The more advanced rare earth stocks awoke from their slumber today after China's Information Office of the State Council published a White Paper about its rare earth industry "Situation and Policies of China's Rare Earth Industry") that qualifies as an advance response to the WTO complaint filed earlier this year about China's use of export quotas to restrict supply to the rest of the world.

In its White Paper China reiterates what we have known for some time, namely that it has decided to stop subsidizing rare earth prices by allowing weak or absent and largely unenforced emission standards to dump the real cost of producing rare earths onto its citizens, soil and waters, and to further stop subsidizing cheap prices by tolerating inefficient production and processing methods that are depleting its naturally abundant resource much more quickly than ever expected thanks to innovation and policy developments that have ramped up demand for rare earths during the past decade.

Not articulated in the White Paper is China's plan for a new round of fiscal stimulus by subsidizing to the tune of nearly $100 billion (B) through rebates of domestic consumption of clean energy and technology products. The relationship between rare earths and clean technology deployment is well understood; much of the hostility toward western rare earth companies during the past two years emanated from fossil fuel apologists, climate change deniers, and libertarian right-wingers who see in anything that serves a common good a threat to the freedom of individuals or their corporate surrogates to enrich themselves by dumping costs onto others with no means short of violence to protect against their victimization.

The only sympathy for the non-Chinese rare earth sector from this class arose from uneasiness that the United States military, whose $700B budget is the largest contributor to the federal deficit, might find itself short some inputs critical to enforcing a system of globalized trade where capital invests itself in the jurisdiction most willing to serve as a cost dumping-ground for production. The U.S. Department of Defence (DOD) laughed off this concern because its specific needs are minute, and as long as China remains eager to export its goods to the rest of the world, there will be open channels through which the DOD's critical metal needs can be smuggled.

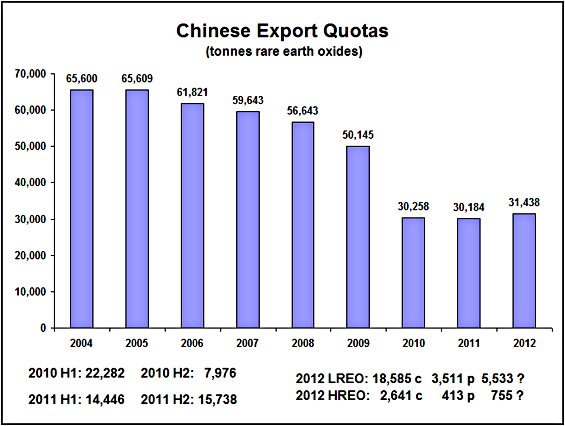

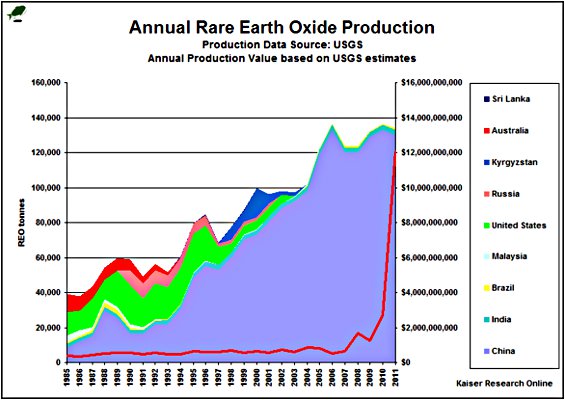

The White Paper does address the smuggling problem, pointing out that China's official rare earth export figures are substantially lower than what it can add up from the rare earth import amounts reported by the customs branches of other countries. From 2006 through 2008 official rare earth imports by the rest of the world were 35%, 59% and 36% higher than China counted and taxed as exports. The White Paper is silent about 2009 and 2010, but it reports that for 2011 rest of world rare earth imports were 120% higher than China's official exports. Despite all the hand-wringing about the curtailment of export quotas in 2010 to 30,000 tonnes, roughly repeated for 2011, just over half of the 2011 export quotas, 18,600 tonnes of the 30,184-tonne quota, were utilized.

Did the soaring FOB spot prices spur massive substitution as the media speculated with active encouragement from end-users? How was it that official Chinese rare earth consumption figures for 2010 jumped to 87,500 tonnes, according to CARE, when experts such as Dudley Kingsnorth were estimating 60,00070,000 tonnes of domestic consumption? The reality was that a good portion of exported rare earths were "domestically" consumed by being fabricated into alloys that were then exported as something other than rare earth products subject to export quotas, while undisguised rare earths were simply smuggled via Myanmar and Vietnam back channels, through which a much larger volume of two-way traffic involving high-value goods flows.

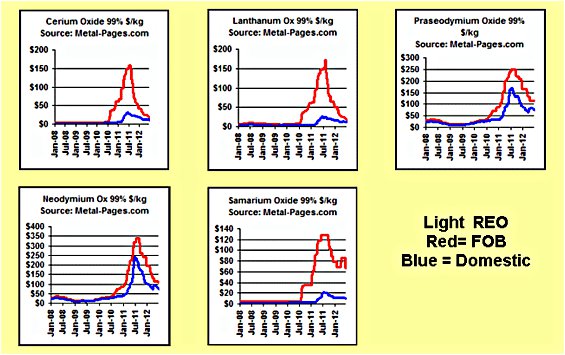

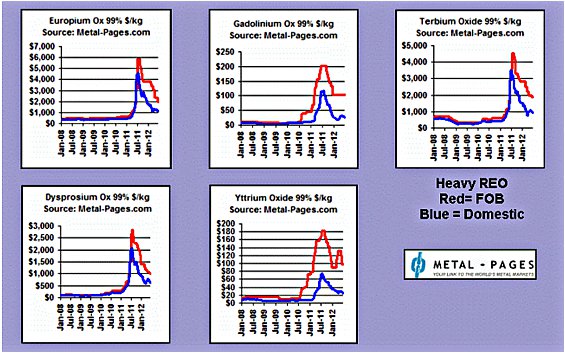

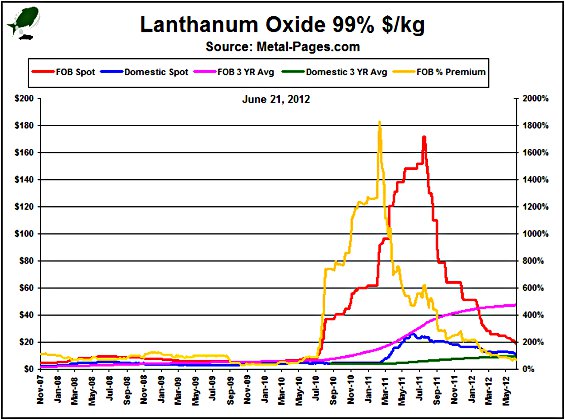

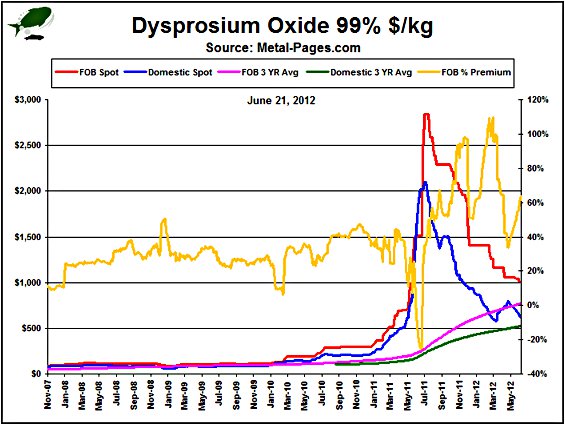

China's poorly thought-out export quota system, which did not distinguish between the lower-value light rare earths and the higher-value "middle to heavy" rare earths, contributed to severe distortions in the FOB spot market, where during the second half of 2010when the curtailed export quotas came into effectthe FOB spot prices of the expensive heavy rare earths maintained their 25% export duty premium over domestic prices, while the FOB spot prices of light rare earths plus the abundant heavy rare earth yttrium achieved 1,000% premiums over domestic prices. That changed in early 2011 when Chinese domestic prices collectively soared as China unleashed its consolidation of the rare earth industry. (The yellow lines in the charts below for the light rare earth lanthanum and for the heavy rare earth dysprosium, which reflect the FOB premium over domestic spot prices, illustrate these changes in differential pricing.)

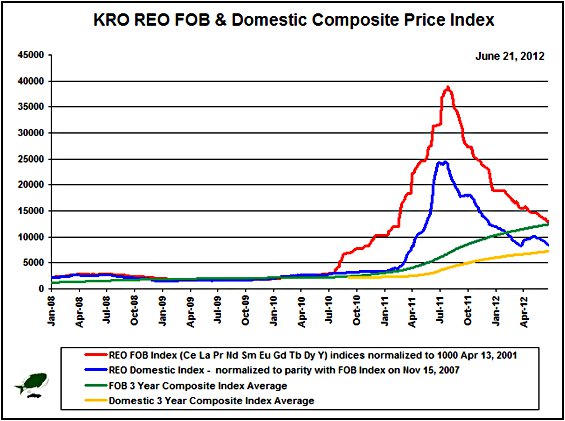

For 2012 China has finally divided rare earth quotas into lights, which are about 85% of the overall quota, while the heavies are 15% of the overall quota, which roughly reflects the distribution of China's overall production profile. As the composite rare earth oxide FOB and domestic indices in the chart below show, FOB prices are still falling while domestic prices are falling again after bouncing off a bottom in early April. The price spike experienced in 2011 for all rare earths in both domestic and FOB markets was created by a western buying panic, which manifested itself through smuggling channels where prices were considerably lower than published FOB prices, and the sellers did not charge Beijing's 15%25% export duty or pocketed it for themselves. The trouble with a capitalist-communist hybrid economy such as China's is that Beijing's best "common good"-oriented intentions get subverted by self-serving Chinese businessmen at every opportunity.

At some point the resulting speculative rare-earth price bubble generated demand destruction as certain rare earth users such as glass polishers simply went out of business, product commercialization plans that relied on rare earths were shelved and others capitulated to China's siren song that factories based in China will always be a preferential recipient of rare earths produced in China. Obviously this was not an option for defense contractors building components for the U.S. military, though it does appear that a fair amount of the electronic military infrastructure was made in China.

Plausible suspicions now abound that the Pentagon's technology system is riddled with Chinese embedded back doors. Whether they can be activated is unknown, but if the Americans and Israelis can infiltrate the Iranian military's communications system with something like the "Flame" cyber-surveillance agent, who can be so arrogant as to believe that the Chinese cannot do the same, especially given the cry for more H-1B visas by U.S. employers who cannot find the skills they need among America's unemployed, and presumably are not just trying to avoid hiring more expensive American workers?

There has been an alarming rise in reports of cyber-espionage emanating from Chinese computers; we may already be living in a new era where there are no specific secrets. That is a frightening proposition, because the only defense against this sort of prying eyes is to make it impossible for anybody to know what they should be looking for. To achieve that condition the state must erect a massive system of obfuscation where only an elite understands what is going on. Sadly, that is where we are heading, and the super-PAC blizzard this fall will be a watershed moment for America, when the last vestiges of critical thinking and democratic decision-making disappear into "Strawberry Fields Forever," that prescient vision the Beatles probably never imagined would be about anything more than too much psychedelic drug use.

Given that before long, if not already, the Chinese can probably steal and replicate anything the Americans can invent, and theoretically can impose absolute export restrictions on critical metals, the "Pivot to Asia" at this point in time makes so much sense it is hard to imagine that the DOD actually thought of it. The primary threat to the smuggled supply on which the DOD relies resides in the possibility that China might expand its political footprint into the Australasian Triangle, which it could turn into a self-sufficient economic trading zone, provided it could replace its supply of Middle Eastern oil through development of the potential oil resource underlying the South China Sea (over which China claims jurisdiction despite competing claims from the surrounding ASEAN nations of southeast Asia). The Chinese threat is not that it will take over the world, but rather that it will expand the "hermit empire" to enclose a much larger part of the world that will not be available to the rest of the world for trade.

The provocative Pivot to Asia initiated by the Obama administration last year, which appears to be at the expense of an American commitment to the Middle East that doubled the defense budget during the Bush administrations, has the support of southeast Asia as well as Australia. The Pivot to Asia seems designed to serve as a containment strategy that keeps Chinese influence boxed within its mainland borders. It is no accident that shortly after Myanmar said no to the Chinese plan to dam the Irrawaddy River, the generals shifted their allegiance from China to the United States, and allowed Aung San Suu Kyi to emerge from house arrest to become a sanctioned political leader. Southeast Asia sees American capital investment a lesser evil than a creeping takeover by Chinese companies that ultimately are extensions of Beijing's Politburo which may not yet own China's wealth but, as the Bo Xilai example testifies, is determined to control wealth for some time yet.

During the past couple months the macroeconomic discourse has been about the slowdown in growth China is suffering, whose realness is very evident in the softness in rare earth and other critical metal demand I see reported daily in the Metal-Pages "news" reports. After the mild rebound for domestic prices in April, rare earth prices are descending again. The fear for the moment is that domestic rare earth prices are headed much lower later this year, to be followed by an all-out crash in FOB spot prices to historical levels where the premium above domestic prices reflects the export duty tax.

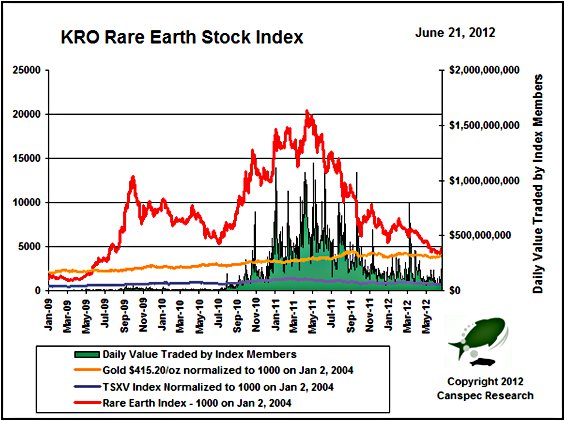

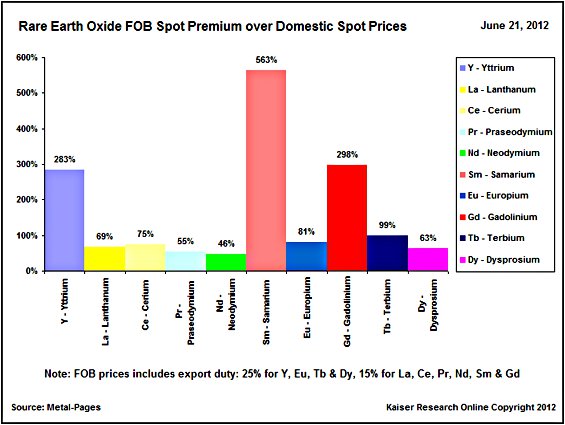

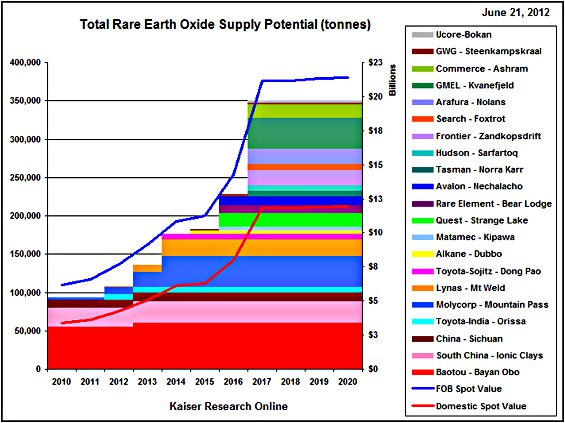

Anybody who knows anything about the rare earth sector pays no attention to the FOB spot prices, except perhaps Wall Street analysts who pumped up market interest by plugging FOB spot prices with laughably modest discounts into their Lynas- and Molycorp-discounted cash flow model-based valuations. The real questions are: Where will domestic prices stabilize, and what impact will the projected 60,000 tonnes of mainly light rare earth oxides from Molycorp and Lynas have on rare earth prices as FOB and domestic prices converge? (The chart below shows that the FOB premium over domestic spot is modest except in a few cases such as ytrrium, samarium and gadolinium.) At the moment nobody knows, though the Chinese state may have its internal targets of what are fair prices, which the White Paper seems to suggest may be somewhat higher than current levels. Given that all the major advanced rare earth projects that matter are either heading into the troublesome commissioning stage, during which joyful noise is rarely emitted, or into feasibility study stage pilot plant studies that cost much more and take longer than ever expected with results that inevitably amount to lower recoveries and higher costs, and the uncertainty about long-term rare earth prices, why did these stocks bounce today, and is this the start of a sustainable recovery?

I think the advanced rare earth juniors with meaningful supply potential (i.e. more than 5,000 tonnes per annum [tpa] output) will establish new bases above the recent lows, but I do not believe the conditions are in place for a sustainable uptrend. The Neo Material and Molycorp merger has closed, but before we can expect this to result in fresh leadership, their operations need to be integrated so that the market no longer sees the merger as a miner and a processor squashed together into a single company, and Molycorp needs to demonstrate that its new Mountain Pass operation will perform as expected. Bad news that neither of these is working will cast a fresh pall on the rest of the advanced rare earth juniors.

However, the White Paper is an important turning point for the rare earth juniors because it makes it very clear to the end-users who are unwilling to move their factories to China that a return to cheap, China-subsidized rare earth supply is over. Either they spend billions engineering technology solutions that avoid rare earths, or they figure out some way of investing billions in non-Chinese rare earth production that does not require them to own and operate the upstream portion of a supply chain whose middle portion contemporary business theory says must consist of laterally diversified independent competitors the end-user can pit against each other in order to secure the lowest possible price.

Ideally several of the major mining companies will conclude that rare earths are a long-term growth business which despite the custom chemical plants and quirky supply-demand dynamics of the market is worth getting involved in. Given the trend by large miners such as BHP Billiton and Rio Tinto to divest themselves of smaller business divisions such as diamonds and specialty metals, I am not inclined to hold my breath. Another alternative is that Molycorp and Lynas each grow into large, diversified producers of critical metals as well as downstream alloys and engineered products. Molycorp is on track toward this goal thanks to the Neo Material merger; if Lynas can get its LAMP plant in Malaysia operational, an obvious next step is to go beyond producing rare earth oxides as a commodity by acquiring the Rhodia rare earth division from the Belgian chemical company Solvay, which acquired the parent Rhodia in 2011. Another possibility is that Chinese rare earth companies acquire non-Chinese rare earth projects and put them into production; such developments are unlikely to meet with approval in the country, which hosts the rare earth deposit without conditions that force the Chinese company to sell the rare earth output to the highest bidder rather than sending it back to China for further downstream processing.

These are scenarios whose materialization the end-users do not control, so their long-term product deployment plans stay stuck in limbo. The option so far pursued by end-users is to seek one-sided off-take agreements with rare earth juniors that accomplish little more than to fill the heads of end-user management with delusions of cleverness while the shareholders of the rare earth junior react with disgust at the incompetence of the juniors' managementand the stupidity of the end-user in thinking the off-take agreement sets up anything other than a future train wreck that is unproductive for all parties. Within the next 12 months the end-users need to get serious, and possibly forge consortiums that collectively bankroll the development of major rare earth deposits with an eye to capital cost repayment and breakeven long-term operation, with the rare earth output auctioned off internally among the consortium members and surplus rare earths either stockpiled internally or sold into the open spot market for incidental users such as happens in the uranium sector. This type of arrangement will likely need advance approval from antitrust regulators. Fortunately China is offering a blueprint on how it plans to do this on behalf of Chinese end-users. And that may be why the White Paper has stirred the rare earth juniors into what may be more than a couple days of upticks.

The White Paper outlines the steps China has taken to consolidate and centralize control of its rare earth industry, implement an invoicing system to better document the production and flow of rare earth products and sharply reduce the downstream consequences of practices so unacceptable in the rest of the world. China has ended up supplying more than 90% of global rare earth production because for decades it tolerated such practices. China has had in place for decades an indirect subsidy of rare earth production that should have prompted the rest of the world to impose import duties or tariffs to bring Chinese rare earth prices up to the level it would have cost to produce those rare earths in their own countries. Needless to say, this never happened. The WTO complaint is in effect an assertion that as China stops its subsidies it should inflict on its own economy the same pain the rest of the world will suffer in terms of higher rare earth costs, and write off the suffering it absorbed while the rest of the world enjoyed the benefits of cheap rare earth prices. Suck it up China, is the message of the WTO complaint.

Americans have no moral leg to stand on in complaining about the actions China has taken. Americans and their other western compatriots have been parasites that have been happy to enjoy the benefits bestowed by cheap rare earths and are now whining that this free ride is ending. Most Americans do not understand that somebody else is paying for the cheap rare earths that have functionalized so many technologies they take for granted. But once they do, only a fragment will be so hypocritical or intellectually dishonest as to reject the legitimacy of what China is doing. In fact, there may be a surprising number who understand that not only is China doing what every American thinks is perfectly alright to do, namely pushing back against being used as somebody else's toilet, but in fact it is doing the rest of the world a favor by raising the domestic cost structure of rare earth production to be in line with the costs in the rest of the world.

The White Paper explicitly makes this point. China's concerns about the adequacy of its ion-adsorption clay rare earth deposits for its long-term needs, the primary source for heavy rare earth production, are legitimate. If the rest of the world fails to bring on stream light rare earth-dominated mine supply, China will probably laugh because that is a voluntary submission of dependency on China's light rare earth output. But China is quite eager to see full-spectrum rare earth deposits come on stream elsewhere in the world, because China can foresee that in the medium term it may need to become an importer of the heavy rare earths. In engineering a rise in rare earth prices which encourages the development of full spectrum rare earth deposits elsewhere in the world, China is not engaging in some sort of charitable action to enhance the common good on a global scale. China is making sure that somebody will finance into production a raw material which it will eventually need to import in order to feed its broader ambition of becoming a global economic powerhouse that runs on self-sufficient clean energy facilitated with clean technology.

The White Paper, in making China's goals explicit and pretty much rendering the WTO complaint a pipedream in terms of delivering satisfaction to the cost dumping complainers, may be pivotal in moving the end-users off the fence into actions that save the rare earth juniors from withering on the grapevine. If current domestic prices are the new long-term reality, and possibly higher if the Chinese so decide, then much of the production potential of the rare earth juniors that make up the KRO Rare Earth Stock Index are in the money at the cost structures described in their PEA, PFS and FS technical reports, even when I reduce the three most abundant rare earthslanthanum, cerium, and yttriumto zero value. Fine tuning and verifying the flow-sheets, along with the associated costs, is the main obstacle now facing these juniors, and they will need deep-pocketed help. The uptick that started on June 20, 2012 is only sustainable if we see evidence of such support from parties with a vested stake in rare earth security of supply.

As far as the worry about rare earth demand destruction happening as a result of heavy R&D expenditure, there are two types of innovation, only one of which destroys demand. The demand destroyer is substitution innovation where the same functionality is achieved through a solution that is much cheaper and relies on readily available inputs. Given the special properties of the lanthanides, such an innovation might be a Nobel prize candidate. Much higher success probability lies with efficiency innovation where the same functionality is achieved while using less of the critical input. Theoretically this should stabilize or even reduce demand growth, thus constituting "demand destruction," but Jevons Paradox argues that efficiency gains in consumption achieved through technological innovation actually boosts total consumption. So the win-win scenario here is that R&D into more efficient rare earth utilization reduces the physical amount of rare earths required, which brings down the total cost of the required rare earths at current prices, thus allowing commercialization of products to continue, while at the same time acceptance of the new post-subsidy rare earth price levels enables deposits to come on stream elsewhere in the world, ensuring an abundance of supply that gives end users the confidence to develop and commercialize new products that require rare earths in more efficient incremental units. China's White Paper has declared that higher prices are the new reality, and that it will continue to use them and invent more applications that require them. The rest of the world can either shut up and do without, or roll up its sleeves to bankroll non-Chinese rare earth production.

John Kaiser

Kaiser Research Online