For many years now gold and silver by its pattern of following gold wherever it goes have been treated by traders, investors and central banks as a 'counter to the U.S. dollar' and quite rightly so; this definition, however, applies primarily to the long-term value of the dollar and not simply to the daily gyrations of the dollar's exchange rate.

For many months now, gold and silver have not simply acted as a counter to the dollar but linked on a day-to-day basis with the euro. It's reasonable, one would think, for them to have that relationship because the euro is the second most important currency in the world. But when the euro itself has problems with its value then the relationship must surely become suspect?

What we've seen lately is gold and silver prices moving with (and often faster, both ways) than the euro, but the link remain solid. With concern for the future gold and silver prices in mind, it's time to examine this relationship to see where it's taking these precious metals. With the Eurozone crisis moving to potential 'runs' on Greek and Spanish banks, the future of the euro is now on the line. A look at a precipitous fall in the euro and the potential for gold and silver to follow is warranted. Investors should be prepared for very volatile and surprising gold and silver price moves.

Meaning of 'Counter to the Dollar'

It would have been better had the saying included currencies in general. With gold respected worldwide as alternative money to currencies, the presence of the two in national gold and foreign exchange reserves enabled the balance of changing values in the two to allow the net value to remain relatively constant. As the gold and silver prices fell against currencies, so the value of currencies rose. Central bankers hold these reserves to ensure that a nation has reserves with which to continue trading internationally in the event of a national disaster preventing international dealing by the state. The maintenance of their value in all weathers is a fundamental necessity.

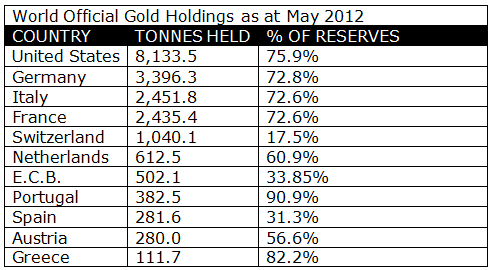

With the U.S. dollar being around 63% of global reserves, it's appropriate for European nations to hold gold in large quantities. The table below shows the percentages that the developed world holds as a percentage of their reserves:

The gold holding will only have significance when the financial weather turns very stormy, not on a day-to-day basis. That's why when central bankers buy, they are relatively price insensitive. Their target is to acquire volumes of gold because it's that volume or the number of ounces that counts when push comes to shove. When they buy they simply accept direct offers of gold that the market makes to them. Chasing prices is out. The long-term steady acquisition of ounces and tonnes is the objective. A look at the figures in this table again highlights what we mean in a market that supplies only around 4,400 tonnes a year. Of this 36% is recycled gold, which can prove a heavy variable. Another 700 tonnes never leaves its country of origin. Thus the daily gold price depends upon less than half of the annual gold supply reaching the international gold market. So central banks are cautious, price insensitive buyers.

As we have seen in the market place, traders mainly have been linking the euro to the gold price's moves. There's a danger that readers of this article and subscribers will think it right to make decisions on the basis of the moves in the euro against the dollar only. To do so from now on may be the wrong moves.

Tied to the Euro?

The Eurozone crisis has seen remarkably little change in the €: $ exchange rate considering the extent of the sovereign debt crisis inside the Eurozone. Its peak was at €1: $1.40 and its low today at €1: $1.2550. This is only a move of 10%. Much of this narrow range of movement has to do with the swap arrangements between the Federal Reserve and the European Central Bank who have actively 'managed' the exchange rate to ensure as much stability as they can. If it had been left entirely to market forces, the picture would have been very different.

If a financial panic ensues in the Eurozone's banks, it's possible that we see the euro fall back to its start point around €1: $1. Will the gold price follow it down? Take a look at the second table below and see what happens to gold if it follows the euro.

Let's take the current gold price of $1,560 as the start point for the projections and move the gold price with the decline of the euro.

Please note that it's the euro that's falling alongside all those currencies that look to the Eurozone as their key trading partner and to whose currency they are determined to adhere in a tight trading band (by interference if necessary). This does not reflect U.S. dollar strength; the dollar has been steady against other currencies and will likely remain so.

Before we answer the question, 'Will gold follow the euro down?' it's good to ask what the gold prices have been in both the euro and the dollar over the last decade.

In 2005 the gold price in the U.S. dollar was around $300 and around €240.

Today we see the gold price in the U.S. dollar at $1,560 or over five times higher than it was then. As to the euro price the same multiplier of over five times is true again at €1,244.52.

So our dilemma is that traders who have been driving the gold price of late will attempt to move the gold price with the euro's fall. Will investors from other nations follow suit?

To answer this we have to look closely at other buyers using other currencies. USD investors look at their dollar based Technical analysis and project price patterns in the dollar gold and silver price.

With somewhere close to 60% of the world's gold demand coming from China and India, we must recognize that those investors look at the gold price in the Indian Rupee and the Chinese Yuan.

The Chinese government wants their people to buy gold so are not happy to see the Yuan appreciate, or see their own people's gold investments suffer losses in the Yuan.

In India, the scene is different the Rupee has been very weak, having fallen over the last year from Rs.42: $1 to Rs.56: $1 a fall of 33%. Accordingly gold prices in the Rupee have risen as the dollar gold price has fallen.

Right now, Indian demand is weak, being supplied mainly by sales of locally held gold, suffocating gold imports, so Indian demand is almost absent from the international market, at the moment. This leaves the weight of demand on Central banks and the Chinese with developed world demand at present lows.

This gives traders the reins over the gold prices on a daily basis but for how long and at what price?

Indian gold investors are very price conscious. Their buying pattern is to wait for a floor to be established so that when they buy, they won't see prices fall afterwards. They believe that the gold price in the Rupee will go up after that. They are not so wise, yet, to see that the Rupee's value is not likely to increase, bringing Rupee gold prices down. All they see are Rupee prices rising, as the Rupee falls.

What we will see if the above table is seen in the next few weeks is the gold price in the dollar falling faster than Rupee gold prices are rising. This will give the appearance of a Rupee 'floor' price and they will enter the market and support Chinese and central bank buying.

If the Reserve Bank of India does succeed in halting the fall of the Rupee this probability will happen faster. If they succeed in strengthening the Rupee by 'managing' (i.e. interfering in the forces driving the Rupee) it then Rupee gold prices will fall. That will bring out Indian buyers for sure.

Member's only:

Where will gold prices go in the next few days and weeks?

Get the rest of the article. Subscribe @

www.GoldForecaster.com / www.SilverForecaster.com

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina, have based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina make no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina only and are subject to change without notice. Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina assume no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.

Julian Phillips

Gold Forecaster