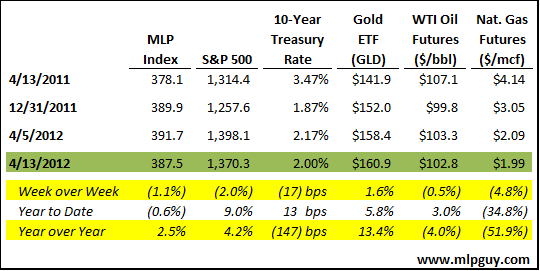

Happy distribution announcement season! So far 8 MLPs and 1 GP have announced their distributions for the 1st quarter 2012. 6 out of 8 MLPs increased distributions, with average distribution growth of 2.3% quarter over quarter. All of that equity and capex from last year should start to bear fruit in the next few quarters, and lead to a strong year of distribution growth overall. As that growth becomes more evident, I expect MLPs to narrow the very wide performance gap between the MLP Index and S&P 500. This week may have been the start of that comeback by MLPs. MLPs were down ONLY 1.1% this week, compared with 2.0% for the S&P 500. MLPs are still slightly negative on a YTD basis, compared with 9.0% for the S&P 500.

A sharp decline in the 10-year interest rate helped MLPs outperform this week. The 10-year closed at 2.0% this week, and it may test the year to date low of 1.8%. If that happens, it will be the result of some crisis in Europe, or the result of a series of bad economic data from China or the U.S. If that were the case, stocks would likely struggle, and MLPs would come back into favor as a high yielding defensive investment with the tailwinds of a secular growth industry: domestic energy production.

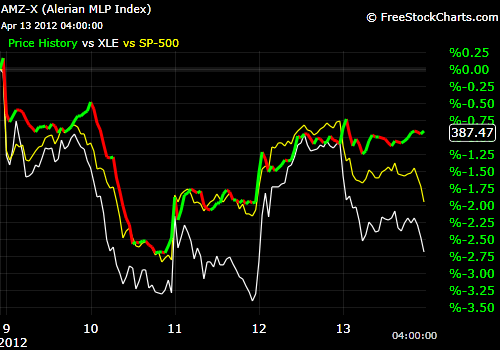

Speaking of domestic energy production, natural gas hit fresh lows this week, closing the week under $2.00 per mmbtu. Fresh lows for natural gas prices translated to fresh annual highs for the companies that are poised to most directly benefit, such as $LNG (up 7.4% Friday) and $TNH (up 12.3% for the week). Generally, energy stocks lagged this week, as represented by $XLE in the chart below. The S&P 500 was down for the second straight week. MLPs very closely mirrored the S&P 500 until the S&P 500 broke lower Friday and MLPs held flat.

So, the markets look fairly bleak, but there are pockets of good performance within the energy industry and within the MLP sector. The key appears to be resisting the temptation to fall into MLP value traps. No matter how attractive the relative valuation of EROC, APL and BWP look, they will break your heart in the absence of a natural gas price uplift, which is not coming soon. I own EROC and APL, so I am guilty of this as well, which is a result of my instinct to be wary of obvious trends and what everyone thinks they know.

But for now, liquids-focused MLPs (I am considering crude oil a liquid here) are still your best bet, but the trick is to find liquids-focused MLPs at a good price. Best time to find those reasonably-priced, liquids-focused MLPs is either (1) during times like this when the market pushes everything down, (2) after an equity offering or (3) a combination of both. Also, as you will read below, all of the M&A activity these days is rich-gas, NGL or crude focused. Liquids remain the story that works, no matter how cheap dry gas focused MLPs look.

News of the (MLP) World

Enterprise Products, Anadarko Petroleum and DCP Midstream LLC announce new NGL pipeline (press release):

- 435 mile NGL pipeline from DJ Basin in Colorado to Skellytown, TX

- Each party will own 1/3rd of the JV

- Pipeline will be called Front Range Pipeline

- Initial capacity expected to be 150 mbpd, with potential to expand to 230 mbpd

- Expected to be in service in 4Q 2013

- Volumes anchored by NGL volumes produced from facilities owned by APC and DCP Midstream

- Related story: DCP Midstream Partners Acquires 10% Stake in Texas Express Pipeline from EPD for $85 million (press release).

QR Energy Equity Offering (press release)

- Combination primary and secondary offering

- Priced at $19.18, 9.5% yield

- 6.2mm primary units sold for $119M

- 11.3mm units sold by Quantum, $217M in gross proceeds to Quantum

- Quantum still holds around $460M in QRE equity in the form of preferred and subordinated units

Penn Virginia Resource Partners announces acquisition of Chief Gathering LLC for $1.0 billion (press release)

- Marcellus assets

- By Year end 2013, midstream business unit will account for 75% of PVRs EBITDA, up from 40% today

- $1.0 billion purchase price will be funded with combination of cash and $200M in special units that dont pay distributions until conversion in 6 quarters

- $800 million cash portion will be funded with:

- $400M in units of new class of PVR Class B Units that pay distributions in the form of more Class B Units until conversion in 8 quarters. Riverstone is the purchaser of these units

- $180M private placement of common units to Kayne Anderson and Magnetar Capital

- $220M senior unsecured bridge facility, although PVR plans to issue term debt rather than draw on this facility

- Transaction expected to generate around $154 to $167 million in 2014, or a 6.0x to 6.5x EBITDA multiple

- Assets include 6 gathering systems, with 100% fee-based contracts

ONEOK Partners to build 1,300 mile Bakken to Cushing crude pipeline (press release)

- Will invest $1.5 to $1.8 billion between today and 2015

- 1,300 mile crude oil pipeline with 200,000 bpd capacity extending from Bakken Shale to the Cushing, OK crude hub

Disclosure: The information in this article is not meant to be financial advice, I am not your financial advisor and I am posting my comments for informational purposes only. Long EPD, OKS, APL, EROC.

Hinds Howard, MLP HINDSight