Recent angst among analysts, pundits, mavens, gurus, savants, wizards and other assorted talking heads has China plummeting toward a "hard landing." These views in combination with the ongoing and never-ending worry over the euro, the currency without a country, have weighed heavily on the entire resource market since the first of May.

Oil, gold and copper, the world's benchmark energy and metal commodities, have shed roughly 10% of their unit values this month. Most experts have adopted a very bearish outlook to the point of jumping on the doom and gloom bandwagon and have not considered these drops as simple market corrections.

Not I, sayeth The Mercenary Geologist. My current opinion is best illustrated by the 2011 supply and demand fundamentals of Dr. Copper, Ph.D. Economics:

- Mine supply: 16 million (M) tonnes of copper.

- World production: 19.7M tonnes of copper, including secondary refined scrap.

- World usage: 22.1M tonnes, including recycled scrap.

Ergo, we used 6.1M more tonnes of copper than we mined last year.

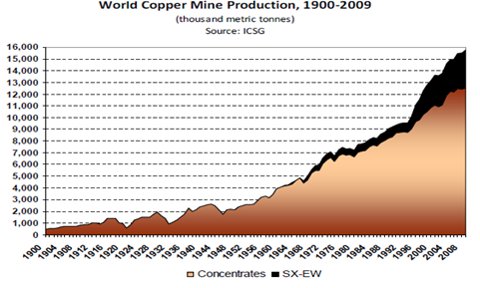

This chart shows the annualized 4% growth of copper supply since the widespread advent of electricity in industrialized countries starting in 1900. The steeper growth curve beginning in the mid-1990s can be attributed to emerging market countries, mainly in Asia, demanding electricity for their massive populations. Also note the increasing role of cheaply processed oxide copper by acid leach, solvent extraction, and electrowinning versus concentrated and refined sulfide copper:

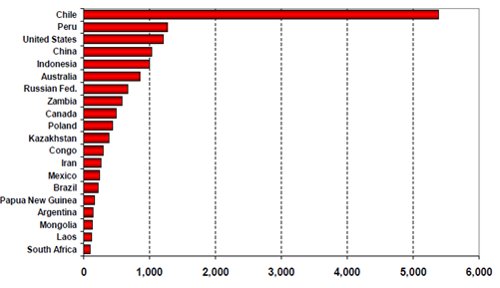

World copper production was dominated by Chile and the United States for several decades. Chilean mines still supply about 35% and the U.S. remains a large producer, but increasing contributions have come from Peru, China and Indonesia over the past two decades. Zambia and the Congo have the world's richest copper deposits; however, geopolitical problems continue to severely hamper mine development in southern Africa:

World Copper Mine Production (000s Tonnes) Source: ICSG

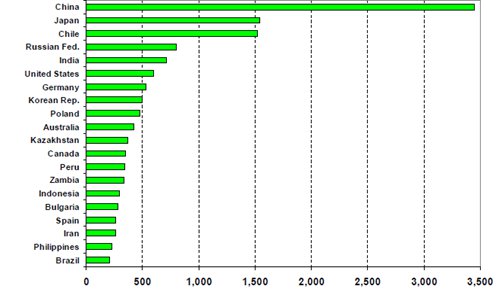

There was a significant shift in the location of copper refineries to Asia beginning in the 1980s as aging smelters were retired in the United States and its domestic production became dominated by oxide copper deposits. Especially noteworthy has been the steadily increasing capacity of China, now refining over twice the sulfide copper of its closest competitors, Japan and Chile:

World Primary Copper Refinery Production (000s Tonnes) Source: ICSG

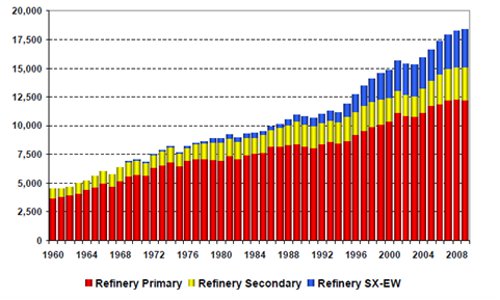

Breakdown of total refined copper production illustrates steady growth and the increasing roles of oxide copper and refined scrap since the mid-1970s:

World Total Refined Copper Production (000s Tonnes) Source: ICSG

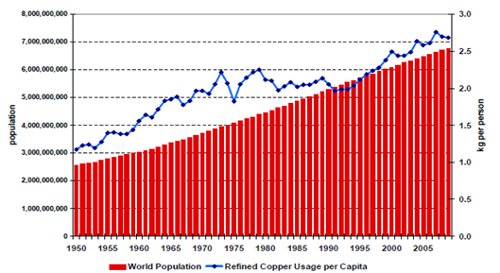

World demand for copper is closely correlated to population growth. Rising GDPs and demand from emerging market countries, mainly the BIICs (Brazil, India, Indonesia and China) are significant contributors to the rapid growth in world per capita use since the mid-1990s:

Source: ICSG

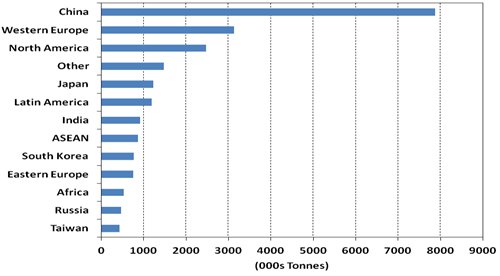

Here's a breakdown by country of the 22.1M tonnes of copper used in 2009. Note that the Chinese used 36% of world demand, and that was only slightly less copper per year (7.9M tonnes) than the Americas, Europe and Japan combined (8.0M tonnes):

2009 Copper Usage Source: ICGS

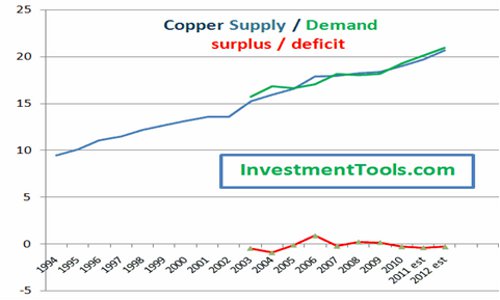

Over the past four years copper has been in a delicate supply and demand balance:

Copper Production, Consumption and Balance in Millions of Tonnes

World mine production accounted for about 16.5M tonnes of copper in 2011. Folks, that's a whole lotta love for the red metal. However, as often pointed out by fellow geo-analyst Brent Cook, it's only slightly less than what has come out of this big hole in the ground over the past 150 years:

Bingham Canyon Copper Mine, Ophir Mountains, Utah

For those unfamiliar, Bingham Canyon has produced continuously since 1863 and became the world's first large-scale, open-pit copper mine in1906. It is mankind's largest excavation at 1.2 kilometers (km) deep and 4.0 km wide and is visible with the naked eye from outer space.

Over this humongous mine's lifetime, it has produced 17.5M tonnes of copper, 26M ounces (oz) of gold, 220Moz of silver, and over 1.1 billion pounds of molybdenum. The value of its extracted resources exceeds those of the California, Comstock Lode and Klondike gold rushes combined. Immense reserves and resources are known both below and surrounding the current open-pit mine and are sufficient for operations to continue for many more decades.

The world is using about one Bingham Canyon worth of copper every year. Our demand budget has to be replaced every year by new prospects discovered, deposits found, reserves proven, and mines developed. This is indeed a formidable task as I discussed earlier this year (Mercenary Musing, January 30, 2012), because most of the easily exploited surface deposits of copper were discovered long ago.

For many decades now, explorationists have employed indirect surface geology clues, subsurface geophysics, geochemical and biochemical sampling, and remote sensing to target and discover new economic deposits of copper that do not crop out. The increased in exploration over the past eight years has resulted in discovery of major new resources. However, geopolitical instability, government bureaucracy, environmental opposition, permitting delays, and threats of nationalization have produced long lead times to development and mining, hindering primary market supply.

Geologists and engineers are not finding, developing, and mining enough copper to meet the historically validated projections of 4% demand growth year over year. The world uses 5 to 6M more tonnes of copper than it mines every year. This steadily growing shortfall has been offset by refining of secondary supplies and recently, significant recycling of old scrap.

All the above data and charts emphasize the current dominance of world copper markets by China. It is apparent that if the Chinese economy tanks, you can throw my analysis out the door for the short- to mid-term.

However, I take a longer-term and perhaps contrarian view, largely because copper is essential to transmit electricity. According to Scientific American, 130 years after Thomas Edison invented the light bulb, 25% of the world's population (i.e., 1.7 billion people) still grope in the dark without it.

Most of the world's future demand increases will come from the rapidly growing middle classes in BIIC countries, which desire electricity and modern conveniences that we consider essential in the developed world.

So shy of a complete global economic meltdown or a catastrophic natural disaster, long-term supply and demand fundamentals remain strong and that certainly bodes well for a robust and healthy Dr. Copper.

Viva el cobre!

Ciao for now,

Mickey Fulp

The Mercenary Geologist

Acknowledgement: Erin Ostrom is the editor of MercenaryGeologist.com. I thank Mark Turner for thoughtful comments.

The Mercenary Geologist Michael S. "Mickey" Fulp is a Certified Professional Geologist with a bachelor's degree in earth sciences with honors from the University of Tulsa, and master's degree in geology from the University of New Mexico. Fulp has over 30 years experience as an exploration geologist searching for economic deposits of base and precious metals, industrial minerals, uranium, coal, oil and gas, and water in North and South America, Europe and Asia.

Fulp has worked for junior explorers, major mining companies, private companies and investors as a consulting economic geologist for the past 24 years, specializing in geological mapping, property evaluation and business development. In addition to Fulp's professional credentials and experience, he is high-altitude proficient, and is bilingual in English and Spanish. From 2003 to 2006, he made four outcrop ore discoveries in Peru, Nevada, Chile and British Columbia. Fulp is well-known and highly respected throughout the mining and exploration community due to his ongoing work as an analyst, writer, and speaker. Contact: [email protected]

Disclaimer: I am not a certified financial analyst, broker, or professional qualified to offer investment advice. Nothing in a report, commentary, this website, interview, and other content constitutes or can be construed as investment advice or an offer or solicitation to buy or sell stock. Information is obtained from research of public documents and content available on the company's website, regulatory filings, various stock exchange websites, and stock information services, through discussions with company representatives, agents, other professionals and investors, and field visits. While the information is believed to be accurate and reliable, it is not guaranteed or implied to be so. The information may not be complete or correct; it is provided in good faith but without any legal responsibility or obligation to provide future updates. I accept no responsibility, or assume any liability, whatsoever, for any direct, indirect or consequential loss arising from the use of the information. The information contained in a report, commentary, this website, interview, and other content is subject to change without notice, may become outdated, and will not be updated. A report, commentary, this website, interview, and other content reflect my personal opinions and views and nothing more. All content of this website is subject to international copyright protection and no part or portion of this website, report, commentary, interview, and other content may be altered, reproduced, copied, emailed, faxed, or distributed in any form without the express written consent of Michael S. (Mickey) Fulp, Mercenary Geologist.com LLC.

Copyright © 2012 MercenaryGeologist.com. LLC All Rights Reserved.