Most micro-cap resource stocks have been underwater since a four year high ended in early March 2011 with the Toronto Venture Exchange Index down over 50% since that time. Stock performance has been abysmal despite record or near-record prices for most commodities in 2011 and continuing high prices in 2012.

Many factors have contributed to the decline in junior exploration and mining stocks and I see little evidence for a quick recovery. However, stock markets, and certainly yours truly, will always find something to be long on. That current something for me in the junior resource sector is graphite.

Along with diamond, graphite is an allotrope of the semi-metal element carbon. However, it has almost the exact opposite physical and chemical properties. Graphite is gray to black, opaque with a metallic luster, a soft mineral with Mohs hardness of 1 to 2, and arranged in parallel hexagonal sheets. It is chemically inert and flexible, yet very strong. Graphite is of low specific gravity, highly refractory with a 3927 C melting point, and electrically and thermally conductive. Its unique characteristics have led to many industrial applications. Graphite deposits occur in high-grade metamorphic rocks that are widespread and abundant across the Earth. They tend to be small deposits that make low-cost mines.

Graphite is much more than the lead in your pencil and the carbon fiber additive that lets you "grip it and rip it" with a big-headed composite driver. These uses actually constitute a small part of demand. Three quarters of the world's graphite is used in traditional applications such as steel-making, foundry moldings, refractories, auto parts, and lubricants. Minor uses include batteries, pencils, electronics, and numerous other products. Significant future demand growth is projected to include fuel cells, lithium-ion and vanadium redox batteries, and pebble-bed nuclear reactors. Development and commercial application of the much-ballyhooed graphene (single atom layer graphite) technology is a decade or more away.

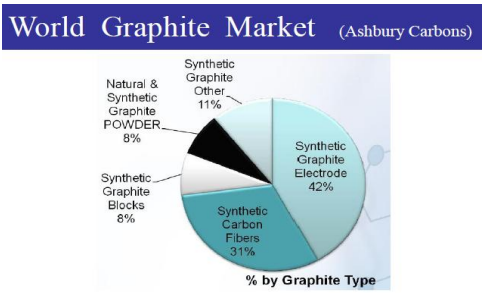

The graphite industry is divided into three parts: natural, synthetic, and carbon fiber. Supply cannot meet current demand, and prices have risen substantially since late 2009. The world market is worth about $13 billion per year, of which $8 billion is synthetic graphite, $4 billion is carbon fiber, and $1 billion is natural graphite. It is further broken down into these sources:

Synthetic graphite and carbon fiber are high purity, expensive forms produced from petroleum coke, primarily in the United States with significant exports to other consuming countries. They constitute the majority of graphite demand.

Natural graphite production is mainly from small underground mines in China. By the early 2000s, graphite mines outside of China were rendered uneconomic when it flooded the market and drove prices down. World production totaled about 1.1 million tonnes in 2011 with an estimated 75 % coming from that country. Other countries with significant graphite mine production include Brazil, North Korea, Canada, India, Romania, Ukraine, Mexico, Madagascar, Austria, Turkey, and Sri Lanka.

Three types of natural graphite are produced:

Vein, aka lump graphite, is coarsely crystalline, a small specialized market, and the highestpriced natural graphite. It is produced from Sri Lanka mines by hand-sorting and comprises only 1% of the market.

Flake graphite is categorized by crystal size with large (+80 mesh), medium (-80 to +100 mesh), and fine (-100 to +300 mesh). Marketable products must grade 94-97% graphitic carbon (Cg) and are used for both traditional and new applications. Flake constitutes 49% of the market.

Amorphous powder graphite a misnomer. It is actually crystalline but very fine grained (-300 mesh). At 80-85% Cg, the amorphous variety is used for lower-priced applications and amounts to 50% of the total natural graphite market.

In general, larger crystal sizes and higher Cg content command higher prices per tonne.

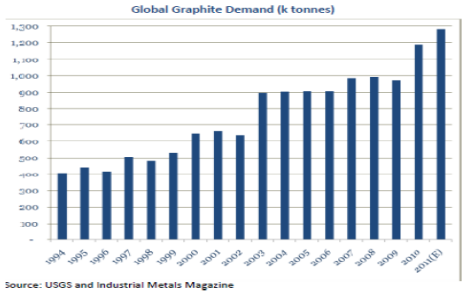

Demand has increased over the past 18 years, although not exactly year over year. The natural graphite industry is strongly correlated with world economic health, illustrated by the chart below:

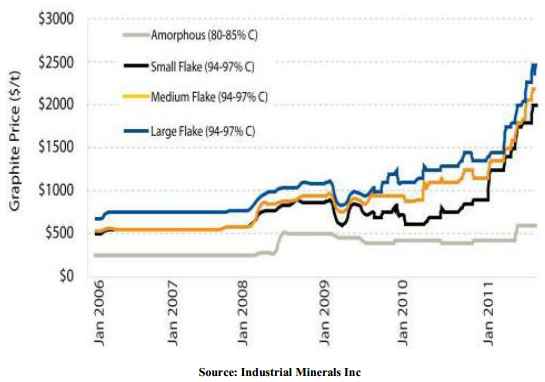

Rapid growth in demand has led to significant price increases over the past three years:

Many specialized markets command premium prices but require further purification and processing. Examples include spherical graphite, necessary for Li-ion batteries, and expanded graphite, used increasingly in heat-sensitive applications.

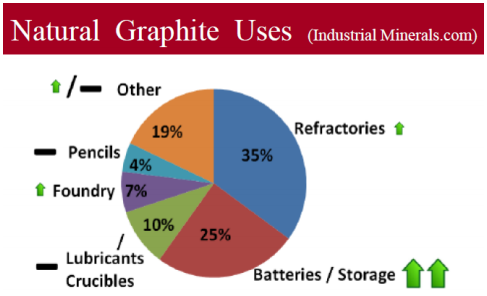

Natural graphite uses are broken down as follows:

Growing users include the refractory and foundry industries and especially the battery sector.

Reminiscent of the rare earth element run-up in 2009-2010, the graphite boom is driven by these catalysts:

Prices have increased because traditional demand exceeds mine supply. New technology applications have favored flake graphite, widening the price gap over amorphous graphite.

China has few flake deposits and mostly mines low-value amorphous graphite underground.

With domestic demand growing, China is restricting exports thru taxes and licensing and may impose export quotas.

China is rationalizing its fragmented industry into a state-sponsored monopoly or oligopoly to remediate environmental degradation, improve labor standards, and address infrastructure and transportation problems.

The Western World views dependency on Chinese graphite as an unreliable and capricious source.

With rising prices, new export policies, and consolidation in China, graphite companies have been successfully promoted with dramatic increases in market capitalizations.

Like the REE bubble in 2009-2011, graphite is now the "Next Big Thing."

Also much like the rare earth elements, graphite deposits are plentiful and occur worldwide. The best deposits are restricted to high-grade metamorphic terranes whose protoliths were organic-bearing sedimentary rocks. Most deposits are small, structurally deformed lenses that are irregular in geometry.

One year ago I was aware of two graphite-focused companies on the Toronto Venture Exchange. Based on evaluations of the commodity fundamentals and insight into those particular stocks, I became a shareholder of a private graphite development company that went public in February 2012. At this juncture, these three companies appear to be ahead of the game and are in my opinion "the cream of the crop".

Now it seems every snake, shark, charlatan, and shyster within a half kilometer of Vancouver's Coal Harbor has a new graphite deal via a capital pool company, shell, IPO, or change of business. The bubble has blown up quickly with over 35 listed Venture Exchange companies and more than 50 worldwide that hold graphite projects. There are doubtless many more in process.

Like recent junior sector bubbles (e.g., uranium, lithium, rare earth elements, Colombia gold, Yukon gold), the graphite space will fill with many pretenders amongst the very few contenders. Many will mine the stock market until another next big thing comes along. As per previous booms, 95% or more are destined to fail.

Promotion of micro-cap graphite companies has been tied to future growth of high tech and green tech applications. However, demand from traditional applications is currently pressuring supply, and many mines in China are nearly the end of their productive lives. Therefore, there is optimism that this particular boom will demonstrate some staying power.

My favorite few are graphite developers that have an advanced deposit or a former mine in a geopolitically stable and mining-friendly location, nearby infrastructure including highway, power, water, and port, high-grade (> 5%) and/or a high percentage flake component, open pit configuration with a low strip ratio, and favorable process metallurgy.

Graphite beneficiation uses standard mineral industry technology with crushing, grinding, flotation, drying, packing, and shipping. However, producing a marketable concentrate with >94% Cg content often requires multi-stage processing that reduces flake size. As with most commodities, metallurgy can be a fatal flaw and as always, a graphite producer should fall into the lowest cost quartile of its peers to ensure sufficient margins in times of slow demand and low prices.

Most graphite deposits are small so there should be room for development of a number of mines by competent juniors. Rationalization of the business by merger and acquisition will probably occur and may lead to large, integrated mine-to-market graphite companies. There are a dozen large public and private synthetic graphite and carbon fiber companies worldwide, and they likely will be players as the up-and-coming natural graphite mining sector consolidates.

Graphite does not trade openly and marketing and sales are of utmost importance. Capital expenditures should be significantly less than $100M and at one past-producing mine, capex is projected at under $25M. Project financings are likely to be achieved thru a combination of off-take agreements with strategic partners (consumers and end-users) and private debt instruments (merchant banks, hedge funds, and/or high net-worth investors), and hopefully not by equity raises that tend to dilute and harm early shareholders.

Because mines tend to be small with low capital requirements, the graphite market is more suited to junior companies with limited financial means than the lithium or REE sectors that generally require huge capital expenditures and a major partner.

A graphite company is no different than any other junior resource company. In addition to evaluating its flagship project, we must always assess a company's share structure, the people, and its peer market valuation. In that regard, I urge you to read about my proven evaluation methods and trading philosophy at http://www.MercenaryGeologist.com.

Ciao for now,

Mickey Fulp,

Mercenary Geologist