There was little reason for optimism and certainly no optimists that we could find in the junior space this month.

This month's editorial continues the discussion of what large companies seem to be looking for and what juniors should be looking for too. This sort of shift is not a short-term scenario. By definition it's going to take some time for companies to retool and approach projects from a different direction with different assumptions. Even then, this will only work for a subset of companies.

Short term, I still think discoveries are the best path to salvation for individual companies and perhaps the broader sector. Maybe gold gets a big bounce in the next few weeks but with the drubbing everyone has taken I don't see traders heavily on the bid unless higher gold prices are already in the rear view mirror.

The "currency war" scenario remains in play and this is almost always going to favor the $US. War is too dramatic a term for it. Japan is pushing the yen down but euro weakness has more to do with political ineptitude than formal policy. Traders are having trouble buying into the idea of second half growth in euroland. Gold is testing lows as this issue is released which may determine the length of the bottom.

***

In the last issue of the Journal I talked about the paradigm shift in the resource space that has been adding to the pain of juniors and their shareholders. Major companies seem to be out of the market for new deposits and there has been a shift in the type of deposit they are looking for. This has left many juniors high and dry.

I am not assuming that the change that has taken place in the past two years is permanent. It probably isn't. Industries move in cycles and management practices are more subject to fads and herd behavior than most things.

At some point in the future, and it may not be far off, many large, low-grade projects will be back in fashion. There are two reasons for this. One is that it's not going to get easier to find large deposits. While we might hit a rough patch as large mine startups lift the supply of metals like copper or iron ore but those changes are also cyclical. Metal prices aren't going back to pre-2000 norms and there are always mines getting depleted and closing.

Miners will not be able to rest on their laurels and prices should stay high enough that bulk tonnage will always have its placeif costs get under control. While miners will not prefer lower grade deposits and they may not be the first ones bought, at some point many of them will still get mined.

The second reason is the psychology of management in larger organizations. Many CEOs got chopped in the past year. That lesson is not lost on their peers but don't count on the lesson maintaining its power forever.

People who work their way to the top of large organizations tend to be empire builders. It's in their nature to want to maximize the size of the organization and the importance of their position.

We've seen this over and over again in other sectors. Every decade or so there is a rash of mergers. A lot of them end up being non-accretive at best or disastrous at worst. Shareholders and analysts decry them and CEOs promise to forget they ever heard the term "M&A." A few years later they are back at it again. I see no reason to think the mining sector will be any different.

That's light at the end of the tunnel, but it's a long tunnel. A few juniors could cycle through other projects or hunker down while maintaining interest in a large resource no one currently wants. I'm pretty sure that is exactly what will happen in many cases.

I also expect the creation of a number of midsize companies that will cast their nets more widely for projects and generate new takeover demand. In a normal bull cycle this sort of company gets created organically. Some companies go into production successfully and keep doing it until they control a number of mining operations and a substantial top line revenue stream.

This happened this cycle but it's not as evident because there was a rash of takeovers mid-decade that saw mid-sized producers either merging or being bought out by their larger brethren. The mid-cap space was hollowed out. That normally takes a long time to correct but there is a movement afoot that could accelerate it.

Many large companies are facing demands to "right-size," splitting into geographic and/or commodity subunits. In theory at least this would make the growth path smoother for these newly minted companies.

If you are a company that produces two million ounces a year of gold it should, in theory at least, be much easier to deliver 10% production growth. That's 200,000 ounces a year, which one moderate mining operation or two smaller ones can provide. This still isn't a piece of cake, but it's a lot easier than adding a million ounces a year.

The largest miners didn't seek projects with maximum scale out of some sort of perverse obstinacy. They had shareholders demanding revenue and profit growth at levels that demanded large project spending.

It is absolutely no coincidence that the largest mining houses in the world focused on iron ore and metallurgical coal for the past decade or more. If you are RTZ or Vale or BHP it's not just desirable to have projects in these commoditiesit's necessity. No other commodities have individual projects that generate revenues at a scale that delivers the percentage top line growth shareholders demanded. In order to continue to position themselves as growth stories, they had to bulk up on this stuff.

This meant plenty of competition not just for projects but for specialized large scale equipment and one-off engineering and design talent. It's tricky to build huge complexes capable of processing and shipping tens of millions of tonnes of material annually, not to mention rail and port facilities to go with them.

While the situation was less extreme in the precious and base metal space the large project bias helped magnify existing bottlenecks for things like heavy haul trucks and extra-large mills. Combine that with a stressed supply chain and exploding prices for major inputs like steel and you have a recipe for extreme cost inflation.

An added problem that I think exists but doesn't really get talked about much is lack of experience on the project management and engineering side. You can only train people so fast. The number of projects under development grew so rapidly that personnel were spread too thin. Its highly likely that some of the problems with cost overruns were exacerbated by poor project management and initial cost estimates by relatively untrained engineers that were just plain wrong.

It will be difficult for the really large mining houses to escape the vicious cycle of cost overruns unless they downshift growth plans for an extended period. The best managers need to be put on the most important projects. Prices for things like mills and trucks are sticky and it will take several quarters of relative inactivity before prices stabilize and, hopefully, fall.

I don't see the largest mining houses "right-sizing" unless they split into commodity groups but there is room for midsized and large precious and base metal miners to do it. There should be more spin out transactions as non-core assets are shed and business units are split off. This will give the new entities the ability to reset things starting with a sustainable revenue level that would be easier to grow from based on smaller more manageable operations.

This would give rise to a new group of small- and mid-cap miners. It's been lonely in the mid-cap space for some years. We haven't seen the rise of many new multi mine producers of the type that were formed in earlier cycles. I think this growth at the small end of the mining production sector is coming anyway but it will happen much faster if some larger companies split themselves up.

The reemergence of the mid-cap space in the mining sector should generate new demand for projects in the 1-5 million gold ounce equivalent range. That gives some hope to juniors sitting on this type of project though I stress that buyers will be very picky and high margin projects will be the only ones getting bought any time soon.

What will they be looking for? Lowest quartile cash costs and, where possible, lowest quartile capital intensity too.

Capital Intensity is a measure of the initial capital required to generate an ounce of gold, pound of copper, etc. Lower capital intensity projects should be easier to finance and, other things equal, will have shorter payback periods. In some situations, capital intensity can be so low that it can help overcome even grade.

A good example of this is a number of new mines in Sonora, Mexico. These are all heap-leach operations at present and most have low grade resources. Even so, many of them produce gold in the $400-600/oz cash cost range and generate impressive returns thanks to good infrastructure and low capex. I expect Mexico and other areas with infrastructure and cost structure advantages to come back to prominence in the next couple of years.

Another thing you will see majors going after again is underground resources. This will come as a surprise to many. It's been a mantra in the exploration and mining sector for years that open pit trumps underground. This viewpoint made my dear departed brother David crazy. Dave went to a mining school and thought investors vastly overestimated the cost advantage of open pits.

There is a cost advantage but it's smaller than most people think. A well run underground mine can have mining costs in the $50-75/tonne range. If the resource is shallow enough to be ramped to rather than requiring a hoist and head frame the capital cost can be greatly reduced and the construction period significantly shortened.

Underground operations often run at much lower daily production rates. This means a smaller mill (it's almost always a mill). Yes, milling has higher costs per tonne than heap leach but there are some significant consolations. The biggest one is recoveries.

While there are simple oxide resources with high gold heap-leach recoveries you'll generally recover a lot more gold in a well-run mill. Gold recovery per tonne 20-40% higher than heap leach are not uncommon and for silver the amount recovered is often as much as 100% higher. That is the reason you'll see Silvercrest run a lot of its leached ore through a mill once it gets one up and running. There is still significant value in the ore when the leaching is finishedand Santa Elena has high leach recoveries compared to most.

Underground operations often have better survivability during bad times as well. It's common practice to run several stopes or working faces simultaneously, often producing from areas with different grades. The output from these different areas is mixed on its way to the mill to produce feed with an average grade approaching that of the entire ore body.

If metal prices drop the mine can focus on higher grade areas that produce at lower operating costs and keep the mine alive. This is not the preferred way to go as you're robbing grade from the later stage of the mine life but at least its keeps things going.

This sort of selective mining is generally not feasible in an open pit scenario. An old miner's saying is "you can't stope an open pit." By that they mean that it's difficult and perhaps impossible to adjust head grades by changing the mining plan in a bulk tonnage deposit. If the price of your commodity drops below production cost, you're done. This is one more reason why suddenly risk adverse management might learn to love underground deposits again.

While all mining operations have some similar clean up issues like tailings, underground operations often have much smaller environmental footprints. They are also just less visible, particularly when it's a ramp only situation. In many modern operations even the tailings and waste issue is alleviated though the use of backfill that returns mined rock to underground workings areas that are no longer active. Lighter environmental impact can simplify and speed up the permitting process.

I'm not assuming a wholesale change of direction by every major mining company but I do think the game has changed. It's now about high margin, low capital intensity projects. If a project can deliver that and it's a low environmental footprint situation so much the better. I think underground will be back in vogue.

That doesn't mean open pits go away. High grade heap leach operations can also be low cost low capex and some large operations have great returns. Investment returns will have to be high though, and long payback periods will be difficult to sell to bankers and investors. If you're looking at companies with advanced projects be sure that they fit these new parameters. I think it will be a long time before a project gets developed or sold if it does not.

On the investment side, there may be no cure but time and success for the sector. In addition to the mismatch between market value and project cost that you see in scores of development companies you have a big trust issue. So many companies have blown up projects with cost overruns and under performance that traders don't believe the study numbers any more.

In past years one might look at a company with a $20 million value and a project with a $500 million NPV and say "that looks cheap." These days we are much more likely to say "No way can they ever finance that (probably true, alas) and they'll probably just screw it up if they do."

I don't expect a sudden rise of "faith-based investing" in the junior space. Failing that the only way to close the gap between company value and apparent project value is successful developments. Traders need to see companies bring projects through development on time and on, or at least near, budget. Having managed that, the market will also want to see a few quarters of profit numbers reasonably close to expectations.

If a bunch of development level companies can pull that off it will help not only their own shareholders but those of companies earlier in the development cycle.

It takes time to get even a small operation up and running. The timelines would be much more manageable than a megaproject though. Small (20-100K ounces/year) projects use off-the-shelf mining and recovery equipment. They also tend to have shorter permitting periods because the amount of disturbance is much smaller.

Getting from development to production takes money and it's a tough financing environment. It's much more possible with a small operation however, especially in a region with good infrastructure. Several companies have managed to get heap-leach operations in northwest Mexico going for tens rather than hundreds of millions.

The same thing should be possible in the southwestern U.S., especially in the post-housing bubble era where construction and earth moving costs have dropped substantially. It's not going to be easy but management that can convincingly show it has proven capability to go into production will find money, even in this sort of market.

I expected to start seeing retooled economic studies that favor small, low capital intensity projects. Some juniors will be able to graduate to production with these. One thing about small production scenarios is that they can't really support outrageously expensive feasibility work. This is another area that has seen huge cost inflation.

This will be tricky to manage because the regulators will not let companies talk about project economics in anything but very vague terms until a large third party engineering firm has sprinkled "bankable feasibility" holy water on it.

I understand that the regulators are trying to protect investors. Companies can't talk project economics unless a third party Qualified Person has vetted the estimates. That is fine as far as it goes but it imposes huge costs on even small projects unless the company can raise financing without a feasibility study. On really "capex-lite" projects spending millions on feasibility rather than spending money just putting the dammed thing in production will not make any sense.

Will some of those low budget production startups blow up in everyone's face? Yep. Welcome to business start-ups 101. It will happen in some cases, with or without a feasibility study. You can't predict everything and failures happen across every sector and mining is no different. I'm not trying to dump on the engineering industry but it's worth remembering that many of the current projects with the worst cost overruns and initial production stats are also the most expensively over engineered ones. Giant, expensive studies have not guaranteed success.

When looking at potential production situation without lots of third party vetting, it will be imperative to get a feel for the competence of management. Resumes will have to be checked and should include supervisory experience in mine construction and operations. Exploration geologists with no minesite experience should not be trying to develop projects on their own. Thankfully, most of them have the sense to know that and will add relevant personnel.

Large engineering groups have been delivering "gold-plated" project designs for years. Some of them were sued in the past when there were production startup issues. Their response has been to over engineer everything. This makes a failure in the production flow sheet less likely but it also makes the project significantly less economic overall and more susceptible to cost overrun.

The whole industry won't move to seat of the pants mine building but some sort of happy medium has to be found. One of the most interesting recent news releases came from First Quantum Mining (FM-T).HRA followed FM from its inception until it reached $100/share several years later. It got there by developing or redeveloping several large copper projects, mainly in the Zambian copper belt.

First Quantum has always done most of its planning and project management internally. Because it's been so successful it has a great deal of street cred. This means that when it lays out an economic model for a new operation the market takes it seriously.

FM recently acquired Inmet, and the main motivation for the takeover was to get control of the giant Panama Cobre deposit. Cobre was mainly designed and costed by large international engineering firms and has an estimated capex of $6.2 billion.

FM announced a few days ago that it was cancelling the contracts of all the outside engineering and construction firms. It plans to spend several months going through the existing feasibility study, tweaking the design and planning to try and cut costs.

FM's management thinks it can take a billion dollars off the cost and I won't be the least bit surprised if they do it. You'll see a lot more of this in the future I think. It's similar to the trend in other industries to hire in house legal counsel. A big part of the job of an inside counsel is policing the billing of external law firms. Expect mining companies to use a similar model with engineering and to get a lot more hard-nosed about the costs they will accept.

The sector is not disappearing but like any industry that has had a major growth spurt mining has excesses that need to be dealt with. The cost squeeze will go on for a while and so will the slow pace of takeovers. Takeovers will return however and this new paradigm will give select juniors a chance to move to production on a small scale themselves.

Creation of a new set of companies that can climb to the mid-tier space is overdue. The current bear should not stop that transition and may even accelerate it. I'm looking for contenders for the HRA list.

Market Overview

Metals and the junior markets continued their dive this month. There is some indication that we might be seeing a bottom in the gold price but that bottom is in the process of being tested. It's too early to know if the test succeeds this time.

Gold was finding its feet when it was knocked back by release of the latest Fed meeting minutes and a report from Goldman Sachs calling for lower gold prices.

The Fed minutes showed that several Fed governors were calling for an end of QE3 this year. That is not too shocking. Several Fed board members have been opposed to the expansion of the Fed balance sheet from day one. Note also that this meeting took place before the release of the March employment report in the US. When the Fed was meeting the consensus estimate was for 250,000 new jobs in March. The actual number was a very disappointing 88,000. At that rate of job growth it would take years to get to Bernanke's 6.5% unemployment target for ending QE3.

Goldman's report just came out but I don't expect it to say anything too compelling. Wall St is basing gold forecasts on QE3 and not much else. Gold went up for years without QE1-3. Buying was based on an easing US Dollar and also on increased wealth levels in developing countries, particularly India and China.

Recent economic news out of China has been relatively good. India is a bit of a mess but soft commodity prices are high and the strength and price of harvests have as much impact on the appetite of Indians for gold as anything else.

The chart of the $US on this page is impressive in that it looks like the US dollar wants to roll over. That is meaningful given how hard the Bank of Japan is working to weaken the yen and the pandemic of foot in mouth disease in Europe. All the jawboning in Washington is just thatjawboning. Only a complete idiot would want a higher currency in this environment.

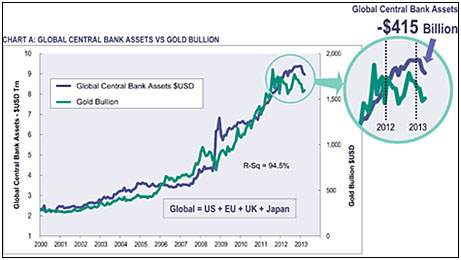

Note the chart on the previous page, which I stole from Dave Franklin at Sprott Asset Management. The chart shows the long term trend of gold prices versus global (US+ECB+UK+Japan) central bank assets. The long term correlation is impressively high with an R2 of 0.945. Correlation doesn't mean causation but when it's this high you have a relationship worth watching.

Central bank assets actually declined in Q1 as the ECB reeled in some of its 2 year refinance paper. That has all changed since the Bank of Japan opened the spigots. If Europe keeps dragging odds are the EBC grows its balance sheet again too.

With Japan's $75 billion added to the ongoing Fed $85 billion in balance sheet expansion, global central bank assets could grow by another $1.3 trillion by year end. That implies a $300/ounce increase in the gold price based on the relationship graphed above. No guarantee obviously, but a cheery thought to end with.

Ω

Eric Coffin recently presented at the Toronto Subscriber Investment Summit on March 2, 2013. To watch this exclusive subscriber only video of Eric's presentation titled "Is This It Or?" please click here now.

The HRA Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-based expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2010 Stockwork Consulting Ltd. All Rights Reserved.