This article is really about potential energy. The coming gold stock mania is gathering essential potential ahead of the most exciting capital growth opportunity we may witness in our lifetimes. As if this was not valuable enough, it will occur as other assets continue to devalue. This is the role of gold for investors in a crisis. For the banks it may well assist them to regain confidence once it is completely lost.

Before I get into this discussion, we need to check a number of factors. I need to begin with a basic and that is that there are a limited number of gold producers on a global basis. Investors will get crowded out of physical and there will be a scramble for gold stocks in all markets due to their rarity.

China remains the worlds number one gold producer however it is a net importer. This means that the growing production is not able to keep up with their growing demand. I have read this figure may be as high as an additional 400 tonnes of gold per annum, over and above the 360 tonnes produced on a per annum basis (as of last year). This reduces the annual global supply of gold back to circa 1,700 metric tonnes. The worlds next largest producer of gold is Australia with around 265 tonnes in each of 2010 and 2011. Australia does export gold and therefore it contributes to fresh global supply.

The Australian gold stock sector is therefore one of significant importance. I should qualify this statement to maintain integrity. It is true that several offshore majors are operating in Australia and they do contribute to that production figure. However the ASX producers (domiciled in Australia) also operate mines internationally and this offsets the adjustment. Newcrest is the major contributor to this however there are several more ASX listed gold companies with operations in Asia, Africa and even parts of Europe.

We have a special group of rapidly growing gold producers that should outperform the top heavy global producers which are struggling to maintain their resources. The special group of miners here are developing mines and growing production as they establish themselves for future benefit. Most of this group of stocks have seen their share prices fall as their operations have improved. The main irony however is that this fall in share price has occurred just when their incomes finally began to get well clear of their total cost.

This is occurring because gold has risen faster than their costs since late 2008. I have completed a study that looks closely at this and quantifies the anomaly. They represent stunning value and as gold rises again this increases exponentially. I have conducted independent research to quantify their relative value across this gold rally to date and the valuation levels in this sector against gold. Finally I added the main ingredient which is profitability. I have been able to simplify this into a single figure which has greatly pleased my accountant & other professional clients.

Before I go into this further, the points I want to discuss would be moot in isolation. One must consider the top down analysis to establish the likelihood of a continuation of the trend which might reverse the gold stock malaise we have endured as gold stock investors over the past 18 months.

Take Australia as an investment destination. We have a stable political system and I do expect the current minority government to be resolved in the final quarter next year at the upcoming election. Our politicians are fairly typical of their peers around the world unfortunately. When they are not spinning their agenda or bragging about the work actually done by the corporations and real work force they are making life harder for us not easier. I will not sit here and claim Australia is the ultimate destination due to our stable financial system; I would not want to insult anybody. It is comparatively acceptable however at this stage.

I believe I need to periodically test my overall thesis and investment strategy. This also involves constant attention to detail as I monitor the markets and signals I receive. It is nice to see elite Funds backing up my analysis on Australia. The likes of BlackRock and Van Eck have been, and by recent substantial holder reports, appear to continue to soak up extreme oversold levels in this gold sector. Good luck to them; for they are gradually positioning themselves in many of the same stocks I have represented in my Educational Portfolio at higher weighting levels.

Over recent months I have monitored gold and the gold stocks closely in relation to the ongoing global financial crisis. Back in April I produced Newsletter 55 for Members which investigated and quantified the relationship between the Australian gold sector and the Australian price of gold. This has been a continuing confusion for most investors. This relationship is very important because most of the domestic miners earn their returns here in Australia in our dollar (AUD).

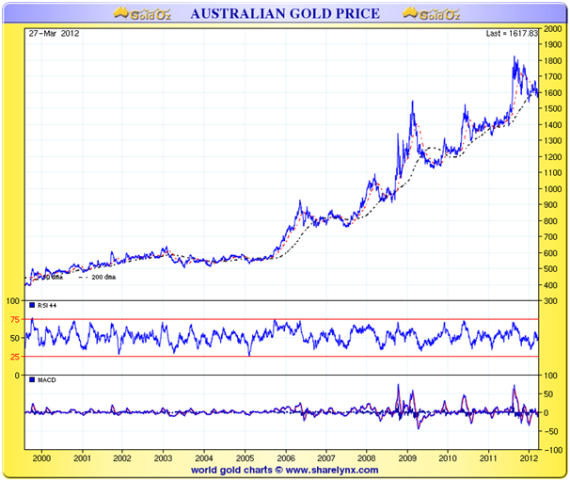

Speaking of the Aussie gold price here is a chart showing the magnificent uptrend.

Alpha is king

As you can see above the Australian gold sector is enjoying the strong AUD gold price. As the AUD falls the sector becomes cheaper for offshore investors especially in the USA. There is some downside risk, on the AUD (for US investors) at present due to a slowing China and troubles in our banking sector. Global funding issues are adding to the problems of the local banks, with their dilemma also due to falling real estate prices. I believe the RBA here will be forced to gradually lower their interest rate to support the banks here. This is not without consequences however the pressure has set in. As the AUD falls the gold stocks will enjoy a rising AUD gold price. This will increase their earnings and eventually this translates into alpha.

This is especially important in these economic times as alpha is king. Alpha is just a professional term for yield. Even despite the risk on the banking sector here at present we have decent yields in this sector which is holding up their share price. As the global investment community seeks to maintain their wealth in a deleveraging world they will flock to yield. This will be one of the more significant capital flows in the coming decade. Flows not chasing alpha will be seeking a safe haven which will require lack of counterparty risk.

I suggest investors take care to establish a model which can reliably factor risk on the sustainability of yield moving forward however. If yield is not sustainable in your chosen investment class, stand clear you may be looking at a top. Gold stocks however have an increasing yield and the potential for further gains going forward is highly favourable. Despite their growing earnings their share prices have been savaged in line with the rush to liquidity. This is the increasing potential energy I describe, potential capital growth.

Where is gold now?

I strongly believe that this gold consolidation phase is just that. It is yet another sideways movement to consolidate former gains and to gather energy for a new up-leg. I have read some talk that even physical gold is a risk asset which is quite ludicrous for the simple reason that is has no sovereign or counter party risk. The real reason it sold off in risk off events of the past few months was related to liquidity. This same phenomenon was last seen in the 2008 bank crisis however it passed quickly. Gold bottomed just seven months after the March 2008 high. In this consolidation phase gold has made a new bottom (triple) nine months after the recent high. Gold and equities sell off first because they are liquid. Capital flees (initially) towards the USD and bond market because they are liquid.

QE to be or not to be has become a trigger mechanism for gold price movements during this consolidation phase and yet M2 growth remains at +10% growth post QE2. Therefore this whole argument makes no sense either. We have argued that ultra-low interest rates are a form of stimulus and could also be considered to be a form of QE. This is all about the adjustment to a low growth world after a long debt binge which grew to unsustainable levels. This created the banking crisis which then shifts to a sovereign debt crisis as the banks are bailed out by governments. The stimulus is an attempt to maintain the status quo and slow deflation.

Interest rates will remain low (negative real interest rates) and other assets will continue to come off. Instability and volatility will remain in the global financial system in the coming years. No wonder gold is tracking at this new higher price plateau. In this environment gold will eventually continue on its uptrend.

This will cause the gold stocks to become more profitable over time. The gold price consolidation is gradually drawing to an end which is the very reason the large Funds are accumulating. They cannot get set too quickly or they force prices higher in the process. The northern hemisphere summer could see a firming of the gold price as Europe simmers. The bond yields are blowing out on Spain and Italy at this time. The chances are that we either get a massive QE sovereign bond purchase here or we get a disaster. Both outcomes would be highly gold positive.

From a technical perspective we hit a triple low, with the last low divided and clumped into three dips during May with a buy divergence. This has since seen a bounce on June 1st with an $80 range, straight up hitting a falling Bollinger Band (I use 20 day, 2 standard deviations). The minor correction that followed stabilized at the 20dma and now we have started a longer bounce rising up towards a now rising top Bollinger Band. This is a bullish pattern. I will leave the timing of the coming break out to other commentators however my guess would coincide with the end of the northern hemisphere holidays based on the monthly patterns and general gold market. For now I am expecting the gold price to firm up a little and consolidate a little higher or print a false break out ahead of the real event. Those of us watching this from the start have seen it all before.

How undervalued?

Now to the quantity of undervaluation I promised you above in the title and opening paragraph. The following is part of Newsletter 55 from April this year.

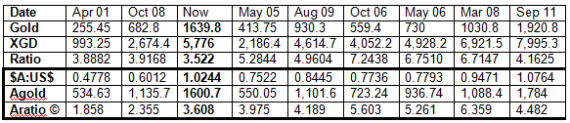

At the end of April 2001 gold traded at US$255.45 when the XGD was just 993.25 at a ratio of 3.8882. This was at the end of a 20 year bear market and only marginally below the low reached in the 2008 melt down. In effect the 2008 low retraced the entire bull market in gold stocks going back 7 years (at the time) and this is understandable; by 2008 the cost of production had risen significantly across the industry. What I am saying is that with gold at those extreme lows in 2008 it was equivalent to a gold price of $255 in margin terms due to the rising cost of gold production over those 7 years.

This is not the full transcript however I followed up with this: Now what about an update are we there yet? I have added some new calculations and research below and slotted the key readings in to appropriate positions for easier comparison. This may not be clear without some careful reading however I urge you to take some time as it will provide clarity on your position or future decisions.

Ratio (line 4 above) is simply the XGD (Australian gold index) divided by the USD gold price. I have used the XGD extremes (low and high) and the gold price at that time for each column. The next line down (running across) is the AUD: USD ratio each measurement. Agold is the next line; it is simply the AUD price of gold for that time. The bottom line is the AUD adjusted Ratio figure which actually adjusts each figure to the AUD price of gold. This is essential to make sense of the AUD gold price as earnings of the sector are controlled by that number. I have copyrighted the Aratio© number as it is part of a more important number. A bit more from the Newsletter to clarify my thoughts:

The top three rows of data are simplified numbers so I have added the three lower rows inside the box. The margin on gold at US$255 in 2001 was deplorable for the global industry however the AUD: USD ratio at the time meant that in AUD terms our gold producers were earning A$534 per ounce. This did not mean Aussie gold stocks were in favour however. The deep pessimism from investors caused them to overlook this sector but who could blame them it was 2001.

I was finally able to make sense of the 2008 panic low which, once adjusted came in under the current level and above the pre-rally launch date in 2001 as it should. After all the rally was 7 years on, sentiment had changed towards gold, it was awake at last. Yet at the time the end of the world was apparently close. The sky was burning and we were about to head back to the caves if you believed the hype at the time. Markets had been in free-fall for months. Before the adjustment for the AUD it appeared that the GFC low was as bad as the pre-2001 gold launch, and that this low right now was below both.

Before the beginning (2001) the Aratio was at 1.858 that was after 20 years of bear market and as you would expect this should be the lowest point for the ratio. The adjusted 2008 figure makes more sense at 2.355. Now as we head under the earlier lowest sentiment induced ratio lows of 4 (May 2005 and August 2009 columns) we have to consider that a low may be close. As you can see above we now have a simplified number to indicate value in the market for this sector.

Another important observation when you look at the figures:

What I do find interesting is that when I use the Fx exchange rate to filter the levels achieved by the XGD in the lower box in this table above we even out the result. Look at the tops in the XGD in terms of the Aratio: May 06 = 5.261, March 2008 = 6.359, November 2010 = 6.04 and April 2011 = 5.946. They were all quite similar and this gives us a more reliable frame of reference to measure tops from. A level of around 6 should indicate a danger of a correction and stops and / or that caution will need to be used. NOTE: When the eventual mania arrives this figure will keep rising and trailing stops along with an exit strategy will need to be used.

The September 2011 high in gold at US$1920.8 did not see a follow through rally on the stocks which drastically underperformed the metal. This statement still applies when you factor the AUD price of gold to create the XGD ÷ AUD$gold = the Aratio©. At this stage of the rally the gold stocks and the Aratio achieved, were very poor, barely reaching 4.482. Since then gold corrected and the gold stocks have followed it down even faster, this cannot last long. This leads us along a path as this picture is still not quite complete (again from the Newsletter):

Something missing here?

There is another important factor left out of this research train of thought however; and that is cost of production. We have to be careful to get this right or we could end up comparing apples to oranges. Therefore to complete this line of reasoning we have to consider the profitability factor. Cash costs are confusing across the industry because they are not standard. Royalties and other factors vary from company to company and lease to lease.

To be continued next week

Good trading / investing.

Neil Charnock

www.goldoz.com.au

GoldOz has now introduced a major point of difference to many services. We offer a Newsletter, data base and gold stock comparison tools plus special interest files on gold companies and investment topics. We have expertise in debt markets and gold equities which gives us a strong edge as independent analysts and market commentators. GoldOz also has free access area on the history of gold, links to Australian gold stocks and miners plus many other resources.

Neil Charnock is not a registered investment advisor. He is an experienced private investor who, in addition to his essay publication offerings, has now assembled a highly experienced panel to assist in the presentation of various research information services. The opinions and statements made in the above publication are the result of extensive research and are believed to be accurate and from reliable sources. The contents are his current opinion only, further more conditions may cause these opinions to change without notice. The insights herein published are made solely for international and educational purposes. The contents in this publication are not to be construed as solicitation or recommendation to be used for formulation of investment decisions in any type of market whatsoever. WARNING share market investment or speculation is a high risk activity. Investors enter such activity at their own risk and must conduct their own due diligence to research and verify all aspects of any investment decision, if necessary seeking competent professional assistance.