Investors seeking leverage to precious metals should focus on junior resource companies who own the world's undeveloped gold and silver deposits as they provide the best exposure to a rising precious metals price environment.

You need to find the quality management teams with money in the treasury, the ability to raise more and owning the advanced projects that are well along the development path towards a mine.

A mine that is going to be a long life, lowest quartile all-in cost producer in a geo-politically safe country.

These companies are the world's future gold/silver producers and of course many will be in the sights of mid-tier and major producers for takeover candidates as reserve replacement targets.

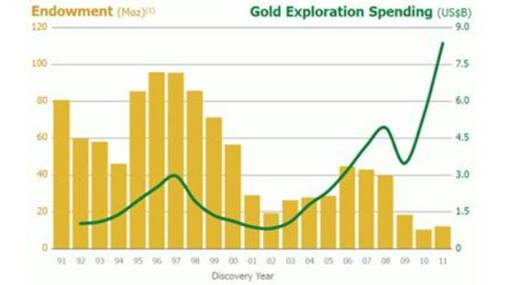

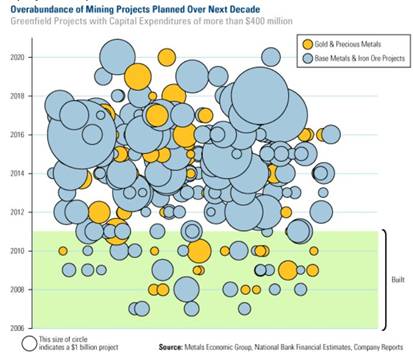

The gold mining industry needs to discover 90 million ounces of gold every year just to stay even.

But despite increased exploration expenditures, a record US$8b in 2011, and an increasing gold price, gold ounce discovery is not keeping up to the rate needed to replace mined ounces.

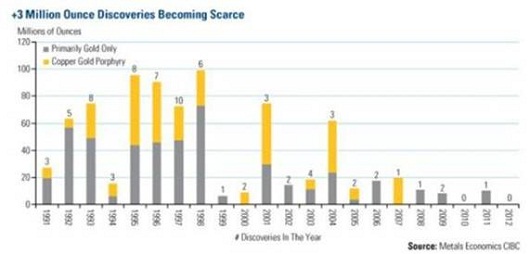

The Metals Economic Group estimates that the 99 significant discoveries (defined as greater than 2 mil oz) found between 1997 and 2011 replaced only 56 percent of the gold mined during that same period.

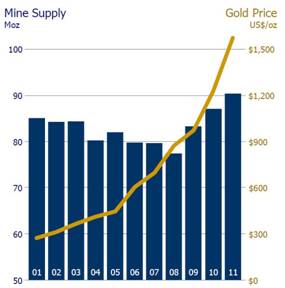

According to the Thomson Reuters GFMS's Gold Survey 2012 global gold mine production was flat (output rose 0.1 percent to 1,366 metric tons) in the first half of 2012.

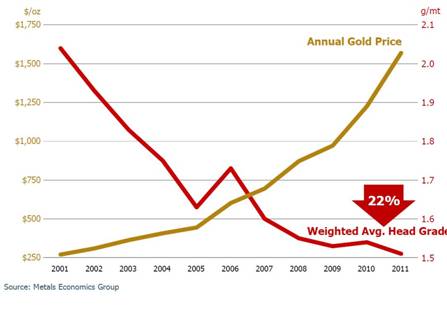

The average grade of ore processed globally dropped 23 percent from 2005 through the end of last year and is forecast to decline another four percent in 2012.

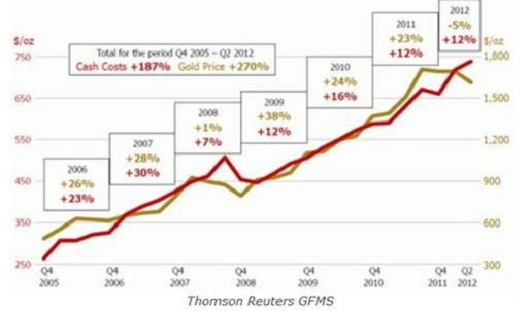

The GFMS report also said the average cash cost across the gold mining industry for mining an ounce of gold is a record $727 per ounce. The average cash margin dropped to $872 an ounce in the second quarter from as much as $1,032 an ounce in last year's third quarter

Average operating/cash cost figures include only those costs directly associated with the production of the gold such as;

- Wages

- Cost of energy

- Raw materials such as steel, explosives etc

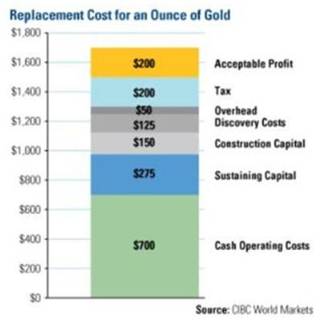

A complete breakdown of costs, an all-in cost figure, courtesy of CIBC, shows cash operating costs pegged at $700 an ounce.

Sustaining capital, construction capital, discovery costs and overhead at $600. Add in $200 for taxes and you get US$1500.00 as the replacement cost for an ounce of gold.

Using the all-in figure provides a more accurate and definitive picture of actual mining cost and profit.

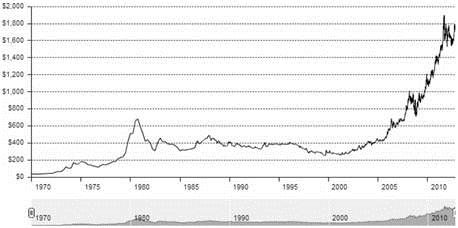

Also, according to CIBC World Markets, the sustainable number gold miners need is $1,700/oz. The long term gold price chart from the World Gold Council shows gold has been in consolidation since late 2011.

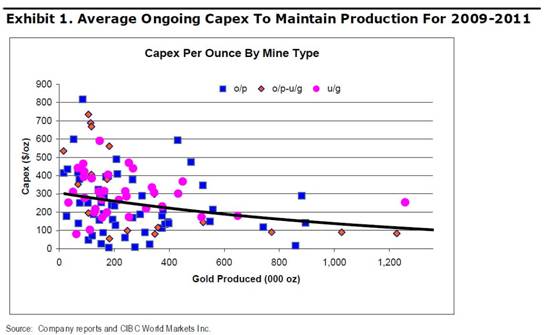

Capital inputs account for about half the total costs in mining production - the average for the economy as a whole is 21 percent. Obviously many of the costs, once incurred, cannot be recovered by sale or transfer of the fixed assets.

Mining is an extremely capital intensive business for two reasons. Firstly mining has a large, up front layout of construction capital called Capex - the costs associated with the development and construction of open-pit and underground mines. There are often other company built infrastructure assets like roads, railways, bridges, power generating stations and seaports to facilitate extraction and shipping of ore and concentrate.

Capex costs are escalating because:

- Declining ore grades means a much larger relative scale of required mining and milling operations

- A growing proportion of mining projects are in remote areas of developing economies where there's little to no existing infrastructure

Secondly there is a continuously rising Opex, or operational expenditures. These are the day to day costs of operation; rubber tires, wages, fuel, camp costs for employees etc.

The bottom line? It is becoming increasingly expensive to bring new mines on line and run them.

"In the next few years, escalating costs, talent shortages and competing infrastructure builds will make it very difficult for mining companies to complete their capital projects on time and on budget. These types of cost and time overruns can create significant risks for miners, including the danger of scaring off potential investors." Deloitte, David Quinlin, European Mining Lead, Switzerland

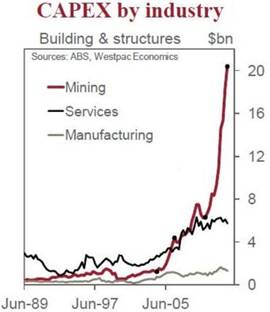

Since 2006 the major gold producers have spent 40 percent of their entire market capitalization building new mines. As you can see in the chart below it isn't going to get any cheaper - major miners will need to spend 60 percent of their market capitalization building new mines in order to sustain the same level of production going forward.

The major gold producers desperately need to replace their mined gold reserves yet can't afford to build many of the large deposits slated to be built.

The reasons behind flat-lining gold production, and record cash and all-in costs, are numerous:

- Production declines in mature mining areas

- Slower than expected ramp-ups of output

- Development time up

- The entire resource extraction industry suffers from a lack of skilled people

- Extreme weather

- Labor strikes

- Protests

Additional challenges include:

- Increasingly more remote and lacking in infrastructure projects

- Higher capex costs

- Increased resource nationalism

- Increased environmental regulation

- More complex metallurgy

- Lower cutoff grades

The declining mined and mineable gold grade is a direct result of the industry's inability to discover new high grade/high margin deposits.

Junior market caps have been savaged - 25 percent of the stocks on the TSX.V are under a nickel, another 25 percent are under a dime 50 percent of the stocks trading on the TSX.v are under a dime, a total of 70 percent are under .20 and 80 percent are under .30 cents. Less than 20 percent of stocks on the Venture are over .30 cents and only seven percent of stocks are over a dollar.

Producers are not able to replace their reserves because there's a lack of discovery, few large high grade deposits are being discovered and most of those that have been discovered aren't owned by producers

"Today, the major producers and their majority-owned subsidiaries hold 39 percent of the reserves and resources in the 99 significant discoveries made in the past 15 years." Metals Economics Group (MEG)

The junior exploration sector is presently in the midst of one of the worst financing environments ever experienced by the sector.

One market analyst recently said that out of the 1800 companies he tracks, as many as 524 have less than $200,000 in working capital.

With today's extremely low share prices, financing - if money is even available - is going to massively dilute shareholders forcing a tremendous number of future rollbacks.

Financing for many juniors is going to be challenging very ironic that just a few short years ago, with gold at only $400 oz, it was much, much easier to raise money then today with gold at $1700.00 oz! Those juniors with some money, and not wanting to excessively dilute shareholders raising more with devastated share prices, will conserve their cash and drastically cut expenditures.

The outlook for many juniors in 2013 is grim, many will not survive. Expect rollbacks, property sales for cash, shares for debt and mergers and acquisitions (M&A) to become the norm. Exploration will drop, the discovery of the future supply of gold, silver and other metals will be put on hold.

A Junior exploration company's place in the food chain is to acquire and explore properties. Their job is to make the discoveries that the mid-tiers and majors takeover and turn into mines. Junior exploration companies own the majority of the world's future gold mines.

The juniors who do have money for exploration and development of their properties, and those few who can get financed, will be well rewarded in the market place for discoveries and bringing the lowest cost projects to production.

This author believes that there is exceptional, and as of yet, undiscovered value in junior companies with quality assets in safe stable countries.

The bottom line for investors in the resource sector is that many juniors working in safe stable jurisdictions, already own what the world's mining companies increasingly, desperately need.

Ahead of the Herd has posted a short list of junior resource precious metal companies with defined deposits operating in North America. The AOTH list is free, you may access it here.

Rick Mills

Ahead of the Herd

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.