A streaming company provides financing for precious metal mining companies in the form of a 'gold streaming deal' whereby an upfront cash payment is exchanged for a percentage of gold production from the mine. You can think of them kind of like a bank, but for mining companies.

The streaming company makes an advance payment to a company with a pre-production stage mineral deposit, and in exchange, negotiates a percentage of the metal produced for the life of the mine. The finance model has also been called a volumetric production payment transaction and originated in the oil and gas sector.

The first company to apply this model to the mining industry was Silver Wheaton(SLW), which remains the largest precious metals streamer today with a market cap of roughly $14 billion.

Streaming companies are similar to the more widely-known royalty companies, which secure GSR (Gross Smelter Revenue), NPI (Net Profit Interest), GPR (GROSS PROCEEDS ROYALTY), (NET SMELTER ROYALTY) or some variation. The main difference is that royalty companies are not paid in gold or silver and do not need sustained capital expenditures going forward except the one time upfront payment when an acquisition is made. The best example of a royalty company today is Royal Gold (RGLD).

Other companies, such as Franco-Nevada (FNV), use a mix of both streaming and royalty deals in their business model. For the purposes of this article, I will focus on streaming companies, as I find their business model more attractive and they have outperformed royalty companies by a wide margin.

Advantages of the Streaming Model

There are considerable advantages of a streaming company including:

1) Diversification A streaming company has agreements with multiple miners, thus spreading and mitigating any potential risk. The larger companies have dozens of deals and multiple streams of income.

2) Unlimited Upside Potential Since the deals they secure are usually for a percentage of the mine's production for life, the streaming company stands to benefit immensely if new zones are discovered and actual production comes in higher than originally forecasted. This occurs all of the time in the industry, as drilling delineates new resources, either increasing annual production or vastly extending the life of the mine.

3) Limited Downside Risk While a miner may see profit margins squeezed as the cost of production rises, the streaming company typically has a contract for a percentage of the gold/silver production, thus eliminating the issue of rising costs. Royalties are paid out of top-line revenue before any operating expenses are accounted for. In addition, the contracts usually contain a number of provisions protecting the streaming company in the event of fraud, misrepresentation, etc. This is all on top of the considerable due diliegence that is exercised before entering into any streaming deal.

4) Favorable Tax Treatment Streamers enjoy a favorable tax situation courtesy of the Canadian Government. As long as they reinvest their proceeds or pay it out as dividends, they are gifted with a tax rate in the neighborhood of 0-8%. That's a huge advantage when it comes to net profit margin.

So, with all of the upside potential and little of the downside risk with mining, what is not to like? Actually, not much, and this is reflected in the performance of streaming companies versus physical metals or miners.

Case Study of Sandstorm's Luna Deal

Let's take a quick look at how a typical deal works, with an example from one of the top-performing streaming companies, Sandstorm Gold(SAND):

We will focus on one of Sandstorm's earlier streaming deals with Luna Gold and take a very high level view for simplicity sake. The cost to Sandstorm for the Luna royalty was US$17.8 million in cash and 5.5 million shares of Sandstorm. In return, Sandstorm is entitled to purchase 17% of the life of mine gold produced from Aurizona, at a per ounce price of US$400.

At the time of the deal, Luna's 43-101 resource estimate on the Aurizona deposit was just over 1 million ounces of gold. If that was the limit of the deposit size, then Sandstorm would purchase, over time, roughly 200,000 ounces at a cash cost of $400 per ounce. This would net Sandstorm $100 million ($900 per ounce gold $400 per ounce cost = $500 per ounce X 200,000 ounces). We then deduct the $17 million payment and the cost of the 5.5 million Sandstorm shares at the time of the deal (roughly $0.40 per share) and we can see that Sandstorm stands to pocket over $80 million from an initial investment of $20 million. This equates to a return of around 400%!

Now the really juicy part that highlights the benefits of the streaming model. The Aurizona deposit has since tripled to over 3 million ounces and the price of gold has doubled from $900 to around $1,800 per ounce. So, for Sandstorm's original investment of about $20 million, they now stand to make roughly $600 million from the deal (original estimate of $100 million x 3 for tripling resource x 2 for doubling gold price). That is a return of nearly 3,000%, all from a single streaming deal!

Sandstorm and other streaming companies get to ride the exploration upside at no additional cost. The risk to Sandstorm is almost entirely confined to the commodity price. And even if the gold price were to drop below the agreed upon purchase price of $400, Sandstorm still gets to buy the gold at the lower of the agreed upon price and the market price, which means a break-even transaction in the event gold goes below $400. Again, streamers benefit from all of the upside potential, yet none (or little) of the risk.

It may seem hard to imagine how this type of deal would be good for Luna Gold or the dozens of other miners inking deals with streaming companies. But when credit markets dry up, this structure is arguably preferable to debt or significant shareholder dilution. After all, nobody is forcing the miners to work with Silver Wheaton or Sandstorm Gold. Their boards have obviously considered the option and decided that working with a streamer is most advantageous for one reason or another.

Sandstorm Resources (now Sandstorm Gold) was founded in 2008, when Nolan Watson and David Awram decided to create a metal streaming company that would be focused on gold acquisitions. Both Watson and Awram were former employees of Silver Wheaton, the first organization to apply this financial model to the mining industry. Let's take a quick look at how well this model has been performing, both in the short-term and longer-term.

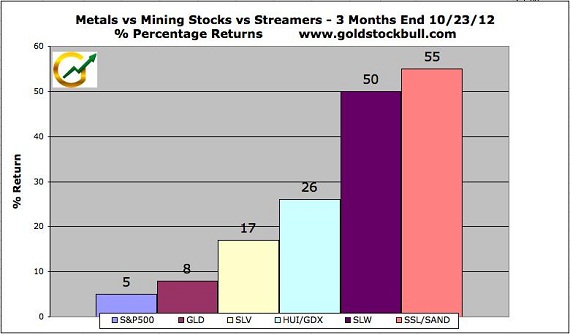

Performance Comparison Gold vs. Silver vs. Gold Stocks vs. Streamers

First, I pulled data over the past three months, to capture performance during the current rally. During this time, gold is up 8%, silver is up 17% and the Market Vectors Gold Miners ETF (GDX) is up 26%. Those are all impressive gains for such a short time frame, with the S&P500 index up only 4.6%. However, during this same period, the streamers are up more than 10 times the S&P 500, 5 times gold and roughly double the gold miners ETF. Silver Wheaton is up 50% and Sandstorm Gold is up 55% in the past three months alone!

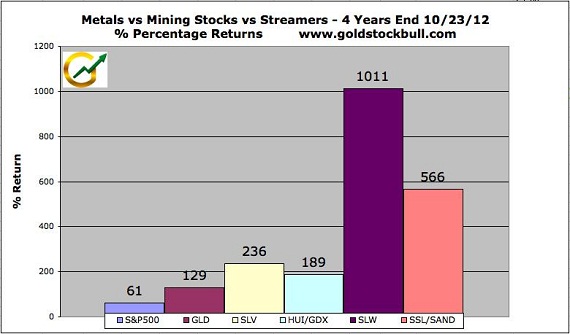

To make sure that we aren't charting a short-term performance anomaly, I also charted the 4-year percentage returns since the financial crisis. Gold is up 129%, silver is up 236% and the gold miners ETF is up 189%. Spectacular results all around, with gold up more than double the S&P500 and silver up nearly 4 times the market. But again, it was the streamers that blew the doors off, putting in gains of 1,011% for Silver Wheaton and 566% for Sandstorm Gold! Those numbers translate to annual gains that even the most successful hedge funds would drool over.

Parting Shot

The next time an analyst, CNBC talking head or investment "expert" warns against gold and calls it a "barborous relic," you might want to show them these charts. And if you are looking for leverage to the advance in precious metals and don't yet have a streaming company in your portfolio, hopefully this article provides some insight and inspiration.

In my estimation, both the gold and silver price have much higher to go before reaching a top. John Williams of ShadowStats has calculated the true inflation-adjusted high for gold at $8,890 and for silver at $517. This is assuming a return to 1980 pricing, but the conditions that caused that spike are much more severe today. So, I think there is a good chance of those targets, despite seeming lofty today, being easily surpassed.

$8,890 gold and $517 silver represent upside of more than 400% for gold and 1,500% for silver. Given the type of leverage we have seen from the streaming companies and select mining stocks, the potential gains are truly astronomic. With governments worldwide embracing quantitative easing, central banks buying huge quantities of gold, and investment demand for silver rocketing higher, precious metals remain one of the best investments of our time.

The Gold Stock Bull newsletter has been recommending streaming companies for several years now. If you would like to receive the newsletter and view all of the stocks in the GSB portfolio, click here to sign up now!

Jason Hamlin

GoldStockBull