"Gold in dollars just went flat from 12 months ago. But in euros. . ."

Friday the 13th saw the gold price in dollars do something it's managed only seven times in the last 11 years.

Gold traded flat from 12 months before.

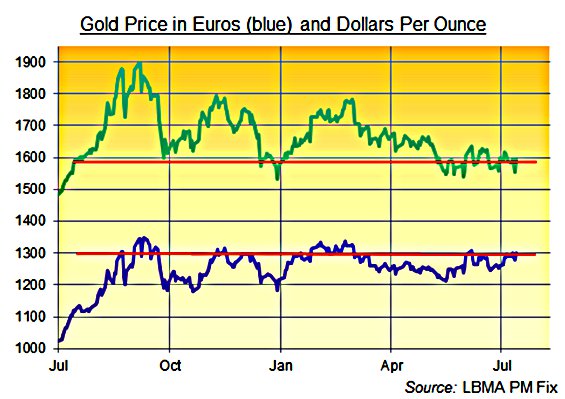

So if you bought on July 13, 2011, you hadn't made a dime by the time New York got itself showered and brushed its teeth this morning. You held just the same dollar-value one year laterbasis the London AM Fixat $1,579/ounce.

Between then and now, in fact, anyone buying gold to insure, hedge or speculate-to-accumulate with their dollar savings was more than likely to have paid a higher price, too.

The gold price in dollars has been higher than it was Friday morning on 227 trading days. All of them came after July 13, 2011. Half of them were in 2011, and the other half here in 2012. Only 25 trading days saw gold below where it stood this morning. Even Friday afternoon's little pop to $1,595/oz left gold in dollars badly lagging the last 12 months' average.

Now contrast that with the gold price in euros today. It's only been higher on 45 trading days. Recording a London Fix of 1,300/oz Friday afternoon, in fact, gold has gained 16% for Eurozone buyers from this day last year.

How come? Most obviously, the euro has of course fallen versus the dollar. So what has been flat for U.S. investors has risen for investors in France, Germany, Italy and the other 14 single-currency states. But what's driven that fall in the Euro highlights both why people buy gold, and what it can help do for them when they do.

The Eurozone crisis might well worsen the economic slowdown worldwide. A true sovereign defaultor exitwould most likely spark the kind of globalized panic not seen since Lehmans failed, or worse. But until then, the focus of these rising tensions is squarely inside the single-currency zone. And if you're buying gold to insure against that kind of concern, it's asking a lot to get insurance on other people's localized crisis as well.

The dollar's rapid tumble of 20022008, for instance, sparked much debate and anxiety about the U.S. currency's role as world #1 reserve. It left euro gold prices pretty much untouched, however, until the financial crisisseemingly localized in the U.S. housing and mortgage marketrevealed itself to be all too international.

Again, the rising temperature in Europe todaywhat the World Gold Council's Marcus Grubb calls "the ambient temperature" of what is now a permanent emergencymay well prove hot for dollar, sterling and yen investors too in due course. Meantime, gold is holding near its all-time record highs for Eurozone citizens. That's a clear sign that the ambient temperature, the background radiation, of this crisis is also dangerously strong.

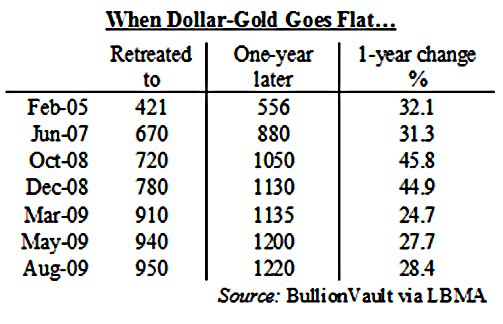

What if the emergency's focus expands to include the dollar, or switches to the U.S. fiscal cliff, zero-rate policy, or long-term structural bankruptcy of the fifty United States? Of those 7 occasions since summer 2001 when the gold price in dollars has been flat from 12 months beforelike it is today then buying that dip has proven a winning trade.

The minimum return 12 months later again has been 25%. On average, buying gold when it's gone nowhereor slipped a couple of percent from a year earlierhas returned 33% for U.S. investors over the following year.

A repeat is far from guaranteed, of course. There's always the possibility that, unlike on the seven previous occasions shown above, the gold price has now slipped out of its bull market. And barring a sharp jump in the next two weeks, gold in dollars will soon be so far under-water from 12 months ago, it'll be drowning compared to the record highs of August and September 2011.

Dollar investors and savers wanting to buy bargain insurance, however, would be forgiven for thinking the financial crisis is a long way from finished just yet.

Adrian Ash

BullionVault

Adrian Ash is head of research at BullionVault the secure, low-cost gold and silver market for private investors online, where you can buy physical gold today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

(c) BullionVault 2012

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events and must be verified elsewhere should you choose to act on it.