The Gold Report: While the NYSE Arca Gold BUGS Index (HUI) is up a bit from its May low, it is still lagging the price of gold and not living up to expectations based on the role it has traditionally played as a safe haven for investors. Are we close to a turning point in that dynamic?

Quinton Hennigh: Many investors and speculators are deservedly frustrated and dejected by the recent performance of gold and, more specifically, the gold mining sector. For many of us in this business these ups and downs are the norm, however, I see the current down as a critical one. Something is going to happen. It could be a month, six months, a year or two years from now. We can't know. We may continue to see more pain in junior stocks until then, but a change is coming, and investors should take heed.

My views regarding the cycles in the world of gold mining crystallized during the time I had the privilege of working for Newmont Mining Corp. (NEM:NYSE) while Pierre Lassonde was president. His views on the Dow:gold ratio and what it says about megacycles in the economy and the gold mining sector (detailed in his book The Gold Book, The Complete Investment Guide to Precious Metals) made sense of what I was seeing in the markets and major mining companies' corporate strategies.

TGR: Where are we in the cycle now?

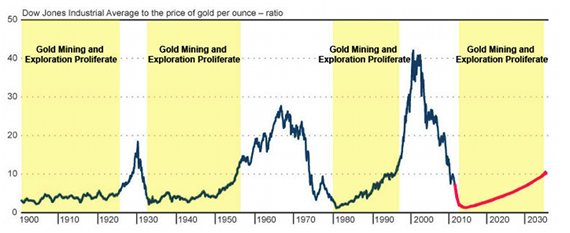

QH: Below is a chart of the Dow:gold ratio over the past 112 years. The peaks generally mark points when the Dow was running hot and gold was in the dumper. Conversely, troughs mark times when gold was riding high and the Dow was down. I have added a few interpretations to the chart. First, I projected this chart forward 25 years with a red line that I believe reflects a pattern that we are likely to experience, given a look back at history. Note that the red line bottoms out as the chart did in 1932 and 1980 and then slowly rises over the subsequent 25 years.

(Figure 1: Dow to gold ratio from 1900 to present and projected to 2035. Vibrant periods in the gold mining and exploration sector are highlighted in yellow.)

Second, yellow shading has been added to highlight periods when gold mining and exploration were generally more vibrant than other times.

TGR: How do you define more vibrant times for gold miners?

QH: This is a bit subjective, but I see these as times when gold mines often made consistent money, the public felt comfortable investing in this sector and perhaps most important, exploration was well-funded, thus contributing to a plethora of great discoveries.

TGR: Why wouldn't gold mining and exploration proliferate as the price of gold rises and the Dow:gold ratio falls?

QH: At first glance, this pattern does appear counterintuitive. When the Dow is down, uncertainty and doubt rule as they do now. We are still climbing the "wall of worry" and that does not aid investment in possible future rewards.

Vibrant periods in the gold world appear to commence around peak gold prices and persist as gold slides downhill. Answers to this conundrum can actually be seen in the world around us right now. The gold mining world is presently experiencing ever increasing capital costs, unpredictable and almost universally high cost of production, and other uncertainties, such as increasing taxes and royalties in countries eager to take advantage of the rising gold price. It is not a comfortable time to invest in this sector.

TGR: So, when will that change?

QH: I do not profess to be an economist, nor do I know when this pivot point, the bottoming of the Dow:gold ratio, will happen or at what level. I simply see this pattern as rather compelling. In fact, it is so simple even a geologist can understand it.

TGR: How can investors capitalize on these trends?

QH: Mining and exploration trundle along during the "white" periods, but it is during the "yellow" times that things are really hopping. These are times when the "gold rush" mentality is alive; geologists are scouring new frontiers for fresh finds and big discoveries are made, one after another. During the period from 1980 through 1997, for example, there was a succession of world-class gold discoveries: Hemlo (15 million ounces (Moz)), Goldstrike (60 Moz), Pipeline (12 Moz), Yanacocha (35 Moz), Pierina (9 Moz) and Busang, the ultimate bubble top. These were discoveries that "made" companies.

Many investors scored huge returns on explorers that struck it big. Investments in majors also paid off. Believe it or not, Newmont was around $5/share in 1983 and hit around $55/share in 1996. Many other people made fortunes as Barrick Gold Corp. (ABX:TSX; ABX:NYSE) moved to the forefront of major gold producers.

Looking back to the gold rush period from the 1930s through the 1950s, huge discoveries were made in the Witwatersrand of South Africa as well as numerous gold camps across the Canadian Shield. Again, these were discoveries that "made" companies. An investment in Homestake Mining in 1929 would have returned 600% by the late 1930s, the height of the Great Depression.

Looking still further back at the cycle that extended from the late 1800s through the early 1920s, gold rushes abounded in the western U.S., Australia, Canada, Africa and beyond. Great gold producers such as Homestake, Gold Fields Ltd. (GFI:NYSE) and Anglo American Plc (AAUK:NASDAQ) made investors fortunes during this boom.

TGR: Are many of these companies still around?

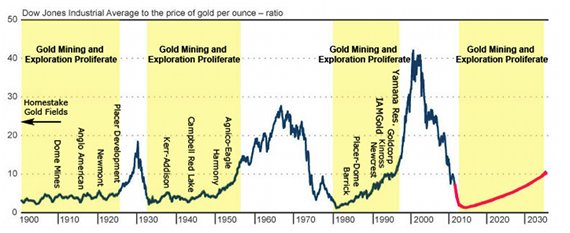

QH: The chart below adds the names of many major gold producers at the point they were founded. Not surprisingly, most major gold producers have roots in these "gold rush" periods. Although there were miners that found their start during the "white" periods, most of these are no longer around, likely because they were gobbled up in the subsequent frenzy. It will be interesting to see what happens to up-and-coming producers like Osisko Mining Corp. (OSK:TSX), Alamos Gold Inc. (AGI:TSX), and Allied Nevada Gold Corp. (ANV:TSX; ANV:NYSE.A) over the next few yearsdo they get bought or survive through acquisitions?

(Figure 2: Dow to gold ratio from 1900 to present and projected to 2035. Vibrant periods in the gold mining and exploration sector are highlighted in yellow. Major gold producers are listed at the point that they were founded.)

TGR: What comes next?

QH: If the next few years play out as I think, we could be approaching a pivot point, one that ushers in the next gold rush. Given current market conditions this may sound crazy, but we could soon see a massive inflow of money similar to what occurred when gold last peaked.

Such a capital influx will likely accompany a sharp run-up in gold prices. Euphoria over gold, although likely short-lived, will pull in speculative money fleeing other sectors that are losing value. This influx of money will likely feed the next cycle of discoveries and acquisitions as it did in the early 1980s.

Again, I don 't know when this pivot point might occur. It could be a month from now, six months, a year or two years. The significance of the cycles is that legitimately profitable deposits will be highly sought after as we roll into the next "up" cycle for gold acquisitions and exploration.

Some 2,000 junior exploration companies are struggling to survive right now. They universally claim to be cheap and in possession of stellar projects. Some actually are cheap and a few do own above average projects. It is our conviction here at Exploration Insights that the few companies holding exceptional properties and deposits will outperform the general junior market and be the target of larger mining company growth strategy. It is our intention to own some of these.

TGR: How can an individual investor know which companies are worth owning?

QH: We need to be positioned for this turnaround; specifically we need to understand what a major company is after and how it makes its acquisition decisions. This is something both Brent Cook and I are experienced with and have been involved in while working for major mining companies. There is much more to it than a good drill hole or reading a third party preliminary economic assessment. The resource has to be evaluated in the context of mining, operating and capital costs. Furthermore, location, existing infrastructure, jurisdiction, sociopolitical realities and environmental issues need to be factored into the price a major can afford to pay for a mineral deposit. But rest assured, if history is any guide, a turnaround is coming.

TGR: Thank you for your insights.

Dr. Quinton Hennigh recently joined Exploration Insights where he provides geological expertise reviewing companies, projects and activity in the junior mining space. He began his career as an economic geologist with large mining companies including Newmont Mining Corp., Newcrest Mining, and Homestake Mining where for fifteen years, he managed exploration projects in North America, Europe, Australia, Asia, and South America. In 2007, he joined the junior gold sector where he has held executive and advisory roles at Gold Canyon Resources, Novo Resources Corporation, Euromax Resources, Prosperity Goldfields and Evolving Gold Corp. He earned a Master of Science degree and a Ph.D in geology and geochemistry from the Colorado School of Mines in 1993 and 1996, respectively.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

1. The following companies mentioned in the interview are sponsors of The Gold Report: Gold Fields Ltd., Allied Nevada Gold Corp. Streetwise Reports does not accept stock in exchange for services. Stories are edited for clarity.

2. Quinton Hennigh: I personally and/or my family own shares of the following companies mentioned in this interview: None. I personally and/or my family am paid by the following companies mentioned in this interview: None. I was not paid by Streetwise for participating in this story.