The Mining Report: You have said that Hillary Clinton could go down in history as one of the best presidents ever. Why?

Matt Badiali: Before we get your readership in an uproar, let me clarify that the oddsmakers say that Hillary Clinton is probably going to take the White House in the next election. Even Berkshire Hathaway CEO Warren Buffet said she is a slam dunk. I'm not personally a huge fan of Hillary Clinton, but I believe whoever the next president is will ride a wave of economic benefits that will cast a rosy glow on the administration.

"If you want to speculate on a uranium discovery, there is only one company out there: Fission Uranium Corp."

Her husband benefitted from the same lucky timing. In the 1980s, people had money and felt secure. It wasn't because of anything Bill Clinton did. He just happened to step onto the train as the economy started humming. Hillary is going to do the same thing. In this case, an abundance of affordable energy will fuel that glow. The fact is things are about to get really good in the United States.

TMR: Are you saying shale oil and gas production can overcome all the other problems in the country?

MB: Cheap natural gas is already impacting the economy. In 2008, we were paying $14/thousand cubic feet ($14/Mcf). Then, in March 2012, the price bottomed below $2/Mcf because we had found so much of it. We quit drilling the shale that only produces dry gas because it wasn't economic. You can't really export natural gas without spending billions to reverse the natural gas importing infrastructure that was put in place before the resource became a domestic boom. The result is that natural gas is so cheap that European and Asian manufacturing companies are moving here. Cheap energy trumps cheap labor any day.

Some peripheral beneficiaries from this cheap energy are in the chemical space. Dow Chemical Co. (DOW:NYSE) and others that make things from petroleum will benefit. One of my favorite plays on cheap energy right now is CF Industries Holdings Inc. (CF:NYSE), a nitrogen fertilizer company. The single biggest cost to this company is natural gas. That is a great business as long as natural gas prices stay low.

The same thing is happening in tight crude oil. We are producing more oil today than we have in decades. We are filling up every tank, reservoir and teacup because we need more pipelines. And it is just getting started. Companies are ramping up production and hiring lots of people. By 2016, the U.S. will have manufacturing, jobs and a healthy export trade. It will be an economic resurgence of epic proportions.

TMR: The economist and The Prize author Daniel Yergin forecasted U.S. oil production of 14 million barrels a day (14 MMbbl/d) by 2035. What are the implications for that both in terms of infrastructure and price?

MB: Let's start with the infrastructure. The U.S. produces over 8.5 MMbbl/d right now; a jump to 14 MMbbl/d would be a 65% increase. That would require an additional 5.5 MMbbl/d.

To put this in perspective, the growth of oil production from 2005 to today is faster than at any other time in American history, including the oil boom of the 1920s and 1930s. And we're adding it in bizarre places like North Dakota, places that have never produced large volumes of oil in the past.

North Dakota now produces over 1.1 MMbbl/d, but doesn't have the pipeline capacity to move the oil to the refineries and the people who use it. There also aren't enough places to store it. The bottlenecks are knocking as much as $10/bbl off the price to producers and resulting in lots of oil tankers on trains.

And it isn't just happening in North Dakota. Oil and gas production in Colorado, Ohio, Pennsylvania and even parts of Texas is overwhelming our existing infrastructure. That is why major pipeline and transportation companies, like Plains All American Pipeline L.P. (PAA:NYSE) and Enterprise Products Partners L.P. (EPD:NYSE), have exploded in value. They already have some infrastructure in place and they have the ability to invest in new pipelines.

There's also a massive amount of growth coming in companies that can process oil quickly. Valero Energy Corp. (VLO:NYSE), a giant refining company, is adding to its existing capacity. Alon USA Energy Inc. (ALJ:NYSE), another refiner, is adding to its rail offloading capacity. It's actually ramping up from 13 Mbbl/d to 150 Mbbl/d at one California refinery.

The problem we are facing in refining is that a few decades ago we thought we were running out of the good stuff, the light sweet crude oil. So refiners invested $100 billion to retool for the heavier, sour crudes from Canada, Venezuela and Mexico. That leaves little capacity for the new sources of high-quality oil being discovered in our backyard. That limited capacity results in lower prices for what should be premium grades.

One solution would be to lift the restriction on crude oil exports that dates back to the 1970s, when we were feeling protectionist. It is illegal for us to export crude oil. And because all the new oil is light sweet crude, the refiners can only use so much. That means the crude oil is piling up.

Peak oil is no longer a problem, but peak storage is. If we could ship the excess overseas, producers would get a fair price for the quality of their products. That would lead them to invest in more discovery. However, if they continue to get less money for their products, investment will slow. There is some good news on that front though.

Pioneer Natural Resources Co. (PXD:NYSE) produces ultralight crude oil called condensate from its Eagle Ford shale wells in Texas. The U.S. Department of Commerce, which regulates oil exports, approved the export of that condensate, if it is run through a simple "splitter." That's the simplest kind of refinery. Allowing companies to export split condensate could buoy falling oil prices and relieve some supply problems. However, it won't solve the whole problem.

TMR: If we do reach peak storage, where we all have oil stored in our swimming pools with no efficient way to move it or ability to export it, what is the price where it becomes uneconomic to produce?

MB: I was in San Antonio a couple weeks ago at Hart Energy's Discovering Unconventional Gas conference, and most of the producers said that at $65/bbl they can still make money, but at $45/bbl, they have to cut off production. Some fantastic oil company stock prices have already been demolished with the overall markets over the last few weeks. There has been a bloodbath, which is fantastic.

TMR: Is everything on sale, as Rick Rule likes to say?

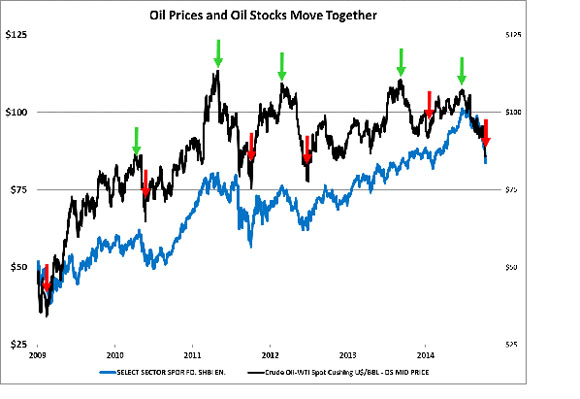

MB: Everything is on sale. But the great thing about oil is it is not like metals. It is cyclical, but it's critical. If you want your boats to cross oceans, your airplanes to fly, your cars to drive and your military to move, you have to have oil. You don't have to buy a new ship today, which would take metals. But if you want that sucker to go from point A to point B, you have to have oil. That's really important. There have been five cycles in oil prices in the last few years.

Oil prices rise and then fall. That's what we call a cycle. Each cycle impacts both the oil price and the stock prices of oil companies. We measured the share prices with the Energy Select Sector SPDR Exchange-Traded Fund (XLE:NYSE.A). These cycles are like clockwork. Their periods vary, but it's been an annual event since 2009. Shale, especially if we can export it, could change all of that.

The rest of the world's economy stinks. Russia and Europe are flirting with recession. China is a black box, but it is not as robust as we thought it was. Extra supply in the U.S. combined with less demand than expected is leading to temporary low oil prices. But strategically and economically, oil is too important for the price to get too low for too long.

I was recently at a conference in Washington, D.C., where International Energy Agency Executive Director Maria van der Hoeven predicted that without significant investment in the oil fields in the Middle East, we can expect a $15/bbl increase in the price of oil globally by 2025.

I don't foresee a lot of people investing in those places right now. A shooting war is not the best place to be invested. I was in Iraq last year and met the Kurds, and they're wonderful people. This is just a nightmare for them. And for the rest of the world it means a $15/bbl increase in oil.

For investors, the prospect of oil back at $100/bbl is not the end of the world. With oil prices down 20% from recent highs and the best companies down over 30% in value, it is a buying opportunity. It means the entire oil sector has just gone on sale, including the companies building the infrastructure.

As oil prices climb back to $100/bbl, companies will continue to invest in producing more oil. And that will turn Hillary Clinton's eight-year presidency into an economic wonderland.

TMR: The last time you and I chatted, you explained that different shales have different geology with different implications for cracking it, drilling it and transporting it. Are there parts of the country where it's cheaper to produce and companies will get higher prices?

MB: The producers in the Bakken are paying about twice as much to ship their oil by rail as the ones in the Permian or in Texas are paying to put it in a pipeline. The Eagle Ford is still my favorite quality shale and it is close to existing pipelines and export infrastructure, if that becomes a viable option. There are farmers being transformed into millionaires in Ohio as we speak, thanks to the Utica Shale.

TMR: What are some companies that are doing a good job figuring out the secret recipe in their respective shales?

Halcón Resources Corp. (HK:NASDAQ) is run by the same management team that built Petrohawk Energy Corporation (HK:NYSE) and sold it to BHP Billiton Ltd. (BHP:NYSE) when shale was a brand new thing. Halcón shares have been utterly destroyed in this downturn, but it is still a great company in the right place with the right people.

Sanchez Energy Corp. (SN:NYSE) is also an expert in the Eagle Ford right now. It's branching out into the Tuscaloosa Marine Shale in Louisiana. It hasn't found the sweet spots in the shale, but if oil gets to $100/bbl, these guys will find a way. In the meantime, Sanchez is profitable at current prices in the Eagle Ford. The Sanchez family has operated a private oil company in Texas for decades. I have a lot of respect for the management team. Sanchez is in parts of the Eagle Ford that people thought weren't going to be economic, and it is making the wells sing. In fact, Sanchez was able to cut its costs in half using new techniques, adding more sand to the wells and drilling multiple wells from a single pad.

I like both of these companies.

TMR: Do you see oil services as a way to leverage the quantity of oil coming out of the shale?

MB: If you were only going to buy one company to play all of the tight oil revolution, it would be Schlumberger Ltd. (SLB:NYSE), a behemoth of an oil services company that is essentially the Levi Strauss of the sector, a one-stop shop for fracking services, including imaging and materials.

TMR: What about the sands providers? Is that another way to play the service companies?

MB: Absolutely. The single most important factor in cracking the shale code is sand. If the pages of a book are the thin layers of rocks in the shale, pumping water is how the producers pop the rock layers apart and sand is the placeholder that props them open despite the enormous pressure from above. Today, for every vertical hole, drillers create long horizontals and divide them into 30+ sections with as much as 1,500 pounds of sand per section. A single pad in the Eagle Ford could anchor four vertical holes with four horizontal legs requiring the equivalent of 200 train car loads of sand.

That is why the shares prices of companies like U.S. Silica Holdings Inc. (SLCA:NYSE) and Hi-Crush Partners L.P. (HCLP:NYSE) soared. They are fairly recent public entities, but their share prices went straight up after their initial public offerings. It's because the volume of sand is just massive. Ironically, it's created a miniboom in states like Wisconsin, where a lot of this sand originates.

Investors need to distinguish between companies that provide highly refined sand for oil services and companies that bag sand for school playgrounds. Fracking sand is filtered and graded for consistency to ensure the most oil is recovered. Investors have to be careful about the type of company they are buying.

TMR: Coal still fuels a big chunk of the electricity in the U.S. Can a commodity be politically incorrect and a good investment?

MB: Coal has a serious headwind, and it's not just that it's politically incorrect. It competes with natural gas as an electrical fuel so you would expect the two commodities would trade for roughly the same price for the amount of electricity they can generate, but they don't. The Environmental Protection Agency is enacting emission standards that are effectively closing down coal-fired power plants. And because it is baseload power, you can't easily shut it off and turn it back on; it has to be maintained. That means it doesn't augment variable power like solar, as well as natural gas, which can be turned on and off like a jet engine turbine. So coal has two strikes against it. It is dirty and it isn't flexible.

Some coal companies could survive this transition, however. Metallurgical coal (met coal) companies, which produce a clean coal for making steel, have better prospects than steam coal. Along with steam coal, met coal prices are at a six-year low. One company stands out. Peabody Energy Corp. (BTU:NYSE) owns the largest coal mine (by production) in the world. The North Antelope Rochelle coal mine produces over 100 million tons per year. That's just from one of its mines. If you live in the lower 48 states (outside of the Northeast and California), there's a pretty good chance that your television is powered by one of Peabody's mines.

It is the worlds largest private-sector coal company. The downturn in the coal price killed the stock price. I expected profit from its Australian met coal assets would keep the company's revenues up. But even met coal prices crashed. We sold our position to preserve our capital.

Generally, I want to own coal that can be exported to India or China, where they really need it. Japan has replaced a lot of its nuclear power with coal and Germany restarted all the coal-fired power plants it had closed because of carbon emissions goals. We are already seeing deindustrialization there due to high energy prices. Cheap energy sources, including coal, will be embraced. I just don't know when.

TMR: A number of experts we have talked to have said uranium is getting ready to turn up. Are you investing in uranium?

MB: I do own uranium. When we are nearing the bottom of a resource market, whether it's potash, coal, uranium or oil, I buy the best company in the space first. The Exxon-Mobils of the space are the ones that are going to come back first. In the uranium space, I bought Cameco Corp. (CCO:TSX; CCJ:NYSE) for my S&A Resource Report newsletter portfolio. It is the company to buy if you're going to speculate on a bottom in uranium.

If you want to speculate on a uranium discovery, there is only one company out there. Fission Uranium Corp. (FCU:TSX) is the best of breed in terms of discoveries of any kind. It's uranium in the right place. It's run by the right guys. Fission Uranium is $0.87/share now. It was twice that in April, so it's fallen by half.

TMR: Do you think that Fission is now a takeover target?

MB: It absolutely is a takeover target. When? I don't know. Is it worth owning at $0.87/share? Absolutely. This is a speculative stock, though. This is one of those companies I would buy, hold in my account and sit on it for a while.

TMR: Thank you for your time, Matt.

MB: Thank you.

Matt Badiali is the editor of the S&A Resource Report, a monthly investment advisory that focuses on natural resources, including silver, uranium, copper, natural gas, oil, water and gold. He is a regular contributor to Growth Stock Wire, a free premarket briefing on the day's most profitable trading opportunities. Badiali has experience as a hydrologist, geologist and consultant to the oil industry. He holds a master's degree in geology from Florida Atlantic University. Click here for subscription information.

Matt Badiali is the editor of the S&A Resource Report, a monthly investment advisory that focuses on natural resources, including silver, uranium, copper, natural gas, oil, water and gold. He is a regular contributor to Growth Stock Wire, a free premarket briefing on the day's most profitable trading opportunities. Badiali has experience as a hydrologist, geologist and consultant to the oil industry. He holds a master's degree in geology from Florida Atlantic University. Click here for subscription information.

Read what other experts are saying about:

Want to read more Mining Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit The Mining Report home page.

DISCLOSURE:

1) JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: None.

2) Matt Badiali: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. Stansberry & Associates has a financial relationship with all companies discussed in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over what companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

3) The following company mentioned in the interview is a sponsor of Streetwise Reports: Fission Uranium Corp. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.