucked to the facilities of Hudbay Minerals Inc. (HBM:TSX; HBM:NYSE), which needs new sources of ore. Callinex has also acquired three primary zinc projects in Canada, for insignificant cost to its treasury. There are very few juniors that offer significant exposure to zinc, particularly with a strong management team. I'm looking ahead to upcoming drilling programs and more acquisitionssupported by recently raised money.

Jayant Bhandari has been an Asia-based institutional investor adviser for the last three years. Prior to that he worked for six years with U.S. Global Investors in the United States, a boutique natural resource investment firm, and for one year with Casey Research. Prior to his involvement in the investment industry he established and managed Indian subsidiary operations of two European companies. He received his Master of Business Administration from Manchester Business School (UK) and holds a Bachelor of Engineering from SGSITS (India). He frequently writes on cultural, political and social issues for several publications.

Read what other experts are saying about:

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) The following companies mentioned in this article are sponsors of Streetwise Reports: Callinex Mines Inc. The companies mentioned in this article were not involved in any aspect of the article preparation. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

2) Jayant Bhandari: I or my family own shares of the following companies mentioned in this article: Callinex Mines Inc. and Reservoir Minerals Inc. I personally am or my family is paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Statement and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author determined which companies would be included in this article based on his research and understanding of the sector. Statement and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview or the time an article is accepted for publication until after it publishes.