The Gold Report: John, as Mark Twain famously quipped, "There are three kinds of lies: lies, damned lies and statistics." The Bureau of Labor Statistics (BLS) just came out with new jobs numbers that show the country added 114,000 jobs since September and the unemployment rate dropped to 7.8%, down from 8.1% in August. On Shadowstats.com, you argue that the numbers are wrong and pointed to politics as a possible reason for the incorrect figures. Are unemployment statistics being manipulated and if so how?

John Williams: I normally put out a commentary on the numbers, and, in this one, I raised the possibility of politics as a factor. The problem is very serious misreporting of the numbers and the result is what appears to be a bogus unemployment rate. The BLS reported a drop in the unemployment rate from 8.1% to 7.8%, three-tenths of a percentage point, which runs counter to what is being experienced in the marketplace.

What few people realize is that the headline unemployment rate is calculated each month using a unique set of seasonal adjustments. The August unemployment rate, which was 8.1%, was calculated using what BLS calls a "concurrent seasonal factor adjustment." Each month the agency recalculates the series to adjust for regular seasonal patterns tied to the school year or holiday shopping season or whatever is considered relevant. The next month, it does the same thing using another set of seasonal factors. Rather than publish a number that's consistent with the prior month's estimate, it recalculates everything, including the previous month, but it doesn't publish the revised number from the previous month.

The assumption is that the monthly recalculations don't make much difference over time, but they do. The depth and the protraction of the current severe economic downturn have thrown off the annual seasonal-factor adjustments. The result is very volatile seasonal factors month-to-month. That means the new calculations for the September number may have resulted in a very significant revision to the August number. Again, though, the BLS doesn't publish that, so the headline August-to-September 2012 change in the unemployment rate is not consistent and not comparable. Last December, when the BLS put the seasonal adjustments on a consistent basis for the year, as it does once per year, the November 2011 unemployment rate had just been reported as showing four-tenths of a percentage point dropan unusually large monthly decline that never took place. When revised to a consistent basis, the drop in headline November unemployment revised to two-tenths of a percent. That is a big change. I think something like that happened here.

The BLS knows what the actual number is. It has an actual estimate for August, which is consistent with September, but it doesn't publish it because it says it "doesn't want to confuse data users." But it is putting out numbers that have no meaning month-to-month. One month before the election and a month after Federal Reserve Chairman Ben Bernanke announced Quantitative Easing (QE) 3, is not a time to have inaccurate numbers. The BLS should publish the consistent numbers now.

TGR: You have said that BLS has been using this recalculation method for years. Do you feel that this month the numbers were more skewed than usual because of the political timing?

JW: Because there is no transparency in the calculation and reporting process, it leaves open the possibility of manipulation. What has happened here, though, is that in the wake of the economic collapse, the seasonal factors have been heavily distorted and are not stable on a month-to-month basis. Where the concept originally might not have made that much of a difference, it does make a big difference now. I suspect that is why we woke up to such a screwy unemployment rate this time around.

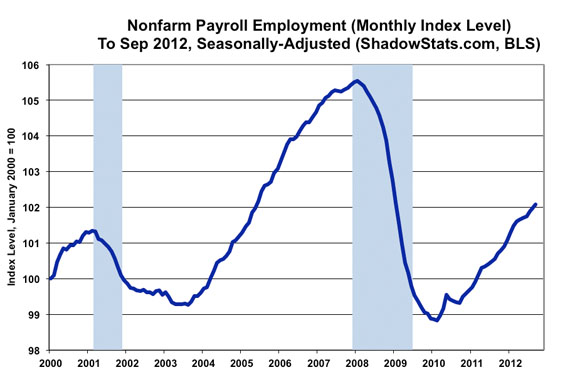

The 114,000 jobs growth in the payroll survey (which reflects the number of payroll jobs, counting multiple jobholders more than once) also is suspect and subject to concurrent-seasonal-factor adjustments. There, however, the BLS publishes revised estimates for the two prior months that are on a consistent basis with the headline number. Nonetheless, jobs in even earlier months are not re-reported, although they too are recalculated each month, with the effect that jobs reported in earlier periods can be moved into present reporting, boosting the current numbers, without the related earlier changes being revised in the published historical numbers. Nonetheless, the purported 114,000 jobs gain was not statistically significant.

From the household survey, which gives us the unemployment rate and counts the number of people who are employed (multiple-job holders are counted but once), the headline gain in employment was 873,000, the largest seasonally-adjusted monthly increase since Ronald Reagan's first-term. That number clearly is nonsense and again suggests there is a severe problem with the seasonal factors.

TGR: Do you think the unemployment rate was manipulated on purpose or did the bad economy just make the reporting more confusing?

JW: It could have been manipulated. I do not know and do not have direct evidence of current political massaging of the data. I know for certain that there have been direct political manipulations by different administrations, since the days of President Lyndon Johnson, involving various data sets that have included the gross domestic product (GDP), the trade numbers and the employment and unemployment numbers.

From what I've seen of the Obama administration, the reporting has been reasonably clean. Nonetheless, at best, the administration is using seriously flawed data, and the reporting and calculation process has the potential for manipulation. The timing of the announcement of such a big downside swing in unemployment certainly is a fortuitous circumstance for the administration's political needs.

Main Street U.S.A., however, has a much better sense on the economic reality than do the government's economic statisticians. If the headline unemployment rate is not as advertised, a goodly portion of the public will not buy it. Past experience has shown gimmicked reporting often backfiring on the manipulators.

TGR: What is the correct unemployment rate? What would be a reliable data set?

JW: I don't know of one. The unemployment rate comes out of government surveying and data manipulation, and the base number is wrong. What are good in theory are the un-adjusted numbers, although unemployment definitions still suffer. Those don't get revised for the seasonal factors. But there you have regular annual patterns of economic activity, so you'll see the unemployment rate go up and down as it follows the normal flow of annual business activity through the various seasons. Even so, it makes some sense to look at that unadjusted series over time. The average person doesn't think of himself or herself as employed on a seasonally adjusted basis, but a lot of people, according to the government, are so employed.

If you surveyed everyone in the country as to whether he or she were unemployed, you'd get an unemployment rate above 22%, instead of the headline 7.8%. The difference is in how the government defines whether someone is unemployed, versus the view from common experience.

TGR: What are the ultimate consequences of inaccurate statistics on the stock market, commodity prices and everyday people?

JW: Right now, the impact of the unemployment numbers is mostly political, although the Federal Reserve has made it part of its targeting in terms of QE3. But the primary political concerns are on the impact to the upcoming election, which is what makes the timing of this release so suspect.

There is a serious problem with the reporting. If it has been used to manipulate the public, that eventually will come out. If it hasn't, the simplest thing is for the BLS just to publish the actual numbers. They have them. They don't have to do any recalculations. They've already done that. They just need to publish them in a timely manner.

TGR: There seemed to be an impact on the stock market. The Dow ended Friday up. Was that simply a coincidence?

JW: Yes, the market jumped all over the place. But I see no rationale whatsoever behind the movements in the stock market. Any numbers will be used to spin a story that will explain what's happening with stocks at a given point in time.

TGR: What about commodity prices? What will this do to gold?

JW: You had some sell-off in gold Friday. Again, that could all be spin. Was it due to people thinking Bernanke was not going to have to ease monetary policy as much? I'm not into day-to-day calling of the markets. The stock market is absolutely irrational. You can make up all sorts of stories based on that. Markets respond to lots of really worthless informationthe 114,000 gain in payrolls for example is not statistically meaningful. It could have been a contraction as well as a gain, when the 129,000-job margin of error is considered. Yet, the markets gyrate wildly over very small changes that have no relationship to what's actually happening in the economy. I think traders just love to trade. It's like going to the racetrack and betting on a horse because of how it wiggles its ears. It has little to do with the underlying fundamentals.

TGR: Is there an ultimate consequence of having faulty data? Do incorrect numbers build on themselves and become more inaccurate over time? Will we see a jump in the unemployment rate in December when they are recalculated after the election? Are there other consequences?

JW: When governments use bad numbers, and believe them, they don't respond appropriately to problems like unemployment and inflation. People don't properly target their investment returns or adjust their income projections. There are good reasons for having accurate information, but accurate numbers just are not coming out of the U.S. government at the moment.

TGR: You mentioned the correlation with the announcement of QE3. When we talked in May, you called QE "dangerous" and said it would eventually lead to a massive decline in the U.S. dollar, triggering new dollar selling and lead to dollar inflation, spikes in oil prices and eventually hyperinflation. Your special commentary on inflation and systemic conditions comes out next week on ShadowStats. Can we expect any good news?

JW: The outlook hasn't changed. I've been looking at this for a long time. Let me put it this way: The economy is not suddenly improving. Underlying fundamentals have not changed. You just are getting bad-quality numbers.

The average guy has a pretty good sense of what is going on. When Main Street suddenly starts getting jobs and businesses pick up, then we will know the economy is picking up. Shy of that, I'd be wary of anything I hear out of the government on business activity.

TGR: So the reports that we are in a recovery aren't accurate? What indicators should we be watching?

JW: Over time, you will find the better-quality statistics are confirming that we never had an economic recovery, and that we're not about to get one. When you have faulty numbers, you need to look at the underlying fundamentals to see what's happening. The problem is the consumer doesn't have the liquidity, either from the standpoint of income growth or credit availability, to sustain positive growth in the GDP.

TGR: Thank you for your time, John. We will check in with you periodically to see if you see any changes in those numbers.

Walter J. "John" Williams has been a private consulting economist and a specialist in government economic reporting for 30 years. His economic consultancy is called Shadow Government Statistics (ShadowStats.com). His early work in economic reporting led to front-page stories in The New York Times and Investor's Business Daily. He received a bachelor's degree in economics, cum laude, from Dartmouth College in 1971, and was awarded a Master of Business Administration from Dartmouth's Amos Tuck School of Business Administration in 1972, where he was named an Edward Tuck Scholar.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise. Charts provided by Shadow Government Statistics. Interviews are edited for clarity.