In December 2012, at the Mines and Money conference in London, Sandstorm Gold Ltd. (SSL:TSX) President and CEO Nolan Watson proclaimed, "Mining finance as you know it is dead!" He proposed that streaming could be part of the solution to a lack of bank financing now available by buying the right to purchase future profits. This works best, Watson said, when mining company and royalty company interests are aligned. While royalty companies started as value arbitrage businesses, he now sees a broader role as funding partners. Sandstorm has started to invest in equity and debt. He went on to predict that royalty space would expand from the big four royalty companies worth $27 billion ($27B) at the end of 2012 to 10 or 20 companies worth hundreds of billions of dollars in the next decade.

We asked other executives in the space if they agreed with Watson's analysis of the sector. "It's a tight point in the cycle," said Silver Wheaton Corp. (SLW:TSX; SLW:NYSE) CEO Randy Smallwood. "Now is the time, however, when streaming and royalties should play a very pivotal role." Smallwood took a long-term view. "It is important to remember that this is a cyclical industry. At some points in the cycle, exploration finance is very hard to come by, which subsequently results in a dearth of new discoveries and ultimately a supply shortage. When supply becomes tight, the funding comes back, and hence the cycle. For Silver Wheaton, these periods of tight financing create opportunityand this is exactly what we are seeing now."

Others saw royalties as part of the funding mix going forward. "In the past 20 years, mine construction was viewed as being funded exclusively through equity or debt," explained Gold Royalties Corp. (GRO:TSX.V) CEO Ryan Kalt. "Going forward, I believe mine construction will be funded by three pillars: a royalty component, a debt component and an equity component. Adding royalty funding is accretive for a mine developer as it can use less equity and debt, while leveraging the cost of capital advantage from its royalty company partner."

Callinan Royalties Corp. (CAA:TSX.V) CEO Roland Butler noted, that perhaps "we are witnessing an end to traditional but unsustainable exploration financing approaches. This has opened the door to re-examination of the role royalty financing can serve, especially in the area of royalty creation at early exploration stage. This would be an adaptation of the grubstake model used decades ago."

Raising equity can result in massive shareholder dilution. Debt, when available, means forcing the unique challenges of building each particular mine into rigid bankers' timetables and punishing covenants. Royalty financing, noted Franco-Nevada Corp. (FNV:TSX; FNV:NYSE) CEO David Harquail, "is patient money assuming risk on project performance, timing and. . .commodity price risk. Royalty financing also means giving up part of the upside of a single project rather than in all the assets and future of a company." He put the role of a royalty somewhere between equity and debt. "There is a lot to like from a developer's perspective."

Royalties today come in lots of sizes and structures. A number of smaller royalty companies have entered the space recently. Americas Bullion Royalty Corp. (AMB:TSX), which was previously known as Golden Predator Corp., CEO Paul Zink is talking to companies in the $550 million ($550M) range as he prepares to do the company's first deal. He sees a role for small royalty companies to come into a niche that is not being filled by the established companies, where it takes a large transaction to move the needle.

Zink also sees demand for royalty companies, including small royalty companies, on the investor side. "The market is now recognizing that based on the gap between mining stocks and gold valuations, royalties are faring relatively better." Zink believes royalty companies play a research role in the industry. "We play the role of vetting projects technically, something an individual investor may not be able to do," he said.

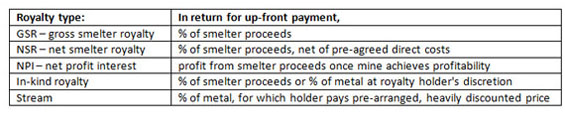

Not all royalties are structured the same. Some start collecting their returns after a company starts processing and making money. Some collect regardless of company profits. Gross smelter royalties or net smelter royalties (NSR) involve a single up-front payment in return for a life-of-mine percentage of cash smelter proceeds, net of pre-negotiated costs. Net profit interests (NPI) pay out only after mining costs have been recovered and profits attained, per an operator's accounting. An in-kind royalty receives metal rather than cash, which minimizes accounting disputes. A stream involves an upfront payment plus a per-ounce payment often covering "cash costs" as metal is produced.

Glossary of Royalty Terms

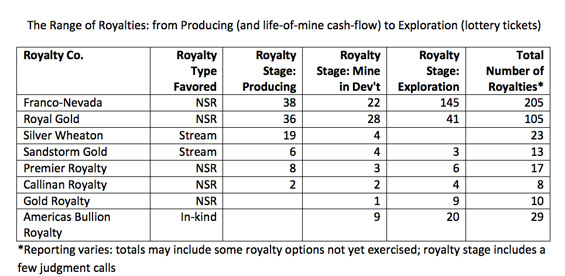

All of Silver Wheaton's revenues are from 19 producing streams. Founded in 2004, Silver Wheaton was the first to implement streaming in hard-rock mining. Focusing on secondary streams of precious metals from primarily base metal producers, Silver Wheaton helps ensure economic viability of mines by covering the co-product cost of the silver and gold attributed to Silver Wheaton. The company is the largest in the business, with a market cap of $8.6B.

Franco-Nevada, which has a market cap of $6.3B, bought its first royalty in 1986 and has 211 mineral-based royalties, the majority of which are NSRs. Franco regards NSRs as the simplest type of royalty to manage and "highest margin, as any deductions for refining are very minor," said CEO Harquail. Still, 39% of 2012 revenues came from stream-based royalties.

Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX), founded in 1991 with a current market cap of $3.6B, has 200 assets, encompassing both streams and NSRs. Royal Gold has made private equity investments to obtain options on future royalties [Seabridge Gold Inc. (SEA:TSX; SA:NYSE.MKT)] and has even funded exploration on the Carlin Trend, then sought a operator for development and production [Placer Dome, now Barrick Gold Corp. (ABX:TSX; ABX:NYSE)] from which royalties were obtained upon highly lucrative terms.

Among new entrants, Sandstorm Gold, which was founded in 2009 by Silver Wheaton's first employee, Nolan Watson, has closed 10 gold streams, but has also bought three NSR advanced exploration royalties on projects Watson regarded as too early stage for a stream. Streams comprise 95% of Sandstorm's net asset value (NAV), which has a market cap: $0.6B.

Newer, more junior entrants such as Premier Royalty Inc. (NSR:TSX), Gold Royalties and Callinan Royalties prefer NSRs. This may be because NSRs as a rule range up to 5% of a mine's output, while streams range from 10% to 20% or more. Streamers finance initiation or expansion of production, providing larger amounts of capital than an NSR buyer, and therefore need greater and lower cost access to capital. "Unlike metal streams, which require a significant per delivered unit cost (e.g., $500/ounce), each dollar of cash flow generated by an NSR royalty has a comparatively much higher operating margin as there are normally more nominal deductions associated with that royalty structure, including smelter, transportation and insurance costs," explained Gold Royalties CEO Kalt. He added that NSRs can have royalty revenue margins in excess of 95%, "much better than metal stream or NPI royalties."

At the same time, Kalt pointed out that an NSR takes less of a producer's cash flow streamtypically less than 5%versus a sizeable gold stream, which can be greater than 25%. "Sustainability of the metal stream for the operator will be a go-forward consideration around streams, as operators also need to have strong full cycle-businesses to help fund the exploration that both NSR and metal stream royalty holders are carried on," he said. All 10 of Gold Royalties' acquisitions have been NSRs.

Americas Bullion has a market cap of $29M and a historic portfolio of Nevada in-kind royalties based on a 25-year-old royalty portfolio Golden Predator CEO Bill Sheriff acquired in 2008. CEO Paul Zink is in the process of turning the company from an explorer into a royalty company.

And some of the royalty companies are mixing it up. Sandstorm bought 60% of Premier Royalty and will pass smaller opportunities to Premier, which will continue to operate as before. Franco-Nevada has obtained rights to invest 50% in Gold Royalty's asset deals up to CA$15M.

Finding the Sweet Spot

All respondents acknowledge that senior miners are retreating from large new projects and focusing on profitability of existing development projects and producing mines. Streams are aiming at midtiers or juniors approaching starting or expanding production. NSRs typically aim at earlier stage projects, often explorers. Callinan CEO and Altius co-founder Butler observed that senior miners, "perhaps sensing opportunity. . .are auctioning their royalty interests on the market. Today there are few large royalty portfolios that remain available."

Silver Wheaton and Sandstorm favor production stage, with a small number of development stage assets. By contrast, Franco-Nevada CEO Harquail states, "we love exploration royalties, and can never have enough of them. Right now, we have 137 exploration royalties and our royalties now cover almost 10M acres on geologically prospective trends." Royal Gold has 36 producing, 28 development and 41 exploration royalties.

Callinan CEO Butler will invest at any stage, but now sees "greater value in smaller and earlier stage opportunities." Of the six investments he has made in the past year, two are for advanced projects with a development and production timeline, accounting for approximately two-thirds of the investment value, and the remaining four are at various stages of exploration.

Gold Royalties CEO Kalt sees the best risk/reward "once an operator has defined a resource and its economic parameters. . .and is in the range of 2 to 4 years from first gold pour." He also finds it "prudent to allocate a modest percentage of a balance sheet to exploration royalties, as unlike exploration stocks, the fixed royalty percentage is carried to production without future dilution and the optionality can have a material impact to NAV per share."

Store of Value

In the paper gold versus bullion hoarding debate, Silver Wheaton CEO Smallwood was not a fan of hedging or hoarding. "Our goal is to be an alternative to owning bullion or an exchange-traded fund and therefore sell our silver and gold as it is delivered. . . .Also, the dynamic nature of the opportunities means that we cannot hold a substantial amount of our capital in bullion as it would limit our ability to readily access those funds."

Sandstorm CEO Watson and Gold Royalties' Kalt agreed. "We intend to continue converting our gold into cash and complete additional gold streams. Our investors can get better leverage to gold by Sandstorm growing its streaming portfolio."

Kalt said, "Royalty companies provide torque to bullion ownership in that they are carried at the project-level for exploration and resource expansion. Hedging that bullion could reduce leverage to that upside characteristic."

Callinan's Butler sees the value of keeping some gold around. "We see holding approximately 20% of our market value in cash as providing option value in that it provides us the ability to swiftly and readily act on exceptional value opportunities. . . .Also, we are careful in cash management and are becoming more wary of where our money is held and in the form in which it is held. Gold, as always, is an increasingly attractive form of money." Courageous words written April 18, after gold's most precipitous drop in decades!

The Investor's Bottom Line

The founder of Adrian Day Asset Management has been buying more royalty companies than ever. "There are more royalty companies available today," Day said in a recent interview in The Gold Report. "For investors, the main goal should be to mitigate risk. For the bigger, senior companies, the biggest risks are replacing ounces produced because a mine is a depleting asset, and because of the continual things that go wrong with a mining operation. The big royalty companies with revenue from various mines diversify and mitigate risk to a very large extent. Once you've bought a royalty, your first dollar in is your last dollar in. You're not obligated to pay for cost overruns. If the government increases taxes, you don't have to pay them. If the water table breaks and the mine shaft floods, you don't have to pay to fix it. You mitigate the risk by avoiding all those unforeseen additional expenses. The owner of a royalty just has to be a little patient and wait for the mine to finally get built and produce gold. That's a big benefit."

Jonathan Gunter co-founded and built two South American wireless companies. Since their sale, he has studied and invested in gold equities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Jonathan Gunter wrote this article for The Gold Report and provides services to The Gold Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: Callinan Royalties Corp., Premier Royalty Inc., Americas Bullion Royalty Corp., and Sandstorm Gold Ltd.

2) The following companies mentioned in the article are sponsors of The Gold Report: Gold Royalties Corp., Franco-Nevada Corp. and Royal Gold Inc. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Streetwise Reports does not make editorial comments or change experts' statements without their consent.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.