The Life Sciences Report: The biotech sector is currently experiencing great market volatility. Does this volatility create a temporary opportunity for careful investors to get in at lower prices, or is it a longer-term change in market direction?

VB: I think it's a temporary drop affording smart investors an opportunity to get into the sector at lower prices. We have clients doing homework all the time in the biotech space, so they have their lists. They see a lot of choices and they are looking for more attractive valuations.

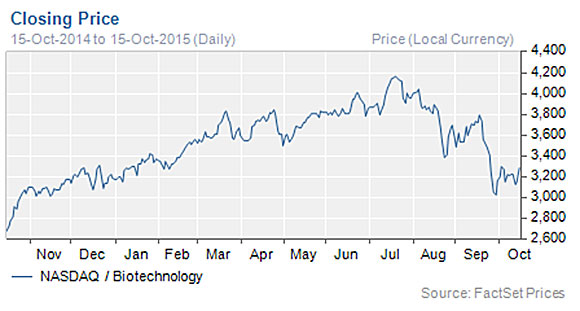

"This temporary drop affords smart investors an opportunity to get into the biotech sector at lower prices."

Biotech stocks ran up a lot this year because of their potential value, which results from innovation and the clinical stages of their product candidates. Many of these technological advances can be used as drug discovery engines, and only became practical in the last five years. Some advancements have already generated drug candidates moving into Phase 2 clinical trials.

With the market pullback, biotech valuations are returning to early 2015 levels, as the NASDAQ Biotechnology Index (NBI) and the NYSE ARCA Biotech Index (BTK) show. Biotechnology stocks had run up 50% year-over-year and are now flat year to date. We think, overall, this makes it a good time to buy.

TLSR: As a sellside analyst, what are you looking for when evaluating life science companies?

VB: At FBR, we leverage our medical, scientific and industry backgrounds to find innovative companies with practical and business-minded strategies. I look at companies with an eyeglass for innovation that can be advanced at a cost that results in operational profit. Even though a cure might help large numbers of people, I always couple development costs with the cost of therapy to evaluate corporate and shareholder value.

TLSR: What are some of the common mistakes that biotech investors make, and how can they be avoided?

VB: Just because there's momentum in a stock, that doesn't mean it's time to buy. The stock may be a long-term investment opportunity, but the valuation may have grown too quickly. Looking at the current market pullback, a lot of stocks are now at cheaper prices. We try to point investors toward stocks with greater opportunities.

TLSR: With your primary focus on inflammation, gene therapy and infectious diseases, what companies stand out as potential winners?

VB: Long-term inflammation is the immune system gone awry. By targeting inflammation, we are developing approaches for treating conditions such as inflammatory bowel diseases, multiple sclerosis and asthma. In this space, we like Immune Pharmaceuticals Inc. (IMNP:NASDAQ), which is developing bertilimumab and is in Phase 2 clinical trials. Bertilimumab targets eotaxin-1, a cytokine found at high levels in people with chronic inflammation and elevated levels of eosinophils. One target indication for bertilimumab is nonalcoholic steatohepatitis (NASH), a condition developing from chronic fatty liver disease. Initiation of Phase 2 clinical trials in that indication is pending.

Fatty liver disease is an inflammatory condition resulting from long-term chronic exposure to fat. Statistics show that one-third of the U.S. population is obese. Furthermore, one-third of the obese population is likely to develop fatty liver disease. One-third of those people with fatty liver disease are likely to develop NASH, with another third advancing to various stages of NASH-related morbidities. Some patients will require a liver transplant. Due to liver availability, only about 6,000 (6K) transplant procedures are performed each year, suggesting a very large market for therapeutic intervention of NASH.

"There are ramifications to high pricing, but to prohibit access through price control is not going to happen."

Also in this space, Intercept Pharmaceuticals Inc. (ICPT:NASDAQ) recently announced initiation of a Phase 3 clinical trial for obeticholic acid (OCA), a drug already in front of the FDA for treating primary biliary cirrhosis (PBC).

In the gene therapy space, Abeona Therapeutics Inc. (ABEO:NASDAQ) is using CRISPR (clustered regularly interspaced short palindromic repeats) gene-editing technology to replace a damaged part of a gene with a correct sequence. Using an adenovirus 9 (AAV9) vector, Abeona is working to treat rare diseases.

The government is interested in advancing therapies for severe illnesses such as Ebola, where there is minimal current therapeutic standard of care. In this space, I like Novavax Inc. (NVAX:NASDAQ), which has an Ebola vaccine in the works. Without government assistance, Novavax is advancing viruslike particle technology to create novel vaccines capable of eliciting better immune responses to respiratory syncytial virus (RSV). This therapy may prove more efficacious than the current therapy, Synagis (palivizumab; MedImmune/AstraZeneca Plc [AZN:NYSE]).

TLSR: Immune Pharmaceuticals is also developing nanoparticle therapeutics. Can you please tell us about that program?

VB: This technology falls under the umbrella of antibody drug conjugates, an antibody attached to a drug payload. In the case of Immune Pharmaceuticals, an antibody of its design is attached to paclitaxel or some other currently validated chemotherapeutic drug. The antibody serves to direct the therapeutic to a specific target, much like a guided missile as opposed to a spray of shotgun pellets. The company's nanoparticle program is essentially monoclonal antibodies attached to a nanoparticle core (NanomAbs). This program still needs to get off the ground. It is currently not valued in our models, but should be a future value driver for the company.

TLSR: You mentioned Intercept Pharmaceuticals and Immune Pharmaceuticals as contenders in the NASH space. When do you expect to see an approved therapeutic for this unmet medical need?

VB: There are currently no regulatory pathways for approval of NASH therapeutics. Intercept is the first horse out of the gate and will likely pave the way for regulatory guidelines. The FDA has indicated what would be called approvable biomarkers, but the way to show a patient is improving is through a liver biopsy. This is problematic because of safety concerns, coupled with the biopsy sampling only about 1/50,000 of the liver tissue. With Phase 3 clinical trials a few years out, Intercept is taking the chance that the regulatory pathway will evolve to recognize its recommended achievable endpoints as appropriate for approval. I think Intercept will get there first, and hopefully it's chosen the right endpoints.

TLSR: What is the market potential for a successful NASH therapeutic?

VB: This is a hard number to determine right now. A competitor recently did a valuation of the NASH landscape and came up with a $40 billion ($40B) market potential. If you start with the third of the U.S. population being obese, and estimate that a third of those people will develop fatty liver disease, that's 30M people. Projecting one third of those with fatty liver disease will advance to NASH, we're talking about a market of approximately 10M people. If the NASH therapy costs $20Karguably cheap as far as therapies gowe are talking about a $20B market.

"In the future, I think companies will need to do pharmacoeconomic analyses to justify high prices for drugs."

However, many of these therapies will likely be priced higher than $20K, because the only treatment for a liver that goes through cirrhosis and ends up in failure is an organ transplant. Comparing the $500K costs for a liver transplant to the projected $20K cost for a NASH treatment, the economics are quite favorable. This is even more significant when you consider that many patients with advanced NASH will die without a transplant. No price can be placed on life.

TLSR: The pharmaceutical industry as a whole has recently received a lot of criticism over pricing. How might this affect Intercept?

VB: I hate to belabor one company, and I like its drug. In Intercept's case, OCA is currently before the FDA in PBC, an indication with a small patient population. With that small patient population, the company can price its drug close to those used to treat rare or orphan diseases. Such pricing is typically high, with companies targeting orphan indications charging anywhere from $300K to $600K a year.

Should OCA get approved only for an advanced stage of NASH, with a patient population of approximately one third of the estimated 10M NASH patients, charging $20K per year makes OCA a multibillion-dollar drug. At the same time, if you already priced OCA for an orphan indication, pricing is likely to be much higher than $20K. The dilemma is, what price do you actually place on this drug? Pricing policies have huge implications as far as corporate strategies are concerned.

"I always couple development costs with the cost of therapy to evaluate corporate and shareholder value."

Not a lot of companies do what is called a pharmacoeconomic benefit study. Such studies provide insight on the cost of treating a disease with and without use of a therapeutic agent. Cytokinetics Inc. (CYTK:NASDAQ), my Top Pick under coverage, has a small molecule drug in development for heart failure. This drug, omecamtiv mecarbil, is intended to improve the heart's function. In the case of chronic heart failure, patients get released from the hospital and eventually come back because no available heart failure drug treats the underlying cause of the disease. If the Cytokinetics drug reduces hospital readmissions, the cost of the drug can be justified based on the pharmacoeconomic benefit of the therapy. In the future, I think companies will need to do such analyses to justify high prices for drugs.

TLSR: We have discussed macromolecular-type drugs and small molecules. If you look broadly at the two drug classes, where do you see the most promise for patients?

VB: I think the innovation will most rapidly continue in the large molecule space because of growing overlap in the patent landscape covering small molecules. To work in much of the small molecule space, you have to wait for some of the intellectual property to expire, which will allow use of some novel side groups that can make a molecule more efficacious. In any regard, we think that the most rapid innovation is occurring in the large molecule arena and includes RNAi, biologics and cell therapies.

TLSR: Are there any additional areas that you'd like to comment on today?

VB: I constantly get asked about market pullbacks, buying opportunities, and whether I believe we're in the beginning or end of the golden age of biotech. I believe that we're still in the golden age of biotech. Specifically, we're in the next wave.

While I don't cover them, the large-cap biotechs, in my opinion, are the first wave of companies whose innovations created this industry. We're now emerging into an era of novel technologies and approaches to treating diseases. Some small-cap companies have been able to target diseases for which there were no therapies because the market potential was too small for a large-cap biotech or a large-cap pharmaceutical company.

With innovation, you can develop therapies for small patient populationsof course, in balance with the drug pricing issue. I think that eventually innovation will win out, and the market, not politicians, will determine the price of drugs. People want access to medicine. There are ramifications to high pricing, but to prohibit access through price control is not going to happen. Even if only through voting, patients will ultimately drive drug pricing.

TLSR: Thanks for your time, Vernon.

Vernon Bernardino is an analyst in FBR & Co.'s life sciences equity research department. His principal focus is on biotechnology, biopharmaceutical, specialty pharmaceutical and immunotherapy companies that focus on treatment of cancer, infectious diseases and cell-based therapies targeting inflammatory disorders and vascular diseases. Bernardino brings more than 10 years of experience covering life sciences companies at various financial institutions, including Rodman & Renshaw, UBS and Dawson James. Earlier in his career, Bernardino was a buyside analyst at Nicholas Applegate Capital Management, and founded the strategic advisory group Oceros Advisors LP. Bernardino holds a bachelor's degree from Rutgers University and a master's degree in business administration (finance) from the University of San Diego.

Want to read more Life Sciences Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Daniel Levy conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: None. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Vernon Bernardino: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.