Related Articles:

How to Minimize Risk and Increase Returns on Juniors: Joe Mazumdar

Mining Equity Bargains Abound, But Buy with Care: Ivan Lo

Grade Is King: Andrew Richmond

Gold's historic run-up from $250 to nearly $2,000 an ounce in the last 10 years has underlined the long-term value and intrinsic worth of a key asset. It has also provided a fabulous, once-in-a-lifetime investment opportunity for many individuals, not to mention a long-term momentum trade for both retail and institutional investors.

Gold has also provided investors with an important lesson in the past year: despite its distinctive safe-haven value, the metal definitely has a speculative element that's critical to its price appreciation. In this regard, gold is no different than other assets. Gold's speculative element was nowhere more evident than in the series of margin requirement hikes last summer, which saw gold fall from an all-time high of just under $2,000 an ounce to a low of around $1,550.

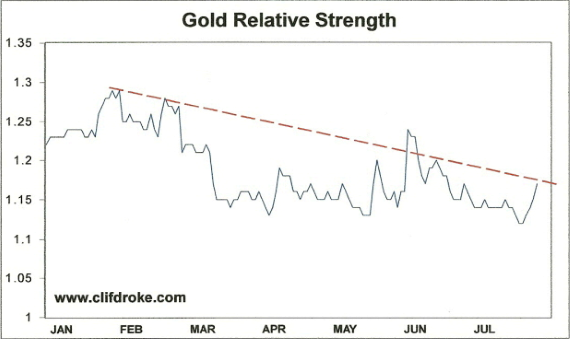

During the 2008 credit crisis, gold benefited from a combination of bullish factors. At the bottom of the crisis in late 2008 -- and well before the smoke finally cleared from financial markets in March 2009 -- gold got the benefit of relative strength versus the equity market. Hedge funds and institutional traders are constantly on the lookout for markets and investment opportunities that are outperforming the general equities market. Compared to the benchmark S&P 500, gold was a shining example of relative strength and it quickly caught the eye of big money traders in the latter part of 2008. indeed, gold became the ultimate relative-strength play in the early stages of the 2009-2011 global recovery.

Gold And QE

Aside from relative strength and valuation considerations, gold also benefited from successive quantitative easing initiatives undertaken by the Federal Reserve between 2009 and 2011. The gold market was a huge recipient of so-called 'hot-money' inflows that resulted from the excessive liquidity generated by QE1 and QE2, both of which helped propel gold to all-time highs.

Fast forward to the summer of 2012 and we find gold in the opposite position it was between 2009-2011. It no longer has the benefit of relative strength and the residual effects of QE2 have long since faded. Worse still (from an intermediate-term perspective), gold doesn't even have the benefit of the leveraged, speculative traders prior to the CME Group's margin hikes last summer. Gold has been forced to undergo a long period of quiet consolidation as the trend-trading crowd seeks opportunities in other markets.

What's Missing

What will change this situation and generate a return of the speculative element so critical for gold's success? One of two possibilities exist for the interim outlook. The first possibility is being widely discussed by investors today, namely a third quantitative easing program (QE3), which is the least likely scenario for fueling a near term gold breakout. A third QE program during an election year would be politically toxic and too controversial to be considered -- barring a massive deterioration in the global economy and financial market between now and November. Moreover, Fed Chairman Bernanke isn't likely to prime the liquidity pump anytime soon given the relatively high levels of prices for both equities and consumer prices.

The second possibility for a gold turnaround is the one most likely by year's end. A conspicuous increase in gold's relative strength would do much to attract the attention of market-moving hedge funds and institutional investors. This could easily be accomplished, even if gold does not break out from its consolidation pattern anytime soon. Indeed, gold need only remain within its lateral trading range of the past few months. That's essentially what happened in the latter part of 2008, which saw the last four-year cycle peak. The fourth quarter of 2008 also provided gold with its opportunity to shine vis-à-vis equities.And that could easily be repeated later this year in Q4.

When Will It Break?

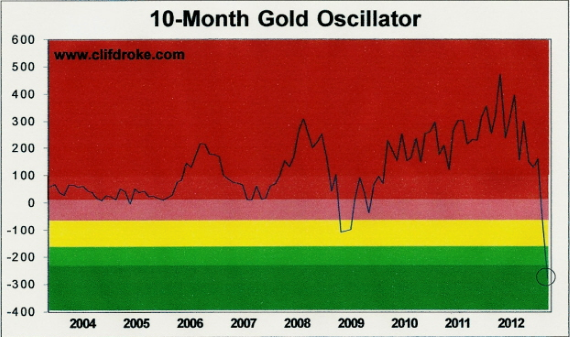

If history repeats, gold will, by this fall, be poised to benefit from both a relative strength increase as well as an historic long-term "oversold" signal (discussed in previous commentaries, see chart below).

There are several prominent trouble spots in the global economy that could easily metastasize and reach crisis proportions by 2013. I'm referring to the European debt problem, China's economic slowdown and next year's looming tax increases in the U.S. Gold will, once again, resume its traditional safe-haven role once concern over these problems reaches a boiling point and morphs into full-fledged fear.

There are two stages during the 60-year economic cycle when gold ownership is most desirable: 1) during the peak phase of the cycle when runaway inflation reaches its apogee, and 2) the trough of the cycle, when extreme deflation is at its worse. We are about to arrive at the end of the cycle when deflationary undercurrents that damaged the economy in recent years will accelerate and become uncontainable. It's in just such a ravaging environment that gold will truly shine.

Clif Droke

Gold & Silver Stock Report