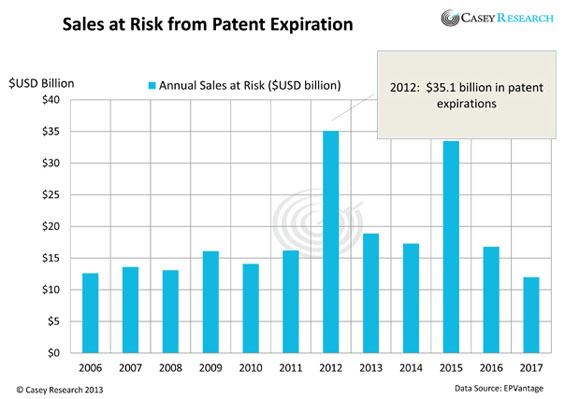

A little over a year ago in this space, we called your attention to a developing situation in the pharmaceutical industry, as shown by the chart below that dramatically illustrates the arrival of the so-called "patent cliff."

Today, the results are in from 2012. The IMS Institute for Healthcare Informatics has released its annual survey of the US drug market. It found that the market shrank last year for the first time ever.

Specifically, nominal drug spending in the US declined by 1% in 2012, to $325.8 billion. Real per-capita spending dropped even more, by 3.5% to $898.

Branded drug spending dipped by $11.4 billion, to $230.2 billion. Generic drug makers, as you would expect, were the beneficiaries here. Generics were used for a full 84% of dispensed scripts, with overall spending on them growing by $8 billion, not quite offsetting the diminishing dollars spent on branded meds.

This spending slide had the predictable consequence of slamming big pharma.

Eli Lilly, for example, was hit hard. The company's revenues, which reached an all-time high of $24.3 billion in 2011, skidded to $22.6 billion last year. Its revenues look set to keep sliding, as Lilly will lose patent protection for blockbuster Cymbaltawhich brings in $4 billion in revenue annuallyat the end of this year. This April, Lilly announced it will be dealing with the revenue erosion by laying off up to 1,000 employees in its US sales force.

Merck lost its protection of Singulaira $5 billion/year drug responsible for 16% of US salesin August of last year. Looking ahead, Merck had already begun cutting jobs in 2011 and wound up axing 30,000, nearly a third of its workforce. With Singulair sales falling 67% in 4Q12, the company experienced a 7% decline in fourth-quarter profits.

Novartis also took drastic steps ahead of its September 2012 loss of Diovan, which produced $2.5 billion/year in domestic revenues, or 15.9% of US sales. The company did $1.9 billion in cost cutting in 2011, followed by another $1.9 billion in 2012. That included the elimination of 2,400 jobs.

Bristol-Myers Squibb was hammered after losing Plavix, the world's second best-selling drug, last May. By 1Q13, Plavix sales had plummeted 95%, dragging down the company's revenues from $5.25 billion to $3.83 billion, and net income from $1.1 billion to $609 million.

And so on, pretty much down the line.

As the chart shows, this is not a one-time phenomenon. Patent expirations remain relatively high this year and next, and balloon again in 2015, when branded drugs' losses will almost equal last year's, at an estimated $33.5 billion. So, the question must be raised: will big pharma slowly waste away after tumbling over the patent cliff?

The short answer is "no." These are going to be some lean years, no question. But there's some good news, too.

"Initially the figures do look depressing, but I don't think people should be running for the hills just yet," says editor Lisa Urquhart of pharma analysts EP Vantage. "The efforts the industry has put in to change business models, which have included investing more in niche busters, mean this time round things might not be as bad."

In addition, most of the patent expiries from last year involved small-molecule drugs, which are easy to replicate. Going forward, a good number of those expiring are biologics, or large-molecule drugs, and these are not as simple to pick apart.

Big pharma is also emerging from a relative dry spell in the way of new products. Sales of newly introduced drugsdefined as products that have been on the market for less than 24 monthsactually grew last year, accounting for $10.8 billion in spending, up from $10.3 billion in 2011. In line with recent trends in the field, the lion's share of new-drug spending came in the specialty category.

Rollouts will continue at a brisk pace, too. IMS projects the launch of new molecular entities (NMEs) to come in at 3237 per year, potentially including new mechanisms of action in Alzheimer's, autoimmune disorders, diabetes, a number of cancers, and orphan diseases. That would establish a pace of 160185 NMEs introduced between 2012 and 2016, well above the 140 launched in 20062010.

"We're not talking a return to the late '90s or the early 2000s, when there were forty or more some years," and the growth rate was in the high single or double digits, says IMS research chief Michael Kleinrock. He notes that we should expect fewer mega-blockbusters and more high-priced specialty and orphan treatments, and adds that, "Rumors to the contrary, the US market is still alive and well. The patent cliff will take some of those dollars out of the mix, but once it's past its peak . . . we're going to see a significant rebound in what's available for both branded and generics companies."

Furthermore, although the US market is likely to stagnateIMS estimates an anemic cumulative growth of 14% from now through 2016the emerging nations are poised for explosive 1216% growth over the same period.

"In the next five years," Kleinrock says, "we will see the maturation, the evolution, of emerging marketswhich are heavily generic and driven by volumes primarily rising from very low-income people that have become more affluent or are otherwise getting better access to medical care."

The US still will remain by far the world's leading drug consumer, with a 31% share of the global market by 2016. But that's sharply down from its 41% share in 2006, with most of the shift going to the "pharmerging" countries, as the IMS calls them. They made up only 14% of the market in 2006 and 20% in 2011, but are predicted to draw nearly even with the US in 2016, when they'll gobble up 30% of the overall pie.

And a substantial pie it will be. Some $1.2 trillion is destined to be spent on pharmaceuticals in 2016, the IMS saysup from $956 billion in 2011with a still-hefty $615-645 billion going to branded drugs and $400430 billion siphoned off by generics.

What does it all mean for big pharma? With sales from existing drugs falling off the patent cliff, there will inevitably be an increased emphasis on development of new therapies that show high earning potential. That means plenty of employment for in-house researchers, but that source is not likely to be rich enough.

The current negative economics of giant mergers probably indicates that we will see few if any of those in the near future. But it's a certainty that big phama is going to be keeping close tabs on smaller companies that have promising drugs in phase 2 or 3 trials. Those are certain to be acquired at an accelerating rate, as their larger brethren seek to restock their R&D shelves in the most cost-effective manner.

Small companies with strong pharmaceutical pipelines are mainstays of the Casey Extraordinary Technology portfolio. While we would never buy shares of a company solely because we were betting on a buyout, that can provide some very nice icing on the cake for early investors when it happens.

Doug Hornig

Casey Research