The U.S. ethanol market remains tight, keeping stocks in an uptrend. Profitability is high for ethanol producers right now. But recent production increases and a delay by U.S. Environmental Protection Agency (EPA) in updating the amount of ethanol to be used in the U.S. will likely create some uncertainty in the near term. (Ethanol is gasoline made from corn, not oil)

I study this issue closely because I made more money in ethanol stocks than anything else in 2014. They have gone from pariahs in late 2012when high corn prices almost bankrupted the industryto some of the most highly traded small cap stocks on the NASDAQ in the last year.

Ethanol and the EPA's Renewable Fuel Standard (RFShow much ethanol U.S. refiners must blend in to the gasoline they make) is a very political issue, but the reality is ethanol is a market based commodity now.

That's why I don't care that on Friday the EPA delayed on deciding the amount of ethanol the refinery industry has to use. The corn crops of the last two years have been so HUGE that corn is now very cheapmaking ethanol very profitable. Refiners saved a lot of money this summer substituting the maximum amount of expensive oil for cheap ethanol.

It has made GREAT economic sense for refiners to use ethanol since the end of the U.S. Midwest drought of 20112012. Back then when corn prices were $7/bushel, and the only reason to use ethanol was because of the RFS.

The political mandate to use ethanol is only useful when corn prices are high and refineries need a regulatory nudge to use ethanol. Now, with gasoline and corn and ethanol economics workingthe Renewable Fuel Standard (RFS) is as useful as screen doors on a submarine.

The Market doesn't need the RFS now. That's because ethanol profitability is high right now, and could stay that way for awhile.

Despite low gasoline prices, ethanol economics are strong now. One bushel of corn makes 2.8 gallons of ethanol. So corn at $3.50/bushel makes ethanol for (3.5/2.8) for $1.25/gallonabout 79 cents below gasoline right now. History shows clearly that ethanol can attract export markets with a 40-50 cent/gallon discount to gasoline. This suggests ethanol could rise another 30 cents a gallon and continue to find new export markets.

There are a couple recently formed clouds on that horizon but let me explain how ethanol went this year, and where I see it headed:

Ethanol traded at a big premium to gasoline in the late winter and spring due to rail disruptions, which was due to the very cold winter (Polar Vortex). Ethanol stocks on the NASDAQ soaredgoing up 200-500% in just months. But those high prices meant ethanol was not economic for export markets. At the same time, ethanol production increased as a result of those high domestic margins. That brought the price down through the entire summer, as it took time to develop export markets.

ETHANOL NOW AND THE NEAR TERM

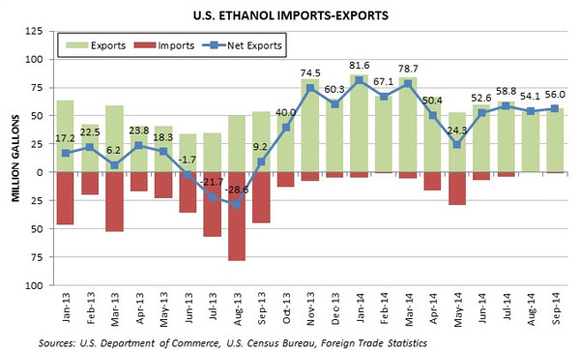

But now U.S. ethanol exports are rockingto the tune of just over 50 million net gallons exported a month. See this chart from the RFA blog (http://www.ethanolrfa.org/pages/blog/c/exports)

Ethanol prices are now above gasoline prices by a couple pennies a gallon. That would normally be bad for demand but refinery utilization is going through a big seasonal upswing, and gasoline inventories are lowa bit of a perfect storm for ethanol.

Let's say the U.S. is on track for a 700 million gallon a year net export rate. If U.S. refineries have to stick with about 13.7 billion gallon for the Renewable Fuel Standard (RFS) for 2015, that means U.S. ethanol industry can produce up to 14.4 billion gallons a year and have a balanced market.

Until last Wednesday's EIA inventory data, the ethanol industry had been producing BELOW a 14.4 billion gallon annual run ratewhich is one reason why ethanol prices have jumped from $1.50/gallon to over $2/gallon recently.

But a BIG jump in production last week to a run rate of 14.87 billion gallons put a scare into the ethanol market, with the price down its limit of 18 cents/gallon at one point Wednesday.

(Wednesday is the most volatile trading day for ethanol and ethanol stocks, as the Market moves very quickly after the EIA production and inventory data is released at 1030 am EST along with all the oil market data.)

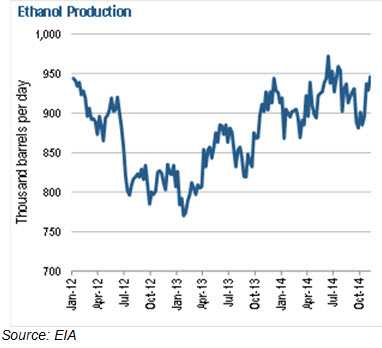

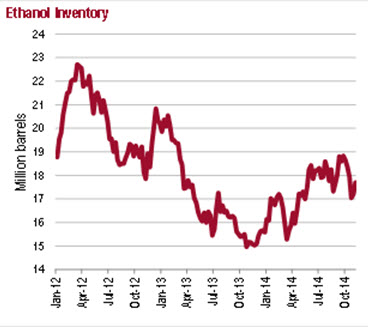

Ethanol production is increasing but those strong exports are keeping domestic inventories in checksee these charts from Credit Suisse a couple weeks ago:

It is a concern that ethanol production is now more than domestic use AND export use. But the U.S. ethanol market is now pretty much flat out producing as much as they can. My research indicates there are only five non-producing plants in the U.S. right nowtwo with equipment that has been removed and three in very poor locations where you simply cannot get corn cheaply.

And despite the increased production above what I consider the tipping point, ethanol inventories did drop last week.

So between higher production and close-to-peaking margins, I sold most of my ethanol stocks. But the reality is ethanol margins still remain strong, and again, inventories did drop last week. I expect corn pricing to remain low until the USDA gives its first acreage estimate on the 2015 corn crop (which is bound to be bullish for corn and bearish for ethanol as the number of corn acres should surely go down after two bumper crops and two years of low prices).

But I think the Market will continue to trade ethanol stocks with caution in the near term as

1) it tries to figure out what this delayed RFS ends up meaning,

2) see how the balance of production and exports go in the next 23 weeks

3) what oil prices do post OPEC meeting on Thurs Nov. 27

Investors should also remember that despite greatly increasing cash flows in the last 18 months, ethanol is NOT a growth storyit's really about playing the margins between corn and gasoline/oil.

Keith Schaefer

Oil and Gas Investments Bulletin