The Gold Report: Your hyperinflation report predicted 2014 would be dominated by economic distress, financial crisis and panics. Were you surprised by the performance of the economy this year?

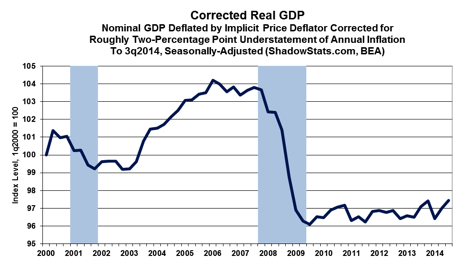

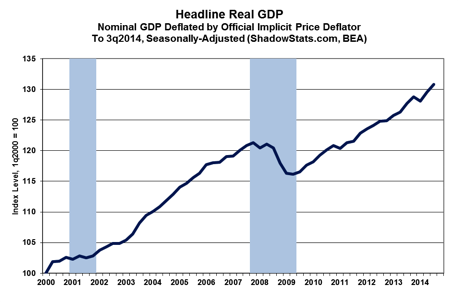

John Williams: No, at least not in terms of the actual performance. We're getting some fantasy numbers, which I'll be glad to address. The economic distress continued. If we look at the consumer conditions, generally median household income has continued to be stagnant at a low level of activity, below where it was in 1967 as adjusted by the Consumer Price Index (CPI). Even though the gross domestic product (GDP) supposedly rebounded in mid-2009it's 7% above where it was before the recession started in 2007there's very little that confirms that.

If the individual consumer is not out there buying, we don't have good activity in the bulk of the U.S. economy. Over 70% of the GDP is tied to personal consumption expenditures, and another couple of percent on top of that is tied to residential investment. If we don't have positive inflation-adjusted growth in incomeI'm talking actual household incomewe can't possibly have an economy that will grow faster than income growth, other than for a temporary boost from credit expansion, and that is not happening.

Credit growth is very limited for the consumer. If we look at consumer credit outstanding, although those numbers have gained since the panic of 2008, all the growth there has been in federally owned student loans, not in the type of consumer loans that would usually go into buying washers and dryers and such. Basically, the consumer's liquidity has been constrained. We are also seeing consumer confidence and sentiment numbers that are typical of a recession, not an economic boom. We have a lack of income growth, a lack of adequate credit availability and, generally, a low level of confidence.

Consider that GDP growth in Q3/14 adjusted for inflation was an annualized 3.9%, and 4.6% in Q2/14. That's two back-to-back quarters of roughly four percentage points. This is the strongest economy in over a decade if you believe the government's statistics, yet I'll challenge you to find someone who thinks that this is that good of an economy. It's just not there. There may be pockets of strength in Silicon Valley or such, but the average homeowner and the average consumer are not seeing it.

TGR: If there are all of these negative signs going on, why are the GDP numbers so high?JW: When Lyndon Johnson was president, he would get to review the GDP numbers every quarter. If he didn't like them, he'd send them back to the Commerce Department and keep sending them back until the Commerce Department gave him what he wanted. We don't have anything quite that overt happening now, but the government understates inflation. The problem is if you use too low a rate of inflation when adjusting economic numbers for inflation, that tends to overstate economic growth. When there is a roughly 2% annual understatement of GDP inflation, it means that GDP is basically overstated by two percentage points. When we look at the current number, 4% annualized GDP growth, we're seeing year-to-year growth of 2.4%. So if we take 2% out of that, you're seeing 0.4% growth. That's negligible.

As far as what happened in 2014, the economic data do not surprise me that much, because there are always problems with how it is reported. The ongoing problems with the economy continued. We did see a couple of flutters in the stock market. What did surprise me was the strength of the dollar. That's where the risks run for the immediate future, particularly into 2015.

The dollar is unusually strong, the strongest it's been in some time. If we look at the factors that drive it, the dollar is very vulnerable. Right now, our economy purportedly is booming, and the rest of the world is in recession. So that, on the surface, would tend to result in a strong dollar. I'll contend, though, that our economic growth is not real. The numbers will weaken. Retail sales and industrial production actually have much higher credibility than the GDP in that we'll see indications there of renewed recession. We've already seen a sharp slowing so far in the data for Q4/14.

TGR: How, in your view, did quantitative easing (QE) and tapering impact the dollar?

JW: QE was a fraud in how it was put forth. The idea here is that the Federal Reserve was doing this to help the economy. But even as he was expanding QE, Fed Chairman Ben Bernanke explicitly expressed that there is very little the Fed can do to stimulate the economy at this point. The systemic financial panic of 2008 brought the financial system, particularly the banking system, to the brink of collapse. That's where it was headed. The Fed and the Treasury did whatever they had to do to prevent total collapse. They created whatever money they had to create. They lent whatever money they had to; they spent it; they bailed out whatever firms they had to; they guaranteed all deposits.

When QE was introduced, the Fed flooded the banking system with cash. Normally, banks would take that money and put it into circulation. If they let it go into the normal flow of commerce, we would have had things pick up in lending, and that would have helped turn the economy around. That didn't happen. What the banks did was deposit the funds back into the Federal Reserve as excess reserves in the monetary base. It didn't help businesses at all. This policy was designed to help banking. That's the Fed's primary function in life, to keep the banking system afloat.

Because of what happened during 2008, it wasn't really a good idea politically to say, "Hey, we're still bailing out the banking system." So the Fed cloaked this policy as an attempt to stimulate the economy. And as the economy remained weak, it would use the weak economy as political cover for increasing the QE. It was helping the banks, but it did nothing to help the domestic economy other than by preventing a complete collapse of the financial system.

TGR: Is that why it didn't have the effect on the dollar that everyone was predicting?

JW: It did have an effect on the dollar early on. Whenever there was a rumor that the Fed was going to have to ease more, the dollar would take a hit and gold would rally. When tapering was indicated, the dollar would rally and gold would sink. There was a very direct relationship there.

Some months back, the economic numbers all of a sudden started to take off in a manner not seen in a decade, not supported by any underlying fundamentals. Then the Fed said it would cut back on its tapering and eliminate its purchases of new Treasury securities, which was seen as a positive for the dollar because it meant the Fed was going to shy away from further, open debasement of the dollar.

But here's where the risk comes: The U.S. economy has not recovered. It's still in trouble. The numbers, as we move forward into 2015, are going to get much weaker. That's going to, again, increase the speculation of a QE4. That will all be very negative for the dollar and very positive for gold.

Relative government stability is another big factor in a currency's value. Over the last year, we've seen the domestic political circumstances go from bad to worse. I think the political situation is going to continue to deteriorate.

We can look at the domestic fiscal circumstances. Now, the cash-based federal deficit shrank this year to less than $0.5 trillionsupposedly good news, but what people don't seem to be thinking about is that the Fed actually monetized 80% of that deficit through quantitative easing. The U.S. government wasn't out there in the markets borrowing openly and honestly. Whatever it was borrowing was also being purchased and taken out of the market by the Fed.

If we look at the annual deficit using generally accepted accounting principles and account for unfunded liabilities for programs such as Social Security, that deficit increases by about $6 trillion ($6T) per year. On an aggregate basis, including roughly $18T worth of gross federal debt, total federal obligations right now are up around $100T in net present value. That's what the government needs to cover its obligations. It doesn't have that and never will. What that means is the federal government does not have a sustainable financial future. That's the long-term fate of the system here.

TGR: Do you think the dollar is in a bubble right now and is going to crash?

JW: I guess you could call it a bubble. I do think it's going to crash. With that crash will come a big spike in oil prices, a big spike in gold and silver prices. The Fed is going to have to ease again. A weak economy means more stress on the banking system, and the Fed is always looking to prop up the banking system.

What you have to keep in mind with inflation and deflation is that there are different ways of looking at them. I'm looking at inflation and deflation basically from the standpoint of consumer expenditures, what people see in the way of prices of what they're purchasing, as opposed to asset inflation or deflation, where we're looking at financial market values. We can also look at growth in the money supply as a measure of inflation and deflation. Money supply growth actually will start to pick up very sharply as the dollar comes under heavy selling pressure.

There are some major problems with how inflation is viewed. I'm talking now about practical, day-to-day household operations. How much did it cost me to live last year? How much is it going to cost me to live same way this year? However much that number increasesthe cost of maintaining a constant standard of livingis the rate of inflation as far as the average person is concerned. That is the rate of inflation to use for targeting income growth or investment return. The government no longer reports it quite that way; the CPI does not measure inflation from the standpoint of maintaining a constant standard of living, or even from the standpoint of reflecting out-of- pocket expenses.

But central banks want to create inflation to prop up their economies and markets. Just blindly creating inflation, however, doesn't make any sense.

The positive type of inflation is created by strong demand for products, and because of short supplies, prices rise, but production also will be increasing. That's how the system would normally adjust for it. In this scenario, people are employed, their salaries are increasing, and the economy is growing. The Fed can't create that kind of inflation, at present. They would like to, but they can't. The central banks can't create that type of inflation, certainly not by flooding the system with cheap money that's not being lent to the consumer. They can only create the type of inflation that is driven by currency weakness.

I'm looking for the dollar to sell off sharply, actually suffer a massive decline, which, in turn, will be reflected in a very strong rise in commodity prices, pushing costs higher, pushing inflation higher, but not strengthening the economy. That's what the central banks are pushing for, which is nonsensical.

TGR: I recently wrote an article based on comments from former Federal Reserve Chairman Alan Greenspan that he gave at the New Orleans Investment Conference. He denied that the Fed was responsible for the housing bubble and explained that bubbles are easy to see but difficult, if not impossible, to pinpoint when they will implode. Do you agree? What bubbles do you see out there?

JW: Greenspan is a very interesting character. He has a wonderful vocabulary and was certainly a very influential politician and Fed chairman over the years, but what you just said is largely nonsense. In fact, you can make a strong case for laying the problems that we have right now in the lap of the former Fed chairman.

There are two things at work here. One, starting about 1970, the U.S. embarked on all sorts of trade practices that encouraged sharp growth in the trade deficit and the weakening of the dollar. As the dollar fell and as domestic production increasingly moved offshore, higher-paying production jobs disappeared. If we look at the government's numbers on the inflation-adjusted income of production workers in the U.S., it is 1015% below where it was in 1970, and it's been flat for the last couple of decades. This is where the problems developed with consumer income. We can't build wealth on producing hamburgers and providing services. We've become a service-based economy. That does not build wealth as does, let's say, manufacturing automobiles or tanks.

When I talk about manufacturing, I'm not talking about having an assembly plant. I'm talking about actually having all the subcontractors that make the parts. That's disappeared, and that put the American consumer in a circumstance where he or she just could not support the economy. Alan Greenspan recognized that. So what he did was encourage debt expansion, particularly in areas such as home equity loans. And the debt expansion that followed was what provided the bulk of the growth in the U.S. economy for the decade before the panic in 2008.

TGR: The housing bubble.

JW: That was a deliberate policy decision at his end. Had the economy taken a hit much earlier, say back in the time of the 1987 stock market crash, there would have been a period of financial discomfort, but the system would have been cleansed of a lot of abuses that had built up over time, and we could have had positive growth going forward. What we did with the debt expansion was to borrow as much growth as we could from the future and pull it into the earlier periods. There had to be a day of reckoning there.

TGR: Have we had that cleansing? Did 2008 get all of that out of the system?

JW: No. All sorts of things are still at work there because the system was not allowed to collapse as it would have. As much as could be was pushed off into the future. We still don't have a healthy, sustainable system. The panic of 2008 is still with us; it's just been pushed a couple of years into the future. We're coming up on it again.

But let me make one other point here because it's an important one regarding Mr. Greenspan's involvement. A lot of the bubble and its detrimental effects were created by all these derivative instrumentsmortgage-backed securities and suchthat were created as new investment vehicles and sold to the rest of the world. That area was highly touted by Alan Greenspan and by the Federal Reserve under his control as a way that the banks could spread risk. For example, insurance companies could take that risk by buying these derivative instruments. It was a way of distributing risk within the system.

The U.S. central bank can be credited with both encouraging an extraordinary debt bubble and in creating and encouraging the derivative instruments that were used to build debt leverage on top of debt leverage that resulted in the collapse in 2008. The Fed and the federal government never addressed the core of the economy's problems, never addressed why is it suffering from a liquidity standpoint. What they did was look for how we could borrow economic growth from the future. They came up with some very creative ways of doing it. When you borrow things from the future, usually you have a period of payback. That's what we're seeing now. That's why we can't get the economy to grow.

TGR: Can you give us a picture of what we can expect in 2015 and how we can prepare for it?

JW: I'll give you a couple of things to look for in 2015. Fundamental economic activity as measured in areas such as retail sales, industrial production, housing starts, payroll numbers and the broadest measure of unemploymentall those numbers are going to deteriorate. The economy is going to head down as we get into reporting in early 2015. Along with that will come renewed expectations of action by the Federal Reserve to accommodate the financial system, particularly the banking system, and the combination of those factors will, I believe, help to trigger a massive decline in the U.S. dollar. As a result of that, we will see spikes in commodity prices, such as oil. We will see a flight to quality in areas such as the precious metalsgold and silver. We will see the stock market and the bond market generally suffer some real selling pressure.

If interest rates go up, they would start to reflect in inflation numbers. Traditionally, long-term interest rates tend to move with inflation. You might see some upside movement there in the longer-term interest rates, which would depress the bond prices. A return to an accommodative mode for the Fed might rally stocks. But guess what? If we value those stocks in either inflation-adjusted dollars or in Swiss francs, we'll find that the real value of the domestic stock market will be in contraction.

Even though the Dow could rally to new highs, I would shy away from stocks. I know gold and silver have taken tremendous hits in this last year, but I would suggest holding physical gold and silver as hedges against the loss of purchasing power in the U.S. dollar. If you can put your liquid assets into something like gold, which will preserve the purchasing power of those assets and continue to provide liquidity. Such an investment would likely help you to get through the inflation crisis and whatever crises follow that. When things settle down, you should still be able to function well, having maintained the purchasing power and liquidity of your assets and wealth.

It's an extraordinary time. I did move my hyperinflation forecast from 2014 into 2015. But the dollar selling can start at any time, with little warning. And there are things that the central bank may do to try and prop up the dollar, but once heavy selling is in place, it's going to be a downhill run for the dollar.

TGR: Thank you for sharing your insights with us.

Walter J. "John" Williams has been a private consulting economist and a specialist in government economic reporting for more than 30 years. His economic consultancy is called Shadow Government Statistics (www.ShadowStats.com). His early work in economic reporting led to front-page stories in The New York Times and Investor's Business Daily. He received a bachelor's degree in economics, cum laude, from Dartmouth College in 1971, and was awarded a master's degree in business administration from Dartmouth's Amos Tuck School of Business Administration in 1972, where he was named an Edward Tuck Scholar.

Walter J. "John" Williams has been a private consulting economist and a specialist in government economic reporting for more than 30 years. His economic consultancy is called Shadow Government Statistics (www.ShadowStats.com). His early work in economic reporting led to front-page stories in The New York Times and Investor's Business Daily. He received a bachelor's degree in economics, cum laude, from Dartmouth College in 1971, and was awarded a master's degree in business administration from Dartmouth's Amos Tuck School of Business Administration in 1972, where he was named an Edward Tuck Scholar.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an employee.

2) John Williams: I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.