The Energy Report: Steven, is the price of oil nearing the point where North American exploration and production companies (E&Ps) will have to curtail production?

Steven Salz: Yes. We're already starting to see hints of a pullback in drilling activity, with the Baker Hughes Inc. (BHI:NYSE) rig count showing a slight decline on a forward basis. In the Q3/14 earnings of major E&Ps, we saw language suggesting more modest plans for 2015 than previously anticipated. We're expecting around a 10%-20% drop off previous expectations in capex for 2015. That translates into a near equivalent drop in the well count year over year (YOY), which has a direct impact on the energy service space.

"Enterprise Group Inc. has seen a doubling in revenue YOY."

If oil prices continue to decline, or even hold steady at $6570 per barrel ($6570/bbl), it's going to be important for investors to position themselves with companies exposed to basins that have low breakeven oil prices per barrel.

TER: Do you think the Baker Hughes/Halliburton Co. (HAL:NYSE) deal is partially a result of this fall in price?

SS: I do. Thoughts on that deal originally fell into two polarized camps. Some thought maybe this was a bottom, and we were going to see a recovery. That's the immediate reaction when investors see deals with such large majors. But I thoughtand we now seethe deal was more about Baker Hughes thinking that tougher times were ahead, and Halliburton wanting to be opportunistic. That's consistent with the recent moves in oil prices. When you have a massive drop in the commodity price, it's expected that companies with a comfortable balance sheet are going to be opportunistic.

TER: Are unconventional and conventional E&Ps equally affected by this price situation?

SS: You would get hurt more on the unconventional side. Both have their advantages, with conventional arguably being lower beta in a falling oil price environment because there's typically a lower cost of production, thus a lower breakeven price per barrel. It's going to depend on which plays you're exposed to. Generally though, unconventional, on average, would need more capital to sustain production given higher costs and quicker declines.

TER: Natural gas prices have been stable and are actually rising again. Is this causing E&Ps to shift their focus to gas production now?

SS: Not at a level that has become apparent. These things have a lagging effect. Oil's really only come off the past few months, so you wouldn't see any material shift in the production profile over less than a quarter's time of decline. We're not seeing a shift yet, but it's possible.

TER: Has the price of natural gas liquids (NGLs) tracked the fall in oil prices?

SS: We are seeing some price compression in NGLs. Crude oil prices impact the price ceilings for propane and butane because they compete with oil-based products, like heating oil and gas oil. That being said, the move has not been as volatile or significant, and that's due to the fact that NGLs don't have the same export restrictions in the U.S. as crude oil exports.

TER: Does that mean dry gas is becoming more highly valued now than it was?

SS: It does. Dry gas wells have a lower cost of production than wet gas. In an environment where the oil price is low, there is compression in NGLs, which reduces the wet gas well netbacks because it can be sold at lower prices. The cost of production is the same, so you get a compressed netback. With stable natural gas prices, or an increase in natural gas prices, you get deeper value in a dry gas play.

TER: How are oilfield services companies responding to the price situation in oil and gas?

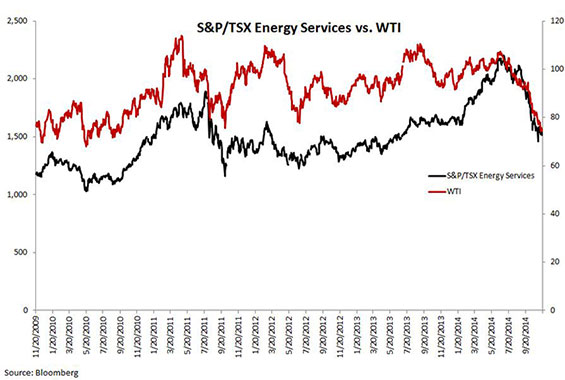

SS: Many have sold off. Energy service companies are impacted by E&P capex. When the oil price falls and capital programs are at risk to be cut or moderated, the pie gets smaller for service companies to fight over. Declines vary by subsector within the energy service space: Drillers and pumpers get hit a bit harder. Those are down 3545% year-to-date. Field service and infrastructure companies are down 1525% year-to-date. I'd say the latter would be considered more maintenance and sustaining services versus exploration spend for the drillers and pumpers.

If you're an energy company facing lower oil prices, you're going to cut new production; you're going to cut your capex programs on new exploration and new projects. You'd rather deploy capital into maximizing existing resources and existing wells. That results in more pain for the exploration service companies, versus companies working in maintenance and sustaining.

TER: How is the situation affecting the companies you cover?

SS: Among the companies we cover, Northern Frontier Corp. (FFF:TSX.V) is more on the maintenance and sustaining sidethat generates almost all of the company's revenue. It has sold off a bit more than the sector due to a recent lengthy financing process, but generally Northern Frontier is more insulated in the current environment and should begin to trade as such.

On the other side, there's Xtreme Coil Drilling Corp. (XDC:TSX), a drilling and coil operator. This company has been hit quite hard. It was up 3040% year-to-date in August, and once oil rolled over, Xtreme sold off, now down about 60% year-to-date. The impact and effect was almost immediate on that side.

"Input Capital Corp. has already demonstrated its ability to deploy capital and sell canola."

Enterprise Group Inc. (E:TSX.V) is right in the middle. This company provides mostly maintenance and sustaining services, so it has been insulated. On the other side of the coin, the market looks at Enterprise as having liquefied natural gas (LNG) exposure, so it's been stuck with that volatility. In an environment where LNG didn't exist, you'd probably see Enterprise bucking the trend right now. But because people feel it is a highly levered LNG play, despite the fact that it has no exposure, the company is getting hit disproportionately.

TER: How is the softening of the LNG market affecting these companies? How are they responding to it?

SS: The only name we cover with any exposure would be Enterprise, although LNG is pure upside to the company. Enterprise now has operating bases in both Fort St. John and Pouce Coupe in British Columbia (B.C.), the heart of LNG, following its recent acquisition of Westar Oilfield Rentals Inc. If LNG does not go through, current activity levels will not change. If LNG is not a reality for Canada until 2020 or 2025, you're not going to see any material impact to Enterprise. None of its current activity is a function of LNG.

TER: Enterprise Group's acquisitions appear to be quite varied. Is there a common theme?

SS: The company is divided into two major bucketsUtility/Infrastructure Construction Services and the Equipment Rentals group. In Utility/Infrastructure services, the company has Calgary Tunnelling & Horizontal Augering and T.C. Backhoe & Directional Drilling L.P. In Equipment Rentals, it has Hart Oilfield Rentals, Artic Therm International Ltd. and now the Westar acquisition. You find commonalities within the two buckets. On a higher level, the common theme would be western Canada-focused companies that offer utilities/energy services to a blue-chip client base.

TER: What does Enterprise look for in an acquisition?

SS: Enterprise looks for specialized companies with a western Canada focus and substantial existing management expertise. It typically leaves management teams in place post-acquisition, and often signs a management agreement. Enterprise will also look for a demonstrated track record of organic growth, and over time, as it builds up its two business segments, it will start looking for complementary businesses. The company wants to see businesses that are tuck-in acquisitions, where it can cross-sell and leverage locations to build into new geographies. I think Westar, which the company closed on in October, is the first receipt of this new breed of acquisition for Enterprise.

TER: How is Enterprise benefitting from the acquisitions it has recently made?

SS: Enterprise has seen a doubling in revenue YOY. There is a substantial increase in its blue-chip client base, which investors want to see. Whether in a downturn in oil prices or just in a general commodity price environment in western Canada, you want to be with blue-chip companies that can weather the storm and aren't going to cut down work too much. We're also seeing an increased geographic presence across Alberta and B.C.

On top of that, there is the beginning of increased vertical integration. The company has the ability now to package three rental groupsArtic Therm, Hart and Westartogether to better service and expand its client base, and do the same on the utility side, with Calgary Tunnelling and T.C. Backhoe. The subsidiaries can leverage one another to strengthen the value proposition.

"If oil prices continue to decline, it's going to be important for investors to position themselves with companies exposed to basins that have low breakeven oil prices per barrel."

As soon as it closed on Westar, the company said it would deploy $3 million ($3M) to expand its equipment fleet as a function of the demand it was already seeing from clients of Hart, which does similar work to Westar. What that said to us is Enterprise has made a very forward-looking acquisition, knowing full well that with Westar it would get new work with a new client base as a function of Westar's existing clients and its existing subsidiaries. That's exactly what you want. You want to be able to pick up companies where you know there's going to be an immediate demand for services from existing clientele. A great way to integrate new acquisitions is with tuck-in acquisitions that are accretive.

TER: How is Enterprise managing this growing stable?

SS: If you rewind a year, the company had just acquired Calgary Tunnelling. It hadn't even picked up Hart or Westar, which were acquired in January and October of this year, respectively. We're only beginning to see the company's ability to manage the diversity of the companies it now has under its umbrella.

We know that Enterprise is expanding its fleet to meet substantial demand, but following Q3/14, which the company reported on Nov. 12, the market has tempered its expectations as to how quickly that will occur. We reduced our target price from $1.50/share to $1.10 in response to a reduced margin profile, which is a function of managing its many subsidiaries' equipment fleets. The company has a variety of equipment spread across Alberta and B.C. right now. I think the market had anticipated a quicker ramp-up and quicker margin accretion than was feasible on the ground.

In Q3/14, we got EBITDA (earnings before interest, taxes, depreciation and amortization) margins of about 24%. The market was looking for 3031%. The difference was the result of an extensive use of third-party equipment in the quarter. What that showed us is that the company has the capacity, with all its acquisitions, to service the client base, but that it just wasn't there in terms of leveraging that capacity effectively to meet the demand. It had to rent equipment from a third party, and then rent it out again to meet demand. Enterprise is managing acquisitions, but I think the market has rightfully tempered its expectations.

TER: Your $6/share target for Xtreme Drilling looks like a moon shot given its decline since the summer. How do you justify your Buy rating?

SS: In July, the stock was well above $5. Now we're talking about $2/share, with the only fundamental change at the company level being higher day rates on its coil units and an up-and-running, two-rig Indian program, both of which are positive events. I think this shows just how levered driller names are to the oil price.

Our Buy rating is still justified by a few things. The company has just over 7,000 contracted days on its XDR rigs, representing revenue of about CA$225235M. That's 75% of 2015 contracted days already locked in, which provides a lot of cash flow certaintymuch more than Canadian drillers can say for themselves. In Canada, Xtreme is going to get hit a little harder simply as a function of the fact that the seasonality is very different, with spring break-up, and the fact that the company operates on a well-to-well contract versus long-term contracts, which Xtreme can achieve in the U.S.

"When you have a massive drop in the commodity price, it's expected that companies with a comfortable balance sheet are going to be opportunistic."

Also, a foundational component of Xtreme is its coil unit business. It's seeing day rates actually increase as oil prices decline. Producers are increasingly cognizant that they need to optimize well productivity and achieve the netbacks to stay profitable in a declining oil price. Xtreme has consistently demonstrated that its coil is the most efficient, and its rates are competitive. Recent rig data shows that Xtreme's U.S. fleet drilled the most footage per month per rig in the U.S. It was at almost two times the average. That substantial efficiency increases profitability for the producer. Should there be long-term concern on rigs the company has in more exposed basins, Xtreme has noted it has optionality to move rigs to India and other international markets, where the company garners more premium day rates.

When oil comes off, usually the shallow-depth rigs get hit first. That class of rigs has been more commoditized, and they're more replaceable. Xtreme has only a couple of shallow-depth rigs in its fleet, which we expect will get hit as oil prices come off. Those are the ones that it can easily move internationally.

TER: Northern Frontier acquisition plans are pretty ambitious in all three of its service areas. What are your expectations for this company?

SS: For Northern Frontier we're looking for some near-term calm. The company has a buy-and-build strategy, but at this oil price and the way the stock has traded, we and management both are looking for execution. A couple of months ago, when it was going for its most recent acquisitionof Central Water & Equipment Services Ltd.the first financing, a wholly debt financing, had to be terminated. Then Northern Frontier came out with a second round. The company ended up utilizing a combination of debt, equity and stock. The equity came in at a little more than what the market anticipated, so it ended up being a dilutive transaction. Subsequent to that, the stock price did fall off a bit.

The deal was priced at $2.15/share. The stock is at $0.60/share now. This is a function of the financing mechanics. Q2/14 was also reported well below expectations, as a function of the weather in the area where it operated, primarily in the Fort McMurray area of Alberta. Then a perfect storm hit, with declining oil prices taking the stock down from the deal price of $2.15/share.

People feel burned, and the company knows that it needs to execute now, and prove out the businesses to a point where it can carry out further transactions. We believe that, over time, Northern Frontier will execute and meet our expectations, and as we mentioned earlier, a focus on maintenance and sustaining services should insulate the name within the current oil price environment.

TER: What effect will the Halliburton/Baker Hughes deal have on these companies, if it goes through?

SS: Baker Hughes and Halliburton have minimal presence in Canada. Northern Frontier and Enterprise Group will not feel the impact of their operations. However, Xtreme, which primarily operates in the U.S., could. It's important to say at the outset that Xtreme already works for both Baker Hughes and Halliburton. The company recently deployed two rigs to India; those are actually working through Halliburton.

"In these selloffs, it becomes extremely important to position in the right basins."

Xtreme has a stronger relationship with Halliburton's groups than with Baker Hughes. In the event of an acquisition closing between those two parties, should the project management groups consolidate and the right people from Halliburton step into the roles of the combined entitywhich we see as highly likely given that Halliburton's group is substantially larger, is more effective, and has a much greater scope, not to mention that Halliburton is acquiring Bakerthat would bode well for Xtreme in terms of the amount of work that it is awarded. Either way, Xtreme's work through Baker and Halliburton is not substantial. Any material change would be incremental.

TER: Let's move on to something entirely different. Can you tell us about another company you have under coverage in a different sector?

SS: Yes. We cover Input Capital Corp. (INP:TSX.V), the first and currently only agricultural streaming company in the world.

TER: Your target price of $5 per share for Input sets the bar pretty high for a stock that has been nowhere near that for the last year. But your Buy rating indicates your faith in the company. Can you explain your thinking on that?

SS: For the investor community and analyst, it's the first time we've ever had to determine the potential of a company like this. We see Input as a classic take on textbook compounding of capital. The company deploys capital into canola contracts at a 20% internal rate of return (IRR). It receives cash on the sale of canola on those contracts as early as a few months later, then redeploys that cash into new contracts, and so on. Input has already demonstrated its ability to deploy capital and sell canola. Should it continue at pace, we think the compounding potentialjust the organic cash deployment, let alone further equity raisesshould catalyze the stock and justify our $5 target price and Buy rating.

TER: The company was exposed to falling canola prices. Are you concerned about that?

SS: I'm not concerned that the canola price has come off. Our valuation is slightly different from other analysts. We value the company not just on a forward cash flow basis, but also on a net asset value (NAV). The reason is the company contracts on a six-year basis, and just has to achieve an average $400425 per metric ton canola price to get the IRRs it's looking for. On top of that, Input, on average, has been selling its canola at an 11.2% premium to spot. That's a function of its effective marketing program.

The company also has significant cash on the balance sheet, which allows it to shift the sale of canola in and out of quarters to more favorably approach the market. Additionally, in a weaker canola price environment, the company can actually lock in lower all-in costs per metric ton on its contracts. It can then have an IRR of 20% at, say, $380/metric ton canola versus the $425/metric ton that it was locking into at a higher canola price. There's a lot of flexibility.

The model is fluid. The company is very insulated, and the market needs to be thinking about this over a six-year timeline, not in terms of a two- to three-month move in the canola price. We're not concerned.

TER: Are you anticipating a new wave of mergers and acquisitions in energy?

SS: I can only speak to what we can see in services. Again, when a sector collapses under commodity price pressure, it's expected that companies with comfortable balance sheets will be opportunistic, and that's what we saw with Halliburton. You could start to see a ripple as Halliburton, because of antitrust concerns, may have to shed and divest up to 7.5% in revenue. We're looking to see what happens with Halliburton, what the divested shares are going to look like, and who will target those. People are going to look for opportunities there. Buyers with cash are seeing the cheapest valuations in years.

The entire services sector has massively sold off. People are going to get squeezed. The million-dollar question right now is: Who's next? You do get industry consolidation when oil prices come off and the survival-of-the-fittest mentality comes in.

Everyone's speculating, from the top down, about which majors will consolidate next, who's looking to pick up tuck-ins, which companies are most exposed to the downswing, and who's going to need to sell themselves or divest noncore assets. We already saw that with Precision Drilling Corp., which divested its coil tubing assets earlier this month.

It's only been a few months of weak oil prices, but we're already seeing some companies looking for an exit opportunity. I think Halliburton sets a precedent, and now we must wait to see what the windfall is.

TER: What are you anticipating for the oil price next year?

SS: The Organization of the Petroleum Exporting Countries (OPEC) decision on Nov. 27 should not have surprised anyone. There was no political incentive for OPEC to cut its own production to support the U.S. I think we're going to see $5565/bbl for a little while as a result. The market seems pretty comfortable with that level.

TER: Any final thoughts? Is this a good time to get into the services?

SS: What investors want to do now is have the right names on their radars. In these selloffs, it becomes extremely important to position in the right basins. That's the only way to survive a turbulent energy market. For us there are core areasthe Bakken, the Eagle Ford, Niobrarathat are consistently rated best for returns in capital spend.

Beyond basin positioning, it's a matter of holding companies with right technology and efficiency. That's going to come increasingly into focus as operators need to put great emphasis on cost per barrel. We look to Xtreme Drilling as a name that fits that criteriaa defensive driller you could sayand that's why we picked up coverage on it in the first place.

Generally, in the services space, I think there's going to be significant near-term volatility. Services are high-beta names and highly correlated to the oil price. Stepping in now could be like catching a falling knife until the dust settles in oil prices. We are cautious until a base builds.

TER: Steven, thank you very much for your time today.

Steven Salz is an event-driven and special situations analyst at M Partners. Before joining M Partners he worked in a generalist equity research role at a major Canadian bank, in its internal retail asset management group. Prior to that Salz worked as a private Canadian defense contractor, and has held a variety of roles at major Canadian banks since 2010. Salz has a bachelor's degree from the University of Western Ontario.

Steven Salz is an event-driven and special situations analyst at M Partners. Before joining M Partners he worked in a generalist equity research role at a major Canadian bank, in its internal retail asset management group. Prior to that Salz worked as a private Canadian defense contractor, and has held a variety of roles at major Canadian banks since 2010. Salz has a bachelor's degree from the University of Western Ontario.

Read what other experts are saying about:

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Tom Armistead conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Enterprise Group Inc. and Input Capital Corp. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Steven Salz: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Northern Frontier Corp., Enterprise Group Inc. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.