The Gold Report: The U.S. Geological Survey's (USGS') Mineral Commodity Summaries (MCS) 2012 describes world mine production and reserves by country. What are the biggest changes from last year?

Micheal George: There weren't a lot of big changes other than replacing reserves that were mined during the previous year. The largest changes were Australia increasing reserves by 100 tons (t) and Canada decreasing reserves by 70 t. The reason behind Canada's decrease was the closure of mines due to exhausting mineable reserves. Australia's increase was due to adding new mines to its potentially active mine list.

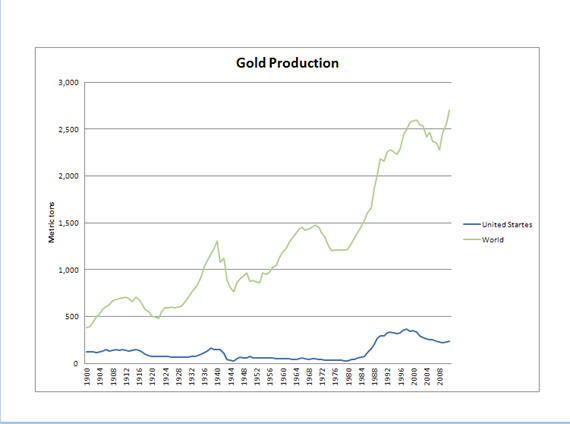

Annual world mine production increased approximately 5% in 2011. It was the third year in a row of an increase in production and marked an all-time high for gold produced since recorded history. Compared to the recent low in 2008, production is up about 19% or 440 t. So it's recovered quite a bit.

TGR: What are the reasons for higher gold production? Is it simply because the gold price was higher?

MG: The gold price was higher, so more mines are processing, and they're pushing out more gold. A lot of it is coming from China right now. Quite a bit of gold is coming from other countries as well.

TGR: Are mining companies replacing reserves through exploration or acquisition?

MG: Both. Nowadays, a lot of the additional reserves have been coming from exploration, mainly around the deposits that are currently being mined.

TGR: How does the USGS estimate reserves for this report?

MG: Reserve estimates are calculated by the government in each country in the report. For example, the Australian government or Canadian government does research and revises reserve numbers and that is what we use in the report. The USGS also researches public company reserve reporting. Sometimes we use company published reserves if we know all of the companies in a country. For example in Papua New Guinea, all the mining companies are publicly traded, so they all have to report their reserves.

TGR: How about production and reserve numbers from China?

MG: The production numbers are straight from the Chinese government. I don't think it has updated countrywide reserves in the last couple of years. If it has, we don't have a new number from it.

TGR: Are you saying the change in gold price and increase in production over the last year hasn't materially changed the reported gold reserves in China?

MG: In our publication, yes, China's reserves have not changed too much mainly because we don't have any new reports out that have updated reserves or that Chinese miners have just basically replaced what they've mined out in recent years. Reserves are a moving target. It's constantly changing based on price, based on technology, based on a whole host of factors.

TGR: At these prices, are we running out of gold? In the energy sector, we hear about "peak oil." We don't really hear about "peak gold." Is there such a thing?

MG: "Peak gold" doesn't really work as a theory. There have been several historical "peaks" in gold production. There was a peak in U.S. gold prior to World War II in 1938 at 161 t. Production then dropped during the war because of a shift to wartime materials. Gold production trended downward until the 1970s because of low gold prices. After a sudden increase in gold prices in the 1980s, a rush to find new gold deposits led to the discovery of additional deposits in the Carlin trend area in Nevada. The Carlin mine had been operating since the 1960s, mining these massive, low-grade deposits. At that time, USGS geologists were out there and investigating these deposits. The U.S. Bureau of Mines helped develop the process of cyanide heap leaching, which, in turn, allowed the low-grade deposits to be economically developed. That caused a substantial increase in U.S. gold production. By 1998, we hit another high of U.S. gold production at 366 t. But at the time, the price of gold was at a historical low. By 2002, the price started to increase and has steadily increased through today. The persistent high gold price has led to increased production in 2010 and 2011, with new mines coming on-line and existing mines expanding operations. Continued exploration spurred by the high gold price has led to numerous discoveries, some of which have quite a bit of reserves, such as on the Cortez trend. There is a mine that just started up a couple of years ago that has a huge reserve right now. The world follows a similar pattern as the U.S., with multiple peaks in production over time.

In this way, gold is unlike oil, which is a consumed material. Gold is unique in that it's an investment, not merely a commodity. Because of its value, gold is rarely ever consumed in a traditional sense. It's nearly indestructible, and it's nearly completely recycled. I think the only gold use I found that isn't recycled is in spacecrafts. This means that an increase in demand may not be solely met by new supply. It could be met by scrap supply. It also takes decades for gold production to respond to price movements because of the time lag it takes from deposit discovery to production. It could take decades for a mine to start up. Also, when gold prices are low, production generally plateaus and may decline, owing to a lower rate of return on investment. At the same time, exploration for new deposits is minimal because companies need to reduce their expenses and they don't go looking for new deposits. That's what happened in the 1990s and early 2000s. There were historically low levels of exploration, so we had this time lag of about 10 years. Now, we're seeing the gold price affecting production and causing production to go up where we didn't see that a couple of years ago.

TGR: Is there a similar situation on the supply side where it takes decades or a long period of time to create sustained demand? Perhaps demand in China is an example?

MG: Not necessarily because demand can really bounce around quite a bit. You have a huge pool of recycled material sitting out there. So if the price gets high enough, people are willing to give up their gold.

TGR: Comparing gold to oil again, one meaning of "peak oil" is that we are running out of cheap and easily obtained oil. Now there's a lot of oil, but it's expensive to get to. Is there a similar situation for gold? As long as the price is high, people are going to look for it, but is it becoming more and more expensive to find, mine and process?

MG: Only when you compare dollars to dollars. Yes, it is more expensive to look for gold now than it was previously, but not significantly. If you put inflation factors on it, exploration and production costs have not risen nearly as much as for oil. However, when the price of gold goes up dramatically, companies will mine lower grade deposits. So if the gold price drops significantly, then ore grade would actually go up. Right now, miners evaluate deposits based on where the deposit ends or where the pit wall is going to be. The mine gets bigger as the price goes up, and the mine gets smaller as the price goes down. With a lower gold price, they are going after higher-grade deposits. But with a high price, they are going after as much ore as they can produce that is profitable.

TGR: You also mentioned that as the price of gold goes up, spending on gold exploration goes up. The 2010 Minerals Yearbook just came out. It says that gold was the primary mineral exploration target with more than 50% of the world's non-ferrous exploration budget of $5.4 billion, 59% more than in 2009. Do you see that trend continuing?

MG: Yes. That trend has continued from 2011. It has gone up again, and gold is still more than 50% of the targeted materials.

TGR: What is the next most popular mineral for exploration?

MG: Probably copper. It gets a little fuzzy because miners may be going after copper porphyry, but copper porphyry also has gold in it. But it's probably copper.

TGR: Is the nature of the mining industry still cyclical?

MG: Yes, it's just how mining is. There are boom and bust periods. The successful companies are able to spread out their risks more than others. They're making huge profits right now to make up for huge losses coming up. Mining is one of the few industries where the companies know they're going to have a big loss coming up eventually. The industry is cyclical. Gold prices go up, gold prices come down. In mining, they have to balance out the really good years with the really bad years. Hopefully the gains and losses offset and the companies make a profit over 30 or 40 years.

TGR: A large component of domestic gold supply listed in the MCS was imports of ore and concentrates from Mexico. How do those fit into the market?

MG: That is cross-border refining. Mexico doesn't have enough refining capacity to refine its own ore so it is sent across the border, sometimes by the same company owning both properties in the U.S. and in Mexico. Ore is sent to the U.S. to be further refined into either dore or bullion to be sold on the market. Sometimes, refined ore will be shipped to another country, say, Switzerland, where it's further refined into bullion, which enters into the London market to be sold.

TGR: Let's dig a little more into the recycling market. Last year, the U.S. had 225 t of gold recycled. That was approximately equal to the domestic mine supply.

MG: Yes. Regarding scrap, the price is driving people to give up their gold. Television commercials for buying gold air every day, and that's essentially what's driving the market. People are parting with their gold jewelry that they don't want anymore.

TGR: But for every buyer, there's a seller. So who's driving the demand side?

MG: Investment is driving the demand side, especially worldwide investors. Across the board, even in the U.S., people are investing in gold as a safe haven. They don't want to invest in the dollar or the euro because they aren't doing so well. So they find something else that is gaining value and that gives them a good rate of return but also has the liquidity in that they can sell it anytime, anywhere. Even if the world economy collapsed, gold would be valued by somebody somewhere.

TGR: Is this individual investors or central banks or both?

MG: Both. Central banks have historically been sellers on the market until 2010. Now they are buyers. The sellers are traditionally the European banks, and now we're seeing buyers from non-European banks.

TGR: What about institutional investors?

MG: Oh, yes, they're buying gold, too. Everyone from Joe Public to the Russian Central Bank and Chinese Central Bank is buying gold. Everyone is buying gold for investment.

TGR: We hear a lot about emerging geographies for gold exploration and mining. What about Africa? What are the largest producing countries in Africa?

MG: Africa as a continent is one of the largest gold producers, and it has more reserves than most of the other areas because it's underdeveloped right now. I just got some new numbers that show this year the third largest producer in Africa is Tanzania. Mali, which is now number four, went up, but Tanzania went up by more. Their numbers are pretty close to each other, so they probably will flop back and forth. They both have several large mines owned by multinational companies, so they're pretty stable owners. However, they won't catch up to South Africa any time soon.

TGR: South Africa is still number one?

MG: South Africa is number one, but it's falling just because of its age. Its mines are so much older, so much deeper and so much more complex. It's also been having labor issues. Across the board, costs have gone up. Everything is underground, and there are some mines that are two miles underground.

TGR: What country is number two in Africa?

MG: Number two is Ghana. Ghana is almost double Tanzania and Mali. South Africa is another 100 t above Ghana. So there's still room. No one is going to catch South Africa right away. It will take years.

TGR: And how is the U.S. doing?

MG: U.S. production is increasing. It increased again last year a little bit.

TGR: According to your report, annual production is approximately 230 t?

MG: It's been about that for a while. Some of the larger mines are aging so they're showing some drops in production. It can be hard to get new mines started in the U.S. The U.S. has several world-class deposits that are either in lawsuits or just having difficulties getting permitted.

There is a lot of gold up in Alaska that is untouched. There are a lot of areas in Alaska that are untouched for exploration also. Nevada still has quite a few deposits that are not developed that can come on-line soon. As I said, Cortez came on a couple of years ago, and now it's a huge mine.

TGR: Are there other areas in the U.S. that might contribute to gold production in the future? North Carolina has seen some activity during this cycle.

MG: North Carolina is an interesting area. It's all on private land. Mining companies own the land, so they don't have to worry about permitting like out West, where they have to permit through the Bureau of Land Management or the Bureau of Reclamation. They just have to get their permits through state agencies. It's a little easier that way. The deposits are different, the gold is locked up in quartz and greenschist, which is a little harder material to work with, but it can produce gold. There is one project that's far ahead of everybody else, and then there are a couple that are still in the early phases.

TGR: What is the project that is most advanced?

MG: The Haile mine from Romarco Minerals Inc. (R:TSX).

TGR: Can you explain what your group at the USGS does? Do you promote mineral development in the U.S.?

MG: We are like a warehouse of information. A company could call me up and ask questions about what has happened in the past and why the price has gone up in the last few years. It could ask me questions, but we don't do anything to directly promote mineral development.

We produce the MCS, which gives a quick glance at what's going on today in the gold industry. The larger, more detailed Yearbook gives more of an overview of what happened during that year so you can see where development and production took place. It provides insight into why production was flat per se or why exploration has gone up. It gives a good basis to understand the industry during the past year.

TGR: Thank you for your insights.

The most up-to-date documents referenced in this interview can be accessed here.

Micheal George is a mineral commodity specialist at the U.S. Geological Survey, where he serves as the principal contact for mineral commodity data and information, and as a referral source for business and industry representatives, foreign representatives, the general public and other agencies. George has also served as an economist for the Mineral Management Service and a researcher in the U.S. Bureau of Mines. George holds a Bachelor of Science degree in mineral economics from Pennsylvania State University and a master's degree in cartographic and geographic sciences from George Mason University.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

1) Alec Gimurtu of The Gold Report conducted this interview. He personally and/or his family own shares of the following companies mentioned in this interview: Romarco Minerals Inc.

2) The following companies mentioned in the interview are sponsors of The Gold Report: None. Streetwise Reports does not accept stock in exchange for services. Interviews are edited for clarity.

3) Micheal George: I personally and/or my family own shares of the following companies mentioned in this interview: None. I personally and/or my family am paid by the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this story.