To many, the Federal Reserve and its monetary policies seem mysterious and ill-defined. How do they decide on a policy that sees the necessity for near-zero interest rates for the next two years? What exactly is in their crystal ball?

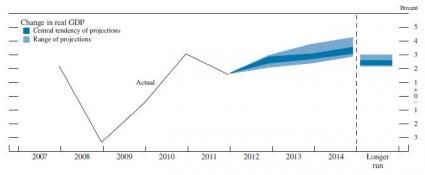

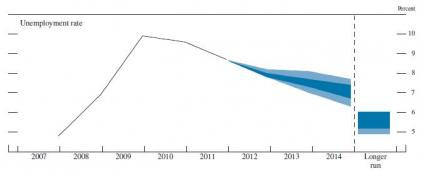

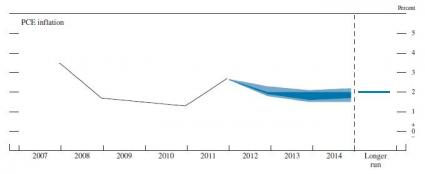

One thing the Bernanke Fed has done well to provide clarity and prevent confusion is to publish the economic projections of the FOMC members along with post-meeting statements, usually on a quarterly basis. In a few PDF pages, we get simple charts and tables on three important areas of forecast: GDP, unemployment and inflation.

Seeing What the FOMC Sees

Looking at these three charts helps us see what the world's most important economists are using as decision metrics for setting interest rates and proposing, or opposing, more quantitative easing.

I won't try to interpret these charts too much, as they practically speak for themselves. They appear on page 2 of a 5-page PDF on the FederalReserve.gov website and are titled "Central tendencies and ranges of economic projections, 2012-14 and over the longer run." The PDF is tricky to find, and so I assume most people don't ever see it. That's why I think it's important to share.

Okay, I know I said I wouldn't interpret, but I can't help it. Allow me to summarize what the FOMC sees in its own forecasts that makes it lean as a policy-setting body toward keeping interest rates very accommodative for nearly two more years:

First, most members see GDP struggling to get above 3% in the next two years.

Second, while they see unemployment falling below 8%, they don't see it picking up momentum to carry it below 7% very soon.

Third, despite what common sense might seem to dictate in an era of extraordinary accommodation (QE), inflation is forecasted to stay below 2% for quite a while. This is the Bernanke gambit that deflation is the far worse evil and that it is far better to tempt too much inflation than too little.

This last point is certainly the most controversial. Some might say that the Fed has a conflict of interest here. While they want to backstop the economy and the stock market, they don't want to acknowledge that they could actually be fanning the flames of an inflation wildfire.

The next few years will certainly be the most interesting in terms of the evolution and impact of Fed policy. We can definitely say that the Bernanke Fed is winning the war against deflation. But we have no idea what things will look like three years from now in terms of inflation.

Fed footnotes to graphs:

1. The central tendency excludes the three highest and three lowest projections for each variable in each year.

2. The range for a variable in a given year includes all participants projections, from lowest to highest, for that variable in that year.

3. Longer-run projections for core PCE inflation are not collected.

A Very Positive Twist

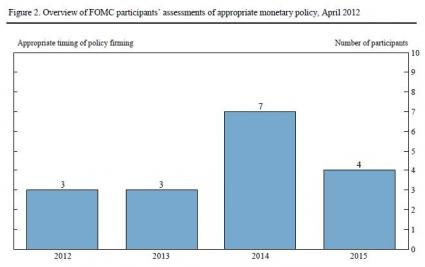

Market participants expecting more QE this week, or some extension of Operation Twist, were sorely disappointed. They should not have been surprised though because this Fed is very good at telegraphing its views, intentions, and actions.

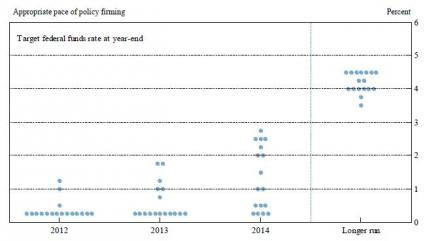

What this Fed does surprise us with is more and more transparency. Starting this year, they began showing where the FOMC voting was spread out in terms of the policy decisions. Below are the graphs included in the PDF.

Diversity and Debate

In the fall of 2011, I started to note the "dissent" on the FOMC from certain members who were becoming more hawkish. I thought this was great news, but not because I was eager to see rates rise and prevent inflation. I agree with current Fed policy that beating deflation is still the major battle.

The dissent and debate is good because it means our best economic minds are hard at work crunching the data and arguing amongst themselves about where we stand. True, there may be PhD-size egos involved as well. But we want this debate happening at this time and we want to know as much about it as we can.

One way to keep informed is to read all the speeches of all the Fed Board Members and Bank Presidents, whether they are FOMC voting members or not. That's a lot of work in some weeks where there might be a half-dozen speaking. But, contrary to simple opinion, it's not just Ben Bernanke's show and we need to understand how the other economists at the most important bank in the world think.

The only thing the Fed could do now for more transparency is put the names of the voters on each forecast and policy firming stance. The FOMC will always stand in the light of sharp criticism. But why should Ben take all the heat?

I think he should get a lot of credit for pushing policy to its current extremes, especially when we needed it in 2008 and 2009, and in 2010 and 2011 when we needed it maintained. And now the other members will become ever more important as we can realistically start looking for the QE exits. . .at least a year from now, anyway.

Kevin Cook is a Senior Stock Strategist with Zacks.com