The Gold Report: So far in 2016, the Dow Jones Industrial Average is down, oil is at near-decade lows and the Chinese stock markets continue to slide. How is that translating to your coverage universe? Should investors be worried?

Geordie Mark: It's certainly been a tough ride in the markets for many of the precious metals producers and development-stage companiesbut we see that as an opportunity. Precious metals have taken a good run in the New Year, which has certainly enabled production-related companies to bolster their operating margins through higher underlying commodity prices and lower fuel prices. While there are obviously tumultuous markets out there and some overriding geopolitical hotspots, we see this adding to the case for the risk-off trade moving toward gold, and underpinning some strength in the gold price. We see that as a glimmer of strength and opportunity for investors.

TGR: As of late January, China's Shanghai Index had fallen 47% since its peak in June. To date, ongoing economic weakness in China has had little impact on the gold price. Do you expect that to change?

GM: If we look at the relationship between the gold price over the last year or so and the Shanghai Index, we have seen some broadly defined and sporadic antithetic relationships, with gold picking up more recently in correlation with the equity indices coming down. But much more than China drives the risk-off trade toward gold. For instance, uncertainty is being exacerbated by vacillations in the reactions to the implications of the Federal Reserve's decision to raise interest rates and the likelihood of further monetary policy engagement in 2016. These factors alone are impacting U.S. dollar and commodity price volatility, but are embodied within a global monetary policy climate catering for faltering economies through the adoption of accommodative monetary practices resulting in inflation and domestic currency weakness that further separates the Fed's actions culminating in some semblance of relative strength for the US dollar.

"Asanko Gold Inc. should deliver free cash flow in 2017."

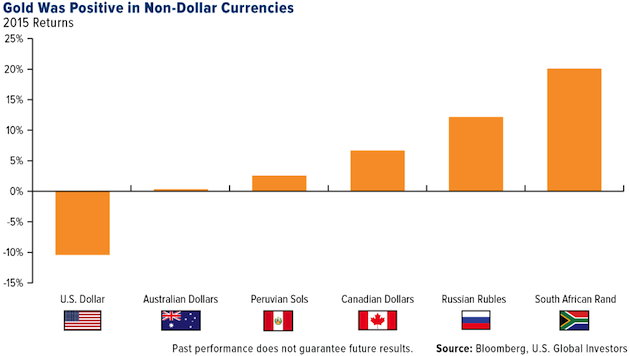

Within that context, gold has performed relatively well over the last 14 months when considered in other denominationsSouth African rand, Australian dollar, Canadian dollar and New Zealand dollar. Such commodity price action has aided operations domiciled in these regions to protect and/or expand their margins in addition to the benefits achieved through deflation in consumables costs (e.g., fuel, steel and reagents). There has been a favorable strength there. Issues in Europe and specific geopolitical hotspots are adding to individual worries on the financial outlook in various economies.

TGR: Do you expect the Chinese to turn toward more personal gold buying if their economy continues to soften?

GM: Perhaps, and encouragingly we note that Chinese gold consumption rose in December, maybe as a safe haven against the government's move to weaken the yuan. We are certainly seeing a recent bid there.

TGR: Do you see any other meaningful trends?

GM: Exchange-traded fund (ETF) gold balances have been on a downward path for several years. That reached a low in early 2016, but since then, we have seen ETF balances strengthen appreciably, which is a positive sign for underlying demand and refocus toward the commodity. Concurrent with EFT buying we are seeing the futures market showing long positions move up and short positions move radically down.

TGR: After being up 7.14% in 2012, gold has fallen each year since. So far this year, gold is on track to make gains of about 6% in 2016. Is that consistent with Haywood's projections?

GM: Right now, we project a $1,200/ounce ($1,200/oz) gold price going forward. We use a flat deck, ultimately, in order to differentiate more so on the relative quality of the assets and operational performance of mining companies versus implanting a potential bias based on commodity price inflections.

For the gold price, there's a far more interwoven tapestry where value is born from differentials on currency. We've certainly seen weakness in the Canadian dollar over the last 14 months and something similar for the Australian dollar, the New Zealand dollar and the South African rand. The weakness in those currencies has really enabled Canadian and Australian gold producers to lower their costs and foster margin expansion to outperform global markets, at least more recently.

TGR: Would you hazard a guess at what gold price would the funding taps turn on again?

GM: We're in an evolving picture of the injection of capital into equities and from where that capital originates. Some of it is from traditional sources like capital markets, funds and individuals. But we're also seeing significant injections from royalty and streaming companiesOsisko Gold Royalties Ltd. (OR:TSX), Sandstorm Gold Ltd. (SSL:TSX.V; SAND:NYSE.MKT), Royal Gold Inc. (RGL:TSX; RGLD:NASDAQ), Silver Wheaton Corp. (SLW:TSX; SLW:NYSE)to enable project development, bolster company balance sheets, and/or for exposure to exploration upside.

"Tahoe Resources Inc.'s Lake Shore Gold acquisition would seem perfectly timed as that company has matured its operations to deliver lower cost production that would augment Tahoe's production base."

We're seeing continued participation at the equity level from some of the midtier to larger producers. For example, Goldcorp Inc. (G:TSX; GG:NYSE) and OceanaGold Corp. (OGC:TSX; OGC:ASX) recently invested in two different tranches in Gold Standard Ventures Corp. (GSV:TSX.V; GSV:NYSE) and its properties in Nevada. We saw B2Gold Corp. (BTG:NYSE; BTO:TSX; B2G:NSX) entertaining the engagement in a range of joint ventures with partners. And some significant high net-worth individuals, such as Lukas Lundin and Ross Beaty, are coming into the space for somewhat contrarian, long-term equity investments. Lundin and Beaty each took significant equity positions in Kaminak Gold Corp. (KAM:TSX.V).

We are experiencing a very interesting period for gold where divergences in currency strength are locally fostering resurgence of domestic gold prices in absence of an appreciable move in the U.S. dollar-denominated gold price. These manifestations have occurred concurrently with a continued downward trend in input costs that have aided operating cost profiles for numerous operators (e.g., Detour Gold Corp. [DGC:TSX], Evolution Mining Ltd. [EVN:ASX], Richmont Mines Inc. [RIC:NYSE.MKT; RIC:TSX], Northern Star Resources Ltd. [NST:ASX]). Radical differences in currency strength are certainly aiding the margin, longevity and economic potential of operations and development-stage assets in the aforementioned countries, and we expect that most investment focus is likely to be drawn to assets in those regions, but contrarian investors with longer-term investment horizons will not be bound to any jurisdiction. Overall, of course, I think we'll get more and more interest in an increasing gold-price environment where we expect greater participation from generalist funds and the retail investor.

TGR: A recent report by Haywood said that few development projects are likely to be funded for production considering the assets available, prevailing metals prices and low equity valuations. What types of projects are likely to get funded?

GM: For development-stage projects, capital allocation is expected to focus on projects with the potential to deliver strong operating margins for modest capital deployment requirements. Facilitating operating margin potential involves the typical interplay of deposit morphology, grade, metallurgy, and projected operating costs that in themselves have to be considered in the context of initial and ongoing capital requirements. What's more, jurisdiction plays an important role in differentiating asset economics and development potential through its currency strength, clarity in asset ownership structure, fiscal regime transparency and permitting structure. Considering these facets, we are focusing on projects with structured and visible permitting and construction horizons that could enjoy good margins for the deployment of reasonable capital expenditures (capex) that can be funded through modest market participation.

TGR: Tell us about some of the development-stage gold equity stories that you're following that offer most of the elements you listed.

GM: Two of our favorite development-stage companies that take advantage of where the Canadian dollar is and lower oil prices are Atlantic Gold Corp. (AGB:TSX.V) (Buy, $0.55 Target Price [TP]) and Sabina Gold & Silver Corp. (SBB:TSX; RXC:FSE; SGSVF:OTCPK) (Buy, $1.00 TP).

Atlantic Gold's Moose River consolidated gold project is in Nova Scotia. It would be a modest-scale project that could furnish 79,000 oz (79 Koz) gold over a nine-year period. We note that the Touquoy plant and open-pit mine is permitted and ready for development pending the completion of funding requirements.

The company's second gold mine to be integrated into operation at the Moose River Consolidated project is Beaver Dam, which is currently undergoing permitting review, but is only forecast to come into production several years from now. Beaver Dam would feed the Touquoy plant on the cessation of mining at the adjacent Touquoy open-pit mine. The Moose River Consolidated project would be a modest-scale gold-producing asset that would take advantage of a relatively weak Canadian dollar and low consumables costs to drive home appreciable margin potential.

TGR: In a recent report, you wrote that Moose River would become a near-term producer. What time frame were you suggesting?

GM: Moose River could ultimately start development sometime in the next year or so, if the appropriate debt agreement came into place and it could win more capital support through the equity markets. If all goes well in development, first production could occur in early 2018.

TGR: What is the grade?

GM: Open-pit reserves for these two deposits average 1.44 grams per ton (1.44 g/t). In addition to these deposits, Atlantic Gold holds the Cochrane Hill and 15 Mile Stream deposits, grading 1.7 g/t and 1.6 g/t gold respectively, that collectively contain just over 1.1 million ounces (1.1 Moz) gold in resources. Our projection of a nine-year mine life considers the exploitation of only two of the four deposits held by the company. We're looking at a modest-scale project producing about 80 Koz per year at total cash costs of sub-$600/oz. The capital cost could be less than CA$170 million (CA$170M). So we believe the development potential of this project is very achievable.

TGR: Sabina Gold & Silver has the Back River gold project in Nunavut. Tell us about that.

GM: Sabina Gold & Silver has an outstanding resource and reserve base at Back River with 7.2 Moz gold defined in resources that locally crop out, and furnish an average grade north of 6 g/t. President and CEO Bruce McLeod recently came aboard and changed the scope and direction of the company by chiseling the feasibility study down to a modest-scale play. It would start at 1.1 million tons per annum with a modest capex, we estimate a conservative estimate of around CA$500M. Such a project could produce around 200 Koz/year for 12 years at total cash costs of about $680/oz. So herein we believe that the grade represents a great drawing card to support production scale and cost moderation. The project design shows a small-scale operation to start with, but we believe that could expand after commissioning so as to take advantage of the significant resource base endowment beyond the 2P reserves.

TGR: Is there a growth component?

GM: Even though Sabina has a solid 7 Moz gold resource as a cornerstone for further exploitation potential, the exploration team is not resting on its laurels and has come up with some novel approaches to target new styles of gold mineralization, which could add value to the near-term picture. Sabina is engaging in a $2M drilling program to show the camp-scale potential of the area, and as such this work only adds to our belief for the significant growth potential of the underlying resource base at Back River. We expect to see Sabina receive all its major permits and licenses later next year with a development decision possible thereafter.

TGR: What are some other companies that Haywood is following?

GM: Asanko Gold Inc. (AKG:NYSE.MKT; AKG:TSX) (Buy, $3.25 TP) was a developer in Ghana that has evolved into a producer with its first gold pour in late January. The company joins the ranks of other recent producers like Torex Gold Resources Inc. (TXG:TSX) and Guyana Goldfields Inc. (GUY:TSX). We believe that Asanko has delivered on capital cost estimates and reached production a month earlier than originally expected. The mill is already apparently running through stockpiled ore at designed capacity, and we believe that the company should enjoy more attention as the Asanko gold mine ramps up production.

TGR: Have things calmed down sufficiently in Ghana to suitably limit jurisdiction risk?

GM: I'm comfortable with Ghana's geopolitical risk. Numerous gold mines operate there, so there's a lot of history. I think Ghana is the third largest gold-producing country in Africa.

TGR: What's your estimated production for the year? When will it start to generate free cash flow?

GM: We are looking at 2016 production of about 197 Koz at cash costs of $610/oz and all-in sustaining costs just over $900/oz. After the company's ramp-up year, we are looking to the company to deliver free cash flow in 2017. We believe that there is a nearer-term objective to try and elevate mill throughput via the introduction of more oxide material. Such could be undertaken principally through the discovery of additional oxide ounces nearby, and we believe that Asanko is striving to deliver on such aims over the near term.

TGR: What's your investment thesis for producing companies?

GM: We're looking for a track record of delivering production on guidance. Outside of hedging, there are few aspects outside operations that you can control, so delivering on guidance represents an integral facet to understanding management's capacity to deliver and execute to plan. We're also looking for companies that show growth potential and, where appropriate over time, to give a bit back to shareholders through a dividend. I think having an eye to deliver on a dividend keeps management focused on controlling costs and delivery of the underlying free cash flow.

TGR: What are some companies that fit the bill?

GM: We like OceanaGold Corp. (OGC:TSX; OGC:ASX) (Buy, $4.00 TP). The company has delivered through the Didipio ramp-up in the Philippines, and now the plant consistently performs well in increasing throughput. The company is derisking its mine operation through building stockpile inventory. OceanaGold will go underground at Didipio next year, and it has optimized its underground development plan to bring forward ounces.

Meanwhile, OceanaGold is incrementally pushing back the remaining years at both Macraes and Reefton, but, also, through acquisitions, having only recently completed its acquisition of Waihi in New Zealand. It is now the only gold producer in that country. OceanaGold has taken advantage of the weakening New Zealand dollar, fuel prices and electricity prices to help it deliver on margin. Further to that, it has used its success through those acquisitions to buy Romarco Minerals Inc. for the Haile deposit in South Carolina. This ultimately is its next growth step, coming in early Q1/17. Oceana could produce north of 500 Koz of gold next year, with significant copper production, at all-in sustaining gold equivalent costs of $760/oz. We certainly like OceanaGold as a producer.

TGR: What is behind OceanaGold's investment in Gold Standard Ventures?

GM: OceanaGold likes the land package that Gold Standard Ventures has in Nevada. It is also looking at that longer-term picture, not necessarily any particular exploration project but, rather, the potential mineralization in the belt.

TGR: What are some other producers that tick all the boxes?

GM: We cover Tahoe Resources Inc. (TAHO:NYSE; THO:TSX) (Buy, $16.50 TP). It is underpinned by Escobal in Guatemala, which truly is one of the few large, low-cost silver assets out there. Any hallmark for long-term, midtier or large-tier companies is to have a world-class asset as a cornerstone to both furnish and stabilize future cash flow. That certainly typifies Escobal. Tahoe changed its focus somewhat through the acquisition of Rio Alto Mining Ltd. and subsuming gold production out of Peru with La Arena, and now Shahuindo. It certainly has shown some prudence by diversifying jurisdiction but also its commodity base, while adding some growth in production through that. Tahoe is very clear on what the company's goals are through growth and then delivering a dividend paid monthly. If you like where precious metals are going and you like margin underpinned by a world-class asset, Tahoe works really well.

TGR: How is Shahuindo shaping up?

GM: If you take a broader, longer-term picture, you have La Arena tapering down production over the next few years but Shahuindo will aim to pick that production up. A big telling point for Tahoe will be how Shahuindo ramps up its production over the next year. It's an open-pit, heap-leach, run-of-mine operation that will evolve to 36,000 tonnes per day crush and agglomeration operation over time. We estimate gold-equivalent production this year is coming in at just sub-550 Koz at equivalent cash costs of about $640/oz. Heap leaches can be tricky, but the management team is technically sound.

TGR: Tahoe just announced a business combination with Lake Shore Gold Corp. (LSG:TSX) (Buy, $1.75 TP). What is your take on this?

GM: The move by Tahoe is certainly consistent with CEO Kevin McArthur's aim to achieve growth by consolidation. The Lake Shore Gold acquisition would seem perfectly timed as that company has matured its operations to deliver lower cost production that would augment Tahoe's production base. Completion of the acquisition would add jurisdictional and asset diversification leading to an overall lower risk profile albeit at a modest level of dilution with Tahoe shareholders owning 74% of the pro-forma company.

TGR: In the Chinese zodiac in 2016, it's the Year of the Monkey. What will this year be known as in the mining space, at least in your view?

GM: It could be a year of opportunity and consolidation. It's a fantastic time to build mines given that input costs are relatively cheap, and access to quality technical teams is at its highest in a long time. So it's a great time for building and operating mines. Gold producers have radically dropped their all-in sustaining cash costs over the last 12 quarters. That's obviously a coincident change in operational behavior combined with cost restructuring (both passive and active). We believe that there will be change in commodity prices or input prices, as well as a change in staffing structure. We're going to see further operational prudence from producers over the near term. Further, we'll continue to see markets where investors focus on quality, margin and performance, but also look to seek additional exposure to leverage on gold price surges.

TGR: Thank you for your insights, Geordie.

Geordie Mark is the head of mining research at Haywood Securities. He was previously an analyst with Passport Capital. In an earlier period he was vice president of exploration for Cash Minerals. Prior to joining the exploration industry full-time, he lectured in economic geology at Monash University, Australia, and served as an industry consultant. He holds a Ph.D. in geology from James Cook University.

Read what other experts are saying about:

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Asanko Gold Inc., Tahoe Resources Inc., Gold Standard Ventures Corp., Guyana Goldfields Inc. and Silver Wheaton Corp. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Geordie Mark: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Asanko Gold Inc. (AKG:TSX) and Tahoe Resources Inc. (THO:TSX). I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.